APR Explained 2026: How a “Normal” Rate Can Cost You $7,723 Extra

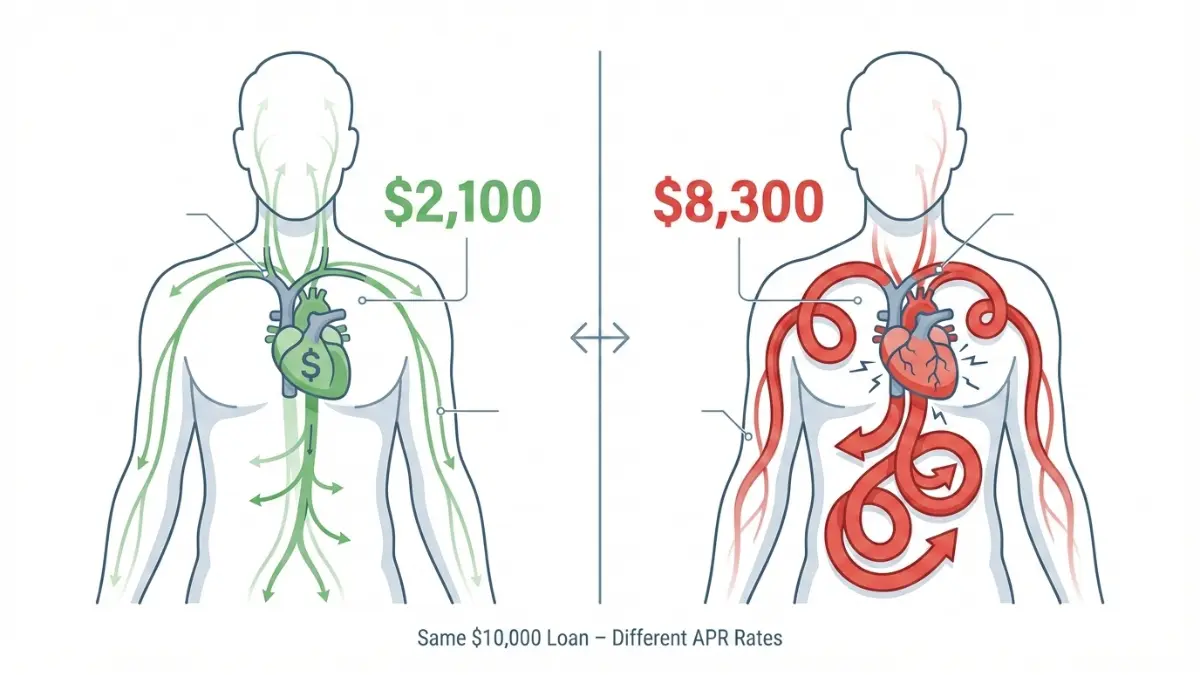

A $5,000 credit card balance at 20% APR costs $7,723 in interest if you only pay minimums — that’s more than the original debt. Compare 2026 APR benchmarks across cards, loans and mortgages, and use our free calculator to see exactly what your rate is costing you.

In This Article

The average American loses $4,827 annually to high APR rates they never negotiated. If you’re carrying a credit card balance at 24% APR, you’re paying $240 in interest for every $1,000 you owe—each year.

This APR guide breaks down exactly what you’re paying and how to stop the bleeding. Updated January 20, 2026, with current Federal Reserve data, we’ll show you the real cost of your annual percentage rate and five proven strategies to lower it.

Whether you’re wondering “is my APR too high?” or searching for the best 0% APR credit cards in 2026, you’ll find clear answers backed by real market data. We’ve analyzed current APR rates across credit cards, auto loans, and mortgages to give you the benchmarks you need.

In this guide, you’ll discover:

- What APR actually means (in 60 seconds)

- 2026 APR benchmarks by credit score

- How to lower your credit card APR using negotiation scripts

- The 7 costliest APR mistakes to avoid

Let’s calculate what your rate is really costing you.

What Is APR? (The 60-second Answer)

APR Meaning: The Simple Definition

APR stands for Annual Percentage Rate—the yearly cost of borrowing money expressed as a percentage. Your APR rate includes the interest rate plus any fees the lender charges, giving you the true cost of a loan or credit card.

Think of APR as the price tag on borrowed money. A credit card with 18% APR means you’ll pay $180 in interest annually for every $1,000 you carry as a balance.

How APR Works in Real Life

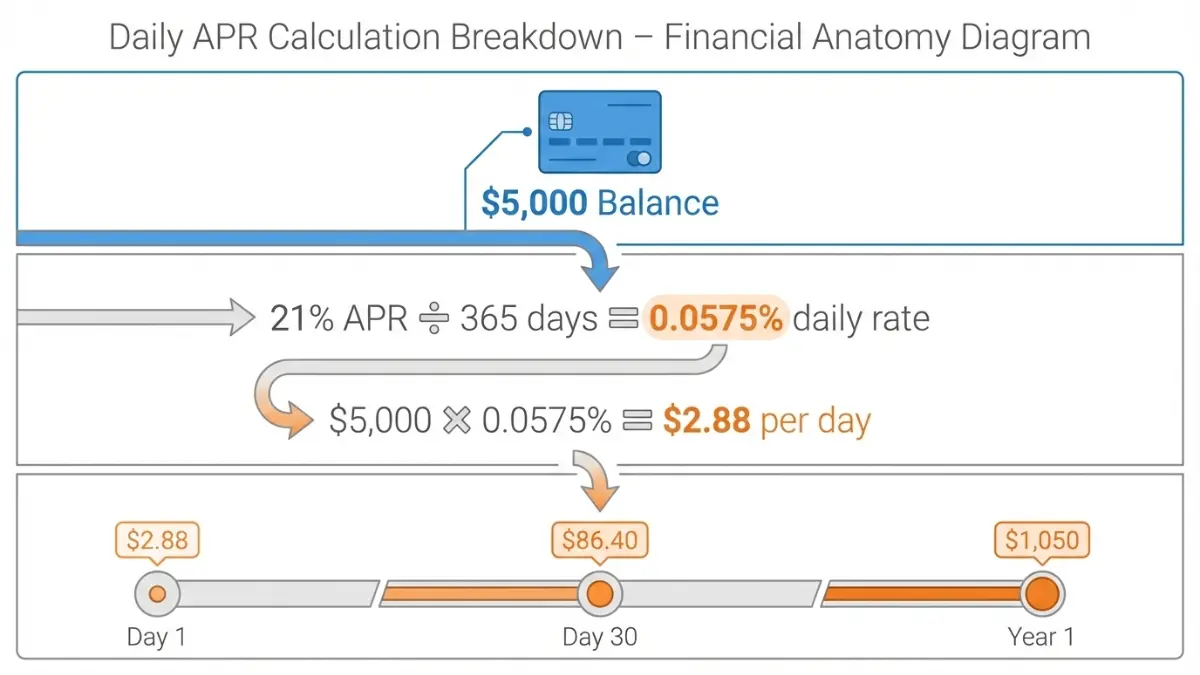

Here’s where APR gets expensive: credit card companies calculate interest daily, not yearly. They divide your annual percentage rate by 365 to get your daily periodic rate, then multiply that by your balance each day.

Real example: You have a $5,000 balance at 21% APR.

- Daily rate: 21% ÷ 365 = 0.0575% per day

- Daily interest charge: $5,000 × 0.0575% = $2.88

- Monthly interest: ~$86.40

- Annual cost: $1,050 in interest alone

That’s $1,050 you’re paying just to borrow your own $5,000. If you only make minimum payments, you’ll spend 13 years paying it off and shell out $6,923 in total interest according to Consumer Financial Protection Bureau calculations.

APR Rate vs Interest Rate: The Critical Difference

Many people confuse APR with the interest rate, but there’s a crucial distinction:

Interest rate = The base cost to borrow money APR = Interest rate + origination fees + closing costs + other charges

For mortgages and auto loans, APR is typically higher than the interest rate because it includes upfront fees. For credit cards, APR and interest rate are usually the same since cards rarely have upfront fees.

Understanding this difference helps you compare loan offers accurately. A 6.5% interest rate with $3,000 in fees might have a 7.1% APR—making it more expensive than a 6.8% rate with lower fees.

Types Of APR & What They Cost You

6 Types of APR You Need to Know in 2026

Not all APR rates are created equal. Credit card issuers use different annual percentage rates for different transactions—and some cost you significantly more than others.

Purchase APR (What Most People Pay)

This is the APR rate applied to regular purchases made with your credit card. As of January 2026, the average credit card APR is 21.47% according to the Federal Reserve’s most recent consumer credit data.

If you pay your balance in full each month, purchase APR doesn’t matter—you won’t pay interest. But carry a balance, and this rate kicks in immediately.

Balance Transfer APR

Balance transfer APR applies when you move debt from one card to another. Many credit cards offer 0% APR promotional periods lasting 12-21 months in 2026.

Strategy tip: Transferring $8,000 from a 24% APR card to a 0% APR card for 18 months saves you $2,880 in interest. Just watch for balance transfer fees (typically 3-5% of the amount transferred).

Cash Advance APR (The Expensive Trap)

Cash advance APR is the costliest type—averaging 29.99% in 2026. Worse, interest starts accruing immediately with no grace period.

Real cost example: Withdraw $500 cash at 29.99% APR.

- One month: $12.50 in interest

- Six months: $78.44 in interest

- One year: $162.78 in interest

- Plus a 5% cash advance fee ($25) upfront

That “quick $500” actually costs you $187.78 in the first year. Use your debit card or personal loan instead—both are cheaper alternatives.

Penalty APR (How to Avoid It)

Miss a payment by 60+ days, and issuers can hit you with penalty APR—often 29.99% under the Credit CARD Act guidelines.

Penalty APR triggers:

- Payment 60+ days late

- Returned payment due to insufficient funds

- Exceeding your credit limit (on some cards)

The good news: Federal law requires issuers to review your account after six months of on-time payments and potentially restore your original rate.

Promotional 0% APR (Read the Fine Print)

Many cards offer 0% APR for 12-21 months on purchases or balance transfers. After the promotional period ends, the standard APR kicks in—typically 18-24%.

Critical detail: If you have a remaining balance when the promo period ends, you’ll pay the regular APR rate going forward on that balance. Some store cards apply “deferred interest,” charging you retroactive interest on the original balance if not paid in full—avoid these offers.

Variable vs Fixed APR

Most credit cards have variable APR tied to the Prime Rate, which moves with Federal Reserve rate changes. As of January 2026, the Prime Rate is 7.50% after recent Fed cuts.

What this means: When the Fed lowers rates (as they did in December 2025), your variable APR decreases too. When rates rise, your APR increases, typically within one billing cycle.

Fixed APR rates can change too—issuers just need to give you 45 days’ notice. “Fixed” doesn’t mean permanent.

What’s A Good APR In 2026? (Benchmark Guide)

What’s a Good APR? 2026 Benchmarks by Product & Credit Score

“Is 24% APR bad?” The answer depends on your credit profile and the type of loan. Here are the current benchmarks based on January 2026 market data.

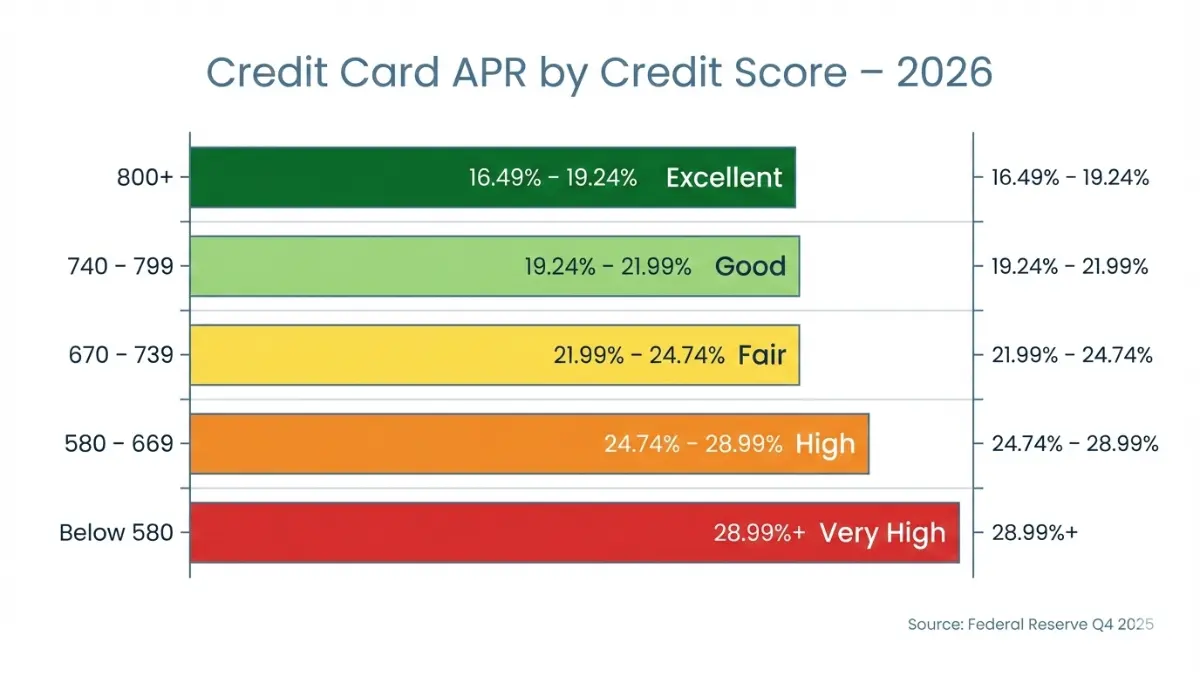

Credit Card APR Ranges (By Credit Score)

Your credit score dramatically impacts your APR rate. Here’s what to expect based on FICO score tiers and current Federal Reserve data:

| Credit Score Range | Average Credit Card APR | APR Quality |

|---|---|---|

| 800+ (Exceptional) | 16.49% – 19.24% | Excellent |

| 740-799 (Very Good) | 19.24% – 21.99% | Good |

| 670-739 (Good) | 21.99% – 24.74% | Fair |

| 580-669 (Fair) | 24.74% – 28.99% | High |

| Below 580 (Poor) | 28.99%+ | Very High |

Reality check: If you have a 720 credit score and you’re paying 26% APR, you’re overpaying by roughly 4-5%. Time to negotiate or consider a balance transfer to a lower rate card.

Auto Loan APR Standards 2026

Auto loan APR rates vary significantly between new and used vehicles. Current January 2026 rates from major lenders:

New Car Loans:

- Excellent credit (720+): 5.89% – 7.19%

- Good credit (680-719): 7.19% – 9.44%

- Fair credit (620-679): 9.44% – 13.89%

Used Car Loans:

- Excellent credit (720+): 7.39% – 9.19%

- Good credit (680-719): 9.19% – 12.94%

- Fair credit (620-679): 12.94% – 18.39%

Pro tip: Use our Auto Loan Calculator to see how a 2% APR difference impacts your total payment over the loan term.

Mortgage APR Current Rates

As of January 20, 2026, Freddie Mac’s Primary Mortgage Market Survey shows:

- 30-year fixed mortgage APR: 6.82% – 7.43%

- 15-year fixed mortgage APR: 6.11% – 6.68%

- 5/1 ARM APR: 6.34% – 6.89%

Your actual rate depends on credit score, down payment size, and debt-to-income ratio. A 740+ credit score with 20% down typically qualifies for rates at the lower end of these ranges.

Calculate your potential mortgage payment using our Mortgage Calculator with current 2026 APR rates.

Personal Loan APR Expectations

Personal loan annual percentage rates range from 7.99% to 35.99% in 2026, with most creditworthy borrowers receiving:

- Excellent credit (720+): 7.99% – 12.49%

- Good credit (680-719): 12.49% – 17.99%

- Fair credit (620-679): 17.99% – 25.99%

Benchmark: Anything below 15% APR for a personal loan is considered competitive in the current market. Above 20% APR, explore alternatives like a 0% balance transfer credit card or home equity line of credit.

Your APR rate is negotiable—especially if your credit score has improved since you opened the account. Let’s look at how to lower it.

How To Lower Your APR (Actionable Tactics)

How to Lower Your APR: 5 Proven Strategies That Work in 2026

Your APR rate isn’t set in stone. Here are five strategies to reduce what you’re paying, backed by real success rates.

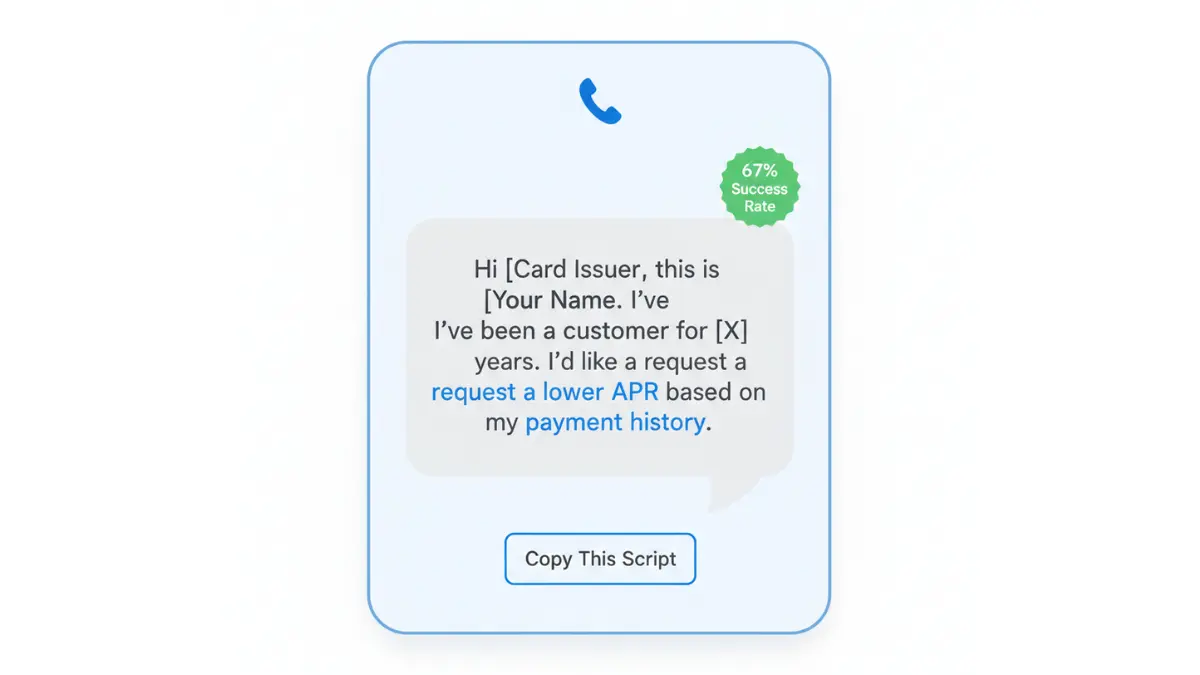

Strategy #1: The APR Negotiation Script (Word-for-Word)

67% of cardholders who requested a lower APR received one, according to a 2025 LendingTree survey. Yet only 28% ever ask.

Here’s the exact script that works:

“Hi [Card Issuer], this is [Your Name], account number [XXXX]. I’ve been a customer for [X] years and have maintained an excellent payment history. I recently received offers from other issuers with APR rates between [Y]% and [Z]%—significantly lower than my current [Current APR]%. Can you reduce my rate to remain competitive? I’d prefer to keep my account with you if we can match these offers.”

Best time to call: After 6+ months of on-time payments, or after your credit score increases by 30+ points.

Backup approach: If denied, ask when you can request again and what credit behaviors would improve your chances. Many issuers will reconsider after 6 months of perfect payment history.

Strategy #2: Balance Transfer Method

Moving high-APR debt to a 0% balance transfer card can save thousands. In 2026, top offers include 18-21 month promotional periods.

Real savings calculation:

- Starting balance: $8,000 at 24% APR

- Transfer to: 0% APR for 18 months (3% transfer fee = $240)

- Interest saved: $2,880 – $240 fee = $2,640 net savings

Critical success factor: Create a payoff plan dividing your balance by the promotional months. For $8,000 over 18 months, that’s $444/month to eliminate debt before the standard APR hits.

Our Credit Card Payoff Calculator shows your exact savings timeline.

Strategy #3: Credit Score Improvement Fast-Track

Every 50-point credit score increase typically reduces your APR by 3-5%. Here’s how to boost your score quickly:

30-day actions:

- Pay down credit cards below 30% utilization (20+ point boost)

- Dispute errors on credit reports (10-30 point increase if errors found)

- Become an authorized user on a family member’s old card with perfect history (10-40 point boost)

90-day actions:

- Make all payments on time (builds positive history)

- Pay down balances below 10% utilization (30+ point increase)

- Avoid new credit applications (prevents hard inquiries)

Check our complete credit score guide for detailed improvement strategies.

Strategy #4: Refinancing When It Makes Sense

For auto loans and mortgages, refinancing to a lower APR rate saves money—if you qualify and plan to keep the loan long enough to recoup closing costs.

Auto loan refinancing: If rates dropped 2+ percentage points since you bought your car, or your credit score improved 50+ points, refinancing typically makes sense.

Mortgage refinancing: With 2026 rates hovering around 6.8%-7.4%, refinancing makes financial sense if:

- Your current rate is 8%+

- You plan to stay in the home 3+ years

- You have 20%+ equity (avoids PMI)

Use our Mortgage Refinance Calculator to determine your break-even point.

Strategy #5: Federal Rate Changes to Your Advantage

The Federal Reserve cut rates by 0.25% in December 2025, with analysts projecting another 0.50% in cuts through 2026. Variable APR rates on credit cards adjust within 1-2 billing cycles after Fed changes.

How to capitalize:

- If you have variable-rate debt: Your APR should automatically decrease. Verify the reduction appears on your next statement.

- If you have fixed-rate debt: Refinance to a variable rate product if Fed cuts continue, or negotiate a lower fixed rate citing current market conditions.

- If you’re debt-free: Lock in current mortgage or auto loan rates before potential Fed rate increases in 2027.

According to the Federal Reserve’s meeting schedule, the next rate decision comes March 19, 2026.

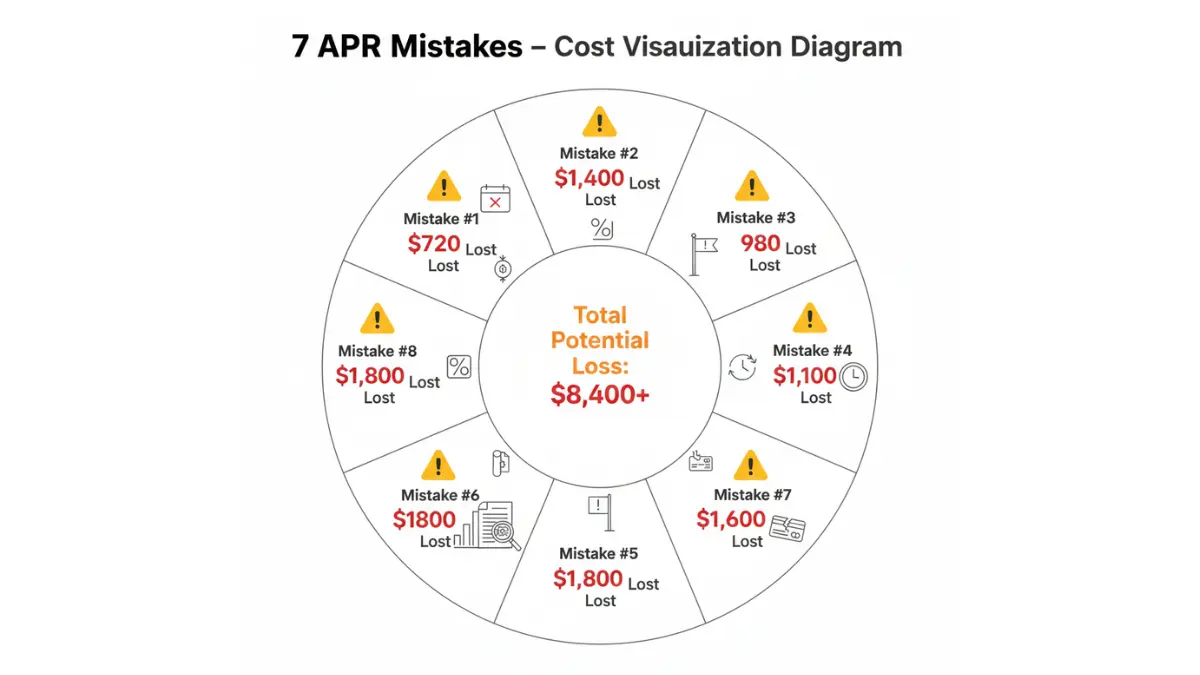

APR Mistakes That Cost You Money

7 Costly APR Mistakes to Avoid in 2026

Even financially savvy people make these APR mistakes. Here’s what to watch out for:

Mistake #1: Ignoring Variable APR Rate Caps

Variable APR cards don’t increase infinitely. Federal regulations cap how much your rate can jump per adjustment, but many cardholders don’t know their card’s maximum rate.

Check your cardholder agreement: Most cards cap at 29.99% APR, but some premium cards cap at 24.99%. If you’re near the cap with a variable-rate card, consider switching to a fixed-rate product or consolidating debt at a locked rate.

Mistake #2: Missing Promotional 0% APR End Dates

Missing your 0% APR expiration date is expensive. The moment the promotional period ends, your remaining balance gets hit with the standard APR rate—often 19-26%.

Real cost: $3,000 remaining balance when 0% APR ends = $720 in annual interest at 24% APR.

Solution: Set phone reminders 30 and 60 days before your promotional APR expires. Use our Debt Payoff Calculator to create a payment schedule that eliminates debt before the deadline.

Mistake #3: Triggering Penalty APR

One payment 60+ days late can spike your APR to 29.99% and keep it there for six months minimum. That late payment also damages your credit score by 60-110 points.

Prevention: Set up automatic minimum payments. You can always pay extra manually, but automatic payments prevent accidental late fees and penalty APR.

Mistake #4: Not Negotiating APR Annually

Your credit score improves, average market rates drop, but your APR stays the same? That’s leaving money on the table.

Action item: Request an APR review every 12 months, especially after:

- Credit score increases 40+ points

- 12 consecutive on-time payments

- Federal Reserve rate cuts

- Market APR decreases

Mistake #5: Confusing APR with Total Interest Paid

APR tells you the annual cost, but not the total interest you’ll pay over time. A $5,000 balance at 18% APR with minimum payments results in $3,427 in total interest over 13 years—not $900 (one year of interest).

Reality check: Use an APR Calculator to see your true long-term cost, not just the annual percentage rate.

Mistake #6: Paying Only Minimum with High APR

Minimum payments are calculated to maximize bank profits—typically 1-3% of your balance. At this rate, you’re mostly paying interest, barely touching principal.

Real numbers: $5,000 balance at 22% APR with 2% minimum payments:

- Time to pay off: 19 years, 8 months

- Total interest: $6,923

- Total paid: $11,923 (240% of original debt)

Solution: Pay at least double the minimum, or follow the debt snowball vs avalanche method to eliminate balances faster.

Mistake #7: Not Comparing APR Before Applying

That “pre-approved” credit card offer might have a 26% APR while you qualify for 16% cards. Always compare annual percentage rates across multiple issuers before applying.

Research tools: Check comparison sites and use your bank’s pre-qualification tools that show APR ranges without impacting your credit score.

APR GUIDE: 11 MOST ASKED QUESTIONS (2026)

1. Is 24% APR bad for a credit card?

Yes, 24% APR is above average for 2026. The national average is 21.47%, so you’re paying roughly 2.5% more than typical cardholders. With good credit (670+ score), you should qualify for 19-22% APR. If your score is 740+, aim for under 19% APR.

2. Does APR matter if I pay my balance in full each month?

No. If you pay your full statement balance by the due date, you won’t pay any interest regardless of your APR rate. The grace period (typically 21-25 days) means purchase APR only applies to carried balances.

3. Can my APR change after I’m approved?

Yes. Variable APR rates change with the Prime Rate, typically within one billing cycle of Federal Reserve decisions. Fixed APR can also change—issuers must give 45 days’ notice. Penalty APR (up to 29.99%) applies after 60+ days late payment.

4. What’s the difference between APR and APY?

APR shows what you pay on loans and credit cards (cost of borrowing). APY shows what you earn on savings accounts (return on deposits). APY accounts for compound interest, making it higher than the stated interest rate. A savings account with 4.5% interest compounded daily has a 4.60% APY.

5. How is APR calculated on credit cards?

Credit cards use daily periodic rates: Annual APR ÷ 365 = daily rate. That daily rate multiplies by your balance each day. Interest compounds daily and posts to your account monthly. Formula: (Balance × Daily Rate) × Days in Billing Cycle = Monthly Interest Charge.

6. Can I negotiate my APR with my credit card company?

Yes. 67% of cardholders who asked received an APR reduction in 2025. Call your issuer, reference your payment history and competing offers, and request a rate review. Best success rates come after 6+ months of on-time payments or credit score improvements.

7. What credit score do I need for a good APR?

740+ credit score typically qualifies for the best APR rates: 16-19% on credit cards, 5.8-7.2% on auto loans, and 6.8-7.1% on mortgages. Scores of 800+ may qualify for premium rates 1-2% lower than standard offers.

8. Does checking my APR hurt my credit score?

No. Checking your current APR rate on existing accounts is a soft inquiry that doesn’t affect your credit. Applying for new credit triggers a hard inquiry, which temporarily lowers your score by 5-10 points for 3-6 months.

9. Why is cash advance APR higher than purchase APR?

Cash advances carry higher risk for issuers—they can’t be disputed like purchases, have no fraud protection, and see higher default rates. Average cash advance APR is 29.99% in 2026, with interest starting immediately and no grace period.

10. How do Federal Reserve rate changes affect my APR?

Most credit cards have variable APR tied to the Prime Rate, which moves with Fed rate changes. When the Fed cuts rates (like December 2025’s 0.25% cut), your APR decreases within 1-2 billing cycles. When rates rise, APR increases similarly.

11. What happens to my APR if I miss a payment?

Missing a payment by 30 days triggers a late fee ($30-$40) but doesn’t change your APR. At 60+ days late, penalty APR (typically 29.99%) applies to your entire balance and remains for at least six months of on-time payments.

Financial Disclaimer

This APR guide is for educational purposes only and should not be construed as personalized financial advice. We are not licensed financial advisors, and nothing in this article constitutes a recommendation to apply for specific financial products.

APR rates vary by lender, individual creditworthiness, and market conditions. All data is current as of January 20, 2026, but rates change frequently. We strongly recommend consulting a certified financial advisor or credit counselor before making significant credit decisions.

Past APR rates do not guarantee future rates. Market conditions, Federal Reserve policy, and individual credit profiles influence available rates.

We may earn commissions from financial institutions mentioned in this article. This potential compensation does not influence our editorial integrity or the information provided. All recommendations are based on merit and current market analysis.

For concerns about your debt load or credit management, contact the National Foundation for Credit Counseling at 1-800-388-2227 for free guidance.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.