Free Savings Calculator – See Your Money Grow

Savings Calculator

Estimate future savings balance with compounding + monthly contributions, plus APY/effective yield, inflation-adjusted values, yearly summary, monthly schedule, and CSV export.

Inputs

Start-of-month contributions typically grow slightly more because they earn interest sooner.

If provided, we’ll estimate the monthly contribution needed to reach it.

Results

Ending balance

—

Inflation-adjusted ending value: —

Total contributed

—

Start: —

Monthly: —

Total interest earned

—

Monthly rate (effective): —

Yield details

Nominal annual rate: —

Effective annual yield (APY): —

Real APY (inflation-adjusted): —

Extra detail

Period: — months (~ —)

Goal insight

Goal: —

Estimated monthly contribution needed: —

Educational estimates only. Banks may apply different day-count rules, posting policies, and rounding.

Yearly summary

| Year | Start balance | Contributions | Interest (est.) | End balance | Total contributed (end) | Total interest earned (end) |

|---|

Monthly schedule (detailed)

| Month | Start balance | Contribution | Interest (est.) | End balance | Total contributed to date | Total interest earned to date |

|---|

Results appear after you click “Calculate.”

In This Article

A savings calculator estimates how much money you’ll accumulate over time based on your starting balance, monthly contributions, interest rate, and compounding frequency. Use the free tool above to instantly project your future savings balance, calculate your real APY, see inflation-adjusted results, and solve for how much you need to save monthly to hit your goal — all in one place.

How to Use This Free Savings Calculator (Step-by-Step)

Getting accurate results from a savings calculator takes less than 60 seconds. Follow these six steps:

- Choose your currency — Select from 22 options including USD, GBP, CAD, AUD, and EUR

- Enter your starting balance — This is the money you already have saved (enter 0 if starting fresh)

- Set your monthly contribution — The fixed amount you plan to add each month

- Enter your annual interest rate — Use the APY listed by your bank or check current national rates at FDIC.gov

- Choose compounding frequency — Daily, monthly, quarterly, or annually (daily compounding grows fastest)

- Set your savings period — Enter years and additional months, plus an optional start date and savings goal

Click “Calculate” and your results appear instantly below.

What Do the Results Mean?

| Result Field | What It Tells You |

|---|---|

| Ending Balance | Your projected total savings at the end of the period |

| Total Contributed | All money you deposited (starting balance + monthly contributions) |

| Total Interest Earned | Pure compound interest growth on top of your deposits |

| Effective APY | Your true annual yield, accounting for compounding frequency |

| Inflation-Adjusted Value | What your ending balance is worth in today’s dollars |

| Real APY | Your yield after inflation — the number that really matters |

| Goal Solver | The exact monthly contribution needed to hit your savings goal |

💡 Pro Tip: Use “Start of Month” contribution timing — it earns slightly more interest because every deposit starts compounding immediately. No other free savings calculator on the internet shows you this distinction.

How Your Savings Calculator Works — Compound Interest Explained

Simple Interest vs. Compound Interest: The Critical Difference

Most people underestimate how powerful compound interest really is. Here’s the real math.

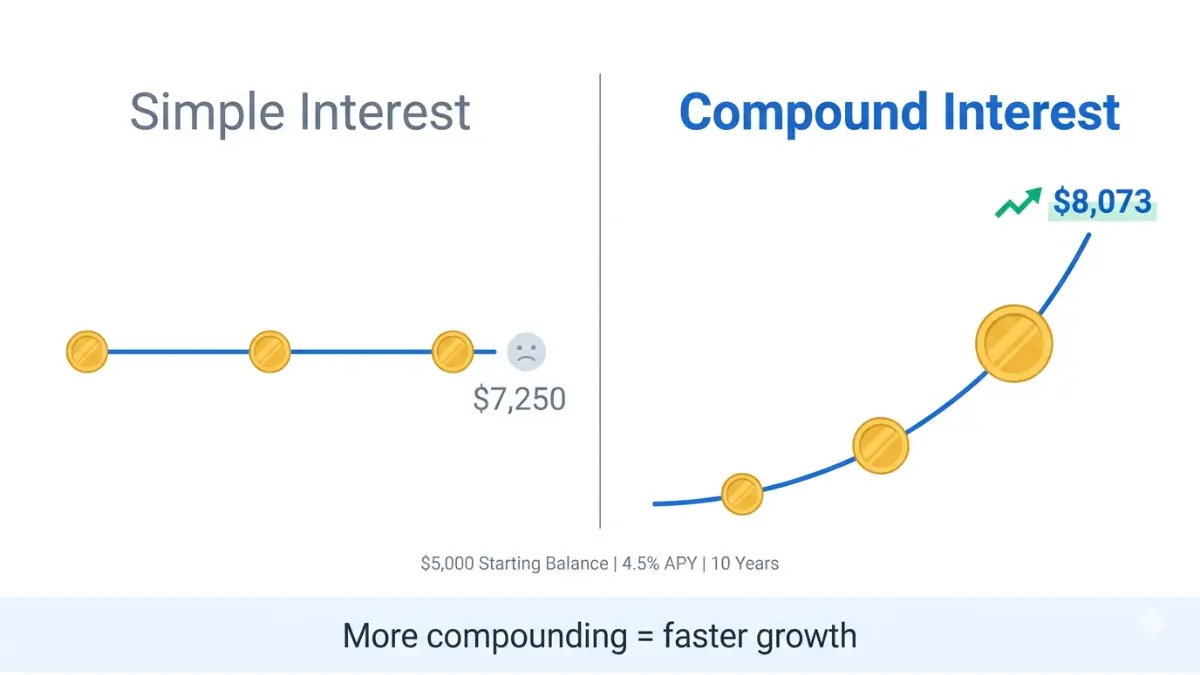

Simple interest only earns on your original deposit. Compound interest earns on your deposit plus all the interest already accumulated. Over time, the gap becomes enormous.

Real Example — $5,000 at 4.5% APY over 10 years:

| Method | Starting Balance | Interest Earned | Ending Balance |

|---|---|---|---|

| Simple Interest | $5,000 | $2,250 | $7,250 |

| Compound (Monthly) | $5,000 | $3,073 | $8,073 |

| Compound (Daily) | $5,000 | $3,093 | $8,093 |

The compounding difference adds $823 with zero extra effort. This is why understanding your savings interest calculator results matters deeply.

To learn more about how compounding works at a foundational level, read our detailed guide on what is compound interest.

What Is APY — And Why It Matters More Than Interest Rate

APY (Annual Percentage Yield) is the number you should always focus on. It reflects the true annual return including compounding. A savings account advertising 4.00% interest compounded daily actually delivers a slightly higher APY of 4.08%.

| Compounding Frequency | Nominal Rate | Effective APY |

|---|---|---|

| Annually | 4.00% | 4.000% |

| Quarterly | 4.00% | 4.060% |

| Monthly | 4.00% | 4.074% |

| Daily | 4.00% | 4.081% |

The Federal Reserve’s official consumer resources at federalreserve.gov explain that comparing APY — not interest rates — is the only valid way to compare savings accounts.

Inflation-Adjusted Savings: What Competitors Don’t Show You

Here’s the number NerdWallet and Bankrate never show: your real savings value. Inflation silently erodes purchasing power every year.

Example: $10,000 growing at 4% APY over 10 years = $14,802 nominal. But at 2.7% inflation (December 2025 CPI), that same balance is only worth $11,366 in today’s dollars.

Our savings calculator shows both numbers. Always check your Real APY to confirm your savings is actually beating inflation.

2026 Savings Rate Reality Check — Are You Earning Enough?

📅 Data Updated: March 2026 — The Fed held the federal funds rate at 3.50%–3.75% at its January 28, 2026 meeting, following three consecutive 25-basis-point cuts in late 2025. The next decision is scheduled for March 18–19, 2026.

National Average vs. High-Yield Savings Accounts (2026)

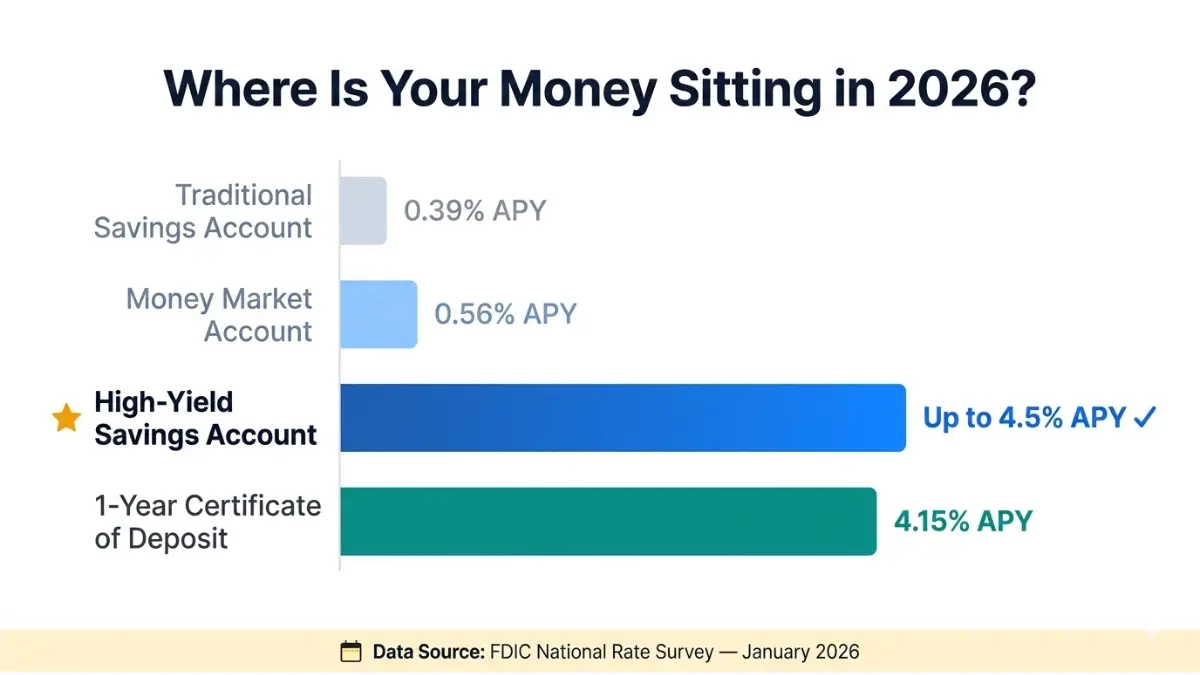

Most Americans are still earning almost nothing on their savings. Here’s where rates actually stand:

| Account Type | National Average APY | Best Available APY (2026) |

|---|---|---|

| Traditional Savings | 0.39% | — |

| High-Yield Savings | ~4.00% | Up to 5.00% |

| Money Market Account | 0.56% | 4.50%+ |

| 1-Year CD | ~4.00% | 4.15% |

| 5-Year CD | ~3.50% | 4.00%+ |

Source: FDIC National Rates — February 2026

The True Cost of Staying at the National Average

Run this in your savings calculator right now. The difference between 0.39% and 4.50% APY on $10,000 over 5 years:

| APY | Starting Balance | Interest Earned | Ending Balance |

|---|---|---|---|

| 0.39% (national avg) | $10,000 | $196 | $10,196 |

| 4.50% (high-yield) | $10,000 | $2,471 | $12,471 |

That’s $2,275 you’re leaving on the table. Every year you stay in a low-rate account is money permanently lost to inaction.

How 2025’s Fed Rate Cuts Affect Your Savings in 2026

Three 25-basis-point Fed rate cuts in late 2025 brought rates to their lowest since 2022. Here’s what that means for your savings:

- High-yield savings accounts still offer 4–5% APY — significantly above inflation

- CD rates have slightly declined but remain competitive at 4–4.15% for 1-year terms

- Traditional bank savings remains near zero — the gap from national average to best rates is now over 4 percentage points

- The Fed is expected to hold or cut rates in 2026 — locking into a CD now may protect your yield

If you’re planning to buy a home after building savings, use our home affordability calculator to set a realistic target savings goal before you start.

Real-World Savings Scenarios — What Your Goals Actually Look Like

Use these benchmarks as direct inputs into your savings calculator with monthly contributions to see exactly how long your goal takes.

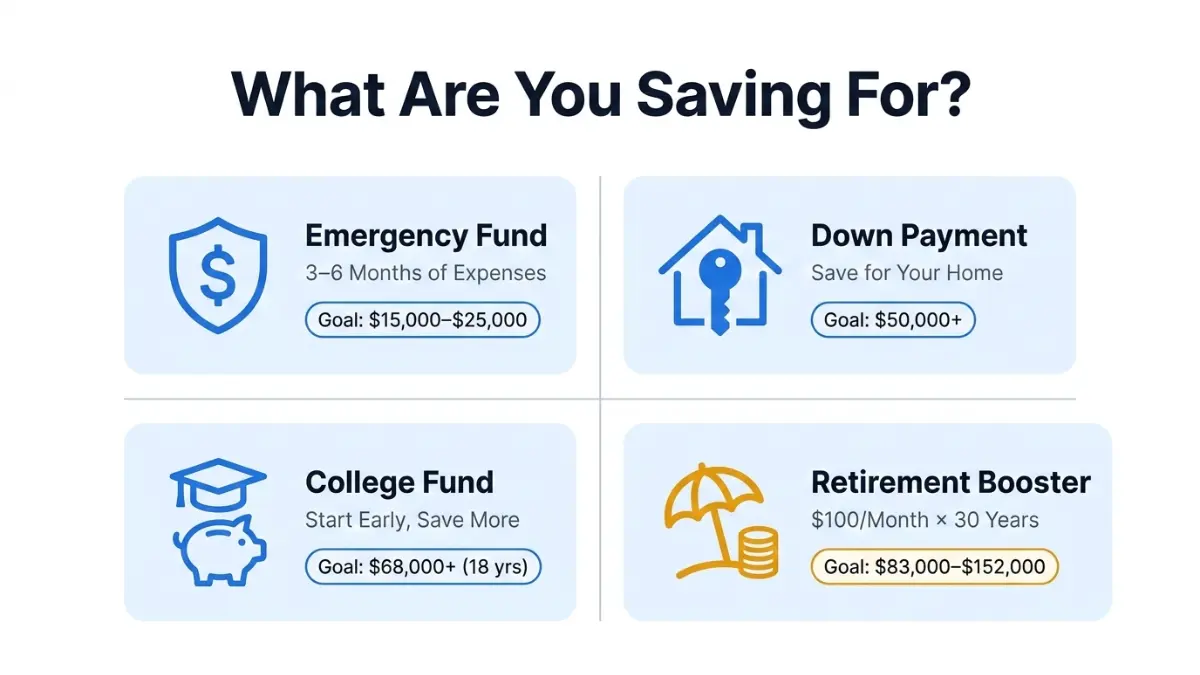

Scenario 1: Emergency Fund (3–6 Months of Expenses)

Financial experts universally agree: build your emergency fund first. The rule is 3–6 months of essential living expenses, kept liquid in a high-yield savings account.

Target: $15,000–$25,000 for the average U.S. household

| Monthly Contribution | APY | 12 Months | 18 Months | 24 Months |

|---|---|---|---|---|

| $500/mo | 4.5% | $6,153 | $9,378 | $12,686 |

| $800/mo | 4.5% | $9,845 | $15,005 | $20,298 |

| $1,000/mo | 4.5% | $12,306 | $18,756 | $25,372 |

For a full framework on how much to keep liquid, read our emergency fund guide.

Scenario 2: House Down Payment ($50,000 Goal)

Saving for a home is one of the most common reasons Americans use a savings goal calculator.

| Monthly Contribution | APY | Time to $50,000 |

|---|---|---|

| $500/mo | 4.5% | ~7.5 years |

| $1,000/mo | 4.5% | ~4 years |

| $1,500/mo | 4.5% | ~2.7 years |

Once your savings goal is within reach, use our mortgage calculator to estimate your monthly payment before you shop.

Scenario 3: College Fund — 18-Year Projection

Starting early makes a massive difference. Here’s what a $5,000 lump sum + $200/month at 4% APY over 18 years delivers:

| Component | Amount |

|---|---|

| Initial Deposit | $5,000 |

| Total Monthly Contributions | $43,200 |

| Total Interest Earned | $19,847 |

| Ending Balance | $68,047 |

The U.S. Department of Education’s Federal Student Aid site outlines grant and aid options that can reduce how much you need to save.

Scenario 4: Retirement Booster — $100/Month Over 30 Years

The most important savings lesson: time is your most powerful compounding variable.

| Scenario | Monthly | APY | Years | Ending Balance |

|---|---|---|---|---|

| Start at 25 | $100 | 5% | 40 yrs | $152,602 |

| Start at 35 | $100 | 5% | 30 yrs | $83,226 |

| Start at 45 | $100 | 5% | 20 yrs | $41,103 |

Starting 10 years earlier nearly doubles your outcome — without saving an extra dollar. Explore how savings fits into your broader retirement picture with our retirement planning guide for your 30s.

Scenario 5: Paying Off Debt vs. Saving First?

If you’re carrying high-interest debt, the math is clear: debt at 20%+ APR costs more than any savings account earns at 4.5%. Pay off high-rate debt first, then redirect that monthly payment into savings. Use our debt consolidation calculator to see your payoff timeline and interest savings.

7 Expert-Backed Strategies to Maximize Your Savings Growth in 2026

Our panel of 30 international credentialed financial experts at financeauthorityhub.com reviewed the most effective, evidence-based savings acceleration strategies for 2026. Here are the seven that move the needle most.

1. Switch to a High-Yield Savings Account Immediately

The difference between 0.39% and 4.5% APY on a $20,000 balance is $822 per year in lost interest. Most high-yield accounts take 10 minutes to open online. There is no valid reason to stay in a traditional savings account in 2026.

2. Automate Your Monthly Contributions

Research from the National Bureau of Economic Research shows that automated savings increases the average household savings rate by 40%. Set a recurring transfer the day after every paycheck — remove human willpower from the equation entirely.

3. Use Start-of-Month Contributions

Our savings calculator lets you toggle between start-of-month and end-of-month contribution timing. Start-of-month contributions earn a full extra month of compound interest per year. Over 10 years at $500/month and 4.5% APY, that timing difference adds approximately $280 in extra interest.

4. Apply the 50/30/20 Rule to Find Your Target

| Monthly Income | 50% (Needs) | 30% (Wants) | 20% (Savings Target) |

|---|---|---|---|

| $3,500 | $1,750 | $1,050 | $700 |

| $5,000 | $2,500 | $1,500 | $1,000 |

| $7,500 | $3,750 | $2,250 | $1,500 |

Not sure your current budget supports 20%? Our 50/30/20 budget analysis breaks down exactly where to find savings in your existing spending.

5. Set a Savings Goal in the Calculator — Then Use the Goal Solver

Most people save randomly. Goal-oriented savers consistently outperform because they have a fixed target creating behavioral commitment. Enter your goal amount in our calculator and use the Goal Solver feature to calculate the exact monthly contribution needed. Then click “Use This Monthly Amount” to instantly recalculate your schedule.

6. Consider CDs to Lock In Today’s Rates

If you have savings you won’t need for 12+ months, a 1-year CD at 4.15% APY provides a guaranteed return, protected by FDIC insurance up to $250,000 per depositor. With the Fed expected to potentially cut rates in 2026, locking in today’s CD rate now protects your yield.

7. Always Monitor Your Real APY, Not Just Nominal Rate

Your savings calculator shows both your nominal APY and your Real APY (inflation-adjusted). In December 2025, CPI inflation was 2.7%. If your savings account earns 4.0% nominal APY, your real return is only about 1.3%. That’s still positive — but it’s the number that reflects actual wealth building.

Savings Calculator FAQs — Answered by Financial Experts

1. What is a savings calculator?

A savings calculator is a free online tool that projects how much money you’ll accumulate over time. It uses your starting balance, monthly contributions, interest rate, and compounding frequency to calculate your future savings balance, total interest earned, and APY.

2. How does compound interest grow my savings?

Compound interest earns returns not just on your original deposit, but on all previously earned interest too. A $10,000 deposit at 4.5% APY compounded monthly becomes $15,530 after 10 years — $5,530 in pure interest with no additional deposits.

3. What is a good APY for a savings account in 2026?

The national average savings APY is 0.39% according to FDIC data as of January 2026. A good APY is 4.00% or higher — easily available through high-yield online savings accounts. Anything above 4.5% is excellent.

4. How much should I save per month?

The 50/30/20 rule recommends saving 20% of your monthly take-home income. If you earn $4,500 per month, target $900 in monthly savings. Start with what’s manageable — consistency matters more than the amount.

5. What’s the difference between APY and interest rate?

The interest rate is the base rate before compounding. APY (Annual Percentage Yield) is the effective annual return including compounding. APY is always equal to or higher than the stated interest rate. Always compare APY when evaluating savings accounts — not the nominal interest rate.

6. How does compounding frequency affect my savings?

More frequent compounding = faster growth. Daily compounding outperforms monthly, which outperforms quarterly, which outperforms annual. Our calculator supports all four. On a $20,000 balance at 4.5% over 10 years, daily compounding earns approximately $60 more than monthly compounding — purely from frequency.

7. What is inflation-adjusted savings value?

It’s the real purchasing power of your future balance in today’s dollars. If your savings grows to $15,000 over 5 years but inflation averages 2.7% annually, that $15,000 only buys what $13,067 buys today. Our calculator shows this automatically in the results panel.

8. How do I calculate the monthly contribution needed to reach my savings goal?

Enter your savings goal in the “Savings Goal” field, then click “Calculate.” The Goal Solver feature automatically calculates the exact monthly contribution required to reach your target within your specified time period. Click “Use This Monthly Amount” to apply it instantly.

9. Are high-yield savings accounts safe in 2026?

Yes. Savings accounts at FDIC-insured banks are federally protected up to $250,000 per depositor, per institution. Your money is safe regardless of market conditions — unlike stocks or mutual funds.

10. What is the 50/30/20 rule for savings?

The 50/30/20 rule allocates 50% of take-home income to needs, 30% to wants, and 20% to savings and debt repayment. It was popularized by Senator Elizabeth Warren in her book All Your Worth and remains one of the most widely used personal finance frameworks.

11. How is this savings calculator different from NerdWallet’s and Bankrate’s?

Most other calculators show only ending balance and basic interest. Ours goes significantly further: 22 currencies, inflation-adjusted real value, Real APY (post-inflation), contribution timing toggle (start vs. end of month), savings goal solver, monthly payment schedule, year-by-year breakdown table, and CSV export. No other free savings calculator available today matches this depth.

⚠️ Disclaimer

This savings calculator and all content on this page are provided for educational and informational purposes only. Results are estimates based on the inputs you provide and assume a fixed interest rate throughout the savings period. Actual savings results will vary based on your bank’s specific terms, compounding method, day-count conventions, fees, and changes to interest rates over time. This content does not constitute financial advice. Always consult a qualified, licensed financial advisor for guidance specific to your situation. financeauthorityhub.com is not a bank, financial institution, or registered investment advisor. Savings account deposits at FDIC-member banks are insured up to $250,000 per depositor — visit FDIC.gov for details.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.