Income Tax Calculator 2026 – Free and Instant Results

Income Tax Calculator

Build your own tax brackets (progressive) or use a flat tax rate, then get a transparent bracket-by-bracket breakdown, marginal vs effective tax rates, net income by pay period, and “what-if” extra income impact. Progressive systems tax different ranges (“brackets”) at different rates, so your marginal rate can differ from your effective rate. [web:360][web:359]

Inputs

“Taxable income” is typically what remains after deductions; gross income is before deductions. [web:369]

Results

Taxable income

—

Gross: —

Pre-tax: — • Deductions: —

Total tax

—

Core tax: —

Credits: — • After credits: —

Local tax: —

Net income (simple)

—

Pay periods: —

Per-period gross: —

Per-period tax: — • Net: —

Rates

Marginal rate: —

Effective (tax ÷ gross): —

Effective (tax ÷ taxable): —

Effective rate is an average, often computed as total tax divided by taxable income (×100). [web:362]

What-if (extra income)

Extra income: — • Added tax: — • Added net: —

Implied tax on extra income: — • New marginal rate: —

Bracket-by-bracket breakdown

| Bracket | From | To | Rate | Taxed amount | Tax |

|---|

Step-by-step math

Results appear after you click “Calculate.”

In This Article

What Is an Income Tax Calculator and How Does It Work?

An income tax calculator is a free tool that estimates how much federal income tax you owe — or the refund you may receive — based on your income, filing status, and deductions. Enter your numbers above and get instant results, including your taxable income, effective tax rate, and net take-home pay.

In 2026, the federal income tax system uses seven progressive tax brackets ranging from 10% to 37%. The One Big Beautiful Bill (OBBB), signed into law on July 4, 2025, permanently changed several key thresholds. For tax year 2026, the standard deduction rises to $16,100 for single filers and $32,200 for married couples filing jointly.

What this calculator gives you — instantly:

- Your taxable income after deductions

- Total federal tax owed, bracket by bracket

- Your effective vs. marginal tax rate

- Net take-home pay per month, biweekly, or weekly

- A “What-If” scenario: what happens if you earn more

Use it alongside our Salary Calculator and Budget Calculator for a complete picture of your finances.

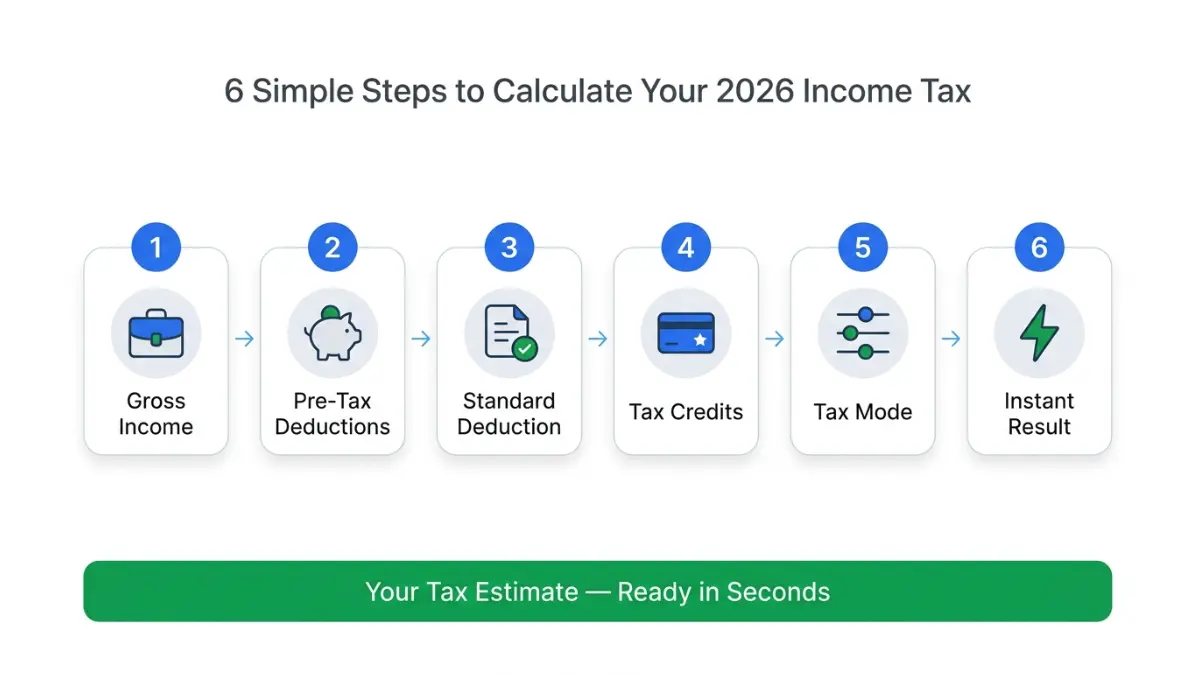

How to Use Our Free Income Tax Calculator — Step by Step

Most online calculators give you one number and leave you confused. Ours shows you every step of the math. Here’s how to use it:

Step 1 — Enter your annual gross income This is your total earnings before any deductions. Include wages, freelance income, tips, and investment income.

Step 2 — Add pre-tax deductions Enter contributions to your 401(k), HSA, or other pre-tax accounts. These reduce your taxable income dollar-for-dollar.

Step 3 — Enter your deductions Choose the standard deduction (recommended for ~90% of taxpayers) or your total itemized deductions if higher. See the 2026 amounts in Section 3 below.

Step 4 — Add tax credits Credits like the Child Tax Credit directly reduce your tax bill — not just your taxable income. Enter the total credits you qualify for.

Step 5 — Choose progressive brackets or flat rate The calculator supports both. For U.S. federal taxes, use progressive brackets. The default brackets are pre-loaded with 2026 IRS rates.

Step 6 — Run the “What-If” scenario Enter a raise amount (e.g., $5,000 bonus) to see exactly how much more tax you’d pay and what your new marginal rate would be.

Pro Tip: Use the Download CSV button to save your full estimate — useful when planning with your CPA or running year-end tax projections.

Understanding your adjusted gross income (AGI) is critical before running the calculator. Read our in-depth guide on AGI and Form 1040 to ensure you’re entering the right number.

2026 Federal Income Tax Brackets (Updated for One Big Beautiful Bill)

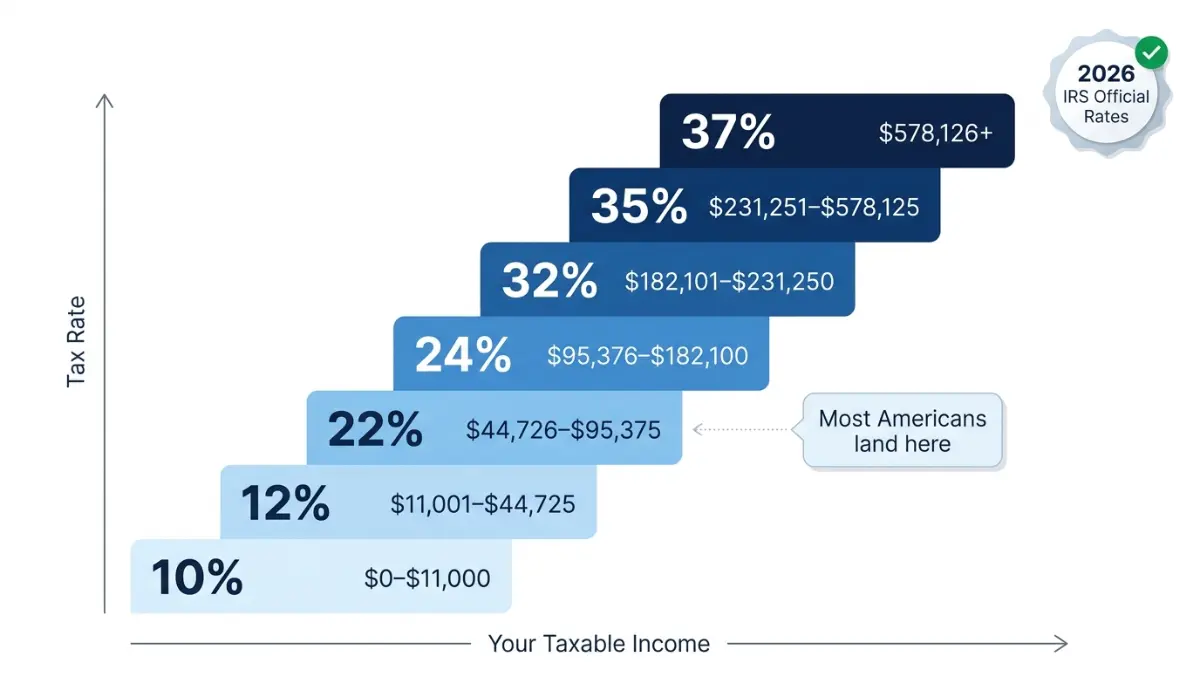

The federal income tax has seven tax rates in 2026: 10%, 12%, 22%, 24%, 32%, 35%, and 37%. The top marginal income tax rate of 37% hits taxpayers with taxable income above $640,600 for single filers and above $768,600 for married couples filing jointly.

2026 Tax Brackets — Single Filers

| Taxable Income | Tax Rate |

|---|---|

| $0 – $12,400 | 10% |

| $12,401 – $50,400 | 12% |

| $50,401 – $100,800 | 22% |

| $100,801 – $201,775 | 24% |

| $201,776 – $256,225 | 32% |

| $256,226 – $640,600 | 35% |

| Over $640,600 | 37% |

2026 Tax Brackets — Married Filing Jointly

| Taxable Income | Tax Rate |

|---|---|

| $0 – $24,800 | 10% |

| $24,801 – $100,800 | 12% |

| $100,801 – $201,600 | 22% |

| $201,601 – $403,550 | 24% |

| $403,551 – $512,450 | 32% |

| $512,451 – $768,700 | 35% |

| Over $768,700 | 37% |

Source: IRS Revenue Procedure 2025-32

2026 Standard Deduction — All Filing Statuses

| Filing Status | 2026 Standard Deduction |

|---|---|

| Single | $16,100 |

| Married Filing Jointly | $32,200 |

| Head of Household | $24,150 |

| Married Filing Separately | $16,100 |

🔥 Key OBBB Changes for 2026 — What Competitors Missed

Several new tax deductions were introduced for the 2026 filing season. Seniors 65 and older may be eligible to claim an additional $6,000 deduction. Tipped workers may deduct up to $25,000 for qualified tips. Individuals may be eligible to deduct up to $12,500 ($25,000 for joint filers) for qualified overtime.

- SALT cap raised to $40,400 (was $10,000 since 2018)

- Senior bonus deduction of up to $6,000 for ages 65+ (phases out above $75,000 income)

- Overtime deduction — up to $12,500 single / $25,000 joint (new Schedule 1-A)

- Tip income deduction — up to $25,000 for service workers

- TCJA tax rates made permanent — no sunset cliff for brackets

What This Means For You: If you’re 65+, a tipped worker, or receive overtime pay, your 2026 taxable income could be significantly lower than last year. Run the calculator above with these new deductions applied.

For a deeper look at all 2026 bracket changes, see our complete guide: 2026 Tax Brackets: Deductions & Calculator.

Marginal Rate vs. Effective Rate — The Difference That Matters

| Rate Type | Definition | Example ($75,000 Single) |

|---|---|---|

| Marginal Rate | Rate on your last dollar earned | 22% |

| Effective Rate | Total tax ÷ gross income | ~15.8% |

Most people think they “pay 22% in taxes.” They don’t. The effective rate is always lower because only the income in each bracket is taxed at that bracket’s rate — not all income.

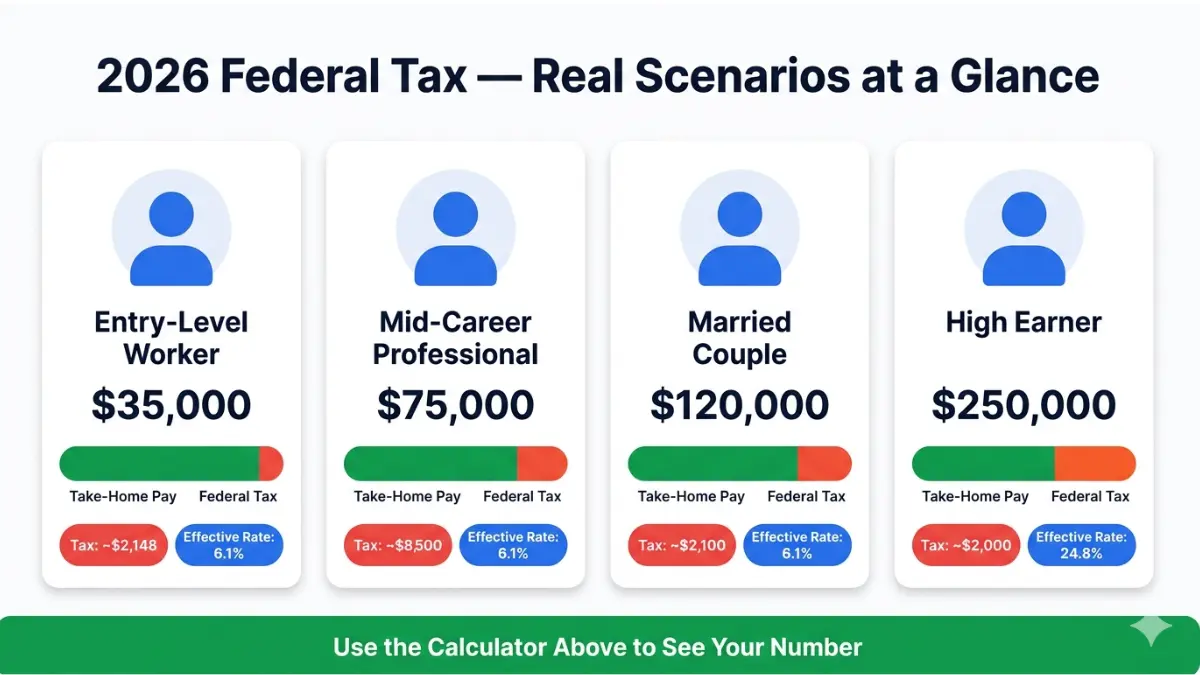

How Much Income Tax Will I Pay in 2026? Real Examples

These are based on IRS 2026 brackets with standard deduction applied, no additional credits.

| Profile | Gross Income | Filing Status | Taxable Income | Est. Federal Tax | Effective Rate |

|---|---|---|---|---|---|

| Entry-Level Worker | $35,000 | Single | $18,900 | ~$2,148 | 6.1% |

| Mid-Career Professional | $75,000 | Single | $58,900 | ~$8,074 | 10.8% |

| Dual-Income Couple | $120,000 | Married Filing Jointly | $87,800 | ~$10,220 | 8.5% |

| High Earner | $250,000 | Single | $233,900 | ~$52,843 | 21.1% |

Real Example — Step-by-Step Math for a $60,000 Single Filer:

- Gross income: $60,000

- Standard deduction: $16,100

- Taxable income: $43,900

- 10% on first $12,400 = $1,240

- 12% on $12,401–$43,900 ($31,500) = $3,780

- Total federal tax: $5,020

- Effective rate: 8.4%

This is exactly how the income tax calculator above computes your result — step by step, fully transparent.

What-If: You Get a $10,000 Raise

If our $60,000 single filer gets a $10,000 raise to $70,000:

- New taxable income: $53,900

- Additional tax on the extra $10,000: ~$2,200 (at 22% marginal rate)

- Net gain from the raise: ~$7,800 — not $10,000

This is why the “What-If” feature in our calculator is critical for salary negotiations and job change planning.

Expert Insight: “Most Americans dramatically overestimate their effective tax rate. The progressive system means a $10,000 raise rarely pushes your entire income into a new bracket — only the amount above the threshold is taxed higher.” — Laura M. Bennett, CFP®, financeauthorityhub.com Expert Panel

After knowing your take-home pay, use our Home Affordability Calculator to see how much house you can actually afford, or our Retirement Calculator to project long-term savings on your net income.

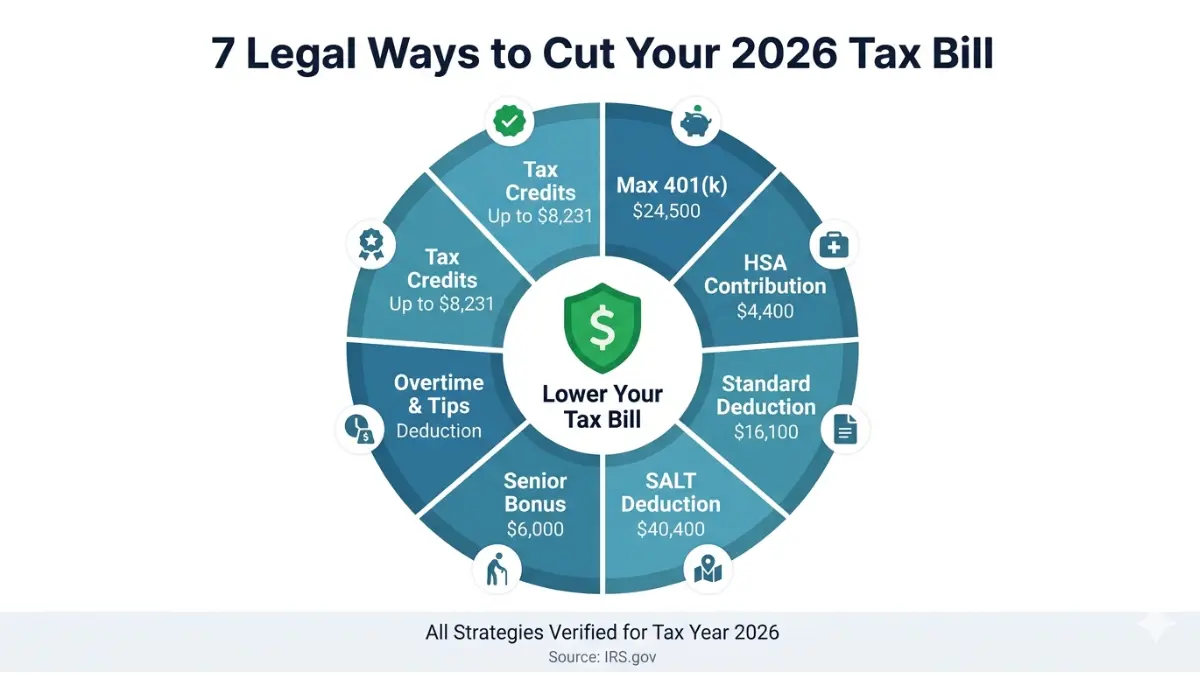

7 Legal Ways to Lower Your Income Tax Bill in 2026

These are not loopholes. These are legal, IRS-approved strategies every American taxpayer should use.

1. Maximize Your 401(k) Contributions

The annual contribution limit for employees in 401(k) plans has increased to $24,500 for 2026, up from $23,500 for 2025. Catch-up contributions for those aged 50 and older are $8,000 in 2026.

- Under 50: Contribute up to $24,500 — reduces your taxable income by up to $24,500

- Age 50–59 or 64+: Contribute up to $32,500

- Age 60–63 (SECURE 2.0 Super Catch-Up): Contribute up to $35,750

Use our 401(k) Calculator to model exactly how much tax you save at different contribution levels.

2. Open or Max Out Your HSA

The annual amount individuals can contribute to health savings accounts will increase to $4,400 for individual coverage and $8,750 for family coverage in 2026.

HSAs offer a triple tax advantage: contributions are tax-deductible, growth is tax-free, and qualified withdrawals are tax-free. No other account matches this. Read our full analysis on HSA vs. 401(k) to understand which to prioritize.

3. Claim the Full 2026 Standard Deduction

About 90% of Americans take the standard deduction because it’s larger than their itemized deductions. In 2026, the amounts are: $16,100 single, $32,200 MFJ, $24,150 HOH. Always verify whether itemizing saves you more — especially if you have high mortgage interest or state taxes.

4. Use the New SALT Deduction (Up to $40,400)

The SALT cap jumped from $10,000 to $40,400 in 2026. If you live in a high-tax state like California, New York, or New Jersey and pay significant state income or property taxes, this could push itemizing ahead of the standard deduction. Pair this with our Property Tax Calculator to calculate your deductible amount.

5. Claim the Senior Bonus Deduction (Age 65+)

Eligible taxpayers can claim the new deduction whether they take the standard deduction or itemize on their return, but it’s offered only through the 2028 tax year when this OBBB provision expires. The deduction is up to $6,000, phasing out at $75,000 income (single) or $150,000 (joint).

6. Deduct Overtime and Tip Income (New for 2026)

This is the single biggest new deduction most Americans don’t know about. Service workers and hourly employees with overtime can deduct up to $12,500 in overtime pay (single) and up to $25,000 in qualified tips. Visit the IRS New Deductions page for full eligibility rules.

7. Maximize Tax Credits

Credits reduce your actual tax bill — not just your taxable income. Key 2026 credits include:

| Credit | Max Amount | Who Qualifies |

|---|---|---|

| Child Tax Credit | $2,200 per child | Parents with qualifying children |

| Earned Income Tax Credit | Up to $8,231 (3+ children) | Low-to-moderate income earners |

| Child & Dependent Care | $3,000 (1 child), $6,000 (2+) | Working parents paying for childcare |

| American Opportunity Credit | $2,500/year | First 4 years of college |

Planning to build your tax savings into a bigger future? Use our Roth IRA Calculator or Investment Calculator to see how after-tax dollars compound over time. And if your tax refund is earmarked for debt payoff, our Debt Consolidation Calculator shows the fastest path to becoming debt-free.

For a complete walkthrough of your 1040, see our guide: 1040 Tax Form 2026 — Avoid 7 Costly Mistakes. And if you want to know how your tax refund could be maximized this year, read Tax Refund 2026 — Claim a $1,000 Increase.

Full 2026 bracket rates and strategies are also detailed by the Tax Foundation’s 2026 Tax Brackets guide, one of the most authoritative non-government sources on federal tax policy.

Income Tax Calculator — Frequently Asked Questions

1. What is an income tax calculator?

An income tax calculator is a free online tool that estimates your federal tax liability based on your income, filing status, deductions, and credits. It shows your taxable income, total tax owed, effective rate, and net take-home pay — without filing a return.

2. How accurate is an online income tax calculator?

Very accurate for estimates — typically within 1–3% of your actual tax bill when inputs are correct. The calculator uses official IRS 2026 bracket rates. It doesn’t account for every unique tax situation, so always verify with a CPA for final filing.

3. What is the difference between taxable income and gross income?

Gross income is everything you earn before any deductions. Taxable income is what remains after subtracting pre-tax deductions (like 401(k) contributions) and your standard or itemized deduction. Federal tax brackets are applied to your taxable income, not your gross income.

4. What is the difference between marginal and effective tax rate?

Your marginal rate is the rate applied to your last dollar of income — the top bracket you fall into. Your effective rate is your total tax divided by your total income. The effective rate is always lower and is a more accurate measure of your actual tax burden.

5. What are the 2026 federal income tax brackets?

There are seven brackets: 10%, 12%, 22%, 24%, 32%, 35%, and 37%. For single filers, the 37% rate begins at $640,600. See the full bracket table in Section 3 above.

6. How much federal tax is taken out of my paycheck?

It depends on your W-4 withholding elections. Use the calculator above to estimate your annual tax, then divide by your pay periods (e.g., 24 for semi-monthly). For precise paycheck estimates, use our Salary Calculator.

7. Can I use this calculator for state income tax?

Yes — the calculator includes an optional local/state tax field. Enter your state’s tax rate as a percentage of taxable income. Rates vary widely, from 0% in states like Texas and Florida to over 13% in California.

8. What are the biggest income tax changes for 2026?

The OBBB introduced new deductions for overtime pay, tip income, and a $6,000 senior bonus deduction for ages 65+. The SALT cap rose to $40,400. Standard deductions increased to $16,100 (single) and $32,200 (MFJ). All TCJA bracket rates were made permanent.

9. How does the One Big Beautiful Bill affect my 2026 taxes?

Most taxpayers will pay less in 2026 under the OBBB than they would have under expiring TCJA rules. The law permanently extends existing low rates, adds new deductions for workers and seniors, and raises several key thresholds for inflation. Full details are at IRS.gov.

10. What is the standard deduction for 2026?

The 2026 standard deduction is $16,100 for single filers, $32,200 for married filing jointly, and $24,150 for head of household. Taxpayers 65+ receive an additional $1,900 (single) or $1,500 per qualifying spouse (MFJ), plus the new $6,000 senior bonus deduction (income-limited).

11. When is the 2026 tax return filing deadline?

Tax year 2026 returns (income earned January 1 – December 31, 2026) are due April 15, 2027. You can request a 6-month extension, but any taxes owed are still due by April 15. Start planning now with our eFile 2026 guide.

Disclaimer: This income tax calculator and article are provided for educational and informational purposes only and do not constitute tax, legal, or financial advice. Tax laws are subject to change. All calculations are estimates based on IRS-published 2026 rates and may not reflect your complete individual tax situation. Always consult a licensed CPA, enrolled agent, or qualified tax professional before making financial decisions. financeauthorityhub.com is not affiliated with the IRS or any government agency.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.