Take-Home Pay Calculator: Real Net Pay 2026

Take Home Pay Calculator

Estimate net take-home pay after pre-tax deductions, income tax, employee contributions, and post-tax deductions—then view per-paycheck details, bracket breakdown, and “extra income” impact.

Inputs

Results

Net pay (per paycheck)

—

Net per month (avg): —

Gross pay (per paycheck)

—

Net per week (avg): —

Annual net take-home

—

Net per hour (est): —

Rates

Take-home: —

Effective tax (taxable): —

Marginal rate (est): —

Annual totals (estimate)

Gross: — • Bonus included: —

Pre-tax deductions: — • Post-tax deductions: —

Income tax: — • Employee contributions: — • Total withheld: —

Effective tax on gross: — • Tax wedge (employer-cost basis): —

Employer total cost: —

Representative paycheck (paystub-style)

If bonus is “paid once”, only that paycheck changes; the table shows every paycheck.

Extra income impact (annual)

| + Gross income | + Net take-home | Take-home of extra |

|---|

This helps users understand “why” net pay doesn’t rise 1:1 with gross (taxes + contributions + deductions).

Annual bracket breakdown (progressive mode)

| From | Up to | Rate | Amount taxed | Tax |

|---|

Per-paycheck breakdown (1 year)

| Paycheck | Gross | Bonus | Pre-tax | Taxable | Income tax | Employee contrib | Post-tax | Net pay | Employer cost |

|---|

Results appear after you click “Calculate.”

In This Article

Your offer letter says $75,000. Your bank account will see around $54,800. That $20,200 gap is not a mistake — it is taxes, FICA, and deductions doing their job every single pay period.

This take-home pay calculator above gives you your exact net pay after all federal deductions, state taxes, pre-tax contributions, and the new 2026 OBBBA exemptions — in under 60 seconds.

What you will learn in this guide:

- Exactly what comes out of every paycheck in 2026

- Real salary breakdowns at $45K, $75K, and $120K

- 7 legal strategies to keep more of what you earn

Last updated: March 2026 | Uses 2026 IRS tax brackets and OBBBA rules

How to Use This Take-Home Pay Calculator

Getting your real net pay takes under two minutes. Follow these five steps:

Step 1 — Enter Your Income Type and Amount

- Salaried workers: Enter your annual gross salary (the number on your offer letter)

- Hourly workers: Enter your hourly rate, regular hours per week, and any overtime hours

- Add annual bonus or commission if applicable

Step 2 — Select Your Pay Frequency

Choose how often your employer pays you:

- Weekly — 52 paychecks per year

- Biweekly — 26 paychecks per year (most common in the USA)

- Semi-monthly — 24 paychecks per year

- Monthly — 12 paychecks per year

Pro Tip: Biweekly workers receive two extra paychecks annually compared to semi-monthly workers — this can significantly affect your monthly budgeting. Use our Salary Calculator to compare both scenarios side by side.

Step 3 — Add Your Pre-Tax Deductions

Enter your per-paycheck contributions to:

- Retirement plan (401k %, HSA, or fixed dollar amount)

- Health insurance premiums

- Any other pre-tax benefits

These deductions lower your taxable income before taxes are calculated — which is why they are so powerful.

Step 4 — Choose Your Tax Mode

- Flat rate: Enter a single percentage (useful for international users or simple estimates)

- Progressive brackets: Enter your state’s bracket table for a precise calculation

Step 5 — Read Your Real Net Pay Results

The calculator shows your net paycheck per period, annual take-home total, effective tax rate, marginal rate, and a full per-paycheck breakdown table. You can also download a CSV of every paycheck in the year.

What Actually Comes Out of Your Paycheck in 2026?

Most Americans overestimate their take-home pay by 15–20%, according to the IRS Taxpayer Advocate Service 2026 annual report. Understanding every deduction line is the first step to accurate budgeting.

Federal Income Tax — 2026 Brackets

Federal income tax uses a progressive system, meaning only the portion of your income that falls in each bracket is taxed at that rate. You do not pay 22% on your entire salary just because you earn $55,000.

| Tax Rate | Single Filer | Married Filing Jointly |

|---|---|---|

| 10% | $0 – $11,925 | $0 – $23,850 |

| 12% | $11,926 – $48,475 | $23,851 – $96,950 |

| 22% | $48,476 – $103,350 | $96,951 – $206,700 |

| 24% | $103,351 – $197,300 | $206,701 – $394,600 |

| 32% | $197,301 – $250,525 | $394,601 – $501,050 |

| 35% | $250,526 – $626,350 | $501,051 – $751,600 |

| 37% | Over $626,350 | Over $751,600 |

Source: IRS Publication 15-T, 2026 Federal Income Tax Withholding Methods

Standard deductions for 2026:

- Single filers: $16,100 (up from $15,000 in 2025)

- Married filing jointly: $32,200 (up from $30,000 in 2025)

- Head of household: $24,150

FICA Taxes — Social Security and Medicare (2026 Rates)

FICA taxes come out of every paycheck before you even see your money:

- Social Security: 6.2% on wages up to $184,500 (2026 wage base cap)

- Medicare: 1.45% on all wages, no cap

- Additional Medicare Tax: 0.9% on wages above $200,000 (single) or $250,000 (married)

- Your employer matches the 6.2% Social Security and 1.45% Medicare — meaning the full FICA cost is 15.3% of your wages, split equally

The SSA confirms the 2026 Social Security wage base is $184,500 — meaning once you earn above that threshold, Social Security tax stops for the year.

State Income Tax — Where You Live Changes Everything

| State | Income Tax Rate | Impact on $75K Salary |

|---|---|---|

| California | Up to 13.3% | ~$6,975 extra vs Texas |

| New York | Up to 10.9% | ~$5,700 extra vs Florida |

| Oregon | Up to 9.9% | ~$5,100 extra vs Nevada |

| Texas | 0% | No state income tax |

| Florida | 0% | No state income tax |

| Nevada | 0% | No state income tax |

Nine states have zero state income tax in 2026: Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming.

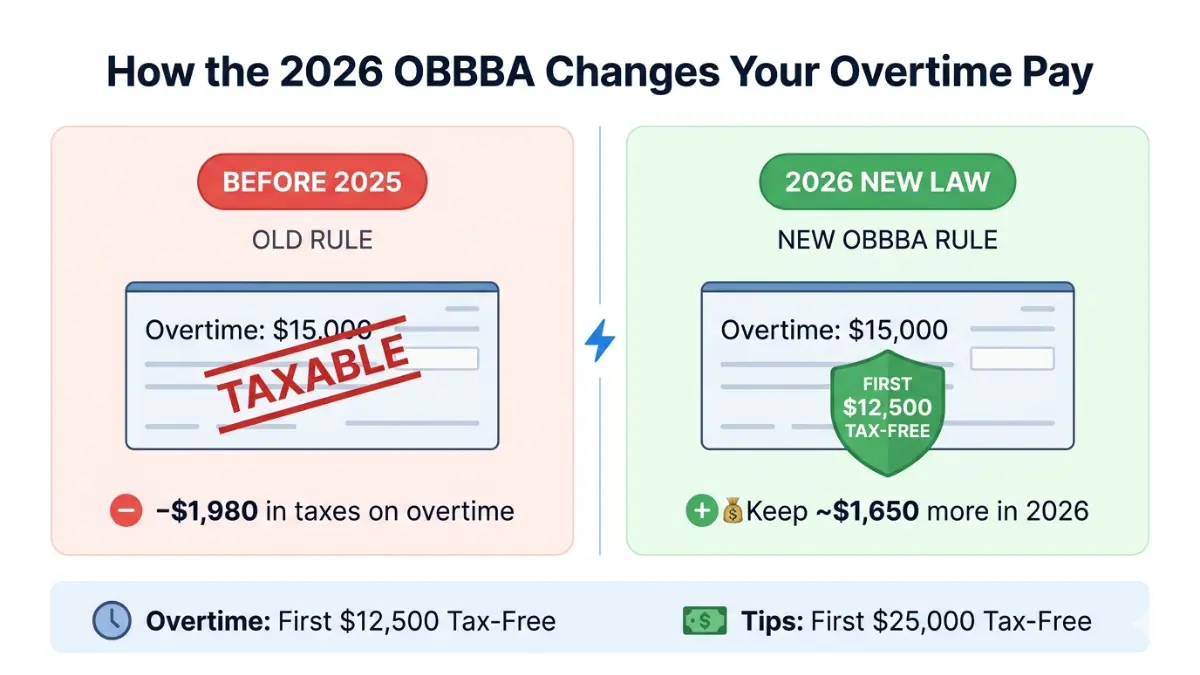

⚡ The NEW 2026 OBBBA Deductions — What Most Calculators Still Miss

The One Big Beautiful Bill Act (OBBBA), signed into law in 2025, introduced two major tax-free deductions effective for the 2026 tax year. The IRS updated its Tax Withholding Estimator in March 2026 to reflect these changes.

Overtime Exemption:

- First $12,500 of overtime wages is federally tax-free

- Phases out for incomes above $150,000 (single) / $300,000 (married filing jointly)

- Social Security and Medicare taxes still apply to overtime

Tips Exemption:

- First $25,000 in qualified tips is federally tax-free

- Applies to hospitality, food service, hair care, and other tip-based industries

- Same phase-out thresholds as the overtime exemption

What This Means For You: A restaurant server earning $20,000 in tips annually saves approximately $2,400 in federal income tax under the 2026 OBBBA rules. A construction worker earning $15,000 in overtime saves around $1,650 in federal tax. This is money that stays in your paycheck.

Pre-Tax Deductions That Shrink Your Tax Bill Legally

These come out before income tax is calculated, reducing how much of your income gets taxed:

- 401(k) contributions: Up to $23,500 in 2026 ($31,000 if age 50+)

- HSA contributions: Up to $4,300 (individual) / $8,550 (family) in 2026

- Health insurance premiums: Fully pre-tax when paid via payroll

- Flexible Spending Account (FSA): Up to $3,300 in 2026

Bold key takeaway: A $500/month 401(k) contribution ($6,000/year) reduces your federal taxable income by $6,000 — saving a 22% bracket worker approximately $1,320 per year in taxes while still growing your retirement account. Use our 401(k) Calculator to model your exact savings.

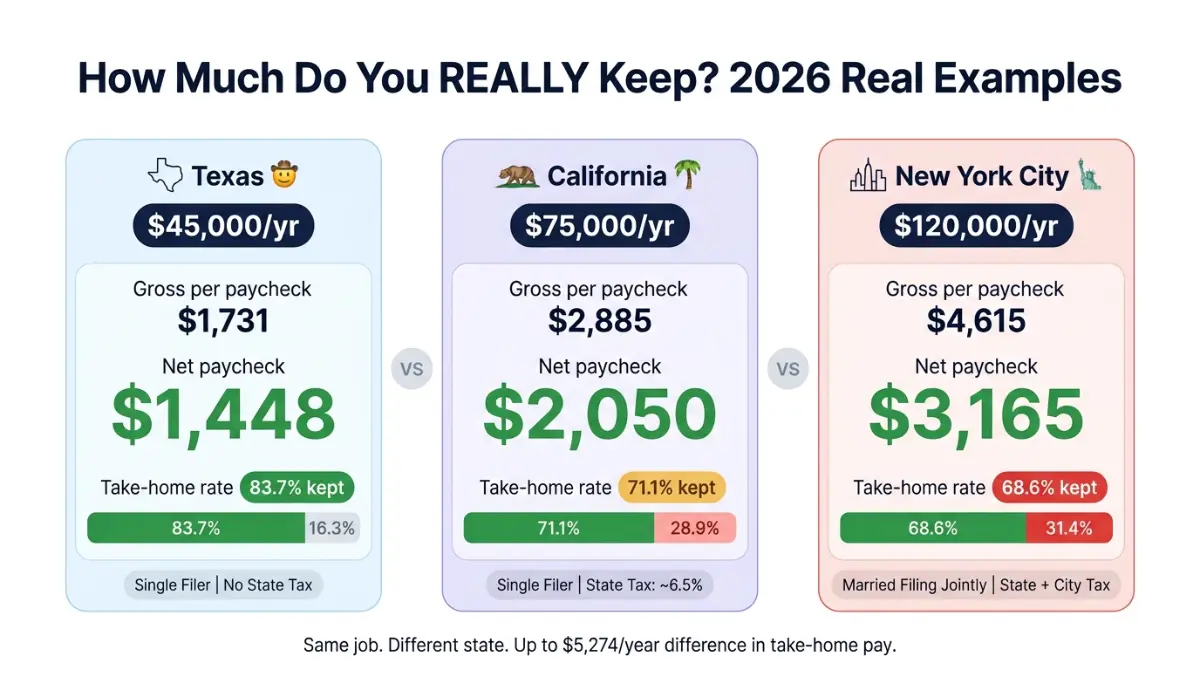

Real Take-Home Pay Examples: $45K, $75K, and $120K Salaries in 2026

$45,000 Salary — Take-Home Pay Breakdown (Single Filer, Texas)

Texas has zero state income tax, making it one of the most favorable states for take-home pay.

| Deduction | Annual Amount | Per Biweekly Paycheck |

|---|---|---|

| Gross Pay | $45,000 | $1,731 |

| Federal Income Tax | $3,898 | $150 |

| Social Security (6.2%) | $2,790 | $107 |

| Medicare (1.45%) | $653 | $25 |

| State Income Tax | $0 | $0 |

| Net Take-Home | ~$37,660 | ~$1,448 |

Take-home rate: 83.7% | Effective federal tax rate: 8.7%

What This Means For You: On $45,000, you keep roughly 84 cents of every dollar in Texas. In California, the same salary nets approximately $34,100 annually — $3,560 less per year — because of state income tax.

$75,000 Salary — Take-Home Pay Breakdown (Single Filer, California)

California’s progressive state tax system significantly impacts net pay at this income level.

| Deduction | Annual Amount | Per Biweekly Paycheck |

|---|---|---|

| Gross Pay | $75,000 | $2,885 |

| Federal Income Tax | $11,088 | $426 |

| Social Security (6.2%) | $4,650 | $179 |

| Medicare (1.45%) | $1,088 | $42 |

| California State Tax (~6.5%) | $4,875 | $188 |

| Net Take-Home | ~$53,300 | ~$2,050 |

Same $75,000 in Texas: ~$58,574 net | Difference: ~$5,274/year more in Texas

What This Means For You: Moving from California to Texas on the same $75,000 salary puts an extra $440/month in your pocket — without a single raise. Use our Home Affordability Calculator to see how that extra monthly net pay changes what you can comfortably afford.

$120,000 Salary — Take-Home Pay Breakdown (Married Filing Jointly, New York)

New York adds both a state tax layer (up to 10.9%) and a NYC local income tax for city residents.

| Deduction | Annual Amount | Per Biweekly Paycheck |

|---|---|---|

| Gross Pay | $120,000 | $4,615 |

| Federal Income Tax | $16,647 | $640 |

| Social Security (6.2%) | $7,440 | $286 |

| Medicare (1.45%) | $1,740 | $67 |

| NY State Tax (~6.4%) | $7,680 | $295 |

| NYC Local Tax (~3.5%) | $4,200 | $162 |

| Net Take-Home | ~$82,293 | ~$3,165 |

Take-home rate: 68.6% | Effective total tax rate: 31.4%

Side-by-Side Comparison:

| Salary | State | Annual Net | Biweekly Net | Take-Home % |

|---|---|---|---|---|

| $45,000 | Texas | ~$37,660 | ~$1,448 | 83.7% |

| $75,000 | California | ~$53,300 | ~$2,050 | 71.1% |

| $75,000 | Texas | ~$58,574 | ~$2,253 | 78.1% |

| $120,000 | New York (NYC) | ~$82,293 | ~$3,165 | 68.6% |

Figures are estimates using 2026 IRS brackets, standard deduction, no additional deductions. Actual results vary.

7 Proven Ways to Increase Your Take-Home Pay in 2026

You do not need a raise to bring home more money. These seven strategies are entirely legal and often overlooked.

1. Max Your Pre-Tax 401(k) Contributions

Every dollar you contribute to a traditional 401(k) reduces your taxable income dollar-for-dollar. The 2026 limit is $23,500 ($31,000 if you are 50 or older). Model your exact retirement contribution impact with our Retirement Calculator.

2. Open an HSA — The Triple Tax Advantage Account

An HSA beats almost every other tax account because contributions are pre-tax, grow tax-free, and withdrawals for medical expenses are tax-free. The 2026 individual limit is $4,300. Read the full breakdown in our guide on how an HSA beats a 401(k) for tax savings in 2026.

3. Update Your W-4 After Every Major Life Change

Marriage, divorce, a new child, a second job, or a home purchase can all shift how much tax should be withheld. Outdated W-4 forms are the leading cause of both under-withholding (a surprise tax bill in April) and over-withholding (giving the IRS an interest-free loan all year). Use the IRS Tax Withholding Estimator to generate an updated W-4 in minutes.

4. Use a Dependent Care FSA

If you pay for childcare or elder care, a Dependent Care FSA lets you contribute up to $5,000 per household pre-tax in 2026. That saves a 22% bracket worker $1,100 in taxes annually — money that goes directly into your net pay.

5. Claim the 2026 OBBBA Overtime Exemption

If you earn overtime pay, the first $12,500 is now federally tax-free under the One Big Beautiful Bill Act. Make sure your employer’s payroll system is applying this correctly. If you are unsure, use our Overtime Calculator to verify your expected net overtime pay.

6. Negotiate Tax-Free Benefits Instead of Salary

Certain employer benefits are completely tax-free: up to $315/month in commuter benefits, employer-paid health premiums, and remote work stipends. Negotiating these instead of a higher salary means you keep 100% of their value — no taxes withheld.

7. Use Your Net Pay to Build Wealth Strategically

Once you know your real take-home pay, the next step is putting it to work. Use our Savings Calculator to see how even $200/month extra in net pay compounds significantly over 10 years. If debt is reducing your monthly cash flow, our Debt Consolidation Calculator can show you how much you could free up each month.

Frequently Asked Questions — Take-Home Pay Calculator

1. What is take-home pay and how is it calculated?

Take-home pay (also called net pay) is the amount deposited into your bank account after all taxes and deductions are subtracted from your gross salary. The formula is: Gross Pay − Pre-Tax Deductions − Income Taxes − FICA Taxes − Post-Tax Deductions = Net Pay.

2. What is the difference between gross pay and net pay?

Gross pay is your total earnings before any deductions — the number on your offer letter. Net pay is what you actually receive. For most U.S. workers, net pay is 70–85% of gross pay, depending on state taxes and contribution elections.

3. How much of my paycheck goes to taxes in 2026?

For a single filer earning $60,000 with no pre-tax deductions, roughly 22–28% goes to combined federal income tax, Social Security, and Medicare. State income tax adds another 0–13.3% depending on where you live. Check your exact 2026 withholding using the IRS Tax Withholding Estimator. To understand how your full tax picture fits together, our Income Tax Calculator gives a complete breakdown.

4. What is a good take-home pay percentage?

A take-home rate of 75–85% is healthy for most U.S. workers in low or no-income-tax states. In high-tax states like California and New York, 65–75% is common at mid-to-high income levels. If your effective rate is below 65%, aggressive pre-tax contribution strategies can meaningfully improve it.

5. How does the 2026 OBBBA affect my take-home pay?

The One Big Beautiful Bill Act exempts the first $12,500 of overtime wages and first $25,000 of qualified tips from federal income tax starting in tax year 2026. This can increase take-home pay for overtime workers and tipped employees by $1,500–$3,000+ annually. The IRS confirmed these changes are now reflected in official withholding guidance.

6. Does my 401(k) contribution reduce my take-home pay?

Yes — but by far less than most people expect. A $200/biweekly paycheck 401(k) contribution reduces your net pay by only about $156, because the $44 difference is taxes you would have paid anyway. You are effectively saving $200 for a net cost of $156. Use our 401(k) Calculator to model your exact scenario.

7. Why is my take-home pay different from my salary?

Your salary is your gross pay — before five to six standard deductions hit every paycheck: federal income tax, Social Security, Medicare, state income tax, health insurance premiums, and any retirement contributions. The result is typically 15–30% lower than your stated salary. This gap surprises many people when they start a new job. Our guide on 2026 tax brackets and deductions explains every line in plain English.

8. How do I calculate my biweekly take-home pay?

Divide your annual gross salary by 26 (for 26 biweekly pay periods), then subtract your estimated biweekly taxes and deductions. Our take-home pay calculator does this automatically. Alternatively, use our Paycheck Calculator for a quick per-paycheck estimate.

9. What states have no income tax in 2026?

Nine states have zero state income tax in 2026: Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming. New Hampshire taxes investment income but not wages. Moving to any of these states on a $75,000 salary can mean $3,000–$7,000 more per year in take-home pay versus high-tax states.

10. Can I increase my take-home pay without a raise?

Yes — and most people are leaving significant money on the table. Strategies include updating your W-4, maxing pre-tax accounts like 401(k) and HSA, claiming OBBBA exemptions if applicable, and negotiating tax-free benefits. If high-interest debt is cutting into your monthly budget, consolidating it can free $300–$500/month. Use our Debt-to-Income Ratio Calculator to see where you stand, and the Social Security Calculator to understand how today’s decisions affect your future benefits.

11. Is this take-home pay calculator accurate for international users?

This calculator is world-ready — you can select currencies from USD, GBP, EUR, CAD, AUD, and 17+ more, and enter your own country’s flat tax rate or progressive bracket structure. For non-U.S. users, switch the tax mode to “Progressive brackets” and enter your country’s exact brackets. Note that FICA-specific fields apply to U.S. users; international users should use the “Employee contributions” fields for their country’s equivalent social insurance contributions.

Expert Note: “Before accepting any job offer, always run your salary through a take-home pay calculator first,” advises Laura M. Bennett, CFP, a senior financial planning expert at financeauthorityhub.com. “We regularly see clients who accepted offers based on gross salary, then struggled to meet mortgage or car loan obligations because their actual net pay was 25% lower than expected. Knowing your real net pay before you sign is non-negotiable.” Use our Mortgage Calculator or Auto Loan Calculator to verify any major financial commitment against your real take-home number.

⚠️ Disclaimer: This article and the calculator tool are for educational and informational purposes only and do not constitute financial, tax, or legal advice. Tax laws, brackets, and deduction limits change annually. All figures are estimates based on 2026 IRS published data and standard assumptions. Individual results will vary based on filing status, state of residence, employer benefits, and personal deductions. Always consult a qualified CPA or tax professional for advice specific to your situation. Calculator results should not be used for official payroll, tax filing, or financial planning without professional verification.

Sources: IRS Publication 15-T (2026) | SSA 2026 FICA Wage Base | IRS Tax Withholding Estimator | IRS OBBBA Withholding Update

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.