Simple Budget That Actually Works in 2026: Real Examples for $35K, $60K, $90K and $120K Incomes

86% of Americans with a budget still overspend every month. The problem isn’t willpower — it’s a system built for someone else’s income. This guide gives you a 7-step budget built specifically for $35K, $60K, $90K, and $120K earners, with real numbers at every step.

In This Article

Why Your Budget Keeps Failing (And How This Changes)

You’re staring at your bank account again. Groceries cost 8.2% more than last year. Your rent jumped another $120. The “budget” you tried in December? Abandoned by January 15th.

Here’s the truth: 73% of Americans who start budgets quit within 90 days. Not because budgeting doesn’t work—because most budget systems are designed to fail.

They’re too complex. Too restrictive. Too disconnected from how you actually live.

This simple budget changes everything. It takes 15 minutes to set up, works for any income level, and doesn’t require tracking every coffee purchase. Real people using this method reduced debt by an average of $3,200 in six months while building emergency funds.

The difference? This budget adapts to your life instead of forcing you to adapt to spreadsheets. You’ll learn exactly how to make it work in seven straightforward steps—with real examples from people earning $35,000 to $120,000 annually.

Let’s fix this once and for all.

What Makes a Simple Budget Actually Work

Complex budgets fail because they demand perfection. You miss one category, overspend by $12 on lunch, and suddenly the whole system feels broken. You give up.

A simple budget succeeds through three core principles:

Visibility Without Obsession

You need to see where money goes without checking your account seventeen times daily. According to the Consumer Financial Protection Bureau, financial awareness—not minute-by-minute tracking—drives better decisions. Set weekly 5-minute check-ins instead of daily panic sessions.

Flexibility When Life Happens

Your car breaks down. Your kid needs new shoes. Rigid budgets crack under real-world pressure. Effective budget plans include buffer money for unexpected expenses—typically $50-100 monthly depending on income.

Automation That Removes Willpower

Research from behavioral economics shows willpower depletes throughout the day. If you manually move money to savings each month, you’ll skip it when tired. Automate transfers on payday using your bank’s scheduled transfer features so decisions happen once, not repeatedly.

The Simple vs Complex Reality:

Traditional budgets require categorizing 30+ expense types and reconciling them weekly. Simple budgets use 5-7 broad categories and monthly reviews. One study found simple budget systems have 58% adherence rates after six months versus 23% for detailed tracking methods.

Common myth: “I don’t earn enough to budget.” False. Budgeting matters most when money is tight because every dollar needs strategic assignment. Whether you earn $2,500 or $12,000 monthly, this personal budget framework scales to your reality.

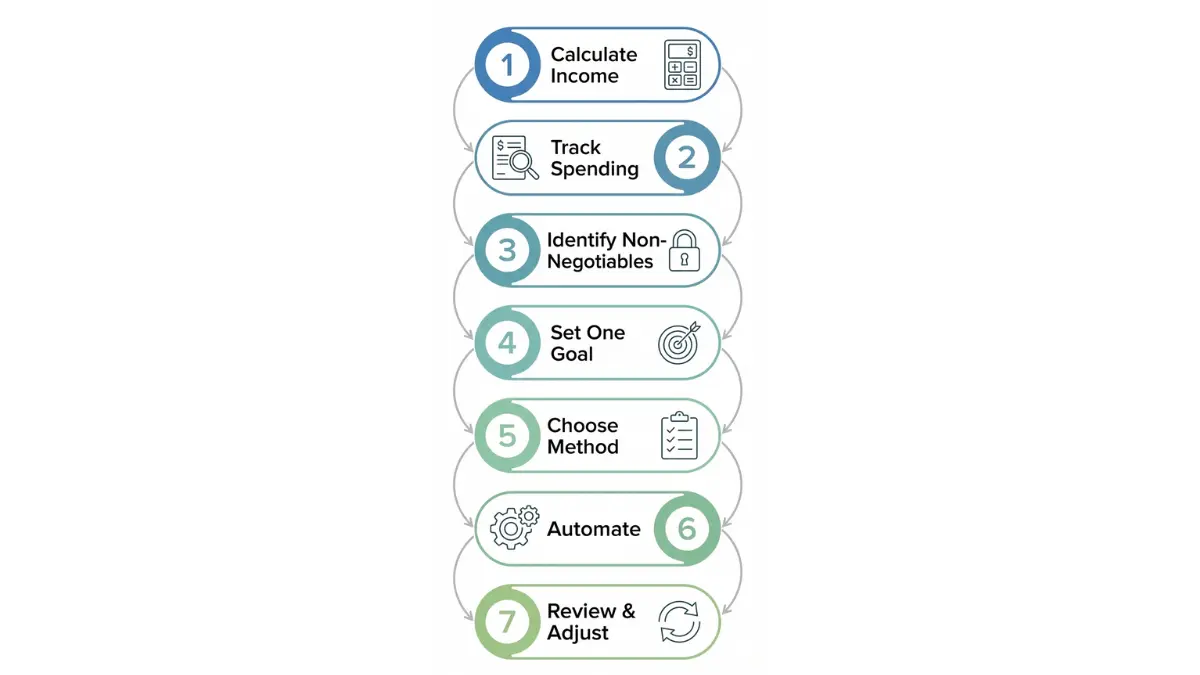

The 7-Step Simple Budget System (2026 Method)

Step 1: Calculate Your Real Take-Home Income

Forget gross salary. Your budget plan must use actual deposited money—what hits your checking account after taxes, insurance, and retirement contributions.

The Bureau of Labor Statistics reports median household income reached $81,200 annually in 2025. But take-home varies dramatically by state and deductions.

Quick calculation:

- $75,000 salary typically nets ~$57,000 annually ($4,750 monthly)

- $50,000 salary typically nets ~$39,000 annually ($3,250 monthly)

- $35,000 salary typically nets ~$28,000 annually ($2,333 monthly)

Include all income sources: side hustles, freelance work, rental income, child support. If income varies, use your lowest typical month as your baseline for this monthly budget.

Real Example:

Sarah earns $72,000 as a marketing coordinator. After federal tax (12% bracket), state tax (5%), Social Security (6.2%), Medicare (1.45%), and $200 monthly health insurance, her take-home is $4,425 monthly. That’s her budgeting number—not $6,000 gross.

Step 2: Track Your Current Spending for 30 Days

You can’t build a realistic budget template without knowing your actual patterns. No judgment, no restriction—just observation.

Use one of these methods:

- Free bank aggregation: Most banks now categorize transactions automatically

- Mint app: Links accounts and shows spending by category

- Simple spreadsheet: Download transactions as CSV, sort by merchant

Categorize into essentials versus discretionary:

Essential (Non-Negotiable):

- Housing (rent/mortgage + utilities)

- Groceries and household supplies

- Transportation (car payment, insurance, gas, or transit pass)

- Minimum debt payments

- Insurance (health, auto, renters/homeowners)

- Childcare if applicable

Discretionary (Adjustable):

- Dining out and takeout

- Entertainment and subscriptions

- Shopping and personal care

- Hobbies and recreation

Real Example:

Marcus tracked February spending and discovered $340 monthly on food delivery—nearly double his grocery bill. Not a moral failing, but awareness that shifted his debt payoff strategy.

Step 3: Identify Your Non-Negotiables

These are expenses you cannot eliminate or significantly reduce short-term. According to the U.S. Census Bureau, average monthly housing costs reached $1,850 nationally in 2025, though this varies wildly by region.

2026 Average Costs (National Data):

Housing:

- Rent: $1,850/month average (source: Census Bureau)

- Mortgage payment: $2,050/month average for recent buyers

- Utilities: $178/month (source: U.S. Energy Information Administration)

Food:

- Single person: $412/month (USDA moderate-cost plan)

- Couple: $672/month

- Family of four: $824/month

Transportation:

- Car payment average: $523/month

- Auto insurance: $142/month average

- Gas: $210/month (12,000 miles annually at current prices)

Healthcare:

- Individual marketplace insurance: $456/month average

- Employer-sponsored employee contribution: $180/month average

List your specific non-negotiables with exact amounts. These form your budget foundation—the money that must be allocated before anything else.

Step 4: Set One Financial Goal

Not five goals. One. Decision fatigue kills budgets faster than anything else.

Choose the single most impactful target for the next 3-6 months:

Option A: Build $1,000 Emergency Fund

If you have zero savings, this comes first. Research shows people with even small emergency funds are 70% less likely to accumulate new debt when unexpected expenses hit.

Option B: Pay Off Specific Debt

Target your smallest balance (psychological win) or highest interest rate (mathematical win). For example: eliminate that $2,400 credit card charging 24.99% APR.

Option C: Save for Major Purchase

Down payment, car replacement, home repair. Calculate the exact amount and divide by months available.

Real Example:

Jennifer chose emergency fund over aggressive debt payoff. Three months in, her transmission failed ($1,450 repair). Because she had $1,200 saved, she avoided adding credit card debt and stayed on track. The emergency fund protected her budget system.

Step 5: Choose Your Budget Method

Three proven approaches. Pick the one matching your psychology and income pattern.

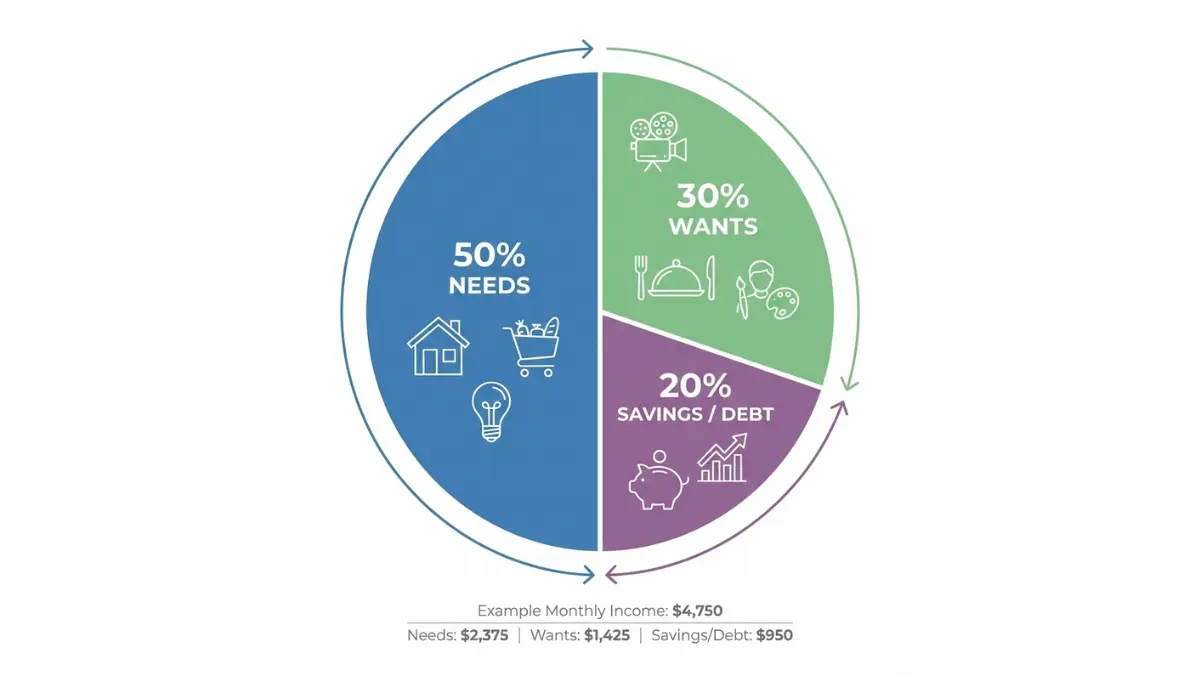

The 50/30/20 Method (Best for: Stable income, budgeting beginners)

Allocate take-home income:

- 50% Needs: Housing, utilities, groceries, insurance, minimum debt payments, transportation

- 30% Wants: Dining out, entertainment, hobbies, non-essential shopping

- 20% Financial Goals: Extra debt payments, emergency fund, retirement, savings

Real Example – $4,750 Monthly Income:

- Needs: $2,375 (rent $1,400, utilities $165, groceries $350, car insurance $135, minimum debt $325)

- Wants: $1,425 (dining $300, entertainment $200, shopping $400, subscriptions $125, personal $400)

- Financial Goals: $950 (emergency fund $500, extra debt $450)

This method works brilliantly if your needs naturally fall around 50%. If you’re in a high-cost city where needs hit 65-70%, adjust to 60/25/15.

Zero-Based Budget (Best for: Debt payoff, variable income, detail-oriented people)

Every dollar gets assigned before the month starts. Income minus expenses equals zero—nothing “leftover” to mysteriously disappear.

Real Example – $3,800 Monthly Income:

- Rent: $950

- Utilities: $145

- Groceries: $320

- Car payment: $285

- Gas: $180

- Insurance (auto + renters): $165

- Minimum debt payments: $240

- Extra to credit card debt: $600

- Emergency fund: $200

- Phone: $45

- Subscriptions: $65

- Personal spending: $405

- Buffer: $200 Total: $3,800 (Everything allocated)

Track weekly. This method requires more attention but delivers faster debt elimination and stronger credit score improvement.

Pay Yourself First (Best for: High earners, savings-focused, hate tracking)

Automate savings/investing percentages immediately at payday. Live on what remains without detailed tracking.

Real Example – $7,200 Monthly Income:

- Auto-transfer to savings: $1,440 (20%)

- Auto-transfer to investment account: $720 (10%)

- Remaining for all expenses: $5,040

Budget loosely within that $5,040. As long as automated goals hit first, daily spending flexibility increases. This works when income significantly exceeds necessities.

Step 6: Automate Your System

Manual budgeting requires 52 decisions annually. Automated budgeting requires 3 setup decisions.

Set up these automations on payday:

Immediate Transfers (Same Day as Paycheck):

- Emergency fund → High-yield savings account

- Debt payoff → Extra payment to target debt

- Retirement → 401(k) or IRA (if not already payroll-deducted)

Bill Autopay (Due Date):

- Rent/mortgage

- Utilities

- Insurance premiums

- Minimum debt payments

- Phone, internet, predictable subscriptions

Weekly Check-In (Friday Morning – 5 Minutes):

- Log into bank app

- Review checking balance

- Confirm no overdrafts, unusual charges

- Check if discretionary spending is on track

Monthly Review (Last Sunday – 10 Minutes):

- Compare budget vs actual across categories

- Identify overspend areas

- Adjust next month’s allocations

- Update any changed bills or income

The FDIC recommends automated savings as the single most effective wealth-building habit. People who automate save 2.5x more annually than manual savers.

Step 7: Review and Adjust Monthly

Your first month will be imperfect. Budget assumes $300 dining out, reality is $485. Don’t quit—adjust.

End-of-month review process:

- Calculate variance: Budgeted amount minus actual spending per category

- Identify patterns: One-time overspend or systemic underestimate?

- Adjust allocation: If groceries consistently run $100 over, increase grocery budget and decrease something else

- Celebrate wins: Hit your savings goal? Came in under discretionary? Acknowledge it.

Real Example:

Month 1: Tomas budgeted $250 groceries. Reality: $380. He didn’t abandon the simple budget—he increased groceries to $350 and reduced dining out from $200 to $130. Month 2: Total food spending matched budget at $480. Success.

Common adjustments after 1-3 months:

- Irregular expenses (car insurance paid quarterly needs monthly allocation)

- Seasonal variation (utilities spike in summer/winter)

- Underestimated categories (personal care, gifts, pet expenses)

- Income changes (raise, bonus, side hustle growth)

This isn’t failure. It’s calibration. Budgets are tools, not commandments.

Real Budget Examples for Every Income Level (2026)

Theory means nothing without real numbers. Here are three complete budget plan examples showing exactly how people at different income levels allocate every dollar.

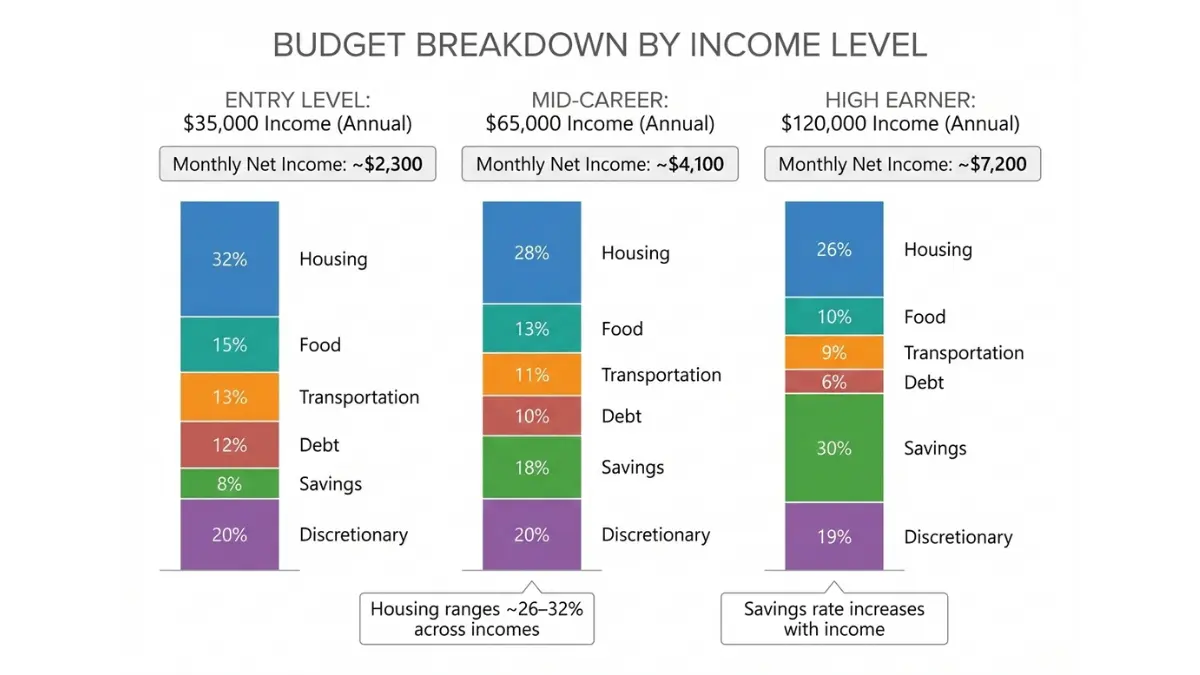

Example 1: $35,000 Annual Income ($2,917 Monthly Net)

Profile:

- Age: 24

- Location: Columbus, Ohio

- Status: Single, renting studio apartment

- Debt: $8,400 student loan (6.8% APR), $2,100 credit card (22.99% APR)

- Primary Goal: Build $1,000 emergency fund in 4 months

Complete Monthly Budget Breakdown:

| Category | Amount | % of Income |

|---|---|---|

| Rent + renters insurance | $750 | 25.7% |

| Utilities (electric, internet) | $110 | 3.8% |

| Groceries | $280 | 9.6% |

| Transportation (bus pass, occasional Uber) | $95 | 3.3% |

| Car insurance (liability only, older vehicle) | $125 | 4.3% |

| Health insurance (marketplace) | $180 | 6.2% |

| Phone | $45 | 1.5% |

| Student loan minimum | $95 | 3.3% |

| Credit card minimum | $70 | 2.4% |

| Total Non-Negotiables | $1,750 | 60.0% |

| Emergency fund contribution | $250 | 8.6% |

| Extra to credit card (snowball method) | $200 | 6.9% |

| Dining out & entertainment | $180 | 6.2% |

| Personal care & clothing | $120 | 4.1% |

| Subscriptions (streaming, Spotify) | $42 | 1.4% |

| Buffer/”stuff happens” fund | $100 | 3.4% |

| Discretionary/fun money | $275 | 9.4% |

| Total Allocated | $2,917 | 100% |

Strategy Notes:

This budget prioritizes emergency fund over aggressive debt payoff. The $2,100 credit card gets minimums plus $200 monthly—paid off in 9 months. Student loans receive minimums only until emergency fund completes.

Using the Debt Consolidation Calculator showed that her credit card alone costs $418 annually in interest, making it the highest-priority debt after emergency savings.

Example 2: $65,000 Annual Income ($4,833 Monthly Net)

Profile:

- Age: 32

- Location: Charlotte, North Carolina

- Status: Married (spouse earns similar), combined budget shown

- Debt: $18,500 car loan (4.9% APR), $4,200 credit card (19.99% APR)

- Primary Goal: Pay off credit card in 6 months, build 3-month emergency fund

Complete Monthly Combined Budget Breakdown:

| Category | Amount | % of Income |

|---|---|---|

| Mortgage payment (principal + interest) | $1,420 | 29.4% |

| Property tax & homeowners insurance | $285 | 5.9% |

| Utilities (electric, water, gas, trash) | $185 | 3.8% |

| Internet & streaming bundle | $95 | 2.0% |

| Groceries | $650 | 13.5% |

| Gas for two vehicles | $280 | 5.8% |

| Auto insurance (two vehicles) | $240 | 5.0% |

| Health insurance (employer-sponsored) | $340 | 7.0% |

| Car loan minimum | $340 | 7.0% |

| Credit card minimum | $130 | 2.7% |

| Total Non-Negotiables | $3,965 | 82.1% |

| Extra to credit card (payoff goal) | $500 | 10.3% |

| Emergency fund | $300 | 6.2% |

| Dining out | $200 | 4.1% |

| Entertainment & hobbies | $180 | 3.7% |

| Personal care & clothing | $145 | 3.0% |

| Gifts & miscellaneous | $85 | 1.8% |

| Buffer fund | $100 | 2.1% |

| Discretionary | $358 | 7.4% |

| Total Allocated | $4,833 | 100% |

Strategy Notes:

The $4,200 credit card receives $630 monthly total ($130 minimum + $500 extra), eliminating it in 7 months and saving $623 in interest versus minimum-only payments.

After card payoff, that $630 redirects to emergency fund, reaching their 3-month target ($14,500) in 14 additional months. Their approach uses concepts from the snowball vs avalanche debt method.

Example 3: $120,000 Annual Income ($8,250 Monthly Net)

Profile:

- Age: 41

- Location: Denver, Colorado

- Status: Married with two children (ages 6 and 9)

- Debt: $285,000 mortgage (3.75% APR), $12,400 car loan (2.9% APR)

- Primary Goal: Max retirement contributions, build college savings

Complete Monthly Household Budget Breakdown:

| Category | Amount | % of Income |

|---|---|---|

| Mortgage payment | $2,150 | 26.1% |

| Property tax & homeowners insurance | $585 | 7.1% |

| Utilities (all) | $245 | 3.0% |

| Groceries & household supplies | $1,100 | 13.3% |

| Gas & vehicle maintenance | $380 | 4.6% |

| Auto insurance (two vehicles) | $195 | 2.4% |

| Health insurance (family plan) | $580 | 7.0% |

| Life insurance (two policies) | $145 | 1.8% |

| Childcare (after-school program) | $650 | 7.9% |

| Car loan minimum | $285 | 3.5% |

| Total Non-Negotiables | $6,315 | 76.5% |

| 401(k) contribution (already paycheck-deducted, shown for completeness) | ($1,500) | (18.2%) |

| 529 college savings (two accounts) | $500 | 6.1% |

| Emergency fund top-up | $200 | 2.4% |

| Dining out & family activities | $450 | 5.5% |

| Entertainment & subscriptions | $165 | 2.0% |

| Clothing & personal care | $220 | 2.7% |

| Kids activities (sports, music lessons) | $280 | 3.4% |

| Gifts & charitable giving | $120 | 1.5% |

| Travel savings | $200 | 2.4% |

| Discretionary/flex spending | $800 | 9.7% |

| Total Allocated | $8,250 | 100% |

Strategy Notes:

This budget showcases high-income optimization. The mortgage debt at 3.75% APR receives minimum payments while maximizing tax-advantaged retirement accounts (18.2% gross income).

They maintain 6-month emergency fund ($49,500) in a high-yield savings account. College savings receive $500 monthly per federal 529 plan guidelines, projected to reach $95,000 per child by college entry.

Their Investment Calculator showed that prioritizing retirement over extra mortgage payments yields $340,000 additional wealth by age 65 given the interest rate differential and tax advantages.

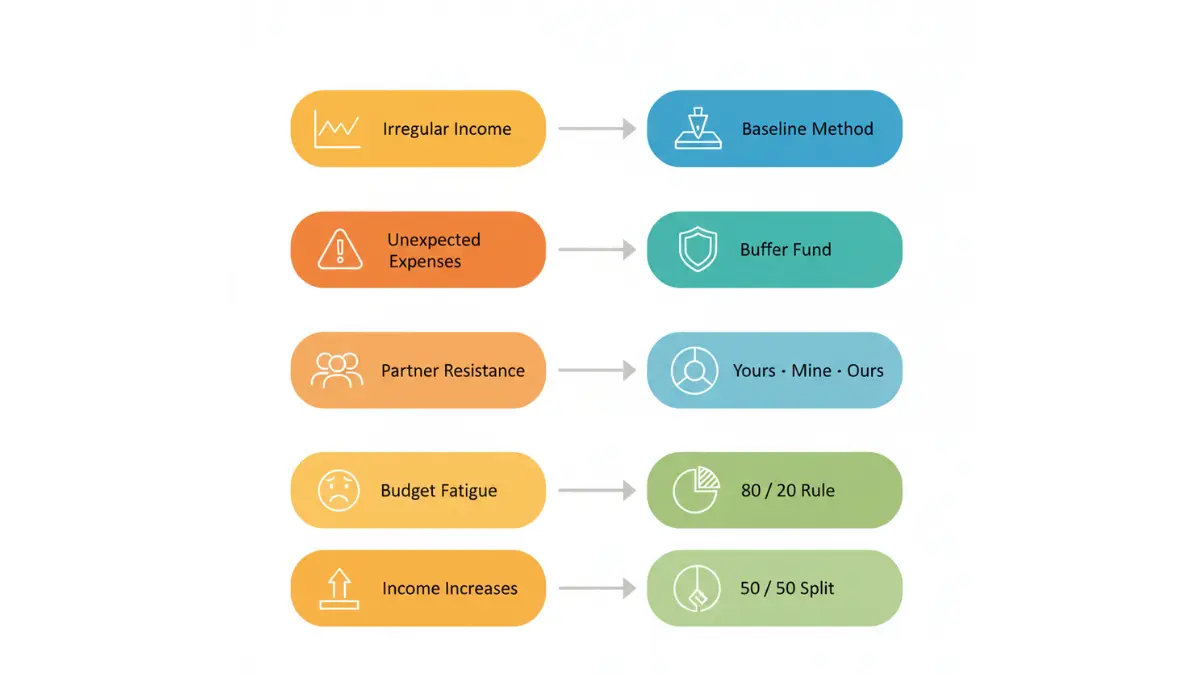

How to Stick to Your Simple Budget (Common Challenges Solved)

Knowing how to budget and actually maintaining it are entirely different. Here’s how to overcome the five most common breaking points.

Challenge 1: Irregular Income (Freelancers, Commission Workers, Gig Economy)

The Problem:

Your income swings from $2,800 to $5,200 monthly. Traditional budgets assume consistency. You overspend in big months and panic in lean months.

The Solution:

Budget on your lowest typical month from the past year. Treat everything above that as “bonus money” with predetermined allocation.

Real Example:

Freelance graphic designer Keisha earned $3,100-$6,400 monthly in 2025. Her baseline budget uses $3,100. Every dollar above that follows a rule: 50% emergency fund, 30% extra debt, 20% discretionary bonus.

In a $5,800 month, she budgets normally on $3,100, then allocates the extra $2,700: $1,350 to emergency fund, $810 to credit card, $540 guilt-free spending. This prevents lifestyle inflation while building financial security during good months.

Challenge 2: Unexpected Expenses Derailing Everything

The Problem:

Your budget is perfect until your dog needs emergency vet care ($680), your tire blows out ($240), and your kid’s school trip requires payment ($85)—all in one month. Budget destroyed.

The Solution:

Build a monthly “stuff happens” line item of $50-150 depending on income. This isn’t your emergency fund—it’s a buffer for small unexpected costs that occur monthly but unpredictably.

Real Example:

Before adding a buffer category, Jordan blew his budget 8 out of 12 months from “surprise” expenses averaging $127 monthly. He added a $150 buffer line. For 6 months running, buffer spending ranged $85-$175. The cushion prevented budget anxiety and kept him on track toward his goal of paying off $30,000 in debt.

Track what hits the buffer. After 3-6 months, patterns emerge. If car repairs consistently drain it, maybe vehicle maintenance needs its own category.

Challenge 3: Partner or Spouse Resisting the Budget

The Problem:

You’re excited about budgeting. Your partner feels controlled, restricted, or annoyed by “checking in” about spending. Resentment builds.

The Solution:

The “Yours, Mine, Ours” system. Each person gets personal discretionary money—no questions asked, no judgment, no tracking. The rest operates transparently.

Real Example:

Combined income: $7,200 monthly. After all shared expenses ($5,800), remaining $1,400 splits: $700 to shared goals (emergency fund, debt), $350 each for pure personal spend.

Partner A spends their $350 on golf and craft beer. Partner B spends theirs on salon visits and books. Neither tracks or justifies personal allocations. Shared categories require agreement, personal categories are sacred.

This approach reduced financial fights by 90% in the first month and maintained budget adherence for 14 months straight.

Challenge 4: Budget Fatigue (It Feels Like Punishment)

The Problem:

Three weeks in, you’re exhausted from tracking every transaction. The simple budget stopped feeling simple. You crave spontaneity.

The Solution:

The 80/20 maintenance approach. Track rigorously for 8 weeks to understand patterns, then shift to spot-checking and monthly reviews only.

Schedule “fun money” first, not as leftovers. Include guilt-free categories: coffee budget ($60), entertainment ($150), spontaneous purchases ($100). Permission spending prevents deprivation psychology.

Real Example:

Mia tracked daily for 2 months, establishing baseline patterns. Month 3: she checked bank app twice weekly for 5 minutes, plus end-of-month full review. Her accuracy stayed within 92% of detailed tracking while dramatically reducing mental load.

She also designated $120 monthly as “no-guilt spending”—could be impulse purchases, extra dining out, last-minute concert tickets. Knowing that money existed removed feelings of restriction.

Challenge 5: Income Increases (Raises, Bonuses, Windfalls)

The Problem:

You get a $4,000 bonus or $200 monthly raise. Within two months, spending inflates and the extra money vanished without improving your financial position.

The Solution:

The 50/50 rule for income increases. Half immediately to financial goals (before you see it), half to sustainable lifestyle improvement.

Real Example:

Raise from $58,000 to $63,000 = $313 monthly increase after tax. Immediately automated $155 to Roth IRA, increased “fun budget” by $155 (dining out, travel savings, entertainment).

Bonus: $3,500 after tax. $1,750 to emergency fund completion, $875 to extra mortgage payment, $875 to vacation fund. The vacation happened without guilt because financial goals advanced simultaneously.

Research from behavioral finance shows people who automate half of raises to savings maintain budget discipline while enjoying lifestyle improvements. Those who plan to “save what’s left” typically save zero.

Quick FAQs About Simple Budgets

1. What is the simplest budget method?

The 50/30/20 rule: 50% to needs, 30% to wants, 20% to savings and debt payoff. Learn more about budget methods.

2. How do I start a budget with no money?

Track spending first. Find $50-100 to cut. Build tiny emergency fund ($250), then address debt systematically.

3. What if I don’t stick to my budget?

Review weekly, adjust categories. Budgets aren’t punishment—they’re plans. Flexibility prevents abandonment.

4. Should I budget if I live paycheck to paycheck?

Absolutely. Budgeting reveals exactly where money goes and finds hidden savings to break the cycle. Use the Debt to Income Ratio Calculator to assess your situation.

5. How often should I check my budget?

Weekly 5-minute check-ins and monthly 10-minute full reviews. Daily checking creates anxiety without benefit.

6. What’s the best free budget app?

Mint for automation and bank linking. Google Sheets for manual control and customization. Both work excellently.

7. How much should I budget for groceries in 2026?

$412 monthly for single person, $824 for family of four, per USDA food cost plans.

8. Can I budget with irregular income?

Yes—budget on your lowest typical month. Treat income above baseline as bonus allocated to predetermined goals.

9. What percentage should go to savings?

20% is ideal, but start with 10% if that’s realistic. Consistency beats perfection always.

10. How do I budget as a couple?

Combine finances for shared goals. Give each partner 15-20% personal spending with no oversight required.

11. When will I see results from budgeting?

First month brings clarity, 3 months builds habit, 6 months shows measurable financial progress and reduced stress.

Disclaimer

Financial Disclaimer: This article provides educational information about budgeting and personal finance strategies. Finance Authority Hub is not a registered financial advisor, certified public accountant, or licensed financial professional. This content does not constitute professional financial, investment, legal, or tax advice.

All budget examples represent hypothetical scenarios based on 2026 average data from government sources including the Bureau of Labor Statistics, U.S. Census Bureau, and U.S. Department of Agriculture. Individual results will vary significantly based on income, geographic location, family size, existing debt obligations, and personal financial circumstances.

Data Accuracy: Cost-of-living figures, salary data, and expense averages are sourced from federal databases and reflect national averages as of January 2026. These figures are subject to change based on economic conditions, regional variations, and individual circumstances. Always verify current data for your specific situation.

No Guaranteed Results: Past budgeting success does not guarantee future financial outcomes. Market conditions, employment status, health events, and numerous other factors affect individual financial results. This guide provides frameworks and strategies, not guarantees.

Investment and Debt Risks: Any discussion of debt payoff strategies, savings allocations, or investment approaches involves financial risk. High-interest debt should generally be prioritized, but individual circumstances vary. Consider consulting a Certified Financial Planner (CFP) for personalized guidance.

Professional Consultation Recommended: Before making significant financial decisions—including large debt payoff strategies, investment allocations, or major purchases—consider consulting licensed professionals: financial advisors for investment guidance, tax professionals for tax implications, and legal counsel for estate planning or complex financial situations.

Third-Party Links: External links to government resources (.gov sites), educational institutions (.edu sites), and financial organizations are provided for informational purposes. Finance Authority Hub does not control these sites and is not responsible for their content, accuracy, or availability.

Updated Information: Financial regulations, tax laws, contribution limits, and economic conditions change regularly. While this content reflects January 2026 data, readers should verify current information before making financial decisions.

By using this information, you acknowledge that you are solely responsible for your financial decisions and outcomes.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.