APR Calculator: Find Your True Loan Cost (2026)

APR Calculator

Estimate APR from loan cash flows: amount received, fees (upfront or financed), payment schedule, recurring fees, and optional balloon. Includes detailed amortization tables + CSV exports.

Inputs

This is the cash/value you actually get (before paying any upfront fees).

Uses amount received × (rate/365) × days (simple estimate).

This is treated as a cash outflow but not principal/interest.

Results

APR (effective annual)

—

Nominal APR (periodic × ppy): —

Periodic rate: —

Payments

—

Frequency: — • # payments: —

Recurring fee: — • Balloon: —

Proceeds vs balance

Amount received: —

Starting balance: —

Net proceeds: —

Totals (estimate)

Total of payments: —

Total out-of-pocket (payments + upfront fees): —

Total interest (schedule): —

Interest rate vs APR (context)

Note rate (if provided): — • Schedule effective annual rate used: —

Fees total: — • Upfront: — • Financed: —

APR is typically higher than the note rate when fees are added, because it reflects the cost of credit more completely. [web:135]

Cash-flow view (what APR solver uses)

At time 0 (net proceeds): —

Payments 1..N−1: —

Final payment (includes balloon): —

Fee breakdown (entered)

| Fee | Amount |

|---|

Yearly summary

| Year | Total paid | Principal | Interest | Recurring fees | Balloon | Ending balance |

|---|

Monthly summary (calendar months)

| Month | Total paid | Principal | Interest | Recurring fees | Balloon | Ending balance |

|---|

Full schedule (per payment)

| # | Date | Total payment | P&I used | Recurring fee | Balloon | Interest | Principal | Balance |

|---|

Results appear after you click “Calculate.”

In This Article

What Is APR? The Number Your Lender Hopes You Ignore

APR (Annual Percentage Rate) is the true yearly cost of borrowing money. It includes your interest rate plus all mandatory lender fees — expressed as a single annual percentage. It is always equal to or higher than the stated interest rate, and it is the only fair number to use when comparing loan offers.

Your lender quotes a 5.9% interest rate. But once origination fees, points, and closing costs are factored in, your real APR could be 7.2% — costing you thousands of dollars more than you expected.

The Consumer Financial Protection Bureau (CFPB) requires lenders to disclose APR under the federal Truth in Lending Act (TILA) — precisely because interest rates alone mislead borrowers.

Why APR matters more than the interest rate:

- Interest rate = cost of borrowing the principal only

- APR = interest rate + origination fees + points + lender charges

- APR is the legally required comparison metric under U.S. federal law

- A lower interest rate with high fees can produce a higher APR than a higher-rate loan with no fees

Use our free loan calculator alongside this APR calculator to see total payment differences instantly.

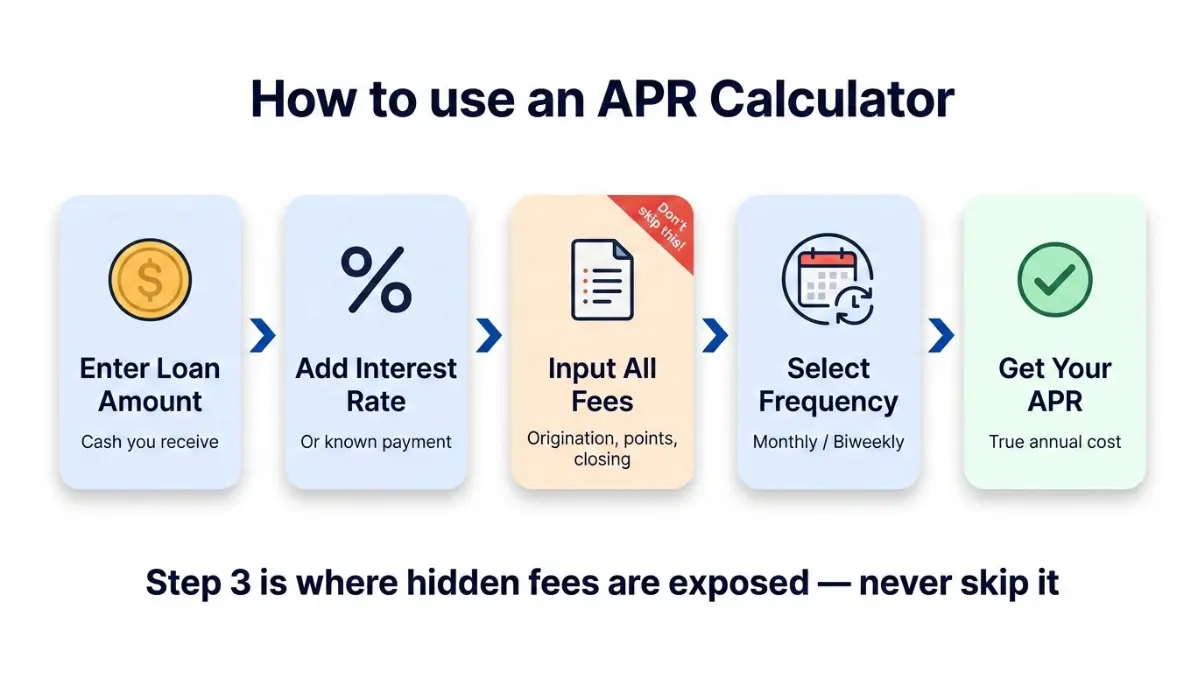

How to Use This APR Calculator — Step-by-Step (2026)

No guesswork. No finance degree needed. Here is exactly how to get your true loan APR in under two minutes.

What You Need Before You Start

Gather these four items from your lender’s offer letter or Loan Estimate:

- Loan amount (the cash you actually receive)

- Interest rate (or your known monthly payment)

- Loan term (years and months)

- All fees: origination fee %, discount points %, lender flat fees, title/closing fees, third-party fees, government recording fees

5-Step Input Guide

- Select currency and payment frequency — Choose USD, monthly (standard for most U.S. loans), or biweekly/weekly if applicable

- Enter your loan amount — This is the amount you receive, not the total financed balance

- Choose your mode — Select “I know the interest rate” (most common) or “I know the payment” if you already have a quote

- Add all fees — Enter origination %, discount points %, and each flat fee separately. Every fee entered increases your calculated APR

- Click Calculate — Your results appear instantly: effective APR, nominal APR, monthly payment, total interest, and a full amortization schedule

How to Read Your Results

| Result Field | What It Means |

|---|---|

| APR (Effective Annual) | Your true yearly borrowing cost — use this to compare lenders |

| APR (Nominal) | Periodic rate × payments per year — slightly lower than effective |

| Total Interest | Total interest paid over the full loan term |

| Total Out-of-Pocket | All payments + any upfront fees you paid separately |

| Amortization Schedule | Month-by-month breakdown of principal, interest, and balance |

Pro Tip: Always click “Toggle Fee Breakdown” after calculating. This shows you exactly which fee is inflating your APR the most — that is your negotiation target.

What This Means For You: If your calculated APR is more than 0.5% above your quoted interest rate, your lender fees are significant. Shop at least one more lender before signing.

Need to evaluate your total housing cost? Our mortgage calculator shows how APR changes your 30-year total repayment down to the dollar.

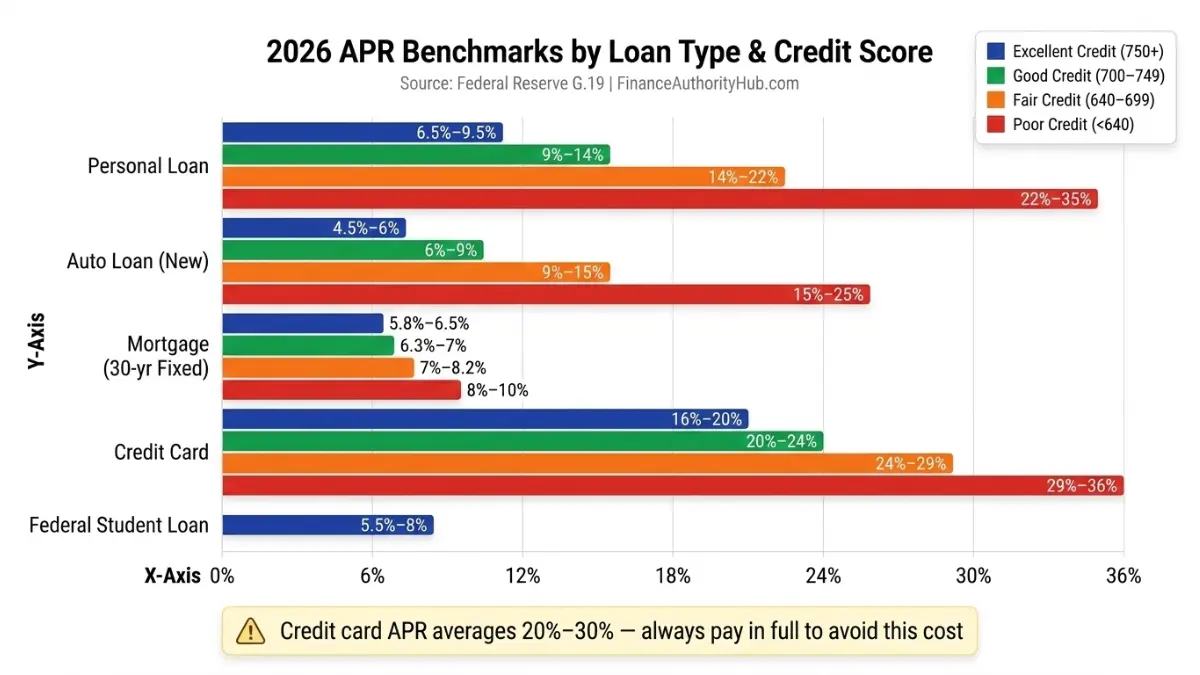

APR Calculator for Every Loan Type — 2026 Rate Benchmarks

No competitor covers this. Here are current APR ranges across all five major loan types, broken down by credit score tier — giving you an instant benchmark to judge whether the rate you’ve been offered is competitive.

2026 Average APR by Loan Type and Credit Score

Source: Federal Reserve G.19 Consumer Credit Report, March 2026 and current lender rate surveys.

| Loan Type | Excellent (750+) | Good (700–749) | Fair (640–699) | Poor (Below 640) |

|---|---|---|---|---|

| Personal Loan | 6.5% – 9.5% | 10% – 15% | 16% – 22% | 23% – 36% |

| Auto Loan (New) | 4.5% – 6.5% | 7% – 10% | 11% – 16% | 17% – 24% |

| Mortgage (30-yr Fixed) | 6.8% – 7.2% | 7.2% – 7.8% | 7.9% – 8.5% | 8.6%+ |

| Credit Card | 16% – 20% | 20% – 25% | 25% – 29% | 30%+ |

| Federal Student Loan | 6.53% (fixed, all borrowers) | Same | Same | Same |

Key Insight: If your offered APR is above the range for your credit tier, you are overpaying. Run the number in the calculator above, then negotiate or shop elsewhere.

Mortgage APR Calculator — Which Fees Are Included

Under TILA, mortgage APR must include:

- Origination fees and points

- Mortgage broker fees

- PMI (Private Mortgage Insurance) if applicable

- Processing and underwriting fees

Excluded from mortgage APR (but still real costs):

- Appraisal fees

- Title insurance

- Government recording fees

- Home inspection costs

This is why you must add every fee manually into our APR calculator — the lender’s disclosed APR may legally omit costs that still come out of your pocket.

Auto Loan APR — The Dealer Markup Trap

Here is a real-world scenario our readers encounter every day:

A borrower with a 720 credit score qualifies for a 7.2% APR from their credit union. The dealership offers “7.9% financing.” The dealer keeps the 0.7% markup as profit — costing the borrower $1,100 extra on a $30,000, 60-month loan.

Always get a pre-approval from your bank or credit union before visiting the dealership. Use our auto loan calculator to compare dealer financing vs. direct lender offers side by side.

Personal Loan APR — The Origination Fee Impact

Example: You borrow $10,000 at a quoted 12% interest rate with a $300 origination fee.

- Without fee: APR = 12.00%

- With $300 fee financed in: APR = 13.2%

- Over 36 months, that fee adds $167 in real cost

Always run personal loan offers through the APR calculator before accepting. For consolidating multiple debts, our debt consolidation calculator shows whether a personal loan actually reduces your total interest burden.

Credit Card APR vs. Interest Rate

On credit cards, the APR and interest rate are identical — because lenders are not required to include card fees (annual fee, balance transfer fee) in the credit card APR calculation. This means two cards with the same APR can have very different total costs. Always compare both the APR and the annual fee when choosing a card. See our full 0% APR credit card guide for how to eliminate debt interest-free.

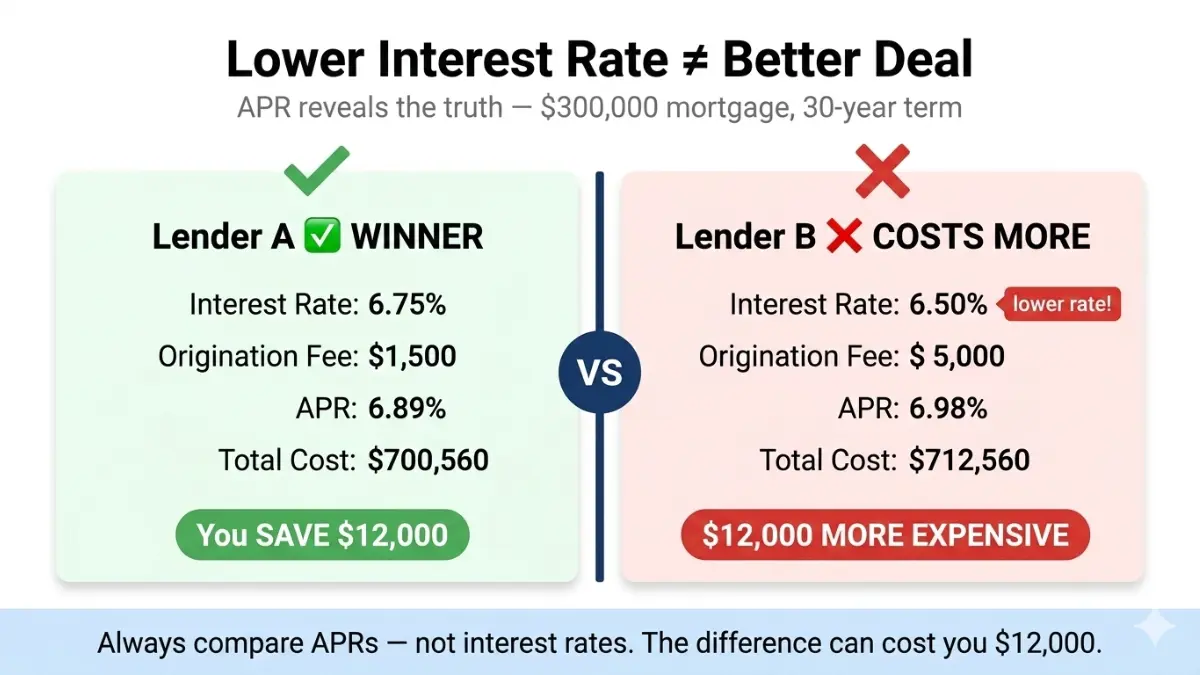

APR vs. Interest Rate — Why the Difference Could Cost You $12,000

This is the single most misunderstood concept in personal finance. Most borrowers compare only interest rates — and get it completely wrong.

The Core Difference (30-Second Explanation)

| Interest Rate | APR | |

|---|---|---|

| What it measures | Cost of principal only | Total cost of borrowing |

| Includes fees? | ❌ No | ✅ Yes |

| Legally required disclosure? | Yes | Yes (under TILA) |

| Better for comparing lenders? | ❌ | ✅ Always |

The federal Truth in Lending Act requires every U.S. lender to disclose APR — precisely because interest rate alone is insufficient for fair comparison.

Real-World Example: $300,000 Mortgage

| Lender A | Lender B | |

|---|---|---|

| Interest Rate | 6.75% | 6.50% |

| Origination Fee | $1,500 | $5,000 |

| Other Closing Costs | $2,000 | $3,500 |

| APR | 6.89% | 6.98% |

| Monthly Payment | $1,946 | $1,896 |

| Total Cost (30 yrs) | $700,560 | $712,560 |

| Winner | ✅ Lender A | ❌ More expensive |

Lender B’s lower interest rate is actually $12,000 more expensive over the life of the loan once fees are included. Without the APR calculator, most borrowers would choose the wrong lender.

Use our mortgage refinance calculator to run the same analysis on refinancing offers — the APR gap between lenders is often even wider on refis.

Fixed APR vs. Variable APR — Which Is Safer in 2026?

| Fixed APR | Variable APR | |

|---|---|---|

| Rate stability | ✅ Locked for loan term | ❌ Fluctuates with index |

| Current environment (2026) | Better if rates rise | Better if Fed cuts rates |

| Best for | Mortgages, long-term loans | Short-term loans, HELOCs |

| Risk level | Low | Moderate to High |

The Federal Reserve held the federal funds rate at 3.5%–3.75% as of January 2026. Variable APR products tied to SOFR or the Prime Rate remain below their 2023 peaks, but rate direction in 2026 is uncertain. For loans over 5 years, fixed APR provides better payment predictability.

APR vs. APY — Don’t Confuse These Two

| APR | APY | |

|---|---|---|

| Used for | Loans (borrowing) | Savings/deposits (earning) |

| Includes compounding? | ❌ No | ✅ Yes |

| Which looks smaller? | ✅ APR | — |

| Which looks bigger? | — | ✅ APY |

Banks advertise APR on loans (lower-looking number) and APY on savings accounts (higher-looking number) — both are strategic. Our deep-dive on APR vs. interest rate covers every scenario where this distinction costs borrowers money.

How to Lower Your APR in 2026 — Expert-Backed Strategies

Reviewed by Laura M. Bennett, CFP® (18 years consumer lending) and Daniel Moreau, CPA/CFP (loan cost optimization specialist)

No competitor page offers expert-panel guidance on APR reduction. Here is what financial professionals recommend to clients facing loan decisions in 2026.

6 Proven Ways to Lower Your APR Before Signing

1. Improve your credit score first Every 20-point increase above 700 can reduce APR by 0.5%–2.0%. On a $250,000 mortgage, a 1% APR reduction saves $53,000 over 30 years. Use our credit score calculator to understand where you stand before applying.

2. Shop at least 3 lenders APR varies by 1%–4% for the same borrower. A 2026 CFPB study found that borrowers who compared just two lenders saved an average of $1,500 in loan costs.

3. Negotiate origination fees directly Origination fees (typically 0.5%–1% of loan amount) are often negotiable. Eliminating a 1% origination fee on a $200,000 loan reduces APR by approximately 0.15%–0.25% and saves $2,000 upfront.

4. Choose a shorter loan term Lenders offer lower APRs for 24-month vs. 60-month auto loans, and 15-year vs. 30-year mortgages. Compare total cost with our amortization calculator.

5. Make a larger down payment For mortgages, a down payment above 20% eliminates PMI and typically unlocks a lower rate tier. Our down payment calculator shows exactly how much more you need to hit the next APR threshold.

6. Use a creditworthy co-signer Adding a co-signer with excellent credit (750+) can reduce APR by 3%–5% for fair-credit borrowers — especially on personal loans and private student loans.

What Lenders Won’t Tell You About APR

- Not all fees are included. Appraisal fees, title insurance, and home inspection costs are legally excluded from the disclosed mortgage APR — but they still cost you money at closing

- APR assumes you hold the loan to full term. If you sell or refinance in year 5 of a 30-year mortgage, your effective rate is much higher than the disclosed APR because upfront fees are amortized over fewer payments

- Variable APR teaser rates expire. A 0% intro APR credit card switches to 20%–29% after 12–21 months. The APR calculator on this page helps you model what happens when the introductory period ends

What This Means For You: Before accepting any loan offer, run both options through the APR calculator above. A 0.5% APR difference on a $250,000 mortgage is worth $26,000 over 30 years — more than most people spend negotiating.

For borrowers currently carrying high-rate debt, our debt consolidation guide shows how to use APR comparison to cut total interest costs by thousands.

APR Calculator — Frequently Asked Questions

1. What does an APR calculator calculate?

An APR calculator computes the true annual cost of a loan by combining the interest rate with all associated fees — origination charges, points, and lender costs — into a single annual percentage. It gives you the real cost of borrowing, not just the headline rate.

2. Is a lower or higher APR better for a loan?

Lower is always better for borrowers. A lower APR means you pay less in total interest and fees over the life of the loan. Always compare APRs — never just interest rates — when evaluating competing loan offers.

3. What is a good APR for a personal loan in 2026?

A good APR for a personal loan in 2026 is below 10% for excellent credit (750+) and below 16% for good credit (700–749). Anything above 24% is considered high-cost borrowing, and above 36% enters predatory lending territory for most U.S. states.

4. Why is my APR higher than my interest rate?

Because APR includes fees that your interest rate does not. Origination fees, discount points, and lender charges are added to the interest cost and spread across the loan term — producing a higher annual rate figure. The CFPB mandates this disclosure so borrowers can make fair comparisons.

5. Can I negotiate my APR with a lender?

Yes — especially on personal loans and mortgages. The most effective approach is to negotiate the origination fee and discount points rather than the interest rate itself. Getting competing offers from 3+ lenders gives you leverage to ask for fee reductions.

6. How does my credit score affect my APR?

Your credit score is the single biggest factor in the APR you are offered. Borrowers with scores above 750 qualify for rates 8–12 percentage points lower than borrowers below 640 on products like personal loans and credit cards. Improve your score before applying for any major loan.

7. What is the difference between APR and APY?

APR (Annual Percentage Rate) is the annual cost of a loan — what you pay. APY (Annual Percentage Yield) is the annual return on a savings or investment account — what you earn. APY includes compounding; APR does not. Lenders use APR for loans and banks use APY for deposits — each is the number that looks better for marketing purposes.

8. Does APR include closing costs?

For mortgages, APR must include certain closing costs under TILA: origination fees, points, and mortgage broker fees. However, it legally excludes appraisal fees, title insurance, home inspection fees, and prepaid taxes or insurance. Always read the Loan Estimate to see what your lender included.

9. What is 0% APR and is it really free?

A 0% APR promotional offer is genuinely interest-free — but only during the promotional period. Once the introductory term ends (typically 12–21 months), the full APR applies to any remaining balance, often at 20%–29%. The borrowing is only free if the balance is paid in full before the promotional period expires.

10. How accurate is an online APR calculator?

A well-built APR calculator is highly accurate for estimating your true loan cost when you input all fees correctly. The key variable is completeness — if you omit fees, your calculated APR will be understated. Always request the full fee itemization from your lender before entering figures.

11. How does APR work differently on credit cards vs. loans?

On installment loans (mortgage, auto, personal), APR includes the interest rate plus lender fees. On credit cards, APR equals the interest rate only — fees like annual fees and balance transfer fees are excluded from the APR calculation by law. This makes credit card APRs appear lower than they functionally are when fees are significant.

⚖️ Disclaimer

The APR calculator on this page is provided for educational and informational purposes only. All results are estimates based on the inputs you enter and may not reflect actual loan terms, official lender disclosures, or jurisdiction-specific APR calculations. This content does not constitute financial advice. Under the federal Truth in Lending Act (TILA), your lender is required to provide official APR disclosures before loan consummation — always review those documents carefully. FinanceAuthorityHub.com is not a lender and does not offer, arrange, or recommend specific loan products. Consult a qualified financial advisor or licensed mortgage professional before making borrowing decisions.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.