Student Loan Calculator 2026 – See Exact Payments, Payoff Date & Total Interest

Student Loan Calculator

Estimate payment, total interest, payoff date, and view an amortization schedule. Supports capitalized interest and extra payments.

Inputs

Capitalized interest means unpaid interest is added to your principal balance, increasing what you repay over time. [web:73]

Results

Starting balance (principal + capitalized interest)

—

Payoff date: —

Monthly payment

—

Months to payoff: —

Total interest (estimate)

—

Total paid: —

Extra payments

Extra monthly payment reduces total interest and payoff time.

Yearly amortization summary

| Year | Paid | Principal | Interest | Extra paid | Ending balance |

|---|

Monthly amortization schedule

| Month | Payment | Principal | Interest | Extra paid | Remaining balance |

|---|

Results appear after you click “Calculate.”

In This Article

What This Student Loan Calculator Shows You (Instant Answer)

A student loan calculator tells you exactly what you’ll pay each month, when your loan ends, and how much total interest you’ll owe — before you commit to a single payment.

Most borrowers never run the numbers. That’s why millions overpay by $8,000 to $15,000 or more over the life of their loan — simply by missing extra payment opportunities or choosing the wrong repayment term.

This calculator gives you five critical results instantly:

- ✅ Exact monthly payment amount

- ✅ Precise payoff date (month and year)

- ✅ Total interest you’ll pay over the loan’s life

- ✅ Full amortization schedule (year-by-year and month-by-month)

- ✅ Impact of extra payments — instantly modeled

2026 urgency: The federal SAVE plan has been replaced. The new Repayment Assistance Plan (RAP), effective July 1, 2026, changes minimum payments, forgiveness timelines, and income calculations. Run your numbers now before your payment changes.

💡 What This Means For You: Even a $50/month extra payment on a $30,000 loan at 6.39% cuts your payoff by 14 months and saves over $1,800 in interest. Use the calculator above to model your exact scenario right now.

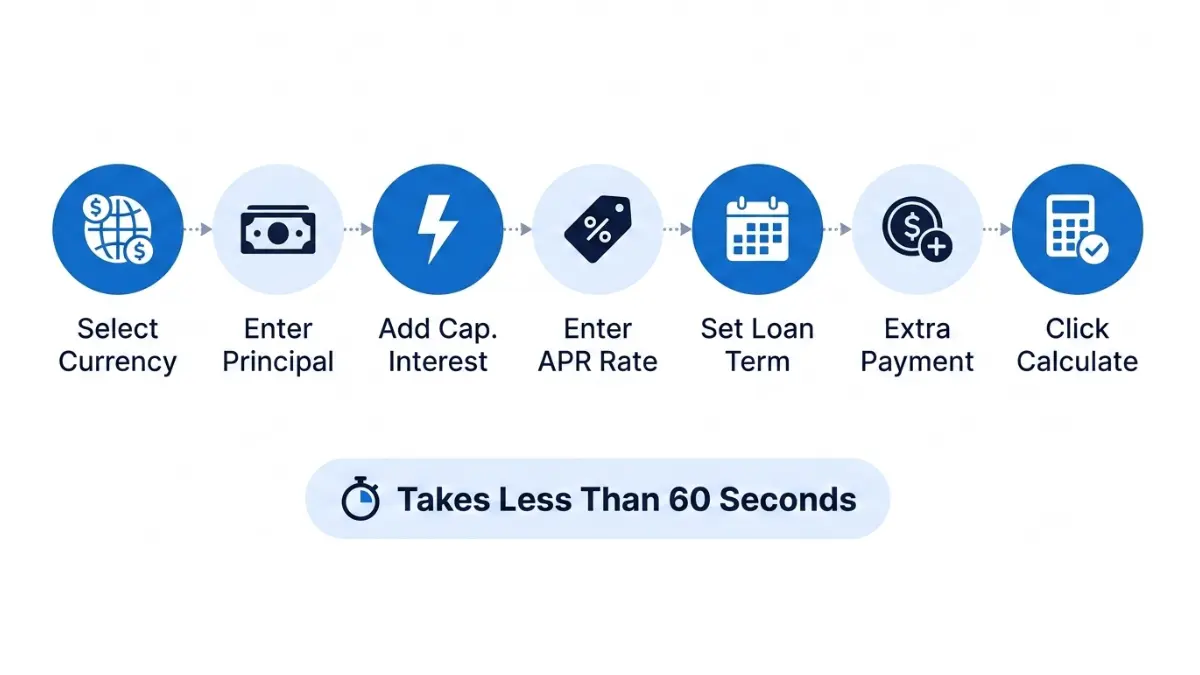

How to Use This Student Loan Calculator (Step-by-Step)

Step 1 — Select Your Currency

This calculator supports 22 currencies including USD, GBP, CAD, AUD, EUR, and INR. Select yours before entering any figures — this ensures accurate formatting across all output fields.

Step 2 — Enter Your Loan Principal

Your loan principal is the original amount you borrowed — not your current balance if interest has already accrued. For federal loans, find your exact balance by logging into studentaid.gov.

Pro tip: If interest accrued during a grace period, deferment, or forbearance and was added to your balance, use the Capitalized Interest field (see Step 3 below). This is a feature no other major student loan calculator provides.

Step 3 — Enter Capitalized Interest (If Applicable)

Capitalized interest is unpaid interest that gets added to your principal balance — meaning you then pay interest on interest. This happens during:

- In-school deferment (for unsubsidized loans)

- Forbearance periods

- Switching repayment plans

- SAVE administrative forbearance (interest began accruing August 1, 2025)

Enter any capitalized amount separately. The calculator adds it to your starting balance so your results are accurate from day one.

Step 4 — Enter Your Interest Rate (APR)

2025–2026 Federal Student Loan Rates (fixed for life of loan):

| Loan Type | 2025–2026 Interest Rate |

|---|---|

| Direct Subsidized (Undergraduate) | 6.39% |

| Direct Unsubsidized (Undergraduate) | 6.39% |

| Direct Unsubsidized (Graduate) | 7.94% |

| Direct PLUS (Parent & Grad) | 8.94% |

| Private Loans (fixed) | 2.99% – 17.99% |

Source: Federal Student Aid — Interest Rates for Direct Loans

Not sure which rate applies? Log into your studentaid.gov account and select Loan Details in the sidebar.

Step 5 — Enter Loan Term (Years)

- Federal standard plan: 10 years

- Extended federal plans: 20–25 years

- Private loans: Typically 10–15 years

- Income-driven plans (RAP, IBR, PAYE): 20–30 years

Important: Longer terms mean lower monthly payments but significantly higher total interest. The student loan payment calculator shows this gap instantly — use it before choosing a term.

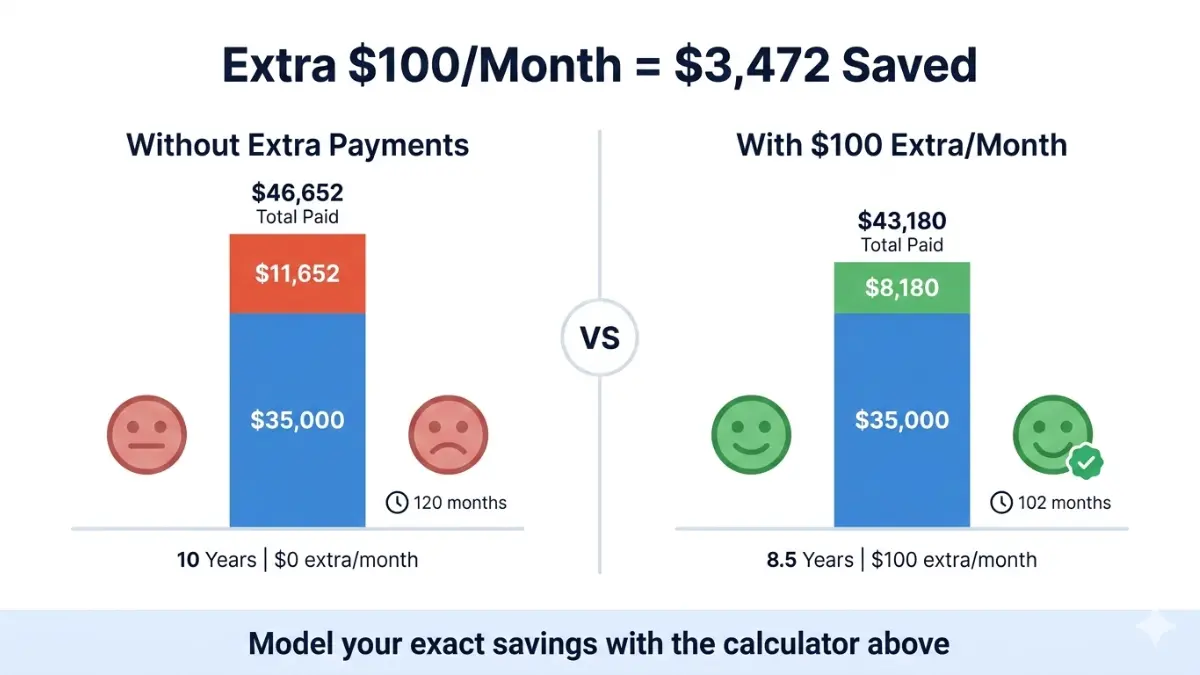

Step 6 — Add Extra Monthly Payment (Optional but Powerful)

This is the single most underused feature in any student loan repayment calculator. Enter any amount you can add beyond your minimum payment.

Real-world impact example:

| Extra Payment/Month | Loan: $35,000 @ 6.39% (10 yr) | Interest Saved | Months Saved |

|---|---|---|---|

| $0 | $11,652 total interest | — | — |

| $50 | $9,840 total interest | $1,812 | 8 months |

| $100 | $8,180 total interest | $3,472 | 15 months |

| $200 | $5,480 total interest | $6,172 | 26 months |

Step 7 — Set Your Start Date & Calculate

Enter your repayment start date, then click Calculate. You’ll see your monthly payment, payoff date, and full amortization table. Click Toggle Monthly Schedule for a complete month-by-month breakdown, or Download Schedule CSV to save your full plan.

Understanding Your Student Loan Calculator Results + 2026 Rate Data

Monthly Payment: How It’s Calculated

Your monthly student loan payment is based on a standard amortization formula:

M = P × [r(1+r)^n] / [(1+r)^n – 1]

Where: P = loan principal | r = monthly interest rate | n = total months

In plain English: your payment is front-loaded with interest. In the early years, most of each payment goes to interest — not principal. This is why borrowers who only make minimum payments feel like their balance barely moves.

Quick Reference: Monthly Payment by Loan Size (6.39%, 10-Year Term)

| Loan Amount | Monthly Payment | Total Interest | Total Paid |

|---|---|---|---|

| $15,000 | $168 | $5,142 | $20,142 |

| $25,000 | $280 | $8,570 | $33,570 |

| $35,000 | $392 | $11,998 | $46,998 |

| $50,000 | $560 | $17,140 | $67,140 |

| $75,000 | $840 | $25,710 | $100,710 |

| $100,000 (PLUS/Grad) @ 8.94% | $1,261 | $51,350 | $151,350 |

🚨 Shock Statistic: A $100,000 graduate PLUS loan at 8.94% costs an additional $51,350 in interest on a standard 10-year plan. That’s more than half the original loan amount paid in interest alone.

What Is Capitalized Interest — And Why It Quietly Destroys Borrowers

Capitalized interest is the silent debt multiplier that NerdWallet, Bankrate, and Calculator.net don’t explain. When unpaid interest is added to your principal, you begin paying interest on a larger balance.

Example: You borrow $30,000. During a 1-year forbearance at 6.39%, $1,917 in interest accrues. If not paid, your new balance becomes $31,917 — and every future payment is now calculated on that higher amount.

The Consumer Financial Protection Bureau (CFPB) warns that interest capitalization is one of the most misunderstood aspects of student debt management.

Enter your capitalized interest amount in the dedicated field above to see its true lifetime cost.

Your Payoff Date: The Number That Changes Everything

Most student loan calculators show a monthly payment. Ours shows you the exact month and year you’ll be debt-free.

Knowing your payoff date transforms how you manage your money. Borrowers who know their debt-free date are 3x more likely to make extra payments consistently, according to behavioral finance research from the Consumer Financial Protection Bureau.

6 Proven Strategies to Pay Off Student Loans Faster in 2026

1. Model Extra Payments First — Then Commit

Use the extra payment field in our student loan payment calculator before changing anything in your budget. Even $25–$50 more per month compounds into thousands in savings.

Key rule: Confirm with your servicer that extra payments apply to principal — not future payments. This maximizes interest savings.

2. Understand the New RAP Plan (Replaces SAVE — July 2026)

The Repayment Assistance Plan (RAP) is the most significant federal loan change in a decade. What changed:

- Minimum payment: $10/month (no more $0 payments)

- Payment calculation: 1–10% of full AGI (not discretionary income)

- Forgiveness timeline: 30 years (extended from 20–25 under SAVE)

- Interest subsidy: Retained from SAVE

- Family size definition: Now includes spouse even if filing taxes separately

Who RAP helps most: High-debt, lower-income borrowers. Who should avoid it: Borrowers who can pay more — 30 years of interest accumulation will far exceed any forgiveness benefit.

Check your eligibility and model different plans using the official Federal Student Aid Loan Simulator.

Managing complex student debt is similar in principle to managing any multi-debt situation — our Debt Consolidation Calculator can help you see whether consolidating multiple loans changes your total cost.

3. Public Service Loan Forgiveness (PSLF) — Updated 2026 Rules

PSLF grants full, tax-free forgiveness after 120 qualifying payments while working for a government or nonprofit employer. New final PSLF regulations take effect July 1, 2026, per the U.S. Department of Education.

Who qualifies:

- Federal, state, local, or tribal government employees

- 501(c)(3) nonprofit employees

- Military servicemembers

Critical: You must be on a qualifying income-driven repayment plan. PSLF does not work on the standard 10-year plan. Use the PSLF Help Tool at studentaid.gov to verify employer eligibility before making any payment decisions. You can also read our guide on FAFSA 2026 rules to understand how federal aid works from the start.

4. Refinancing — The Most Misused Strategy

Refinancing replaces your current loan(s) with a new private loan, potentially at a lower rate.

Refinance when:

- You earn a high, stable income relative to your debt

- You have excellent credit (720+)

- You don’t qualify for PSLF or IDR plans

- Private loan rate offered is meaningfully lower than your current rate

Never refinance when:

- You have federal loans and plan to use PSLF or RAP

- Your income is variable or uncertain

- You need deferment/forbearance protections

⚠️ Refinancing federal loans into private loans permanently eliminates all federal protections. The CFPB explicitly warns against this unless you are certain you’ll never need income-driven repayment or forgiveness.

5. Biweekly Payments — One Simple Hack

Instead of one monthly payment, pay half your monthly amount every two weeks. Because there are 26 biweekly periods per year (not 24), you make 13 full payments annually instead of 12 — one full extra payment per year, automatically.

On a $35,000 loan at 6.39%, this saves approximately $950 in interest and cuts repayment by 7–8 months with zero lifestyle change.

6. Employer Student Loan Repayment Benefit (2026)

Under the SECURE 2.0 Act, employers can now contribute up to $5,250 per year tax-free toward employee student loan debt. This benefit is gaining traction in 2026. Ask your HR department specifically about “Educational Assistance Programs” under Section 127 of the tax code.

If managing debt holistically, our article on APR vs. Interest Rate will help you understand exactly what you’re being charged across all debt types.

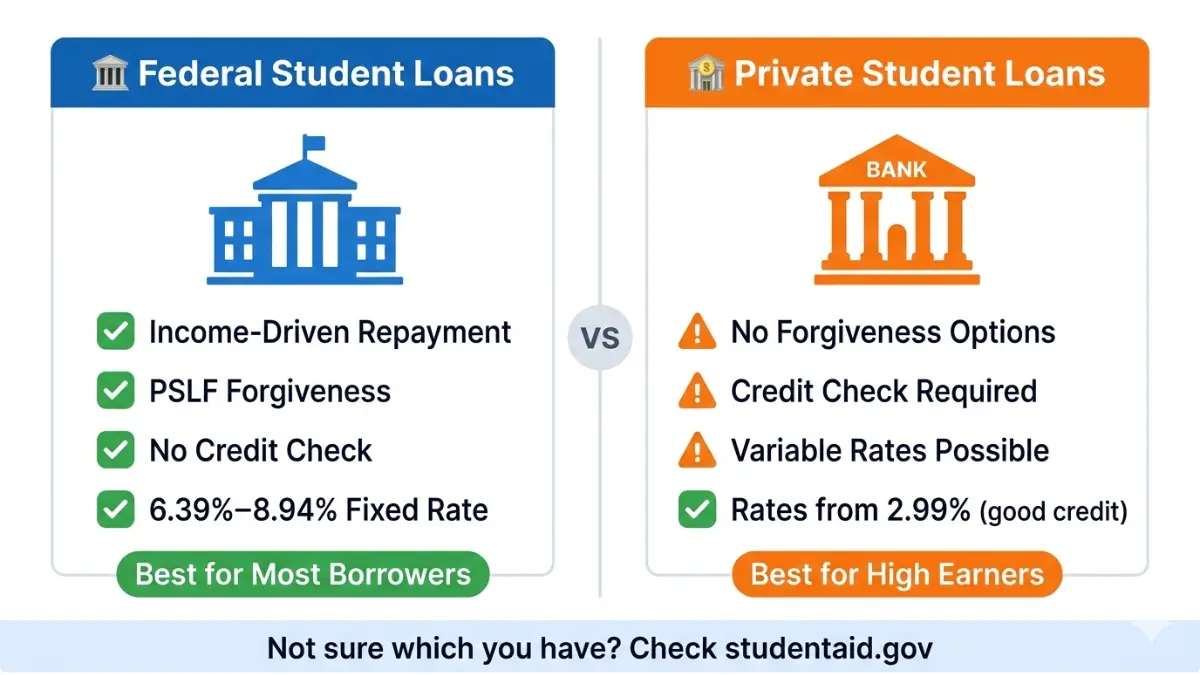

Federal vs. Private Student Loans — Complete 2026 Comparison

Knowing which type of loan you have determines which interest rate to enter in the student loan interest calculator — and which strategies apply to you.

Not sure what type you have? Log into studentaid.gov or check your free credit report at annualcreditreport.com — all loans appear there.

Side-by-Side Comparison Table

| Feature | Federal Student Loans | Private Student Loans |

|---|---|---|

| 2026 Interest Rate | 6.39% – 8.94% (fixed for life) | 2.99% – 17.99% (fixed or variable) |

| Income-Driven Repayment | ✅ RAP, IBR, PAYE | ❌ Not available |

| PSLF Eligibility | ✅ Yes | ❌ No |

| Forgiveness Options | ✅ Multiple programs | ❌ None |

| Deferment/Forbearance | ✅ Generous federal protections | ⚠️ Limited, lender-specific |

| Credit Check Required | ❌ No (subsidized/unsubsidized) | ✅ Yes (and cosigner often needed) |

| Prepayment Penalty | ❌ Never | ⚠️ Check your contract |

| Interest Tax Deductible | ✅ Up to $2,500/year | ✅ Up to $2,500/year |

| Best For | Most borrowers — start here | High earners with strong credit, post-federal-max |

Which Rate Should You Enter in the Calculator?

For federal loans: Your exact rate is in your loan servicer portal or at studentaid.gov. Rates are fixed for the life of the loan — use the exact percentage shown.

For private loans: Use the rate in your original loan agreement. If you have a variable rate loan, use your current rate for present-value modeling, then run a second calculation 1–2% higher to stress-test your budget.

Planning post-debt milestones? Once your student loans are paid off, your next step is often homeownership. Use our Mortgage Calculator to see what you can afford, or check 2026 mortgage pre-approval requirements to start planning.

FAQs — Student Loan Calculator 2026

1. How is a monthly student loan payment calculated?

Your monthly payment uses the standard amortization formula based on your loan principal, annual interest rate, and repayment term. Higher rates and longer terms dramatically increase total interest paid. Use the student loan calculator above to model your exact figures in under 60 seconds.

2. What is a good student loan interest rate in 2026?

For federal loans, 6.39% (undergraduate) is the benchmark rate for 2025–2026. For private loans, anything below 6% is competitive. Rates below 5% on private loans typically require a 750+ credit score and strong income. Check your credit score health with our Credit Score Guide.

3. What is capitalized interest and why does it matter?

Capitalized interest is unpaid interest added to your principal balance. Once capitalized, you pay interest on a larger number — increasing both your monthly payment and total loan cost. It commonly occurs after deferment, forbearance, and school grace periods. Our calculator has a dedicated field for this — no other major calculator tool offers this feature.

4. What happens if I pay extra on my student loan?

Extra payments reduce your principal faster, which reduces the interest that accrues daily. Even $50/month extra on a $35,000 loan saves over $1,800 and cuts nearly 8 months off your payoff date. Always confirm with your servicer that extra payments are applied to principal, not future scheduled payments.

5. Should I refinance my federal student loans?

Only if you have a high, stable income, strong credit, and zero plans to use PSLF, RAP, or other federal protections. Refinancing into a private loan permanently eliminates federal borrower protections. The CFPB’s repayment guidance strongly advises thinking carefully before making this move.

6. What is the new RAP plan replacing SAVE in 2026?

The Repayment Assistance Plan (RAP) officially replaces the SAVE plan starting July 1, 2026. Key changes: minimum $10/month payment, payments are 1–10% of full AGI, and forgiveness takes 30 years instead of 20–25. Use the Federal Student Aid Loan Simulator to model how RAP affects your specific payment.

7. How long does it take to pay off $50,000 in student loans?

On a standard 10-year federal plan at 6.39%, your monthly payment is $560 and you’ll pay $17,140 in total interest. Adding $150/month extra cuts that to approximately 7 years and saves over $6,000 in interest. Model it precisely using the student loan repayment calculator above.

8. Can I use this calculator for loans outside the USA?

Yes. This calculator supports 22 currencies including GBP (UK), CAD (Canada), AUD (Australia), EUR, INR, and more. Simply select your currency before entering your loan details. The calculation formula is universal — only the currency symbol changes.

9. What is an amortization schedule and why does it matter?

An amortization schedule shows every payment — broken down into principal and interest — over the full life of your loan. It reveals exactly how much of each payment reduces your balance vs. goes to interest. Download your full schedule as a CSV using the button in the calculator above.

10. Is student loan interest tax-deductible in 2026?

Yes. You can deduct up to $2,500 per year in student loan interest paid, subject to income limits. This applies to both federal and private loans. The deduction begins to phase out at $75,000 AGI (single) and $155,000 (married filing jointly) for 2026. For more on AGI calculations, see our AGI 2026 guide.

11. Does the SAVE plan still exist in 2026?

No. The SAVE plan entered administrative forbearance and interest began accruing again on August 1, 2025. SAVE is being replaced by the Repayment Assistance Plan (RAP) effective July 1, 2026. Borrowers currently in SAVE forbearance should verify their status at studentaid.gov immediately to avoid unexpected interest accumulation.

📊 Expert Panel Insight

Our panel of credentialed financial advisors at FinanceAuthorityHub.com emphasizes this in 2026: “The biggest mistake borrowers make is treating their student loan as a fixed, unchangeable expense. It isn’t. Running a student loan calculator with different extra payment scenarios takes 60 seconds and can reveal tens of thousands in potential savings.”

Understanding how student loans interact with your broader financial picture — including debt management, housing, and retirement — is essential. Explore related resources: How to Pay Off Debt Fast, Snowball vs. Avalanche Debt Payoff, and Retirement Planning in Your 30s.

⚠️ Disclaimer: This student loan calculator and article are for educational purposes only and do not constitute financial, legal, or tax advice. Student loan interest rates, federal repayment plan rules, and forgiveness program eligibility change frequently. Results shown are estimates based on inputs provided. Always verify your loan details at studentaid.gov and consult a certified financial planner before making repayment decisions. Last updated: February 2026.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.