401(k) Calculator: See Exact 2026 Retirement Number

401(k) Calculator

Project your 401(k) balance using contributions, employer match, and compounded returns. Includes inflation-adjusted estimate, yearly table, and CSV export.

Inputs

Defaults are prefilled for convenience.

Results

Years to retirement

—

Est. monthly income (4% rule): —

Projected balance (nominal)

—

Inflation-adjusted: —

Total contributions

Employee: —

Employer: —

Catch-up: —

Estimated investment growth

—

Growth is an estimate.

Yearly projection

| Year | Age | Salary | Employee | Employer | Catch-up | Ending balance |

|---|

Results appear after you click “Calculate.”

In This Article

Use our free 401(k) calculator above to project your exact retirement balance — including employer match, inflation-adjusted value, and yearly growth — in under 60 seconds. Updated with official 2026 IRS contribution limits.

What Is a 401(k) Calculator — and Why 2026 Changes Everything

A 401(k) calculator is a free financial tool that projects your retirement balance based on your salary, contribution rate, employer match, expected investment return, and years until retirement.

Most Americans are dramatically underestimating their retirement number. According to Vanguard’s How America Saves 2025 report, the average 401(k) balance across all ages reached $148,153 in 2024 — but the median was only $38,176. That gap tells a critical story: most people are not using smart contribution strategies.

Here’s why 2026 is a pivotal year for your 401(k):

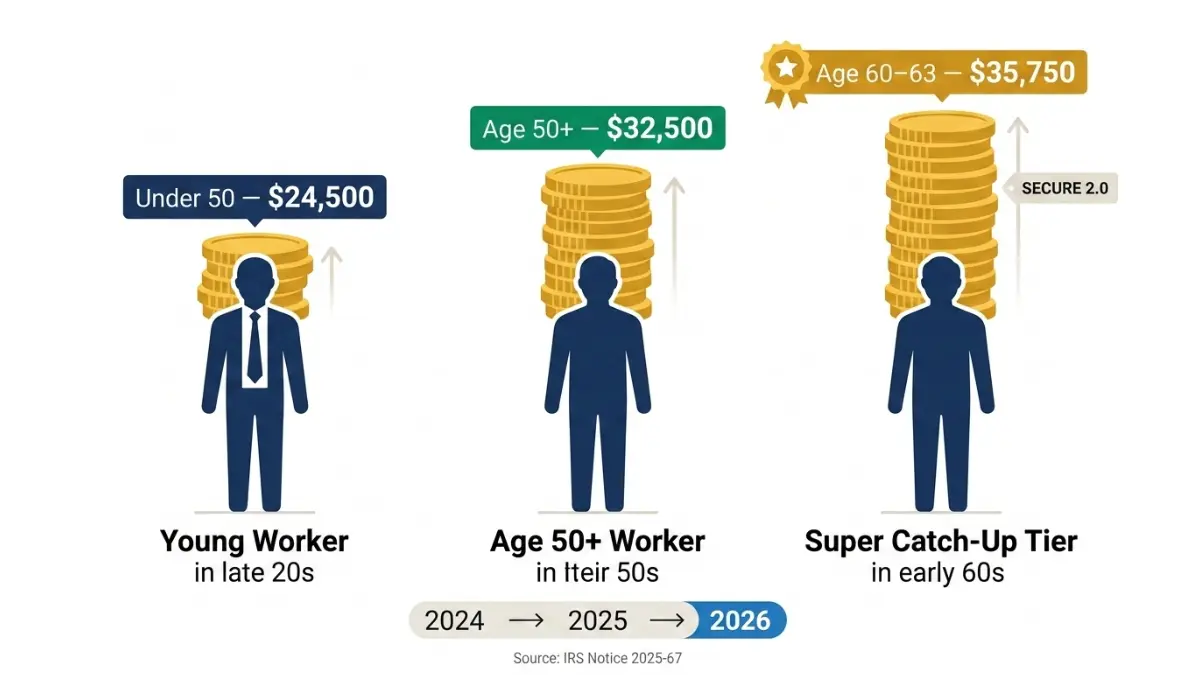

- The IRS raised the standard contribution limit to $24,500 (up from $23,500 in 2025)

- A new “super catch-up” rule under SECURE 2.0 lets workers aged 60–63 contribute up to $35,750 total

- The combined employee + employer limit jumped to $72,000

Use our full financial tools suite to build a complete retirement and savings strategy alongside this calculator.

2026 401(k) Contribution Limits: The Complete Official Breakdown

The IRS officially confirmed all 2026 401(k) limits in Notice 2025-67. Here is the full picture:

Standard Limit (Under Age 50)

You can contribute up to $24,500 of your own salary into your 401(k) in 2026. That is $1,000 more than 2025 — worth tens of thousands of dollars compounded over a career.

Catch-Up Contributions (Age 50 and Older)

Workers aged 50 and above can contribute an extra $8,000 on top of the standard limit in 2026, according to the IRS retirement topics page. That brings the total personal contribution to $32,500.

The Super Catch-Up (Ages 60–63) — What Competitors Miss

This is the most important change most people don’t know about. Under SECURE 2.0, workers aged 60, 61, 62, and 63 qualify for a higher catch-up limit of $11,250 instead of $8,000. Your total personal contribution limit for 2026 reaches $35,750.

This is exactly why our 401(k) calculator includes a dedicated super catch-up field — no other major calculator builds this into a yearly projection table.

2025 vs. 2026 Contribution Limits: Side-by-Side

| Contribution Type | 2025 Limit | 2026 Limit | Increase |

|---|---|---|---|

| Standard (under 50) | $23,500 | $24,500 | +$1,000 |

| Catch-up (age 50+) | $7,500 | $8,000 | +$500 |

| Super catch-up (age 60–63) | $11,250 | $11,250 | No change |

| Total limit (age 60–63) | $34,750 | $35,750 | +$1,000 |

| Annual additions (employee + employer) | $70,000 | $72,000 | +$2,000 |

💡 Key Takeaway: If you are aged 60–63, maximizing the super catch-up in 2026 could add over $300,000 to your final balance by age 70 at a 7% return.

Also worth reading: how a Health Savings Account (HSA) stacks up against your 401(k) for tax savings — a strategy fewer than 10% of Americans use.

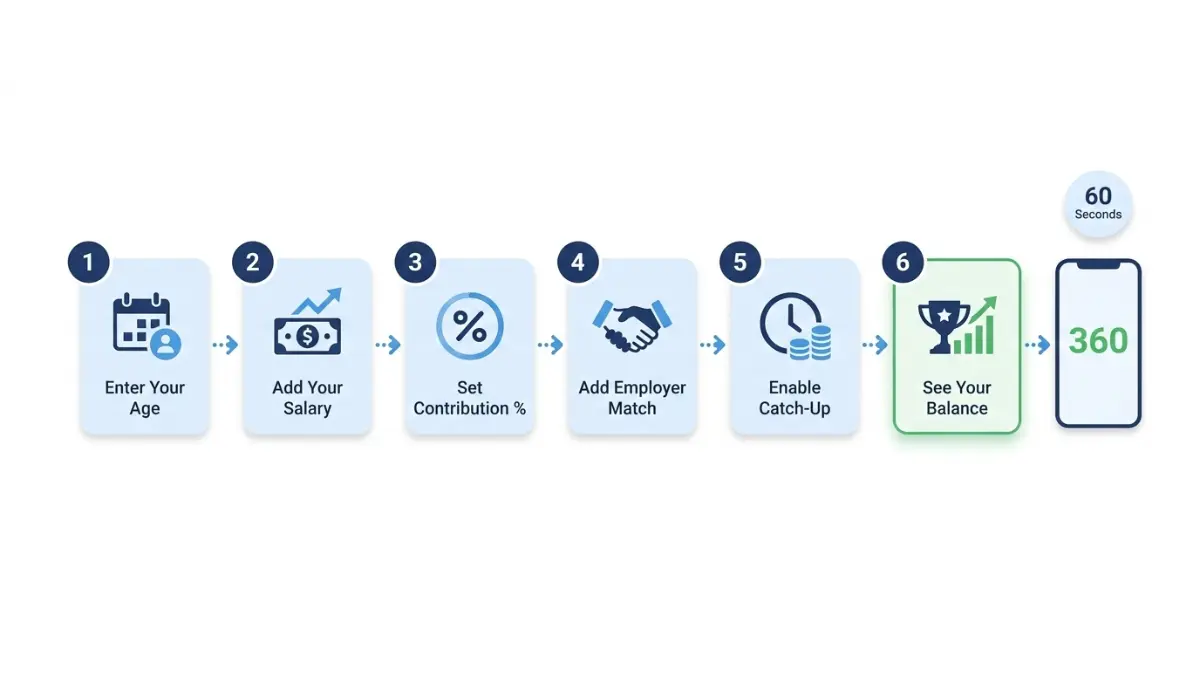

How to Use This 401(k) Calculator: Step-by-Step Guide

None of the top competitors explain how to use their own calculator effectively. This guide closes that gap entirely.

Step 1 — Enter Your Current Age and Retirement Age

Type your current age and the age you plan to retire. Most financial planners target age 65, but full Social Security benefits begin at age 67 for those born after 1960.

Step 2 — Add Your Annual Salary and Salary Growth Rate

Enter your gross annual salary. Then add a salary growth rate — even 2–3% per year makes a significant difference over a 30-year career. Most calculators ignore this field. Ours compounds it year by year.

Step 3 — Set Your Employee Contribution

You can enter either a percentage of salary or a fixed dollar amount per year. The calculator automatically caps your contribution at the 2026 IRS elective deferral limit of $24,500.

Step 4 — Input Your Employer Match Details

Enter two numbers: your employer’s match rate (e.g., 50%) and the salary percentage cap it applies to (e.g., the first 6% of pay). Example: A 50% match on up to 6% of an $80,000 salary = $2,400 in free employer money per year.

Never leave employer match unclaimed. It is the highest guaranteed return available to any worker — instantly 50–100% on contributed dollars.

Step 5 — Set Expected Return and Inflation Rate

Most financial planners use 7% annually as a long-term stock market average return (based on historical S&P 500 data, net of inflation). For a more conservative estimate, use 5–6%. Set your inflation rate at 2.5–3% to see the real purchasing power of your future balance.

Step 6 — Enable Catch-Up Contributions (If Eligible)

Check the catch-up box if you are 50 or older. Enable the super catch-up checkbox if you are aged 60–63. Enter the additional amount you plan to contribute annually in the catch-up field.

Step 7 — Read and Download Your Results

Your results show four critical numbers:

- Projected nominal balance — your raw retirement number

- Inflation-adjusted balance — what that money is worth in today’s dollars

- Estimated monthly income (4% rule) — how much you can withdraw monthly without depleting your savings

- Yearly projection table — a year-by-year breakdown you can download as a CSV file

💡 Real Example: Sarah, age 35, earns $85,000, contributes 10%, receives a 50% employer match on the first 6% of salary, and expects a 7% annual return. With no current balance and 30 years to retire, her projected balance is approximately $1.1 million. Inflation-adjusted to today’s dollars: approximately $546,000 at 2.5% inflation. Estimated monthly income at the 4% rule: $3,667/month.

Average 401(k) Balance by Age in 2026 — Are You on Track?

Data from Vanguard’s How America Saves 2025 — the industry’s most comprehensive retirement study, covering nearly 5 million participants — gives us a clear benchmark.

2026 401(k) Balance Benchmarks by Age

| Age Group | Average Balance | Median Balance | Fidelity “On Track” Target |

|---|---|---|---|

| Under 25 | $6,899 | $1,948 | 0.5x annual salary |

| 25–34 | ~$37,000 | ~$14,000 | 1x annual salary |

| 35–44 | ~$91,000 | ~$35,000 | 2–3x annual salary |

| 45–54 | ~$168,000 | ~$60,000 | 4–5x annual salary |

| 55–64 | ~$244,000 | ~$87,000 | 6–7x annual salary |

| 65+ | $299,442 | $95,425 | 8–10x annual salary |

Source: Vanguard How America Saves 2025 (year-end 2024 data)

💡 Key Takeaway: If your balance is near or above the median for your age group, you are ahead of the typical American saver. If you are below the median, the 2026 limit increases and catch-up rules are your fastest legal path forward.

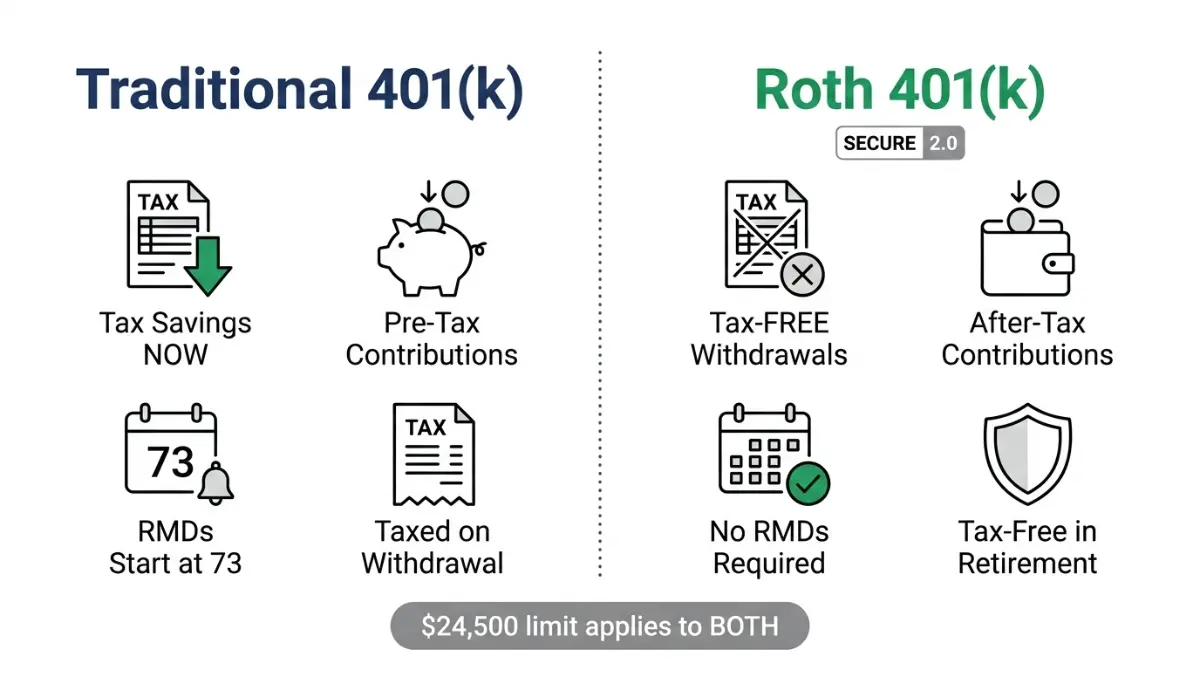

Traditional 401(k) vs. Roth 401(k): Which Is Better for You?

| Factor | Traditional 401(k) | Roth 401(k) |

|---|---|---|

| Tax on contributions | Pre-tax (reduces income now) | After-tax (no deduction now) |

| Tax on withdrawals | Taxed as ordinary income | Tax-free |

| RMDs required? | Yes, starting at age 73 | No RMDs (after SECURE 2.0) |

| Best for | Higher earners now, lower tax bracket in retirement | Younger workers or those expecting higher future taxes |

| 2026 contribution limit | $24,500 | $24,500 (same) |

If you are also weighing Roth IRA vs. 401(k) contributions, our dedicated guide walks through the full tax math.

For a deeper comparison of both account types, see our full 401(k) vs. IRA guide.

If you’re also paying down a mortgage, use our Mortgage Calculator to model whether accelerating payoff or increasing 401(k) contributions produces a better long-term outcome for your specific numbers.

5 Advanced 401(k) Strategies to Retire Richer in 2026

This is the section that no top competitor provides. These are the moves that separate disciplined retirement savers from the majority.

Strategy 1 — Maximize the Super Catch-Up If You Are Aged 60–63

If you are between 60 and 63 in 2026, you have a narrow window that most Americans are not using. Contributing the full $35,750 annually for just three years at 7% return adds over $115,000 to your retirement balance before fees.

This is the single most powerful legal retirement acceleration strategy in the U.S. tax code right now.

Strategy 2 — Use Salary Growth Assumptions Correctly

Most online calculators assume a flat salary forever. Our calculator lets you input a salary growth rate. At 3% annual salary growth, a 35-year-old earning $80,000 will earn approximately $195,000 by age 65. Contribution percentages on that growing salary compound dramatically — a difference of $200,000 or more in final balance versus a flat salary assumption.

Strategy 3 — Understand Your Inflation-Adjusted Balance Before You Retire

A projected balance of $1.2 million in 2055 is not $1.2 million in today’s purchasing power. At 2.5% annual inflation, that balance is worth approximately $560,000 in today’s dollars. Our calculator shows both figures so you can plan realistically — something competitors do not display.

Strategy 4 — Automate Annual Contribution Increases by 1%

The single easiest high-impact move: increase your contribution rate by 1% every year when you get a raise. Most plans allow automatic escalation. A worker who starts at 6% and increases by 1% annually for 10 years ends up at 16% — a level that almost guarantees retirement security without ever feeling a single large pay cut.

Strategy 5 — 401(k) vs. Paying Off Your Mortgage: Which Wins?

This is one of the most searched retirement questions with no clear winner in most articles. The math-based answer: if your mortgage interest rate is below your expected 401(k) return, prioritize the 401(k) first — especially up to the employer match. After maximizing the match, compare your after-tax mortgage rate against your expected return.

Use our Mortgage Refinance Calculator to find your after-tax effective mortgage rate, then compare it against your 401(k) projected return.

Also consider your Savings Calculator to model parallel savings growth alongside your 401(k).

For broader retirement planning strategy, see our expert guide: Retirement Planning in Your 30s and Retirement Savings by Age: 2026 Strategies.

For workers managing student loans alongside retirement savings, our Student Loan Calculator helps model the trade-off between loan payoff speed and 401(k) contributions.

Expert Insight: Our panel of 30 international credentialed financial experts recommends always contributing at least enough to capture the full employer match before directing any extra savings elsewhere — it is the only guaranteed 50–100% immediate return available to workers.

401(k) Calculator: Frequently Asked Questions

1. What does a 401(k) calculator do?

A 401(k) calculator projects your retirement balance using inputs like salary, contribution rate, employer match, expected return, and inflation. It shows both nominal and inflation-adjusted balances so you can plan with realistic purchasing power.

2. What is the 401(k) contribution limit for 2026?

The standard limit is $24,500 for workers under age 50, per the IRS official announcement. Workers aged 50 and older can contribute up to $32,500 with the catch-up addition.

3. What is the super catch-up contribution for ages 60–63 in 2026?

Workers aged 60, 61, 62, or 63 can make a catch-up contribution of $11,250 in 2026 under SECURE 2.0. This brings their total personal limit to $35,750 — the highest ever available for this age group.

4. How does employer match work in a 401(k)?

Your employer contributes additional money to your 401(k) based on how much you contribute — typically matching 50–100% of your contributions up to a cap (e.g., the first 6% of your salary). This is free money that should always be captured first. The Department of Labor provides guidance on how employer plan matching works.

5. What is a good expected rate of return to use?

Most financial planners use 7% per year for a diversified stock portfolio, based on long-term historical S&P 500 performance. For a more conservative projection, use 5–6%. Our calculator lets you adjust this freely.

6. What does the 4% rule mean in the results?

The 4% rule is a widely-used retirement guideline suggesting you can withdraw 4% of your balance annually without running out of money over a 30-year retirement. Our calculator shows you the estimated monthly income this produces from your projected balance.

7. What does inflation-adjusted balance mean?

Inflation-adjusted balance shows what your future retirement balance is worth in today’s purchasing power, accounting for inflation eroding money’s value over time. A $1 million balance in 30 years at 3% inflation is worth about $412,000 in today’s dollars.

8. How much should I have in my 401(k) at age 50?

Fidelity recommends having approximately 6x your annual salary saved by age 50. For someone earning $80,000, that is $480,000. The Vanguard benchmark shows the average 45–54 age group balance is approximately $168,000 — well below this target for most Americans.

9. Can I use this 401(k) calculator for a Roth 401(k)?

Yes. The contribution limits are identical for Traditional and Roth 401(k) plans — $24,500 for under 50 in 2026. The difference is the tax timing, not the contribution cap. The calculator projects your gross balance regardless of account type.

10. What happens to my 401(k) if I change jobs?

Your 401(k) balance belongs to you. When you change jobs, you can leave it in the old plan, roll it into your new employer’s plan, or roll it into a Traditional or Roth IRA. Rolling it over preserves the tax-deferred status and keeps your savings compounding without penalty.

11. When do I have to start withdrawing from my 401(k)?

Under current law, Required Minimum Distributions (RMDs) from Traditional 401(k) accounts must begin at age 73. Failing to take RMDs results in a penalty of 25% of the amount that should have been withdrawn. Roth 401(k) accounts are now exempt from RMDs during the account holder’s lifetime under SECURE 2.0.

📋 Disclaimer: This 401(k) calculator and all content on this page are provided for educational and informational purposes only and do not constitute financial, tax, investment, or legal advice. All projections are estimates based on user-provided inputs and assumed rates of return, which are not guaranteed. Past performance of any investment does not guarantee future results. Contribution limits are based on 2026 IRS guidelines and are subject to change. Please consult a qualified, licensed financial advisor for personalized retirement planning guidance specific to your situation. Reviewed by the financeauthorityhub.com expert panel.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.