Budget Calculator: Plan Your Money in Seconds (2026)

Budget Calculator

Create a detailed budget using monthly equivalents, then see surplus/deficit, annual projections, and deep breakdowns by needs/wants/savings/debt and categories.

Inputs

Classify each outflow as Need / Want / Savings-Investing / Debt payments for better insights.

Results

Net cashflow (monthly)

—

Net cashflow (annualized): —

As of: —

Income

—

Annualized: —

Outflows

—

Annualized: —

Savings rate (goals)

—

Needs: — • Wants: —

Goals (save+debt): —

50/30/20 benchmark (difference vs target)

Needs vs 50%

Delta: —

Wants vs 30%

Delta: —

Goals vs 20%

Delta: —

The 50/30/20 rule is a common guideline that splits after-tax income into needs, wants, and savings/debt. [web:32]

Outflows by group (Needs/Wants/Savings/Debt)

| Group | Monthly | Annualized | % of income |

|---|

Outflows by category (sorted)

| Category | Monthly | Annualized | % of outflows |

|---|

All line items (income + expenses)

| Item | Category | Group | Frequency | Monthly equivalent | Annualized | % of income |

|---|

If you want a “zero-based budget” mode, we can add an “Allocate leftover” step so income minus allocated outflows ends at zero. [web:42]

Results appear after you click “Calculate.”

In This Article

A budget calculator is a free online tool that shows you exactly where your money goes — instantly. Enter your income and expenses, and it calculates your net cash flow, savings rate, and monthly surplus or deficit in seconds. Whether you earn $30,000 or $130,000 a year, a personal budget calculator gives you the financial clarity to stop overspending and start building wealth.

What Is a Budget Calculator and How Does It Work?

A budget calculator is a digital financial planning tool that converts all your income sources and expenses into a clear monthly picture. It computes your net cash flow, shows how your spending compares to proven benchmarks, and flags exactly where your money is going — instantly, with zero math required.

According to the Consumer Financial Protection Bureau (CFPB), nearly half of Americans do not have a working budget — a leading reason people fall behind on bills and accumulate high-interest debt. A monthly budget calculator solves this problem in under five minutes.

How This Free Budget Calculator Works

Our budget calculator uses frequency-adjusted math — meaning you can enter expenses as weekly, bi-weekly, monthly, quarterly, or annual amounts. The tool automatically converts everything into a monthly-equivalent figure so your results are always accurate.

Here’s what makes this tool different from every competitor:

- Multi-currency support — USD, GBP, EUR, CAD, AUD, and 17 more

- Needs / Wants / Savings / Debt classification — categorize every expense for deeper insight

- 50/30/20 benchmark bars — see instantly if you’re over or under on each category

- Annualized projections — see your full-year financial picture, not just one month

- CSV export — download your complete budget breakdown for offline tracking

What You Need to Get Started

Before using this free income and expense calculator, gather:

- ✅ Your net monthly income (take-home pay after taxes — not gross)

- ✅ Last month’s bank and credit card statements

- ✅ A list of fixed bills (rent, insurance, loan payments)

- ✅ Estimates for variable spending (groceries, dining, subscriptions)

Monthly vs. Annual Budget: Quick Reference

| Budget Type | Best For | How to Use It |

|---|---|---|

| Monthly budget | Day-to-day cash flow control | Track income and expenses every 30 days |

| Annual budget | Big-picture planning, irregular expenses | Divide annual bills (car registration, insurance) by 12 |

| Zero-based budget | Maximum financial discipline | Every dollar assigned a job; income minus expenses = $0 |

The Federal Trade Commission’s consumer budgeting guide recommends starting with a monthly budget before scaling to annual planning — exactly the approach this calculator uses.

The 50/30/20 Budget Rule Explained (With 2026 Benchmarks)

The 50/30/20 rule is the most widely used personal budget framework in the United States. It divides your after-tax income into three clear categories:

- 50% → Needs: Rent/mortgage, utilities, groceries, insurance, minimum debt payments

- 30% → Wants: Dining out, entertainment, subscriptions, travel

- 20% → Goals: Savings, investments, retirement contributions, extra debt repayment

This framework was popularized by U.S. Senator Elizabeth Warren and is now the default benchmark used by NerdWallet, Fidelity, and most major financial institutions.

2026 Real Data: How Americans Actually Spend

The U.S. Bureau of Labor Statistics 2023 Consumer Expenditure Survey (the most recent complete data available) shows the average American household spends:

| Category | % of Budget | Annual Average |

|---|---|---|

| Housing | 32.9% | $25,436 |

| Transportation | 17.0% | $13,174 |

| Food (all) | 12.9% | $9,985 |

| Healthcare | 8.0% | $6,159 |

| Entertainment | 4.7% | $3,639 |

| Education | 2.4% | $1,853 |

| Savings / Investments | ~7–10% | Varies by income |

What this means for you: Most households are already over the 50% needs threshold — primarily driven by housing costs. If your rent or mortgage exceeds 30% of your income alone, the standard 50/30/20 rule may need adjustment.

When 50/30/20 Doesn’t Work — And What to Use Instead

The 50/30/20 rule is a starting point, not a law. Here are three alternatives:

| Method | Best For | Core Rule |

|---|---|---|

| Zero-Based Budget | High earners who want maximum control | Income – All Expenses = $0 |

| Reverse Budget | Savers who pay themselves first | Save first, spend the rest |

| Envelope Method | People prone to overspending | Cash allocated in physical envelopes per category |

Our 50-30-20 Budget Analysis breaks down when each method wins — and why the envelope system is making a 2026 comeback.

💡 Key Takeaway: This budget calculator automatically calculates your 50/30/20 split and shows you the exact dollar gap between your current spending and the target — something no competitor tool does in real time.

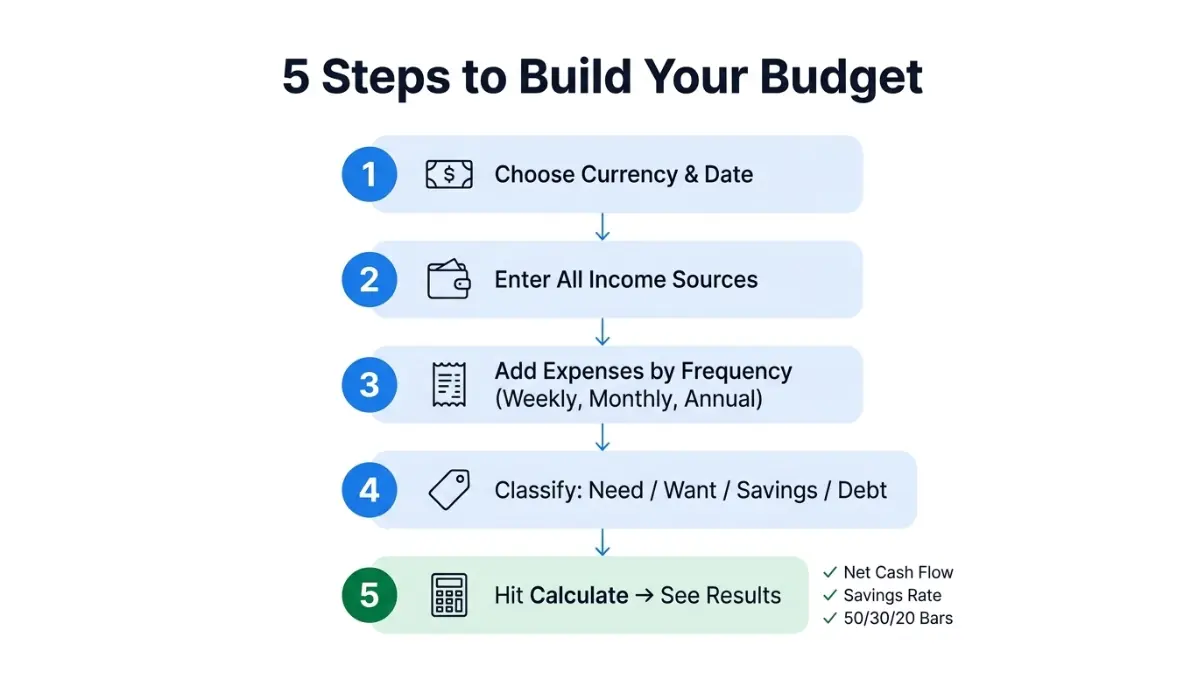

How to Use This Free Budget Calculator — Step-by-Step

Using this monthly budget calculator takes less than five minutes. Follow these steps exactly for the most accurate results.

Step 1: Choose Your Currency and Date

Select your currency from the dropdown (22 currencies available). Enter an optional “as-of” date to time-stamp your budget snapshot — useful when comparing month-to-month progress.

Step 2: Enter All Income Sources

Add every income stream separately for accuracy:

- Primary salary or wages

- Freelance or side hustle income

- Rental income

- Investment dividends

- Any government benefits or pension

Pro Tip: Always use your net income (after taxes and deductions). Using gross income will make your budget look larger than it actually is — the single most common mistake in personal budgeting.

Step 3: Add Every Expense With the Correct Frequency

This is where most household budget calculators fall short. Our tool lets you enter expenses at their natural frequency:

- Weekly → groceries, fuel

- Bi-weekly → gym membership, some utilities

- Monthly → rent, insurance, subscriptions

- Quarterly → estimated taxes, pest control

- Annual → car registration, insurance premiums

The calculator converts everything to a monthly equivalent automatically. A $600 annual car registration becomes $50/month in your budget — accurately reflected in your results.

Step 4: Classify Each Expense

For every expense, choose one group:

- Need → essential survival expenses

- Want → discretionary spending

- Savings / Investing → retirement, brokerage, emergency fund

- Debt Payments → credit cards, student loans, auto loans

If credit card debt is eating your budget, use our Credit Card Payoff Calculator to build a payoff timeline alongside your budget.

Step 5: Hit Calculate — Here’s How to Read Your Results

Once you click Calculate, you’ll see:

| Result Metric | What It Tells You |

|---|---|

| Net Cash Flow (Monthly) | Green = surplus. Red = deficit. |

| Annualized Net | Your financial trajectory over 12 months |

| Savings Rate | % of income going to savings + debt payoff |

| 50/30/20 Bars | Visual gap vs. recommended benchmarks |

| Category Breakdown Table | Where every dollar is going, sorted by amount |

Download your results using the CSV Export button — a feature no competitor’s free budget calculator offers.

Budget Benchmarks by Income Level (2026 Data)

Most budget guides give you generic rules. This section gives you income-specific benchmarks — the exact numbers that apply to your household.

How Much Should You Spend on Housing in 2026?

The traditional rule is no more than 28–30% of gross income on housing. But in 2026, with median rent at record highs in most Tier 1 markets, many households are being forced above this threshold.

Housing affordability benchmarks by income:

| Annual Income | Max Recommended Rent/Mortgage | Reality (2026 avg.) |

|---|---|---|

| $35,000 | $819/month | $1,100+/month in most cities |

| $55,000 | $1,292/month | $1,400–$1,800/month |

| $75,000 | $1,750/month | On target in most markets |

| $100,000+ | $2,333/month | Comfortable range |

If housing costs are straining your budget, our Home Affordability Calculator can show you exactly what mortgage or rent you can realistically carry — before you sign anything.

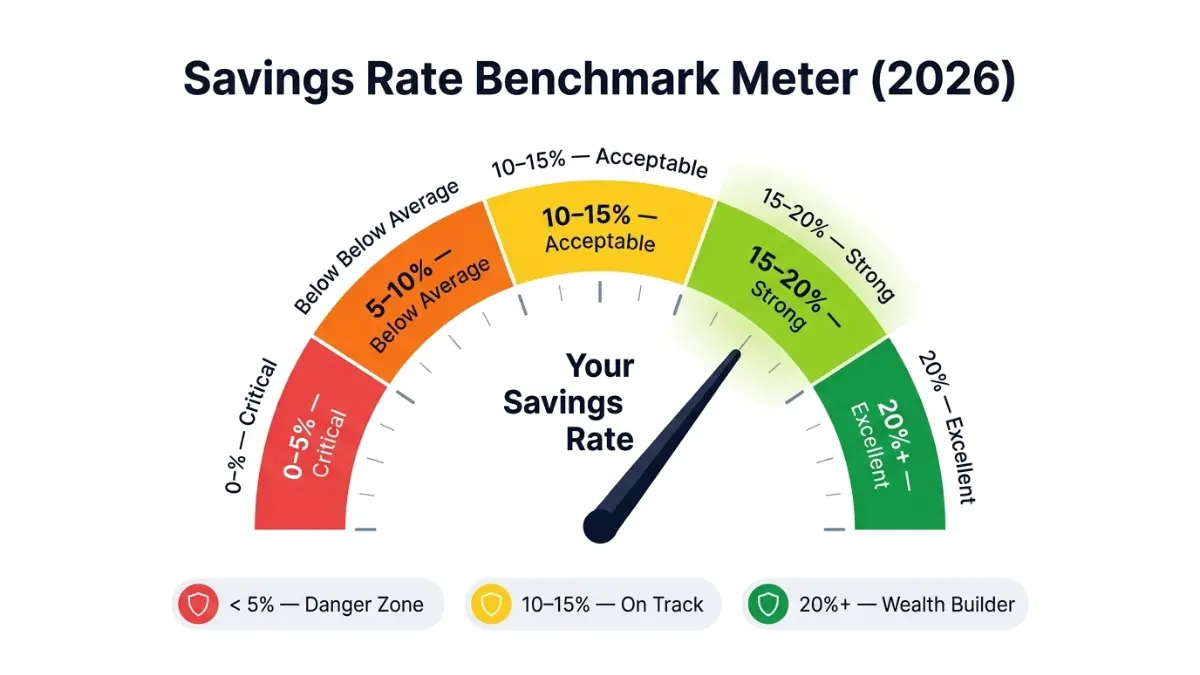

Savings Rate Benchmarks: Are You on Track?

Certified Financial Planner Laura M. Bennett notes: “A 15–20% savings rate is the gold standard for building long-term financial security in the U.S. market. Below 10%, most households remain one emergency away from debt.”

| Savings Rate | Status | Action Needed |

|---|---|---|

| < 5% | Critical | Immediate budget restructure required |

| 5–10% | Below benchmark | Identify 2–3 spending cuts this month |

| 10–15% | Acceptable | On track; push toward 15% |

| 15–20% | Strong | Invest surplus for compound growth |

| 20%+ | Excellent | Optimize investment allocation |

Use our Savings Calculator to project how today’s savings rate translates into wealth over 10, 20, and 30 years.

Average Monthly Expenses by Household Type (2026)

| Household Type | Avg. Monthly Expenses | Top Cost Driver |

|---|---|---|

| Single adult | $3,200–$4,100 | Housing |

| Couple, no kids | $4,800–$6,200 | Housing + Transportation |

| Family of 4 | $7,000–$9,500 | Housing + Childcare + Food |

| Retiree household | $3,800–$5,200 | Healthcare + Housing |

Source: BLS Consumer Expenditure Survey 2023 (most recent complete data)

CPA/CFP Daniel Moreau adds: “The biggest budget mistake families make is planning only for fixed expenses. Variable and irregular costs — car repairs, medical bills, school fees — add 15–20% to actual monthly spending versus what’s planned.”

Build irregular expenses into your plan using our Emergency Fund Guide — a critical step most budgeters skip entirely.

7 Budgeting Mistakes That Destroy Your Finances (And How to Fix Them Fast)

Mistake 1: Using Gross Income Instead of Net Income

The problem: Budgeting based on your $60,000 salary when you only take home $46,000 creates a phantom budget that instantly fails.

Quick Fix: Always enter your take-home pay — the number on your actual paycheck after taxes, health insurance, and 401(k) deductions.

Mistake 2: Forgetting Irregular Expenses

The problem: Annual bills like car registration, holiday gifts, and insurance renewals blindside most budgets because they’re not monthly.

Quick Fix: Divide all annual costs by 12 and add them as monthly line items. A $1,200 car insurance renewal = $100/month in your personal budget calculator.

Mistake 3: Mixing Up Needs and Wants

The problem: Calling a Netflix subscription a “need” inflates your needs percentage and masks where money is truly going.

Quick Fix: Apply this test — “Would I lose my job, home, or health without this?” If no, it’s a want. Use the Needs/Wants/Savings/Debt classification in this tool for an honest breakdown.

Mistake 4: No Emergency Fund Line Item

The problem: Budgets without an emergency fund category collapse the moment an unexpected expense hits — pushing people into credit card debt.

Quick Fix: Add a minimum $50–$200/month “Emergency Savings” line as a Savings category item. Start small; the habit matters more than the amount. For target amounts by income level, see our Emergency Fund Calculator.

Mistake 5: Treating Minimum Debt Payments as “Enough”

The problem: Making only minimum payments on credit cards and loans costs thousands in interest and keeps you trapped in a debt cycle.

Quick Fix: In your budget, classify debt payments separately and aim to pay more than the minimum. Use our Debt Consolidation Calculator to see how consolidating high-interest debt can reduce monthly payments and total interest paid. For deeper strategies, our Snowball vs. Avalanche guide compares both debt payoff methods with real numbers.

Mistake 6: Never Updating Your Budget

The problem: A budget made in January is useless by June if income or expenses have changed.

Quick Fix: Schedule a 15-minute monthly budget review on the first day of each month. Update your monthly budget calculator with actual figures from your bank statement, not estimates.

Mistake 7: Setting an Unrealistic Budget

The problem: Budgets that cut too aggressively fail within two weeks. Slashing dining from $400 to $50 overnight almost never sticks.

Quick Fix: Make 10–15% reductions per category at a time. Sustainable change beats aggressive restriction every time. Our Simple Budget Guide outlines a realistic first-budget framework used by over 50,000 readers.

Frequently Asked Questions About Budget Calculators

1. What is a budget calculator?

A budget calculator is a free online tool that subtracts your monthly expenses from your monthly income to show your net cash flow, savings rate, and spending breakdown by category. It replaces manual spreadsheets with instant, automated results.

2. How do I calculate my monthly budget?

List all income sources (net of taxes), list every expense by category, classify each expense as Need/Want/Savings/Debt, and subtract total expenses from total income. A positive number means surplus; a negative number means deficit.

3. What is the 50/30/20 rule in budgeting?

The 50/30/20 rule allocates 50% of after-tax income to needs (rent, utilities, food), 30% to wants (dining, entertainment), and 20% to savings and debt repayment. It is a guideline, not a rigid rule — income level and cost of living affect what percentages are realistic.

4. How much of my income should go to rent?

The traditional rule is no more than 28–30% of gross monthly income on housing. In high-cost markets like New York, San Francisco, and London, many households exceed this — which means cutting other categories accordingly.

5. What is a good savings rate per month?

Financial experts recommend saving at least 15–20% of net income. Below 10% leaves most households financially vulnerable. Use our Retirement Calculator to see how your current savings rate affects long-term retirement readiness.

6. How do I budget with a low income?

Start with zero-based budgeting — assign every dollar a job, prioritize housing, utilities, and food first, then allocate what remains. Even saving $25/month builds the habit. The Break Paycheck-to-Paycheck Cycle plan offers a 30-day structured approach.

7. What is zero-based budgeting?

Zero-based budgeting means your income minus all planned expenses, savings, and debt payments equals exactly zero. Every dollar has an assigned purpose. It is more labor-intensive than the 50/30/20 method but delivers maximum control over spending.

8. What expenses should be in a personal budget?

A complete personal budget should include: housing, utilities, groceries, transportation, insurance (health, auto, life), healthcare, subscriptions, dining, entertainment, clothing, debt payments, emergency savings, and retirement contributions. Our budget calculator includes all standard categories.

9. How do I reduce my monthly expenses?

– Audit subscriptions — cancel anything unused

– Switch to store-brand groceries (saves 15–25% on food costs)

– Refinance high-interest debt — use our Refinance Calculator to model potential savings

– Lower car insurance by comparing quotes annually

– Cut dining to 10% or less of food budget

10. What is net cash flow in a budget?

Net cash flow = Total monthly income minus total monthly expenses. A positive net cash flow means you have money left over to save or invest. A negative net cash flow means you are spending more than you earn and need immediate budget adjustments.

11. How often should I update my budget?

Update your budget every month — at minimum. Any major life change (new job, salary increase, new loan, new dependent) warrants an immediate budget revision. Monthly review takes 10–15 minutes and is the single habit most correlated with financial stability, according to the CFPB’s budgeting research.

📋 Disclaimer: This budget calculator and all supporting content are provided for educational and informational purposes only. Results are estimates based on the figures you enter and do not constitute professional financial advice. Individual financial situations vary. Please consult a qualified Certified Financial Planner (CFP) or CPA for personalized financial guidance tailored to your specific circumstances. FinanceAuthorityHub.com is not liable for financial decisions made based on calculator outputs.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.