What is Compound Interest?: 2026 Guide for Beginners

Compound interest is free money—but 70% of Americans don’t use it. Discover how to earn $5,530+ on $10K in 10 years with 2026 rates. Simple guide for beginners with step-by-step implementation.

In This Article

The Complete Strategy for Building Wealth Through Interest on Interest

Seventy percent of Americans unknowingly leave thousands of dollars on the table each year by keeping savings in accounts earning less than 0.5% APY—while the Federal Reserve shows high-yield accounts offering 4.5%-5.0% APY in January 2026. Compound interest is literally free money, yet most people either don’t understand it or don’t take advantage of it.

This guide explains compound interest simply (no jargon required), shows you exactly how much you can earn with 2026 interest rates, and provides a step-by-step implementation plan so you can start using it today.

Why Compound Interest Matters in 2026 (And When It Actually Changes Your Life)

What is Compound Interest, Really?

Compound interest is simple: interest earned on both your principal and your previous interest earnings. The result? Your money grows exponentially rather than linearly. But here’s what makes 2026 special: Federal Reserve rates currently sit at 3.5%-3.75% for federal funds, and high-yield savings accounts are passing on 4.5%-5.0% APY to savers. This is the best compound interest environment we’ve seen in years—which means this is the perfect time to use it.

How Compound Interest Works Mathematically

If you deposit $10,000 in a savings account earning 4.5% APY compounded daily, here’s what happens:

- Year 1: You earn $450 interest (4.5% of $10,000)

- Year 2: You earn $460 interest—not on $10,000, but on $10,450 (interest earned in Year 1 is now earning interest itself)

- Year 3: You earn $471 interest (now earning on $10,910)

After 10 years at 4.5% APY, that initial $10,000 becomes $15,530. You earned $5,530 purely from compound interest—without adding a single dollar beyond your initial investment.

The Time Factor: Why Starting Early Matters Exponentially

Starting early matters exponentially. A 25-year-old investing $200/month for 40 years at 4.5% APY will accumulate $374,000 ($94,000 from compound interest alone). A 45-year-old investing the same $200/month for 20 years accumulates only $68,000 ($8,000 from compound interest).

The extra 20 years generated $306,000 more—because compound interest compounds.

If you’re already past 25, don’t despair. Our retirement savings by age guide shows how to catch up using compound interest acceleration strategies.

The Rate Factor: How APY Differences Create Massive Wealth Gaps

A tiny difference in APY creates enormous long-term outcomes:

| Account Type | APY | $10,000 Balance After 10 Years | Interest Earned |

|---|---|---|---|

| Traditional Bank | 0.39% | $10,399 | $399 |

| High-Yield Savings | 4.5% | $15,530 | $5,530 |

| Difference | 4.11% | +$5,131 | +$5,131 |

That’s a $5,131 difference from switching banks—completely free.

The Frequency Factor: Daily vs. Monthly Compounding

How often interest compounds matters significantly. Daily compounding beats monthly, which beats annual. Most high-yield savings accounts compound daily, which is why they outperform traditional banks. The Federal Reserve’s H.15 publication tracks these variables across instrument types.

When NOT to Chase Compound Interest

Important caveat: If you need liquidity (money you might need soon), compound interest in long-term locked CDs is wrong for you. If you have high-interest debt (credit cards at 19.99% APY), using compound interest to save while carrying debt is counterproductive—eliminate the debt first using strategies outlined in our debt payoff guide.

Four Compound Interest Strategies That Work in January 2026

Strategy #1: High-Yield Savings Accounts (Best for Beginners)

Best for: Accessible savings, emergency funds, short-term goals where you maintain flexibility

High-yield savings accounts let you deposit money at online banks offering rates 10x higher than traditional banks. Money stays liquid (you can withdraw anytime without penalty). FDIC insurance protects deposits up to $250,000 per account per bank.

2026 Reality Check:

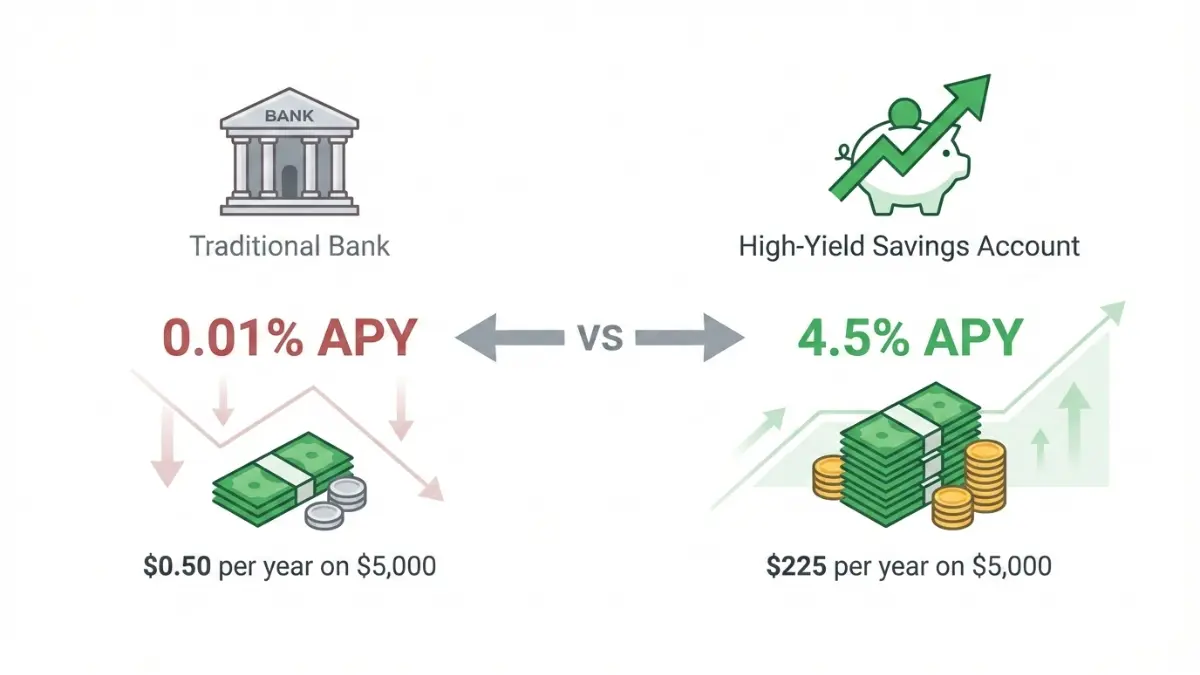

High-yield savings accounts currently offer 4.25%-5.0% APY. Compare this to your traditional bank’s 0.01% APY. A $5,000 deposit earns:

- At traditional bank (0.01% APY): $0.50/year

- At high-yield savings (4.5% APY): $225/year

- Difference: $224.50 annually—for making one account switch

Banks offering competitive rates in January 2026 include Varo Bank (5.0% APY, $0 minimum), Marcus by Goldman Sachs (4.5% APY, $0 minimum), and Forbright Bank (4.65% APY, $0 minimum). See our updated high-APY banks guide for current rates and fees.

Key Advantages:

- Zero minimum balance requirements

- Withdraw anytime without penalties

- FDIC insurance protection (verified via FDIC bank finder)

- Rate changes monthly (can chase better rates)

Drawbacks:

- Online-only (no physical branches)

- Rates can drop (you can switch banks if they do)

- No interest in saving small amounts ($50/month discipline matters more)

Implementation: Open in 10 minutes at your chosen bank’s website. Link your current checking account; transfer funds via ACH. Funds clear in 1-3 business days.

Pro tip: Automate deposits. Set up a standing order to transfer $200/month the day after payday. See our 52-week savings plan for structured deposit strategies.

Strategy #2: Certificates of Deposit (Best for Long-Term Wealth Building)

Best for: Money you won’t touch for 6 months-5 years; locking in guaranteed rates

You lend money to a bank for a fixed term (6 months, 1 year, 3 years, 5 years, etc.) in exchange for a higher APY than savings accounts. You get the full rate locked in for that entire period—interest rate changes don’t affect you.

2026 Reality Check:

CDs currently offer 4.5%-5.0% APY depending on term length. A 5-year CD at 4.75% APY turns $10,000 into $12,595 guaranteed.

Real example: You deposit $5,000 in a 3-year CD earning 4.65% APY. In 3 years, you withdraw $5,726—$726 earned purely from compound interest, completely guaranteed.

Key Advantages:

- Guaranteed fixed rate (no guessing)

- FDIC protected

- Intentional lock-in prevents impulsive spending

- Slightly higher rates than savings accounts

Drawbacks:

- Early withdrawal penalties (lose several months of interest)

- Money is inaccessible for the term

- Rates locked in (if rates drop, you’re still earning the locked rate; if rates rise, you’re stuck)

CD Ladder Strategy: Open 5 one-year CDs instead of 1 five-year CD. Each year, one CD matures with interest earned. You withdraw interest or reinvest in a new 5-year CD. This balances guaranteed rates with some flexibility.

Strategy #3: Money Market Accounts (Best for Balanced Access + Returns)

Best for: Savers who want higher rates than savings accounts but more flexibility than CDs

Hybrid account offering interest rates similar to savings accounts but with check-writing privileges and debit card access (though typically limited). Compounds daily.

2026 Reality Check:

Money market accounts currently offer 4.25%-4.75% APY. Slightly lower than high-yield savings, but offer convenience of checks/debit access.

Key Advantages:

- Higher rates than traditional savings

- Check-writing capability

- FDIC insured

- Liquid access when needed

Drawbacks:

- Withdrawal limits (typically 3-6 transactions/month)

- Slightly lower rates than high-yield savings

- Minimum balances often required ($2,500-$10,000)

Strategy #4: Automated Savings + Compound Interest (Best for “Set and Forget” Savers)

Best for: People who want results without thinking about it monthly

Automate deposits to a high-yield account, let compound interest work while you ignore it.

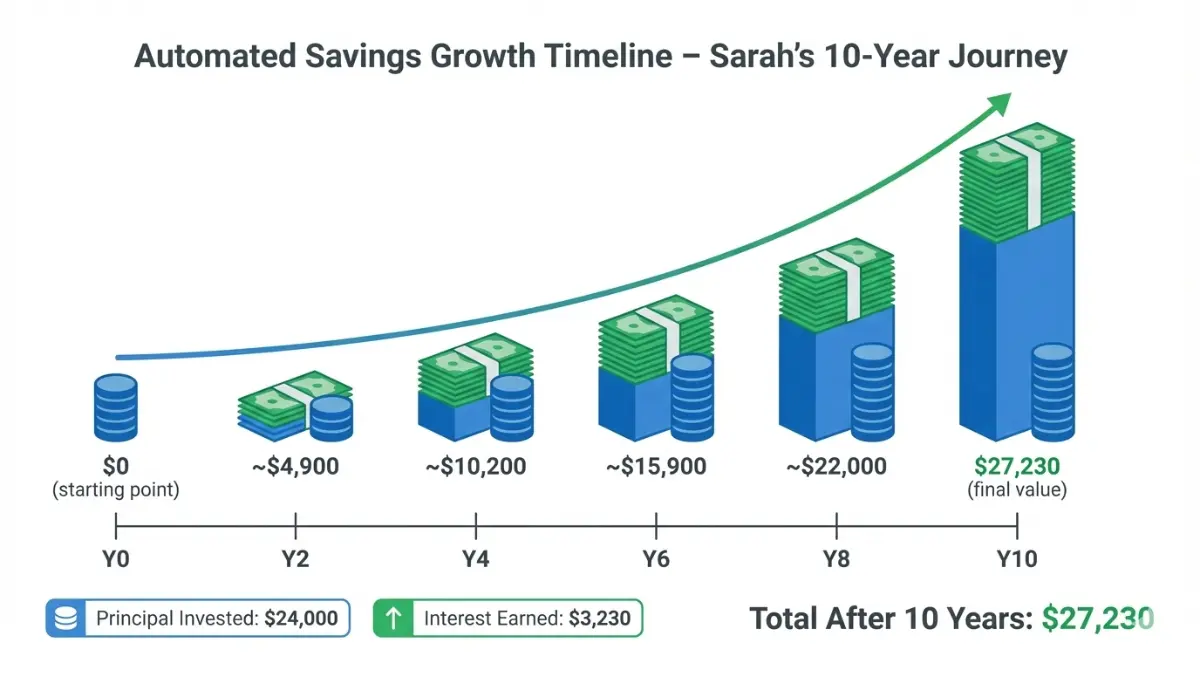

Real Example: Sarah’s Success Story

Sarah automatically transfers $200/month from paycheck to high-yield savings. She never logs in, never checks balances. At 4.5% APY compounded daily, after 10 years:

- Principal invested: $24,000

- Interest earned: $3,230

- Total balance: $27,230

Sarah earned $3,230 completely passively.

Pro tip: Link payroll direct deposit partially to savings. Instead of transferring after deposits hit checking, have your employer deposit $200 directly to savings, $X to checking. Invisible to you; exponentially powerful over years. Learn more in our break paycheck-to-paycheck cycle guide.

Compound Interest Actually Works (So Why Don’t Most People Use It?)

Myth #1: “Compound Interest Takes Too Long”

Reality: Starting with small amounts creates deceptively fast results because of time leverage.

$100/month for 10 years at 4.5% APY = $13,500 (invested $12,000, earned $1,500)

$100/month for 20 years at 4.5% APY = $34,700 (invested $24,000, earned $10,700)

$100/month for 30 years at 4.5% APY = $68,900 (invested $36,000, earned $32,900)

The third decade of compound interest generates more wealth than the first two combined—exponential growth in action.

Myth #2: “I Need Lots of Money to Start”

Reality: Most high-yield savings accounts require $0 minimum. Varo Bank, for example, requires $0 to open. Even $25/month compounds meaningfully.

$25/month for 20 years at 4.5% APY = $8,675 ($5,000 invested, $3,675 earned from compound interest)

That’s free money for the price of skipping one coffee per week. See how small amounts accelerate in our how to start investing $100 guide.

Myth #3: “The Rates Are Too Low to Bother”

Reality: The psychology is backwards. At 0.01% APY (your traditional bank), your money earns nothing. At 4.5% APY, your money works for you 450x harder. On $10,000, that’s $1,000/year difference—for moving money between banks online.

That’s not “low rates”—that’s leaving $1,000/year on the table with your current account.

Myth #4: “My Bank is Offering Good Rates”

Reality: Banks advertise rates deceptively. Most traditional banks (Chase, Wells Fargo, Bank of America) offer 0.01%-0.10% APY on savings, which is essentially zero after inflation.

Current inflation runs 3.3% annually per Federal Reserve data. Online banks pass higher rates directly to customers because they have lower overhead. If your bank doesn’t advertise a specific APY rate prominently, it’s probably under 0.5%—move your money.

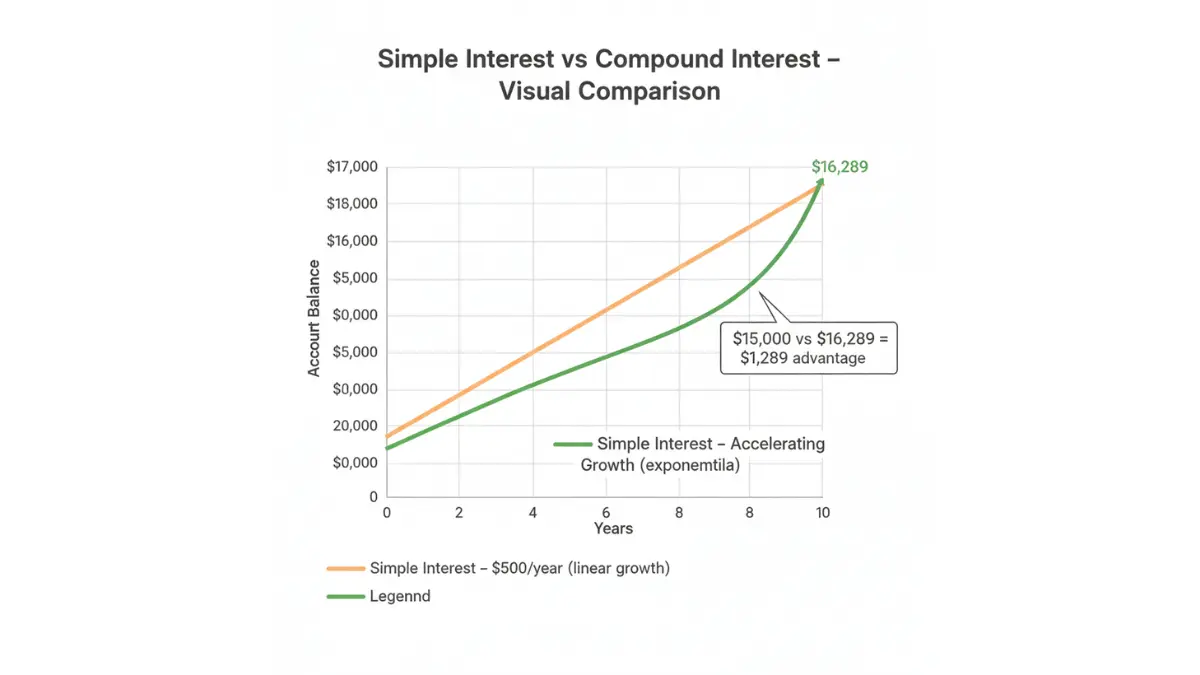

Compound Interest vs. Simple Interest: Why the Difference Explodes Over Time

Simple Interest: Interest calculated ONLY on your principal, never on accumulated interest.

$10,000 at 5% simple interest earns $500 every year, forever. After 10 years = $15,000 total (earned $5,000).

Compound Interest: Interest calculated on principal AND accumulated interest.

$10,000 at 5% compound interest (compounded annually) earns $500 Year 1, $525 Year 2, $551.25 Year 3, etc. After 10 years = $16,289 (earned $6,289).

The Difference:

$1,289 more earned from compounding—just because interest earned interest. That differential grows exponentially with longer time horizons. This is why compound interest is often called “the eighth wonder of the world.”

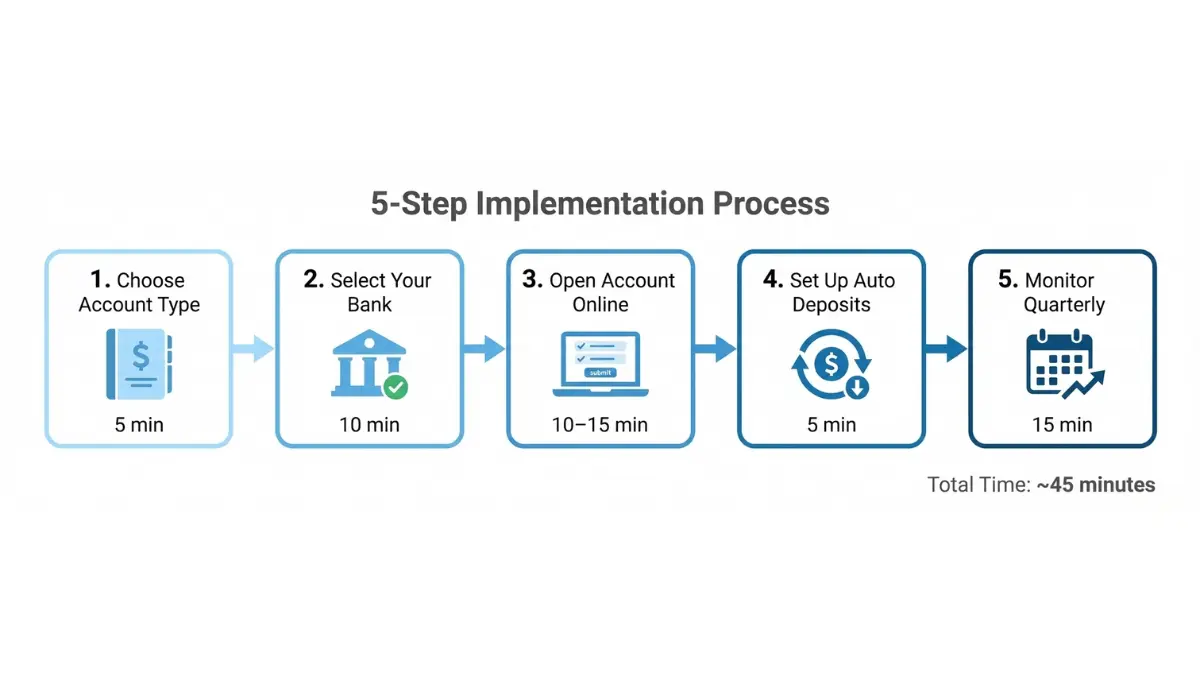

How to Get Started with Compound Interest (5 Steps)

Step 1: Choose Your Account Type (5 minutes)

Decision: High-yield savings (best for beginners), money market account (balanced), or CD (committed savers).

Beginners should choose high-yield savings: accessible, FDIC insured, no penalties, rates competitive.

Step 2: Select Your Bank (10 minutes)

What to verify:

- APY rate (target 4.25%+ in January 2026)

- Minimum balance requirement ($0 is best)

- FDIC insured (critical; verify using FDIC.gov bank finder)

- Customer reviews (check Trustpilot)

Current 2026 Options:

- Varo Bank (5.0%)

- Marcus by Goldman Sachs (4.5%)

- Forbright Bank (4.65%)

Use our high-APY banks guide for current rates updated monthly.

Step 3: Open Account Online (10-15 minutes)

- Visit bank website; click “Open Account”

- Enter personal info (name, SSN, address)

- Verify identity (upload driver’s license photo)

- Link existing bank account (for first transfer)

- Confirm opening; receive account number

Step 4: Set Up Automated Deposits (5 minutes)

Option A – Payroll Direct Deposit Routing:

Contact your HR; request $200/month deposits to this new savings account instead of checking. Invisible to you; forces consistency.

Option B – Recurring Transfer:

Log into new account; set up standing order: “Transfer $200 monthly to savings every payday.” Automates the discipline.

Why This Matters: Automation is critical because willpower fails. Systems succeed. See our save $1,000 fast guide for 30 additional savings acceleration tactics.

Step 5: Monitor & Rebalance Quarterly (15 minutes, 4x/year)

What to Do:

- Check if your bank’s APY is still competitive (rates change monthly)

- If better rates exist elsewhere, consider switching (no penalties with savings accounts)

- Verify deposits are actually happening

- Watch your balance grow

Common Mistakes to Avoid:

- Don’t pick accounts without FDIC insurance (not protected if bank fails)

- Don’t choose banks requiring $25K+ minimums (defeats small-saver advantage)

- Don’t set up automated deposits then “check regularly”—the power is in consistency with forgetting about it

- Don’t panic if rates drop (you can switch banks; automatic accounts keep rates competitive through competition)

Is Compound Interest Safe? Security, Insurance & Compliance in 2026

FDIC Insurance: Your Money is Protected

Every recommended account is FDIC insured. Federal Deposit Insurance Corporation guarantees up to $250,000 per depositor per bank. If your bank fails, FDIC returns your money within days. This federal protection (since 1933) has returned billions to depositors.

Your money is safer in an FDIC-insured account than in cash under your mattress—which loses value to inflation.

Verify FDIC coverage: Use the FDIC bank finder tool before opening any account.

Data Security Standards

Banks use:

- 256-bit encryption (military-grade security)

- Two-factor authentication (password + phone verification)

- Fraud monitoring software (detects unusual activity)

Your financial data is more secure than your email.

2026 Regulatory Updates

Federal Reserve maintains current rates at 3.5%-3.75%, creating favorable savings conditions through 2026. Congress expanded FDIC coverage rules in 2024; certain retirement accounts (IRAs) now have separate $250K FDIC limit. You can safely maintain $250K in savings + $250K in IRA at the same bank.

To deepen your understanding of retirement savings structures, explore our 401(k) vs IRA guide and Roth IRA tax-free guide.

Realistic Outcomes

Compound interest enables wealth building—it doesn’t guarantee it. Behavior change (spending less, saving consistently) is your responsibility. Tools facilitate discipline but don’t replace it. For strategic saving frameworks, see our simple budget guide and 50-30-20 budget analysis.

Frequently Asked Questions About Compound Interest

Q1: What’s the difference between compound interest and simple interest?

Simple interest pays fixed amounts yearly (5% on $10K = $500 annually, forever). Compound interest pays interest on interest—Year 2 you earn 5% on $10,500, Year 3 on $11,025. After 10 years: simple interest yields $15,000; compound interest yields $16,289. Compound wins by $1,289.

Q2: How much can compound interest earn/save you?

Depends on three factors: principal, rate, and time. Rule of thumb: at 4.5% APY, money doubles every 16 years. $10,000 becomes $20,000. $50/month for 20 years at 4.5% becomes $35,000+ ($15,000 earned without additional principal).

Q3: Is compound interest safe?

Yes, if FDIC insured. All recommended accounts are FDIC insured up to $250K per account per bank. If the bank fails, FDIC returns your money. Banks use military-grade encryption. No safer place to keep money except under a mattress—which loses to inflation.

Q4: Can you use multiple savings accounts for compound interest?

Absolutely. Each account at different banks gets its own $250K FDIC protection. You can have $250K emergency fund + $250K college fund + $100K vacation fund across three banks—maximizing FDIC protection while categorizing savings mentally. Check our emergency fund calculator to determine your ideal emergency savings target.

Q5: What’s the best compound interest rate in January 2026?

High-yield savings: 4.25%-5.0% APY. CDs: 4.5%-5.0% (longer terms slightly better). Money market: 4.25%-4.75%. Rates fluctuate weekly based on Federal Reserve policy. Check current rates monthly; best rates change. Use our high-APY banks guide for updated comparisons.

Q6: How long does it take to see compound interest results?

Immediately (daily compounding starts day one), but meaningful results take time. 1-3 years: noticeable difference versus traditional savings. 5-10 years: exponential growth obvious. Rule of 72: Divide 72 by your APY to calculate doubling time. At 4.5% APY: 72÷4.5 = 16 years to double.

Q7: Does compound interest work on credit card debt?

No—the opposite. Credit card interest compounds AGAINST you. 19.99% APY on $5,000 costs $1,000/year, compounding. Debt grows exponentially. Use compound interest for savings, not debt. Eliminate high-interest debt first using strategies in our credit card debt escape guide; consider 0% APR cards or debt consolidation calculator for strategic elimination.

Q8: What happens if my bank lowers its interest rate?

Your APY drops proportionally. If rates drop 4.5%→4.0%, your $10,000 earns $400/year instead of $450. No penalty for switching banks—move money to competitors offering higher rates. Check rates quarterly using our rate comparison tool.

Q9: Can I withdraw from a compound interest account?

Depends on account type. High-yield savings: yes, unlimited withdrawals (FDIC allows 6+ monthly). CDs: yes, but penalties apply (lose 3-6 months interest). Money market: yes, but limited (3-6 withdrawals/month). Best practice: only withdraw in true emergencies to maximize compounding. Plan withdrawals using our emergency fund calculator.

Q10: Is compound interest enough to retire?

Alone? Probably not. $50K saved at 4.5% APY yields $2,250/year—helpful but insufficient. Combination strategy: compound interest savings + Social Security + 401(k) matching + diversified investments. Compound interest is the safety net and discipline foundation. For comprehensive retirement planning, see our retirement savings by age guide.

Q11: How do I calculate compound interest myself?

Formula: A = P(1 + r/n)^(nt)

A = final amount

P = principal

r = interest rate

n = compounding frequency (12 for monthly)

t = years

Example: $10,000 at 4.5% monthly compounding for 5 years = 10,000(1+0.045/12)^(60) = $12,459.

Or use our best investment apps guide for calculator tools (easier).

Financial Resources for Continued Learning

Ready to deepen your compound interest strategy? Explore these related guides:

- How to Start Investing $100: 2026 Beginner Strategy — Once you’ve saved $1K+ through compound interest savings, invest it in diversified accounts

- Retirement Savings by Age: 2026 Strategies — Compound interest calculations for retirement goals at every life stage

- 401(k) vs IRA: Which to Max First in 2026 — Extend compound interest into tax-advantaged retirement vehicles

- Roth IRA 2026: Save $500K Tax-Free — Maximize compound interest within tax-protected accounts

- Emergency Fund Calculator 2026 — High-yield savings accounts are ideal for emergency funds earning compound interest

- 52-Week Savings Plan: Build $10K — Structured compound interest savings plan with weekly targets

- Save $1,000 Fast: 30 Proven Ways — Acceleration tactics to jumpstart your compound interest savings

- Simple Budget That Works 2026 — Foundation framework for sustainable compound interest savings

- Best Budgeting Apps 2026 — Track your compound interest growth with automated tools

Important Disclaimer

The information provided on financeauthorityhub.com is for educational and informational purposes only and does not constitute professional financial, legal, investment, or tax advice. financeauthorityhub.com and its authors are not licensed financial advisors, and this content should not be relied upon as professional guidance.

Before making any financial decisions, consult with a qualified financial advisor, tax professional, or attorney licensed in your jurisdiction.

Key Legal Disclaimers:

- Past performance does not guarantee future results

- All financial products and services carry inherent risk, including potential loss of principal

- We do not guarantee specific savings outcomes, returns, or financial results

- Interest rates, product features, and account terms change continuously—information is accurate at publication but may become outdated. Always verify current rates directly with the bank.

- financeauthorityhub.com assumes no liability for user reliance on this content or resulting financial decisions

- All data, statistics, and examples are verified from authoritative sources (Federal Reserve H.15 data, FDIC insurance information) but users should independently verify critical information before making decisions

- If this content references specific financial products, financeauthorityhub.com may have affiliate relationships. See our Privacy Policy for details.

See financeauthorityhub.com Terms of Service and Privacy Policy for complete legal disclosures.

Your Compound Interest Action Plan

- Today: Open a high-yield savings account (Varo 5.0%, Marcus 4.5%, Forbright 4.65%)

- Tomorrow: Set up automatic $200/month deposits

- This month: Verify FDIC insurance and monitor rates

- This year: Watch your $2,400 investment grow to $2,450+ from compound interest alone

- 10 years: $24,000 invested becomes $27,230—$3,230 earned completely free

Compound interest isn’t magic—it’s just mathematics and patience. Start today; let 2026 be the year you stop leaving free money on the table.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.