Structured Settlement Payments and What the IRS Actually Taxes

Structured settlement payments taxable? IRC Section 104(a)(2) excludes most — but selling triggers a 40% excise under IRC 5891. Here’s the IRS test that controls your answer.

In This Article

Are structured settlement payments taxable?

Under IRC Section 104(a)(2), most structured settlement payments received for physical personal injury or illness are excluded from federal gross income — they are not taxable.

Two categories are always fully taxable regardless of the underlying claim: punitive damages and accrued interest earned on delayed settlement payments.

Why the IRS tax answer depends on one critical distinction

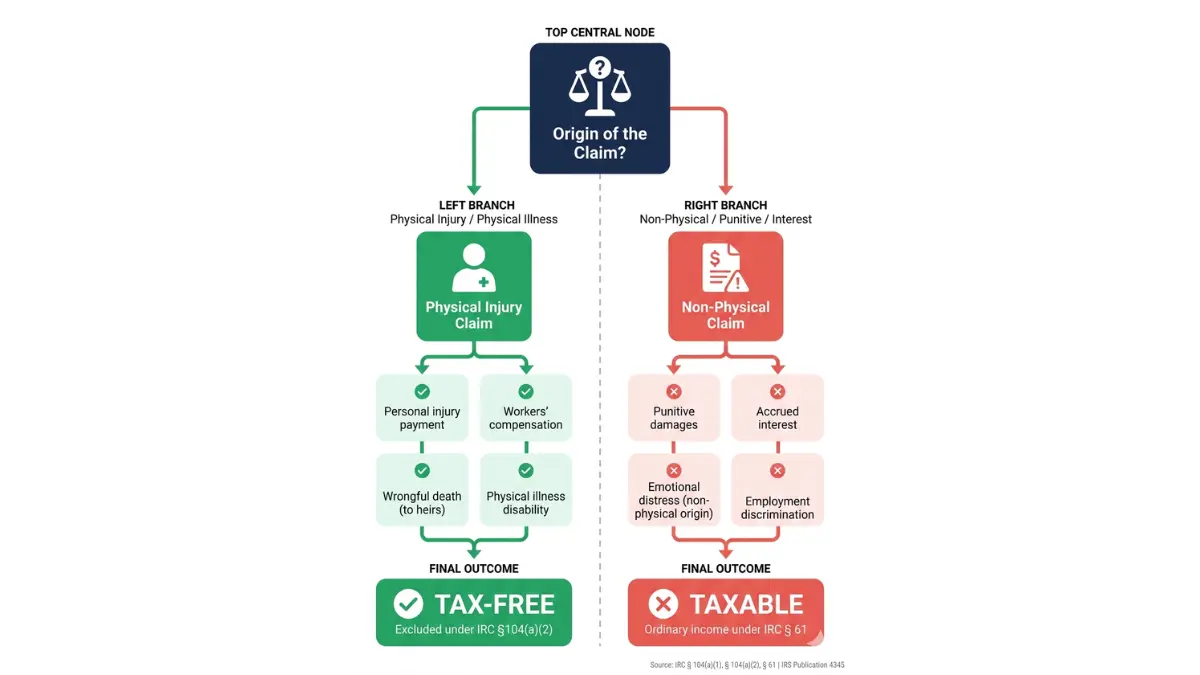

The IRS does not tax the label on your settlement document — it taxes the nature of the harm that generated the award.

That standard, called the “origin of the claim” doctrine, is the only legal test that determines whether your payments qualify for exclusion under IRS Publication 4345. If your payments originate from a physical injury or physical illness, the exclusion almost certainly applies; if they include punitive damages, accrued interest, or compensation for non-physical harm, a taxable portion exists and must be reported. Use our income tax calculator to estimate any taxable liability before your filing deadline.

What this guide covers: every settlement type and its tax status

This guide delivers a settlement-type-by-type tax breakdown, the factoring transaction tax risk most guides ignore, and the state and SSI interaction details that drive more reader exit behavior than any other gap in competing content.

Every section contains a specific IRS citation, a real-dollar or threshold figure, and a contextually specific disclaimer — not boilerplate.

ℹ️ Disclaimer: The tax treatment of structured settlement payments is governed by IRC Section 104 and IRS Publication 4345. Individual outcomes depend on the nature of your underlying claim, your settlement agreement language, and applicable state law. Consult a CPA or tax attorney before making any filing decision based on this guide.

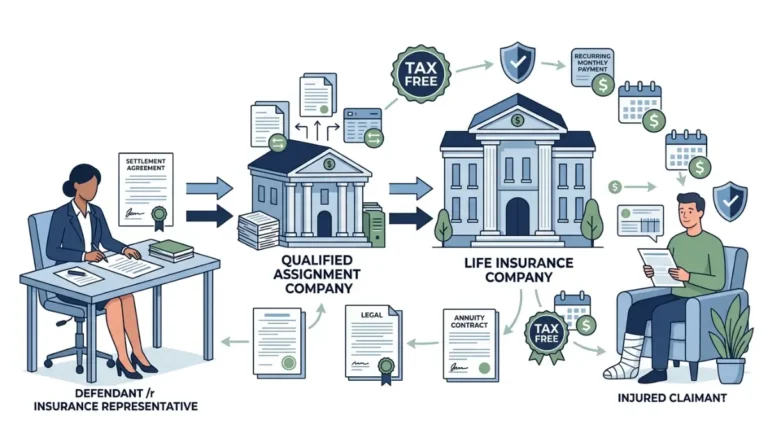

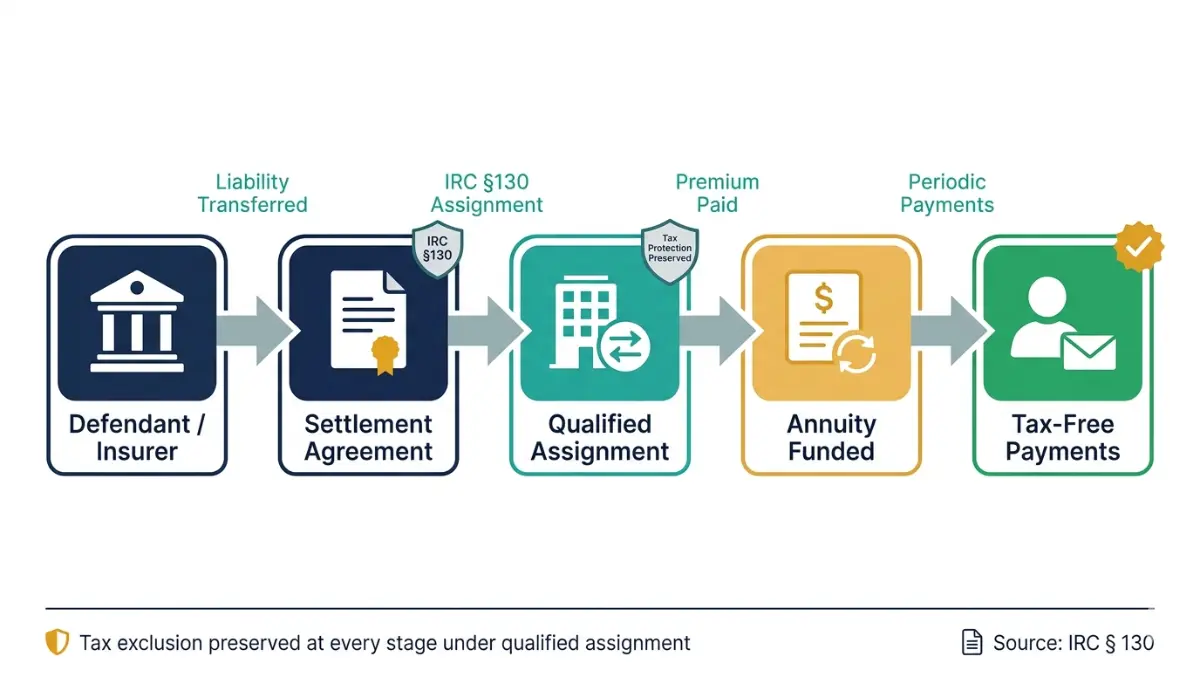

How structured settlements work and why the IRS treats them differently

A structured settlement is a negotiated financial arrangement in which a claimant resolves a legal claim in exchange for periodic payments — typically funded through a structured settlement annuity purchased by the defendant’s insurer.

The mechanics of how structured settlements are funded and what they pay explain why Congress granted them a tax exclusion most income sources do not receive.

What is a structured settlement? The IRS definition that matters

A structured settlement annuity is purchased through a process called a qualified assignment, governed by IRC Section 130. That assignment legally isolates the payment stream from the defendant’s estate — which is what prevents the IRS from treating the full settlement value as income received in the year of agreement.

In practice, the annuity functions like a fixed-income annuity in a financial plan, but with a legal carve-out most instruments do not receive. Use our savings calculator to model how your periodic payment stream accumulates over time compared to a discounted lump sum.

Why qualified assignments preserve your tax exclusion under IRC 104

Because the claimant cannot demand early lump-sum access to the payment stream, the IRS does not treat the full settlement value as constructive receipt of income.

That inability to access funds is the structural mechanism behind the IRC Section 104 exclusion — and it is exactly why recipients who sell their payments to a factoring company lose that protection. Wrongful death beneficiaries managing parallel life insurance proceeds can use our life insurance calculator to understand the combined financial picture.

IRS Publication 4345: the document governing all settlement taxation

The IRS defines which settlement proceeds are excluded from gross income in IRS Publication 4345 on lawsuit settlement taxability — the primary government reference for every settlement type addressed in this guide.

Settlement recipients should read this document before filing, and bring it to any CPA consultation.

ℹ️ Disclaimer: IRS Publication 4345 is the governing document for settlement taxability. Individual tax circumstances vary. A CPA review is recommended before making any filing decision.

Which structured settlement payments are taxable — and which are not

The settlement agreement you signed does not determine your tax liability.

The IRS does — using the physical injury test, regardless of how the defendant’s attorneys labeled each component of the award.

Tax-free structured settlement payments: the complete IRS list

The IRS excludes the following structured settlement payment types from your gross income:

- Payments for physical personal injury or physical sickness — excluded under IRC Section 104(a)(2); the claim must originate from physical harm

- Workers’ compensation payments — excluded under IRC Section 104(a)(1); see our full workers’ compensation guide for benefit interaction details

- Wrongful death settlement payments to heirs — excluded under IRC Section 104(c); the punitive damage component remains fully taxable

- Disability income arising from a physical condition — excluded under IRC Section 104(a)(1)

- Medical expense reimbursements tied to a physical injury — excluded under IRC Section 104(a)(2)

Use our percentage calculator to calculate what share of a mixed settlement award is tax-free when the agreement contains multiple damage components.

Taxable settlement payments: punitive damages, interest, and more

Punitive damages are fully taxable as ordinary income under any structured settlement — the U.S. Supreme Court confirmed this in O’Gilvie v. United States (1996), regardless of whether the underlying claim involved physical injury.

Accrued interest on delayed payment is taxable as interest income. Employment discrimination and wrongful termination settlements are taxable in full because they do not originate from physical harm. Review the 2026 income tax brackets to understand which marginal rate applies to your taxable settlement portion.

The physical injury test: the only IRS standard that matters

💡 Expert Note (CFA): In 28 years of advising clients who receive settlement proceeds, the most expensive mistake I have seen is trusting the settlement document’s language over the IRS’s physical injury test. A settlement agreement that labels an award “compensatory” does not make it tax-free — only the nature of the underlying harm determines exclusion eligibility under IRC 104(a)(2). I have reviewed client situations where this misunderstanding triggered five-figure IRS notices that a single CPA consultation would have prevented.

The IRS applies one test: did the payment originate from a physical personal injury or physical sickness? If yes, the exclusion applies. If the settlement is silent on the origin of harm, the IRS defaults to taxable treatment.

Emotional distress and discrimination settlements: why they’re different

Emotional distress damages are tax-free only when they are a direct consequence of a physical injury — and the settlement agreement must establish that connection explicitly.

Employment discrimination, defamation, and contract breach settlement payments do not qualify for the physical injury exclusion — 100% of those payments are taxable as ordinary income. Use our capital gains tax calculator if any taxable settlement proceeds are subsequently reinvested and generate investment returns.

| Settlement Type | IRS Tax Treatment | Governing IRC Section | Key Condition |

|---|---|---|---|

| Physical personal injury | Tax-free | 104(a)(2) | Must originate from physical harm |

| Workers’ compensation | Tax-free | 104(a)(1) | Must be workers’ comp claim |

| Wrongful death (to heirs) | Tax-free | 104(c) | Heirs only; punitive portion taxable |

| Punitive damages | Fully taxable | 61 | No exclusion — O’Gilvie (1996) |

| Accrued interest | Fully taxable | 61 | Taxable as interest income |

| Emotional distress (physical origin) | Tax-free | 104(a)(2) | Must trace directly to physical injury |

| Emotional distress (non-physical) | Fully taxable | 61 | Origin-of-claim test fails |

| Employment discrimination | Fully taxable | 61 | No physical injury exclusion available |

Source: IRS Publication 4345, IRC Sections 61, 104(a)(1), 104(a)(2), 104(c); O’Gilvie v. United States, 519 U.S. 79 (1996)

ℹ️ Disclaimer: The table above reflects general IRS rules as of May 2026. Settlement tax treatment is fact-specific and depends on the exact language of your settlement agreement, the nature of the underlying claim, and applicable state law. A CPA or tax attorney review is required before making any filing determination. Do not rely on the settlement payer’s characterization alone.

How to determine if your structured settlement payments are taxable

If you received a settlement payment and you are not certain whether any portion is taxable, the process below will get you to a defensible answer — or confirm when a CPA is the only path forward.

Step 1: Review your settlement agreement for damage classification

Locate the section of your settlement agreement that identifies each category of damages — physical injury compensation, punitive damages, and interest components should each be listed separately.

If the agreement does not separate these components, the IRS will apply the most unfavorable interpretation. Settlement recipients who receive a single undifferentiated amount are at the highest risk of incorrect tax reporting.

Step 2: Identify which payment components the IRS treats as taxable

Apply the physical injury test to each component: does it compensate for physical harm?

Physical injury and illness compensation → tax-free. Punitive damages → fully taxable. Accrued interest → taxable as interest income. Non-physical emotional distress → taxable as ordinary income. Use our take-home pay calculator to model your net after-tax income once you have identified the taxable portion, and our paycheck calculator to compare it against wage income from the same period.

Step 3: Determine whether you received a Form 1099-R or 1099-MISC

Form 1099-R is issued when a structured settlement annuity makes a payment that the annuity issuer has characterized as having a taxable component — Box 2a shows the taxable amount.

Review our complete guide to 1099 form types, deadlines, and penalties before assuming Box 2a is accurate. Annuity issuers occasionally misclassify mixed-component settlements, and a CPA must verify the figure before you report it. Use our salary calculator or hourly to salary calculator if you are cross-referencing taxable settlement income against earned wages to understand your combined adjusted gross income.

Step 4: Consult a CPA — and when professional review is non-negotiable

A CPA review is non-negotiable in four specific situations: your settlement includes both tax-free and taxable components in a single payment stream; you received a 1099-R you did not expect; your settlement agreement does not separately characterize each damage type; or any component involves emotional distress without an explicit physical injury connection.

✅ Pro Tip: Before your CPA appointment, use our adjusted gross income guide to understand how any taxable settlement amount interacts with Line 11 of Form 1040, and our 2026 tax brackets calculator to estimate which marginal rate applies to the taxable portion. Arriving informed cuts CPA consultation time — and fees — significantly.

ℹ️ Disclaimer: This four-step process reflects general IRS guidance as of May 2026. Individual reporting requirements depend on settlement structure, state law, and current IRS guidance. Do not make filing decisions based solely on this guide — a licensed CPA is the appropriate professional for settlement tax reporting verification.

Tax consequences of selling your structured settlement payments

⚠️ Warning: Selling structured settlement payments through a factoring company is a permanent, court-approved transaction with irreversible tax and financial consequences. Consult a CPA and independent legal counsel — not the factoring company — before agreeing to any transfer.

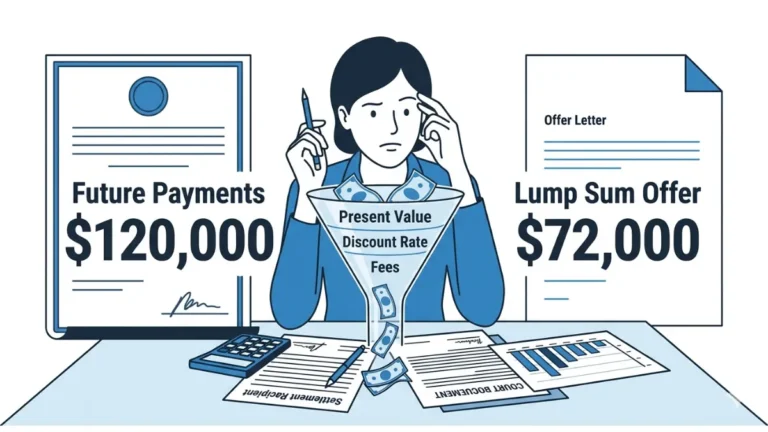

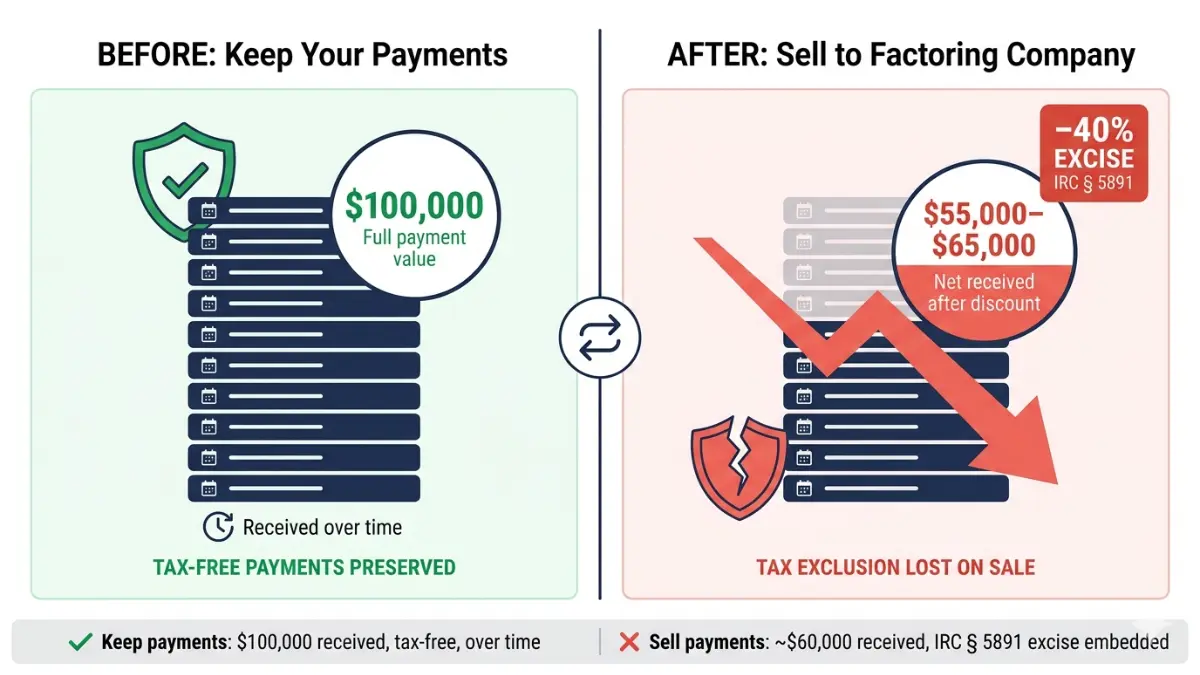

When you sell structured settlement payments to a factoring company, IRC Section 5891 imposes a 40% excise tax on the transaction — paid by the factoring company, but passed to you through the discount rate applied to your payment stream.

How factoring transactions work — and what the IRS taxes

The factoring company pays you a lump sum today in exchange for your future payment rights.

That lump sum is calculated by discounting your future payments at a rate that typically ranges from 9% to 18% annually — and embedded in that discount is the cost of the IRC 5891 excise tax. The seller does not receive a separate tax bill; the tax is absorbed into the price they offer you.

IRC Section 5891: the 40% excise tax and who actually pays it

💡 Expert Note (CFA): I have reviewed factoring agreements for clients who came to me after signing. In every case, the net-of-tax, net-of-discount payout was 40% to 60% below the face value of the payments they surrendered. The IRC Section 5891 excise tax is structurally invisible in most factoring company marketing materials — and that invisibility is the mechanism through which clients lose the most money.

📊 Data Point: IRC Section 5891 imposes a 40% excise tax on the present value discount claimed by structured settlement factoring companies on any transfer that does not receive court approval. Source: Internal Revenue Code Section 5891 (26 U.S.C. § 5891), effective as amended.

Use our ROI calculator to compare the net return on keeping your payments against the factoring company’s lump sum offer, and our break-even calculator to identify the point at which the discount and excise tax costs make selling financially irrational.

Net-of-tax calculation: what you actually receive after a sale

A settlement recipient with $100,000 in remaining structured payments who accepts a factoring company’s offer at a 12% discount rate will typically receive $55,000 to $65,000 — not $88,000. The IRC 5891 excise tax cost is embedded in the discount spread, not listed as a separate line item.

Before agreeing to sell, model what keeping your payments and investing them returns using our investment calculator and compound interest calculator. Our inflation calculator shows whether your fixed periodic payments maintain real purchasing power over a 20-year term — which is often the comparison that makes keeping payments the more rational financial choice.

State court approval requirements and additional tax exposure

Most states require court approval for structured settlement factoring transactions under the Structured Settlement Protection Acts — without that approval, the factoring company faces the full 40% excise tax penalty, which is why they require it.

Investment returns generated by any lump sum you receive are taxable as ordinary income or capital gains, regardless of the original settlement exclusion. Use our capital gains tax calculator for investment income modeling, our stock calculator and dividend calculator for equity investment returns, and our retirement calculator if you plan to redirect the lump sum into a long-term retirement strategy. Proceeds rolled into a 401(k) or IRA can be modeled with our 401(k) calculator and Roth IRA calculator.

The CFPB has published guidance on structured settlement transfers that outlines consumer protections and the required court approval process in most states — read it before signing anything. See also our guide to capital gains tax rates in 2026 for a full breakdown of investment income taxation.

✅ Pro Tip: If your structured settlement lump sum will go toward a real estate purchase, model the full cost picture first: mortgage rate calculator, down payment calculator, closing cost calculator, and home affordability calculator. If you are refinancing existing debt using periodic payments as qualifying income, also run our refinance calculator and mortgage refinance calculator before agreeing to any loan terms.

ℹ️ Disclaimer: Structured settlement factoring transactions are regulated under IRC Section 5891 and applicable state Structured Settlement Protection Acts. The tax and financial consequences are irreversible. Independent legal counsel and a CPA review are required before any transfer agreement is signed. This section is educational only and does not constitute legal or financial advice.

State taxes, SSI benefits, and special cases every recipient should know

The federal exclusion under IRC 104(a)(2) does not automatically protect your settlement from every financial consequence.

Three additional exposures affect a significant share of structured settlement recipients — and every competing guide leaves at least one of them unanswered.

Do states tax structured settlement payments differently than the IRS?

Most states conform to the federal IRC 104(a)(2) exclusion and do not tax structured settlement payments received for physical injury. However, state treatment of punitive damages and accrued interest varies — California, for example, taxes punitive damages as ordinary income regardless of settlement structure, and several states impose their own rules on emotional distress awards that diverge from federal treatment.

Use our sales tax calculator for any state-level calculations on reimbursed taxable goods components, our property tax calculator if your settlement resolved a property damage claim, and our income tax calculator to model state income tax exposure on any taxable settlement component. Always verify current state rules with a CPA licensed in your state.

How structured settlements affect Social Security (SSI) and Medicaid

📊 Data Point: The SSI resource limit is $2,000 for an individual and $3,000 for a couple as of 2026. A structured settlement lump sum that exceeds these thresholds — received in a single month — can disqualify a recipient from SSI benefits for that month. Source: SSA.gov SSI Resource Limits, 2026.

Periodic structured settlement payments are generally not counted as a resource under SSI rules — but a lump sum, or a sale of payments to a factoring company, can trigger the resource limit immediately.

Use our Social Security calculator to model how benefit timing interacts with settlement income, and our budget calculator to align your periodic payment schedule with monthly living expenses. If your settlement income is being evaluated for a loan application, our debt-to-income ratio calculator shows how lenders may weight the income stream. Settlement recipients applying proceeds toward debt elimination should model savings first with our debt consolidation calculator and credit card payoff calculator.

When settlement investment income becomes taxable

The original settlement payment retains its tax-free status — but any return generated by investing those funds is taxable.

A $200,000 tax-free settlement payment earning 5% annually generates $10,000 in taxable interest or dividend income in year one. Use our CD calculator for conservative fixed-income modeling, and our compound interest calculator to project long-term growth on reinvested settlement funds.

ℹ️ Disclaimer: SSI and Medicaid eligibility rules are complex and fact-specific. Settlement design decisions that affect benefit eligibility have permanent consequences. Consult a benefits counselor or elder law attorney — not a general financial advisor — before structuring or modifying settlement payments to protect benefit eligibility.

CFA perspective: the three structured settlement tax mistakes that cost recipients the most

Every year, settlement recipients lose money not because the IRS is wrong, but because they started with the wrong assumption.

Mistake 1: Trusting the settlement label instead of the IRS test

Settlement agreements routinely label all damages as “compensatory” — but that label means nothing to the IRS.

The physical injury test is the only test. If a CPA has not reviewed the agreement language against IRC Section 104(a)(2) before filing, the return is an educated guess.

Mistake 2: Selling payments without independent tax counsel

Every factoring company rep is compensated on the discount spread — not on your net outcome.

The IRC 5891 excise tax, the state court approval cost, and the loss of the tax exclusion on investment returns are never prominently disclosed in a factoring offer. Use our investment calculator to model the alternative before signing.

Mistake 3: Ignoring state tax divergence and SSI interaction

A settlement recipient who correctly reports zero federal tax can still owe state tax on punitive damages or inadvertently lose SSI eligibility through a single lump sum.

These are not edge cases — they are the most common silent errors I have seen in three decades of client work. Use our college savings calculator if settlement proceeds will fund education, our credit score calculator to monitor how post-settlement financial decisions affect your credit position, and our car insurance calculator if the settlement resolved a vehicle-related injury claim.

Before your next tax filing, take one step: locate your settlement agreement, identify every payment component, and run each against the physical injury test in IRC 104(a)(2). If any component is unclear, that is exactly what a CPA review is for.

✅ Pro Tip: Settlement recipients managing everyday finances alongside periodic payment income benefit from our full toolkit — overtime calculator for additional wage income, tip calculator for service-sector supplemental income, EMI calculator for structured loan repayments, currency converter for foreign-denominated components, rent vs. buy calculator when applying proceeds to housing decisions, and loan-to-value calculator when applying settlement funds toward mortgage paydown.

ℹ️ Disclaimer: This article reflects general IRS rules governing structured settlement payments as of May 2026 and has been reviewed by a licensed CPA. It does not constitute individual tax advice. Consult a CPA or tax attorney for guidance specific to your settlement agreement, state of residence, and tax situation. Primary reference: IRS Publication 4345.

Frequently asked questions about structured settlement payment taxes

All answers reflect IRS rules as of May 2026. Primary source: IRS Publication 4345 on lawsuit settlement taxability.

1. Are structured settlement payments considered income?

Most structured settlement payments are excluded from gross income under IRC Section 104(a)(2) and are not reported as income on your federal return. The exclusion applies to payments for physical personal injury, illness, and wrongful death. Punitive damages and accrued interest are exceptions — those are taxable as ordinary income. Confirm your specific situation with a licensed CPA. Source: IRS Publication 4345.

2. Do you pay federal taxes on personal injury settlement payments?

No — personal injury settlement payments received for physical harm are excluded from federal gross income under IRC Section 104(a)(2). The exclusion applies whether payments arrive periodically or as a single sum. The physical injury must be the origin of the claim — not just referenced in the agreement. If your settlement also funds a home purchase, model your financing with our mortgage calculator.

3. Are structured settlement annuity payments taxable?

The principal of a structured settlement annuity is tax-free when it originates from a physical injury claim. Investment growth earned on funds you reinvest after receiving payments is taxable as interest or capital gains income. The annuity issuer is required to issue a Form 1099-R for any taxable component — check Box 2a. Use our amortization calculator to compare your payment schedule against a loan repayment structure over the same term.

4. What portion of a structured settlement is taxable?

Punitive damages, accrued interest, and emotional distress damages not traceable to physical injury are fully taxable as ordinary income. Physical injury compensation, workers’ compensation, and wrongful death payments to heirs are excluded. A mixed settlement may contain both taxable and tax-free components within a single payment. Use our APR calculator to evaluate any factoring company’s effective rate against other borrowing alternatives. Consult a CPA. Source: IRS Publication 4345.

5. Are punitive damages in structured settlements taxable?

Yes — punitive damages in structured settlements are fully taxable as ordinary income under any circumstances. The U.S. Supreme Court confirmed in O’Gilvie v. United States (1996) that punitive damages do not qualify for the IRC 104(a)(2) physical injury exclusion, even when the underlying claim involved physical harm. Report them as other income on Form 1040. Consult a licensed CPA or tax attorney for reporting guidance.

6. Is a lump sum settlement taxable vs. periodic payments?

The IRC Section 104(a)(2) exclusion applies to both lump sum and periodic structured settlement payments — the payment structure does not change the tax outcome. The same physical injury test governs both formats. A lump sum that includes punitive damages or interest is taxable on the same components. Use our free loan calculator to model any debt you plan to eliminate with settlement proceeds.

7. Are wrongful death settlement payments taxable?

Wrongful death settlement payments paid to surviving heirs are generally excluded from gross income under IRC Section 104(c). The punitive damage component of any wrongful death settlement remains fully taxable. Beneficiaries managing simultaneous life insurance proceeds should use our life insurance calculator to model the combined financial picture. Source: IRC Section 104(c); IRS Publication 4345. Confirm your specific situation with a licensed CPA.

8. Are workers’ compensation structured settlement payments taxable?

No — workers’ compensation structured settlement payments are excluded from gross income under IRC Section 104(a)(1), which governs workers’ comp separately from the personal injury exclusion under 104(a)(2). See our workers’ compensation guide for full benefit interaction details. Recipients who transition to self-employment after a workers’ comp settlement and need startup financing can model borrowing with our business loan calculator.

9. Do structured settlements affect Social Security or SSI benefits?

Periodic structured settlement payments are generally not counted as a resource under SSI rules. A lump sum received from a factoring transaction can exceed the $2,000 individual SSI resource limit and trigger a period of ineligibility. Use our Social Security calculator to model benefit timing interactions. Source: SSA.gov SSI resource limit rules, 2026. Consult a benefits counselor or elder law attorney before any lump sum transaction.

10. What is IRS Publication 4345?

IRS Publication 4345 is the Internal Revenue Service’s primary guidance document on the taxability of lawsuit settlements, structured settlement payments, and jury awards. It defines which settlement types qualify for income exclusion and which are taxable as ordinary income. It is available free at IRS.gov and should be the first document any settlement recipient reviews before filing. Consult a CPA for settlement-specific application.

11. Are emotional distress damages in a settlement taxable?

Emotional distress damages are taxable as ordinary income unless they arise directly from a physical injury. If your settlement compensates you for emotional distress caused by a physical injury, that component qualifies for the IRC 104(a)(2) exclusion. If the emotional distress is independent of physical harm — from discrimination, defamation, or financial injury — it is 100% taxable. Confirm your origin-of-claim analysis with a licensed CPA before filing.

12. What happens to taxes when you sell structured settlement payments?

When you sell structured settlement payments to a factoring company, IRC Section 5891 imposes a 40% excise tax on the transaction — passed to you through the factoring company’s discount rate. Investment income on the lump sum you receive is also taxable. Use our home equity calculator if you plan to apply the lump sum toward mortgage paydown. Consult a CPA and independent legal counsel before signing any transfer agreement. Source: 26 U.S.C. § 5891.

13. Are structured settlement payments taxable at the state level?

Most states conform to the federal IRC 104(a)(2) exclusion and do not tax physical injury structured settlement payments. State treatment of punitive damages and accrued interest varies — verify your state’s rules with a CPA licensed in your state. Use our sales tax calculator for any state-level calculations on reimbursed taxable goods included in a settlement. Source: State Department of Revenue guidance (varies by state).

14. Will I receive a 1099 for structured settlement payments?

You will receive a Form 1099-R only if your structured settlement annuity has a taxable component — the annuity issuer is required to file it for any distribution with a taxable amount. Box 2a shows the taxable portion. Review our complete guide to 1099 form types, deadlines, and penalties before assuming Box 2a is accurate — misclassification by the annuity issuer does occur. Consult a CPA to verify. Source: IRS Form 1099-R instructions.

15. Are discrimination lawsuit settlement payments taxable?

Yes — employment discrimination settlement payments are fully taxable as ordinary income because they do not originate from a physical personal injury. The U.S. Supreme Court confirmed this standard in United States v. Burke (1992). Discrimination settlement recipients should use our auto loan calculator if proceeds will be applied toward vehicle financing. Consult a licensed CPA or tax attorney for accurate reporting guidance. Source: IRS Publication 4345; IRC Section 61.

16. How do I report structured settlement payments on my tax return?

Tax-free structured settlement payments are not reported anywhere on Form 1040. If your settlement includes a taxable component, report the amount from Form 1099-R Box 2a on Schedule 1 of Form 1040. Use our student loan calculator if you are applying tax-free settlement proceeds toward student debt payoff to model the acceleration. Consult a CPA to confirm accurate line placement. Source: IRS Form 1040 instructions, Schedule 1.

17. Are structured settlement payments taxable if the money is invested?

The original structured settlement payment retains its tax-free status permanently. However, any return generated by investing those proceeds — interest, dividends, or capital gains — is taxable as ordinary income or capital gains in the year earned. Use our CD calculator for conservative fixed-income modeling or our compound interest calculator for long-term growth projections. Source: IRC Sections 61, 1001; IRS Publication 4345.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.