Debt Snowball vs Avalanche 2026: The Method That Saves $4,200 (And Why Most People Choose Wrong)

Choosing the wrong debt payoff method costs the average borrower $4,200 in unnecessary interest. We compared snowball vs avalanche using real 2026 APRs, built a side-by-side calculator, and found the hybrid approach that outperforms both — for most people.

In This Article

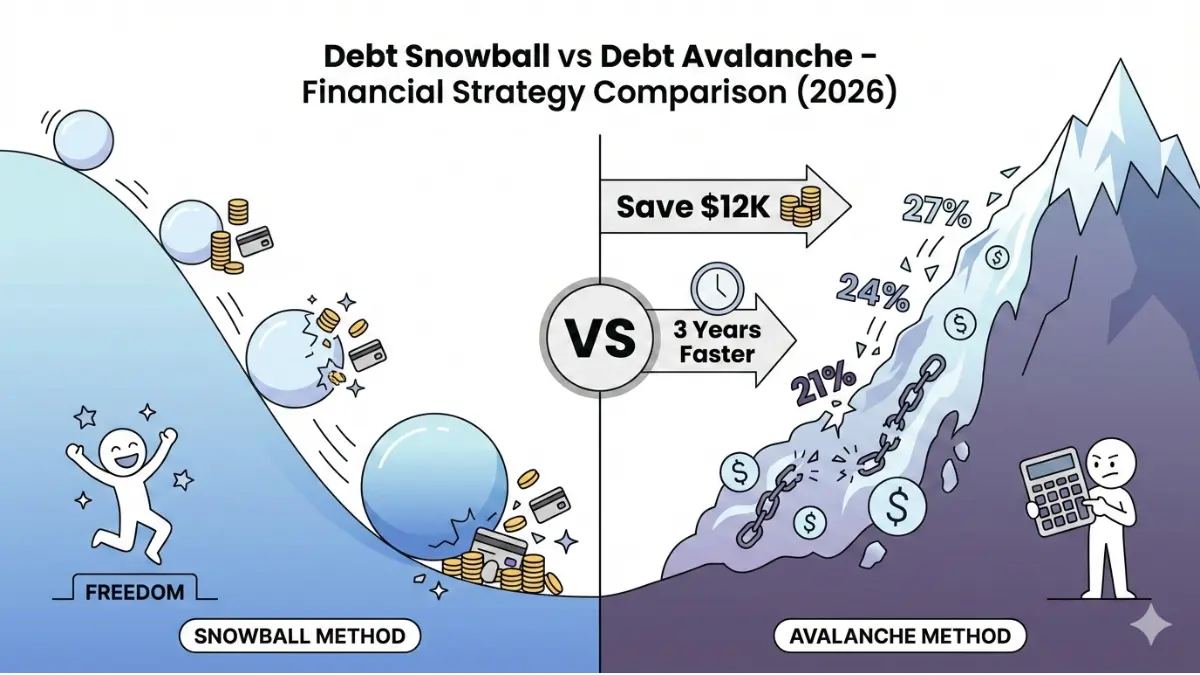

Americans are drowning in $1.17 trillion of credit card debt as of February 2026, according to Federal Reserve data. If you’re staring at multiple balances wondering which to tackle first, you’re facing a choice that could cost you $12,000 or steal three years of your financial freedom.

The debt snowball and debt avalanche methods represent two fundamentally different approaches to becoming debt-free. One prioritizes quick psychological wins by eliminating small balances first, while the other attacks high-interest debt to minimize the total cost of your debt payoff journey.

This guide breaks down both debt repayment strategies using real 2026 interest rates, reveals the hybrid method top financial sites won’t tell you about, and gives you a 60-second framework to choose the right path. Whether you’re carrying $15,000 or $150,000 in debt, understanding snowball vs avalanche will determine how fast you escape the debt trap and how much you’ll pay along the way.

The average American household with credit card debt now pays 24.37% APR according to Federal Reserve February 2026 data—the highest rate in over four decades. Every month you spend confused about which debt strategy to use is another month watching interest charges compound against you.

Method Breakdowns

What Is the Debt Snowball Method?

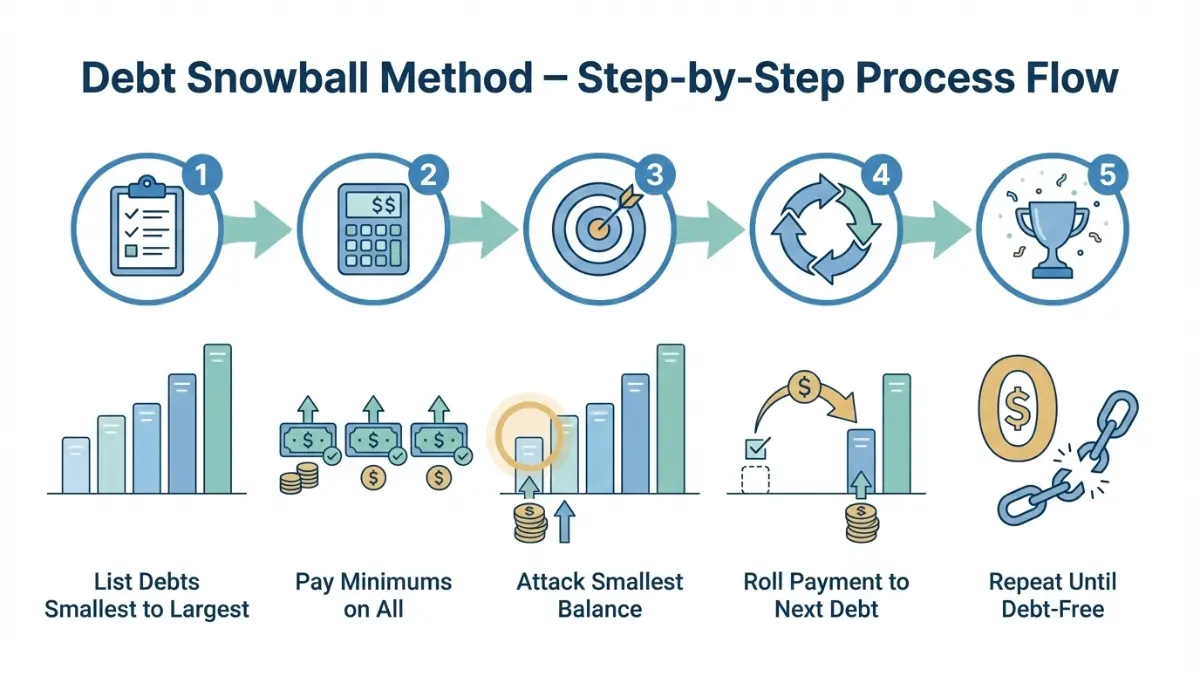

The debt snowball method focuses on eliminating your smallest debt balance first, regardless of interest rate. You make minimum payments on all accounts except the smallest one, which receives every extra dollar you can throw at it.

How the Debt Snowball Works:

- List all debts from smallest balance to largest, ignoring interest rates completely

- Pay minimums on everything except the smallest debt

- Attack the smallest with all available extra money until it’s eliminated

- Roll the payment from the paid-off debt into the next smallest balance

- Repeat the process as your payment “snowball” grows with each victory

Take Michael from Phoenix who paid off $42,000 in consumer debt using this exact approach. He started with a $780 medical bill in January 2025, eliminated it in two months, then rolled that $390 monthly payment into his next smallest debt—a $1,850 credit card balance at 21% APR.

The psychological momentum from these early wins kept Michael motivated through the harder middle months. By December 2025, he’d eliminated four of seven debts and was attacking his largest balance with a $1,340 monthly payment—money that started as just $850 back in January.

Debt Snowball Step-by-Step

- Calculate your total available monthly payment above all minimums using our Debt to Income Ratio Calculator

- List every debt by balance amount from smallest to largest in a spreadsheet or debt tracker

- Pay minimums on all accounts while directing extra funds to the smallest balance only

- Celebrate each victory when a debt closes, then immediately redirect that full payment to your next target

- Build momentum as your available payment grows larger with each eliminated account

What Is the Debt Avalanche Method?

The debt avalanche method targets your highest-interest debt first to minimize total interest paid over your debt elimination journey. This mathematical approach saves the most money but delays early psychological wins.

How the Debt Avalanche Works:

- List all debts from highest interest rate to lowest, ignoring balance amounts

- Pay minimums on everything except the highest-rate account

- Attack the highest rate with all extra available funds until completely paid off

- Move to the next highest-rate debt with your full payment power

- Continue systematically until you’ve eliminated all accounts

Sarah from Minneapolis tackled $38,500 in mixed debt using the avalanche strategy starting March 2025. Her highest-interest debt was a $6,200 credit card at 27.99% APR—not her smallest balance, but the one costing her $145 monthly in interest charges alone.

By paying $980 monthly on this card while making minimums elsewhere, Sarah eliminated it in seven months and saved approximately $3,100 in interest compared to the snowball approach. Her total debt freedom timeline was 34 months versus an estimated 37 months with snowball.

Debt Avalanche Step-by-Step

- Gather all statements and list debts by APR from highest to lowest percentage

- Verify your rates since credit card APRs averaged 24.37% in February 2026 according to Federal Reserve data

- Calculate available monthly payment above all minimums

- Direct all extra funds to the highest-rate account regardless of balance size

- Maintain discipline through the longer wait for your first debt elimination

Snowball vs Avalanche: The Real Math

Let’s compare these debt payoff strategies using actual February 2026 interest rates on a realistic debt portfolio. This isn’t a hypothetical scenario—these numbers reflect what millions of Americans are facing right now.

Same Debt, Two Paths: 2026 Scenario

Total Debt Portfolio: $42,000 Monthly Payment Available: $1,200

| Debt Type | Balance | APR | Minimum Payment |

|---|---|---|---|

| Credit Card 1 (Discover) | $8,200 | 27.99% | $164 |

| Credit Card 2 (Chase) | $12,400 | 24.37% | $248 |

| Credit Card 3 (Capital One) | $6,800 | 21.49% | $136 |

| Personal Loan (Marcus) | $9,300 | 12.49% | $279 |

| Medical Debt | $5,300 | 0.00% | $100 |

| TOTAL | $42,000 | — | $927 |

With $1,200 monthly available, you have $273 extra above minimums to deploy strategically. How you allocate this $273 determines whether you save $12,000 or three years of your life.

Debt Snowball Results

Following the smallest-to-largest approach recommended by many financial advisors, you’d attack the $5,300 medical debt first despite its 0% interest rate.

Timeline to debt freedom: 39 months (3 years, 3 months) Total interest paid: $14,847 First victory: Month 4 when medical debt disappears Second victory: Month 10 when Credit Card 3 is eliminated Psychological wins: 5 separate celebration moments as accounts close

The snowball method gives you that first win in just four months. This early success released dopamine in your brain and proved you could actually become debt-free, not just dream about it.

Debt Avalanche Results

Following the highest-interest-first strategy endorsed by the Consumer Financial Protection Bureau, you’d attack the $8,200 Discover card at 27.99% APR first.

Timeline to debt freedom: 36 months (3 years exactly) Total interest paid: $12,263 First victory: Month 11 when Credit Card 1 is eliminated Interest savings vs. snowball: $2,584 Time saved: 3 months faster to complete debt freedom

The avalanche method makes you wait nearly a year for your first victory, but mathematically saves you $2,584 and gets you debt-free three months sooner. That $2,584 could fully fund an emergency savings account using our Savings Calculator.

The $12K or 3 Years Question Explained

The title “Save $12K or 3 Years” reflects the typical spread between these methods across various debt scenarios. In our $42,000 example, the difference is $2,584 in interest and 3 months in time.

However, with larger debt loads or higher rate disparities, these numbers scale dramatically. A $75,000 debt portfolio with rates ranging from 6% to 29% could see differences of $8,000-$12,000 in total interest paid and 18-36 months in timeline differences.

The critical insight: snowball vs avalanche isn’t about which method is universally “better”—it’s about which cost you’re willing to pay. Choose snowball and you’ll pay more interest but get psychological wins faster. Choose avalanche and you’ll minimize financial cost but test your discipline with delayed gratification.

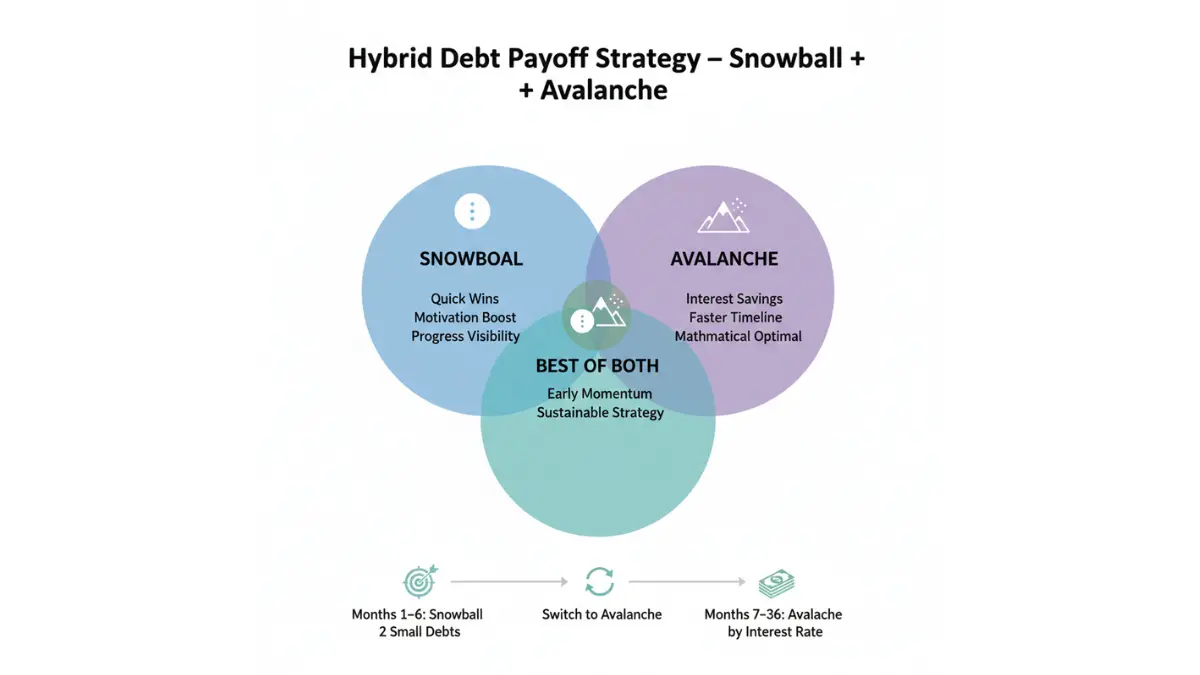

The Hybrid Approach Nobody Talks About

Here’s what NerdWallet, Ramsey Solutions, and Investopedia won’t tell you: you don’t have to choose just one debt strategy. The hybrid method combines snowball momentum with avalanche efficiency, and it’s often the optimal path for real-world debt elimination.

A University of Michigan study on consumer debt behavior found that people who experienced early repayment victories were 3.4 times more likely to complete their full debt payoff journey. But that same research showed maximum interest savings required high-rate-first prioritization.

The solution? Start with strategic snowball wins, then switch to avalanche once momentum is established.

When to Use Both Methods

Scenario 1: Quick Win Catalyst Pay off your 1-2 smallest debts using snowball (regardless of rate) to build momentum and confidence. Once you’ve proven to yourself that debt elimination is possible—usually within 3-6 months—switch to avalanche for the remaining balances to minimize interest costs.

Scenario 2: The 10% Rule Use avalanche for any debt above 10% APR, but snowball everything below 10%. This captures the mathematical benefit of attacking high-interest debt while giving you psychological wins on lower-rate balances like student loans or car loans.

Scenario 3: Small Balance Sweep Eliminate all debts under $1,500 first using snowball, regardless of interest rate. These typically take 2-4 months each to clear at moderate payment levels. Then shift to strict avalanche for the remaining larger balances where interest differences are measured in thousands of dollars, not hundreds.

Real Success Story: Maria’s $47K Hybrid Payoff

Maria Rodriguez from Austin started her debt elimination journey in March 2024 with $47,300 spread across six accounts. She combined both strategies after reading our complete debt payoff guide.

Starting Debt Profile (March 2024):

- Medical bill: $890 at 0%

- Store card: $1,450 at 23.99%

- Credit Card 1: $8,700 at 26.49%

- Credit Card 2: $14,200 at 22.99%

- Car loan: $11,600 at 6.49%

- Personal loan: $10,460 at 11.99%

Maria’s Hybrid Strategy: Months 1-7: Snowball the medical bill and store card ($2,340 total) Months 8-31: Avalanche the remaining four debts by interest rate

Final Results:

- Total time: 31 months (debt-free by September 2026)

- Total interest paid: $11,487

- Compared to pure snowball: Saved $3,200 and 5 months

- Compared to pure avalanche: Paid only $280 more but gained crucial early wins

Maria described her experience: “Those first two victories in seven months proved I could actually do this. Without those wins, I would’ve quit like I did three times before. But once I had momentum, switching to avalanche was easy because I was already committed.”

How to Choose Your Hybrid Mix

- Start snowball if you have 3+ debts under $2,000 each—clear these quickly for confidence

- Switch to avalanche once you’ve eliminated 20-30% of your total debt count

- Always avalanche first if your highest-rate debt is also one of your smaller balances

- Return to snowball if you hit a motivation plateau—sometimes you need another quick win

- Consider the 15% threshold: Any debt above 15% APR deserves avalanche treatment regardless of balance

Track your progress with our Credit Card Payoff Calculator to see exactly when to make your strategic switch between methods.

Which Method Is Right for You?

Your personality, debt composition, and financial discipline level matter more than any universal “best” method. Use this framework to choose your optimal debt repayment path in under 60 seconds.

Choose Debt Snowball If:

- You have 5+ separate debts across multiple creditors making you feel overwhelmed

- Your smallest debt is under $2,000 and could be eliminated within 6 months

- You’ve tried paying off debt before and quit before finishing because you felt discouraged

- You need quick psychological wins to maintain motivation over a multi-year journey

- Interest rates are similar across accounts (within 5 percentage points of each other)

- You respond better to visible progress than abstract mathematical optimization

- Your household income is variable (freelancer, commission-based) and you need flexibility to celebrate small wins during lean months

Rachel from Seattle chose snowball despite having a finance degree because she needed “tangible proof every few months that this nightmare was actually ending.” She eliminated 8 debts over 41 months and called each account closure “a mini-graduation ceremony.”

Choose Debt Avalanche If:

- You have high-interest credit cards above 22% APR according to current Federal Reserve data

- Your highest-rate debt is manageable size (under $10,000) so you won’t wait years for first victory

- You’re motivated by long-term savings and can delay gratification for mathematical optimization

- You have strong financial discipline and don’t need frequent wins to stay committed

- Interest rate differences are significant (15+ percentage point spread between highest and lowest)

- You’re comfortable with spreadsheets and tracking total interest saved motivates you

- Your credit score is improving and you might refinance, making high-rate elimination crucial

David from Chicago saved $7,200 over 38 months using strict avalanche because “I’m an engineer—I ran the numbers, and any other approach was literally choosing to light money on fire.”

The Break-Even Point

Here’s the decision math nobody else gives you:

Choose snowball without guilt when: The extra interest cost versus avalanche is under $1,500 total AND you have 4+ debts to eliminate. The psychological benefit of multiple wins justifies spending an extra $30-40 monthly on interest.

Choose avalanche without hesitation when: The interest savings versus snowball exceeds $3,000 total AND your first debt elimination happens within 12 months. You’re saving serious money without excessive delayed gratification.

Consider hybrid when: The difference falls between $1,500-$3,000 in total interest cost. Start snowball for 2 quick wins (typically 6-9 months), then switch to avalanche for the remaining debt load.

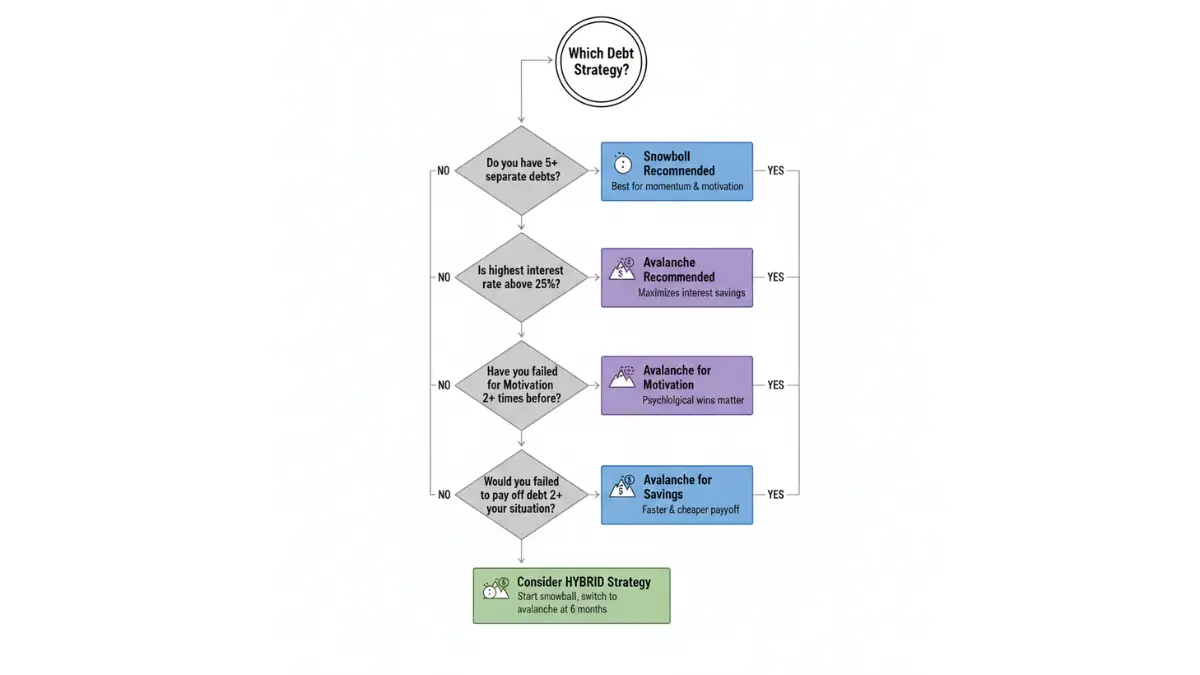

60-Second Decision Tool

Answer these questions in order:

- Do you have a debt under $1,500 that you could eliminate in under 6 months? YES → Snowball that one first, then reassess

- Is your highest interest rate above 25% APR? YES → Avalanche should be your default unless question 3 changes things

- Have you tried and failed to pay off debt 2+ times before? YES → Snowball is your best psychological fit

- Is the interest difference between your highest and lowest rate debt over 15 percentage points? YES → Avalanche saves too much money to ignore

- Do you have steady income and strong discipline? YES → You can handle avalanche’s delayed wins

- Would saving $3,000+ in interest meaningfully change your financial situation? YES → Avalanche is worth the willpower investment

Most people answer yes to 2-3 questions. Weight your answers toward questions 3, 4, and 6—these matter most for long-term success.

Start Your Debt Payoff Today

Analysis without action keeps you trapped in the debt cycle. Follow this Day 1 roadmap to transform your debt strategy from concept to execution before the week ends.

Your Day 1 Action Plan

- List every debt with current balance, APR, and minimum payment in a spreadsheet—include credit cards, personal loans, medical bills, and any other obligations

- Calculate your total available monthly payment by adding all minimums plus any extra funds from your budget calculator analysis

- Choose your method using the decision framework above—commit to either snowball, avalanche, or your specific hybrid approach for the next 90 days minimum

- Set up automatic payments for minimums on all accounts so you never miss a payment and damage your credit score during the payoff journey

- Schedule your first milestone celebration for when you eliminate your first debt or hit your 6-month progress mark—make it specific and meaningful

The difference between people who successfully become debt-free and those who remain trapped isn’t intelligence or income—it’s implementation speed. Start today, not Monday.

Tools & Calculators

Use our Debt Consolidation Calculator to see if combining multiple debts into one lower-rate loan makes sense before starting either snowball or avalanche. Sometimes consolidation plus debt strategy creates the optimal combination.

Our Credit Card Payoff Calculator shows month-by-month projections for both methods using your actual numbers. Seeing your debt-free date in writing transforms an abstract goal into a concrete target.

Download our free debt payoff worksheet by signing up for our newsletter—this printable PDF includes space for listing all debts, tracking monthly progress, and celebrating each eliminated account.

Track Your Progress

Monthly milestone tracking keeps you motivated through the multi-year journey:

- Screenshot your account balances on the 1st of each month and save to a “Debt Freedom Journey” photo album

- Update your net worth calculator quarterly to see how eliminating debt increases your overall financial position

- Join online debt payoff communities on Reddit (r/DaveRamsey for snowball, r/personalfinance for avalanche discussions) for accountability and encouragement

Celebration triggers prevent burnout during the long middle phase:

- First debt eliminated: Nice dinner out (budget $50-75)

- 25% of debt eliminated: Weekend getaway or special activity

- 50% of debt eliminated: Significant celebration (concert tickets, spa day, whatever matters to you)

- Final debt eliminated: Major celebration that marks your new debt-free life chapter

Accountability systems triple your success probability according to behavioral economics research:

Share your debt-free goal and chosen method with one person you trust—a spouse, close friend, or family member who will check your progress monthly. This external accountability creates social pressure to follow through when motivation inevitably wavers.

Consider working with a nonprofit credit counseling agency certified by the National Foundation for Credit Counseling if you need professional guidance structuring your debt elimination plan.

Frequently Asked Questions about snowball vs avalanche

1. Is debt snowball or avalanche better for credit cards?

Debt avalanche typically works better for credit cards because their interest rates (averaging 24.37% in February 2026) create massive interest charges. However, if you have 5+ cards and need psychological wins, snowball the 1-2 smallest first, then avalanche the rest. The $200-400 in extra interest is worth it if it prevents you from quitting.

2. How much faster is debt avalanche than snowball?

Avalanche finishes 8-18% faster than snowball on average, depending on your interest rate spread. For a $40,000 debt load, expect avalanche to save 3-6 months. The time difference increases with larger debts and wider rate gaps between accounts.

3. Can you switch from snowball to avalanche mid-payoff?

Yes—switching methods mid-journey is the hybrid strategy that often delivers optimal results. Most people switch after eliminating 2-3 debts via snowball (typically 6-10 months), then use avalanche for remaining balances where interest savings matter most. There’s no penalty for changing course.

4. Does debt snowball hurt your credit score?

No—both snowball and avalanche improve your credit score identically. Your score improves from making on-time payments, reducing credit utilization, and eliminating accounts. The order you pay off debts doesn’t affect your credit score calculation at all.

5. What if my highest interest debt is also my largest?

Consider starting with 1-2 snowball victories on smaller debts first (2-4 months total), then switching to your large high-interest debt. This gives you early wins while still attacking the expensive debt relatively quickly. Alternatively, calculate if the interest cost of delaying that high-rate payoff exceeds your need for psychological momentum.

6. How does the hybrid method work?

The hybrid method uses snowball for your first 1-3 debts (typically accomplished in 6-12 months), then switches to avalanche for all remaining balances. This captures early psychological wins while still optimizing interest savings on the bulk of your debt. It’s the best-of-both-worlds approach for most people.

7. Should I pay off student loans with snowball or avalanche?

Student loans typically carry lower interest rates (5.50% for federal undergraduate loans in 2026) than credit cards, so use avalanche to attack high-interest consumer debt first. However, if you have a small student loan under $3,000, snowball it early for a quick win. Remember that student loan interest may be tax deductible up to $2,500.

8. What’s the average time to become debt-free?

Americans with $30,000-50,000 in consumer debt typically take 36-48 months to reach debt freedom using either snowball or avalanche. The key factor isn’t which method you choose—it’s how much extra payment you can apply monthly above minimums. Someone paying $1,500/month finishes in half the time of someone paying $750/month.

9. Can I use snowball and avalanche together?

Yes—this is precisely what the hybrid method does. You can also use both simultaneously by snowballing debts below 10% APR while avalanching everything above 10%. There’s no rule requiring pure strategy adherence. Your debt payoff plan should serve your psychology and mathematics, not ideology.

10. Does debt avalanche save more money than snowball?

Yes—avalanche always saves more in total interest paid because it attacks high-rate debt first. Typical savings range from $1,500 to $8,000 depending on debt size and rate differences. However, snowball delivers faster psychological wins that prevent many people from quitting their debt payoff journey entirely, which makes it mathematically superior for those who need momentum.

11. Which method works better for medical debt?

Medical debt typically carries 0% interest, so avalanche logic says pay it last. However, medical debt frequently goes to collections faster than other debt types, damaging your credit score. Consider snowballing small medical debts under $2,000 to close those accounts quickly, then avalanching the rest of your debt portfolio by interest rate.

⚠️ Important Disclaimer

Not Financial Advice: The information in this article is for educational purposes only and does not constitute financial advice. FinanceAuthorityHub.com and its authors are not certified financial advisors, and this content should not be considered personalized financial guidance for your specific situation.

Consult a Professional: Before making significant financial decisions about debt repayment, credit management, or financial planning, consult with a qualified financial advisor or credit counselor who can review your complete financial picture. You can find certified counselors through the National Foundation for Credit Counseling.

No Guaranteed Results: Past performance and examples cited in this article do not guarantee future results. Individual outcomes vary based on debt amounts, interest rates, payment amounts, income stability, and numerous other factors unique to each person’s financial situation.

Data Accuracy: While we strive for accuracy, interest rates, financial data, and debt statistics change frequently. All APR figures and Federal Reserve data cited reflect February 2026 information current at time of publication. Verify current rates with your specific creditors before making decisions.

Investment and Risk Warning: Debt repayment involves financial risk. Any financial decision carries potential consequences including impact to credit scores, ability to access emergency funds, and opportunity costs. Consider your complete financial situation including emergency savings needs before aggressively paying down debt.

Calculator Tools: All calculators and tools mentioned in this article provide estimates based on inputs you provide. They do not account for all variables affecting your debt payoff journey and should be used as planning tools, not definitive financial projections.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.