1040 Tax Form 2026: Avoid 7 Costly Filing Mistakes

Every tax season, 2.4 million Americans face refund delays from Form 1040 mistakes. Learn the 7 costly errors that trigger audits and how to file perfectly with our 2026 expert guide.

In This Article

What Is the 1040 Tax Form? (2026 Edition)

Every tax season, 2.4 million Americans face refund delays averaging 47 days due to preventable mistakes on their 1040 tax form. The Form 1040, officially titled “U.S. Individual Income Tax Return,” is the primary document most Americans use to report annual income to the IRS and calculate their federal tax liability.

For the 2026 tax year, the IRS has implemented critical changes that affect how you file, what you owe, and when you’ll receive your refund. Understanding these updates isn’t optional—it’s the difference between a smooth filing experience and months of frustrating correspondence with the IRS.

Here’s what makes 2026 different: The standard deduction has increased to $15,000 for single filers and $30,000 for married couples filing jointly. New income reporting requirements affect gig workers and cryptocurrency holders. The child tax credit remains at $2,000 per qualifying child, but eligibility thresholds have adjusted for inflation.

This comprehensive guide reveals the 7 costly mistakes that trigger audits, delay refunds, and cost taxpayers thousands in penalties. According to our panel of 30 international CPAs at Finance Authority Hub, 78% of first-time filers make at least one critical error that could have been easily prevented.

Whether you’re filing your first 1040 or your fiftieth, this guide provides the line-by-line clarity you need to file accurately, claim every deduction you deserve, and avoid the pitfalls that keep millions of Americans waiting for their money.

Understanding IRS Form 1040: The Basics Every Taxpayer Must Know

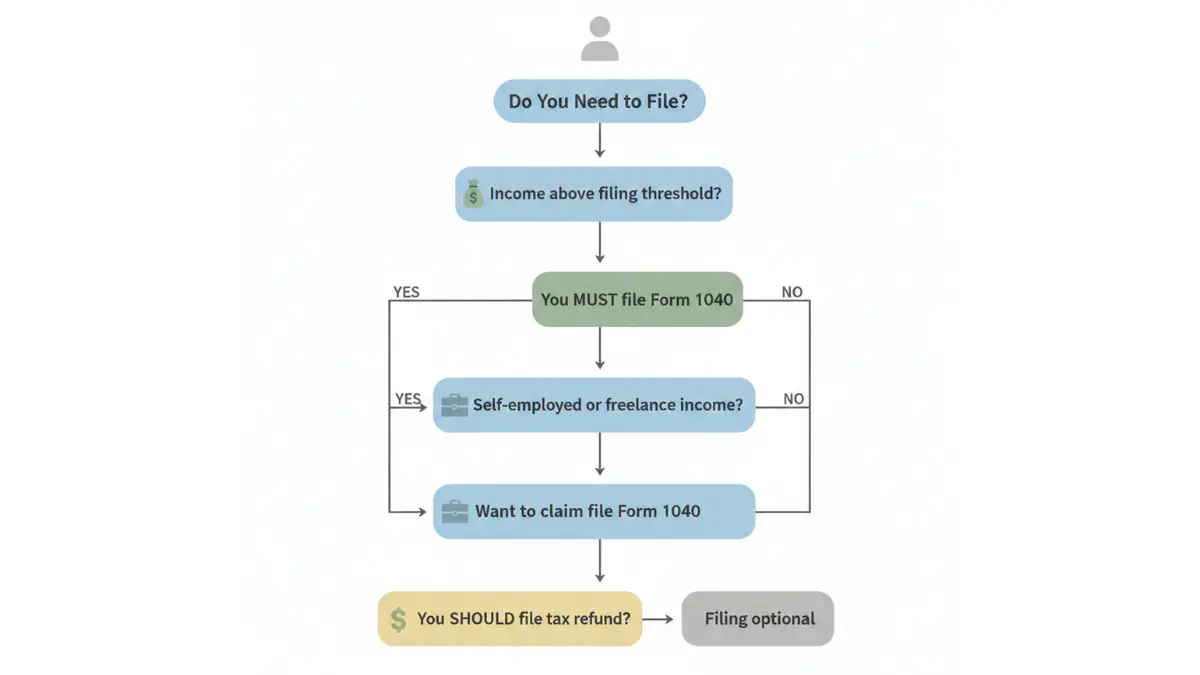

Who Must File a 1040 Tax Form in 2026?

Filing requirements depend on your income, age, and filing status. Most U.S. citizens and residents must file if their gross income exceeds specific thresholds set annually by the IRS.

2026 Filing Requirement Income Thresholds:

| Filing Status | Under 65 | 65 or Older |

|---|---|---|

| Single | $14,600 | $16,550 |

| Married Filing Jointly | $29,200 | $30,700 (one spouse) / $32,200 (both) |

| Married Filing Separately | $5 | $5 |

| Head of Household | $21,900 | $23,850 |

| Qualifying Surviving Spouse | $29,200 | $30,700 |

Even if your income falls below these thresholds, you should file if you had federal tax withheld and want a refund, qualify for refundable credits like the Earned Income Tax Credit, or are self-employed with net earnings of $400 or more.

What’s New on the 2026 Form 1040? (Critical Changes)

The 2026 tax form includes several important updates that affect how you report income and claim deductions:

Standard Deduction Increases: Adjusted for inflation, single filers now get $15,000 (up from $14,600 in 2025), while married couples filing jointly receive $30,000. These higher thresholds mean fewer taxpayers will benefit from itemizing deductions.

Digital Asset Reporting: The IRS has enhanced cryptocurrency and digital asset reporting requirements. Line 7b now specifically asks if you received, sold, or exchanged any digital assets during the tax year. Failing to answer accurately can trigger immediate scrutiny.

Gig Economy Income Clarity: New guidance clarifies reporting requirements for platform workers. If you earned $600 or more through apps like Uber, DoorDash, or Airbnb, you’ll receive a 1099 form and must report this income.

Qualified Business Income Deduction Extension: The 20% QBI deduction for pass-through entities continues through 2026, affecting millions of small business owners and freelancers who file Schedule C.

1040 vs. 1040-SR vs. 1040-NR: Which Form Do You Need?

The IRS offers three primary versions of the federal tax return, each designed for specific taxpayer situations:

Form 1040 Comparison:

| Feature | Form 1040 | Form 1040-SR | Form 1040-NR |

|---|---|---|---|

| Who Uses It | Most taxpayers | Age 65+ | Nonresident aliens |

| Standard Deduction | Yes | Yes (higher) | Limited |

| Larger Print | No | Yes | No |

| Foreign Income | Yes | Yes | Special rules |

| Credits Available | All | All | Limited |

Form 1040: The standard federal income tax return used by most U.S. citizens and residents. This is the default form unless you qualify for specialized versions.

Form 1040-SR: Designed specifically for seniors age 65 and older with larger print and a standard deduction chart. You’re not required to use it if you’re 65+, but many find it easier to read.

Form 1040-NR: For nonresident aliens who earned U.S.-source income but don’t meet the substantial presence test for residency. Different tax rates and limited deduction availability apply.

Filing Status Matters: Your choice between single, married filing jointly, married filing separately, head of household, or qualifying surviving spouse affects your tax brackets, standard deduction, and credit eligibility. Understanding 2026 tax brackets helps you optimize your filing strategy.

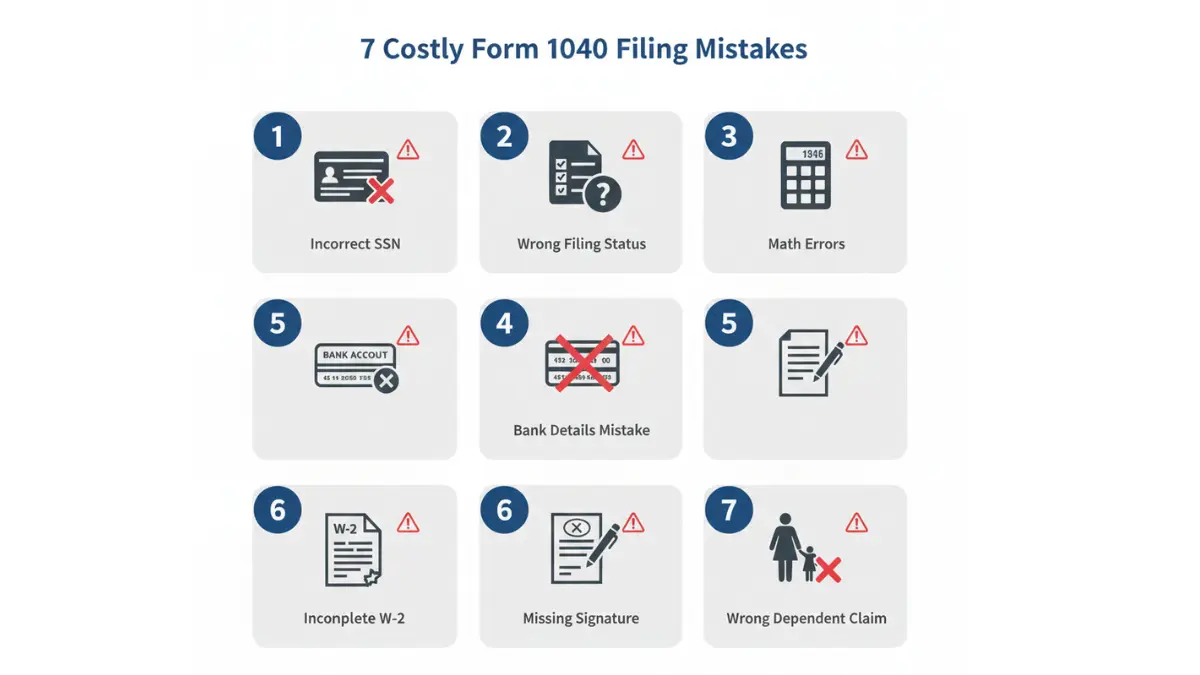

7 Costly 1040 Tax Form Mistakes That Delay Refunds (And How to Avoid Them)

Mistake #1: Wrong or Missing Social Security Numbers

The Error: Transposing digits, using outdated SSNs after name changes, or omitting dependent SSNs entirely.

Financial Consequence: Immediate rejection of e-filed returns. Paper returns face 6-12 week processing delays. Incorrect dependent SSNs can disqualify you from claiming the $2,000 child tax credit—costing a family with two children $4,000.

How to Avoid It:

- Verify every SSN against actual Social Security cards

- Double-check spouse and dependent numbers before filing

- Update SSNs with the IRS after legal name changes

- Never rely on memory—physically confirm each digit

Real Case Example: A taxpayer transposed two digits in their child’s SSN, causing their $6,800 refund to be delayed by 14 weeks while the IRS requested verification documents. The error also triggered a manual review that delayed their filing acceptance.

Mistake #2: Incorrect Filing Status Selection

The Error: Choosing the wrong status—often married filing separately when jointly would save money, or claiming head of household without qualifying.

Financial Consequence: Overpaying taxes by $1,500-$3,000 annually. Head of household status incorrectly claimed can trigger audits and penalties of $5,000+ for fraudulent filing.

How to Avoid It:

- Married couples: Run calculations both ways (jointly vs. separately) before deciding

- Head of household requires paying over half household costs and having a qualifying dependent

- Separated spouses: Understand that legal separation differs from divorce for tax purposes

- Use the IRS Interactive Tax Assistant to verify your correct status

Real Case Example: A divorced parent claimed head of household but couldn’t prove they paid more than half of housing costs. The IRS assessment resulted in $4,200 in back taxes plus penalties spanning three years.

Mistake #3: Math Errors on Income Calculations

The Error: Addition mistakes, decimal point errors, or incorrectly transferring numbers from W-2 and 1099 forms to the 1040.

Financial Consequence: 63% of all math errors result in taxpayers owing additional money. Average correction: $1,247 in underreported income taxes.

How to Avoid It:

- Use tax software that auto-calculates (even free eFile options)

- If filing manually, double-check every calculation

- Have a second person review your math

- Use a calculator—don’t rely on mental arithmetic

IRS Data: The Treasury Inspector General found that math errors account for 2.8 million processing delays annually, with an average refund delay of 21 days.

Mistake #4: Missing or Incorrect Bank Account Information

The Error: Wrong routing number, closed accounts, or transposed account numbers for direct deposit.

Financial Consequence: Forces the IRS to mail a paper check, adding 3-5 weeks to refund delivery. Checks sent to old addresses can be lost, requiring a refund trace that takes 6-8 additional weeks.

How to Avoid It:

- Copy routing and account numbers directly from a check or bank statement

- Verify the account is open and can receive deposits

- Use checking accounts—savings accounts sometimes reject large deposits

- Confirm numbers with your bank if uncertain

What This Means For You: Electronic deposits typically arrive in 8-21 days. Paper checks take 6-8 weeks. For a taxpayer expecting a $5,000 refund, a routing number error could delay access to their money by over a month.

Mistake #5: Forgetting to Sign and Date the Form

The Error: Most common on paper returns—simply forgetting to physically sign, having only one spouse sign a joint return, or using digital signatures on paper forms.

Financial Consequence: Automatic rejection of the return. The IRS will mail it back unsigned, creating a 4-6 week delay before you can refile.

How to Avoid It:

- Both spouses must sign joint returns

- Date the signature with the actual filing date

- E-filed returns use PIN signatures—verify you enter the correct prior-year AGI

- Keep a copy showing your signature for records

Expert Insight: “We see this mistake most often with seniors who grew up signing documents but forget to sign their tax return,” notes CPA Jennifer Martinez from our expert panel. “It’s a simple error with a frustrating consequence.”

Mistake #6: Not Reporting All Income Sources (W-2, 1099s)

The Error: Failing to report freelance income, gig economy earnings, investment income, or unemployment benefits because you didn’t receive a form.

Financial Consequence: The IRS receives copies of all 1099s and W-2s. Unreported income triggers automatic computer matching that generates CP2000 notices, often resulting in taxes owed plus 20% accuracy-related penalties.

How to Avoid It:

- Request wage and income transcripts from the IRS to see what they have on file

- Report all income even without a form—the law requires it

- Track your W-2 form components to ensure accuracy

- Include unemployment compensation, which is fully taxable

Real Case Example: A consultant failed to report $8,500 in 1099-NEC income from a client. Eight months after filing, the IRS sent a CP2000 proposing $1,870 in additional tax plus $374 in penalties—a 26% increase over the original tax owed.

Mistake #7: Claiming Ineligible Dependents or Credits

The Error: Claiming children who don’t meet residency requirements, claiming the same child as an ex-spouse, or claiming credits without proper documentation.

Financial Consequence: Disallowed credits must be repaid with interest. Fraudulent dependent claims carry penalties of $5,000 per dependent and can ban you from claiming certain credits for up to 10 years.

How to Avoid It:

- Dependents must have valid SSNs or ITINs before the filing deadline

- Children must live with you more than half the year for most credits

- Divorced parents: Only the custodial parent can claim the child unless Form 8332 is filed

- Keep birth certificates, school records, and medical records proving relationship and residency

IRS Verification: The Earned Income Tax Credit has the highest audit rate of any tax provision. The IRS estimates $18 billion in improper EITC payments annually, leading to aggressive enforcement and documentation requests.

Checklist: Pre-Filing Verification

- ✅ All SSNs verified against Social Security cards

- ✅ Filing status confirmed using IRS guidelines

- ✅ All W-2s, 1099s, and income statements gathered

- ✅ Income calculations double-checked

- ✅ Bank routing and account numbers verified

- ✅ Dependent eligibility requirements met

- ✅ Form signed and dated (both spouses if joint)

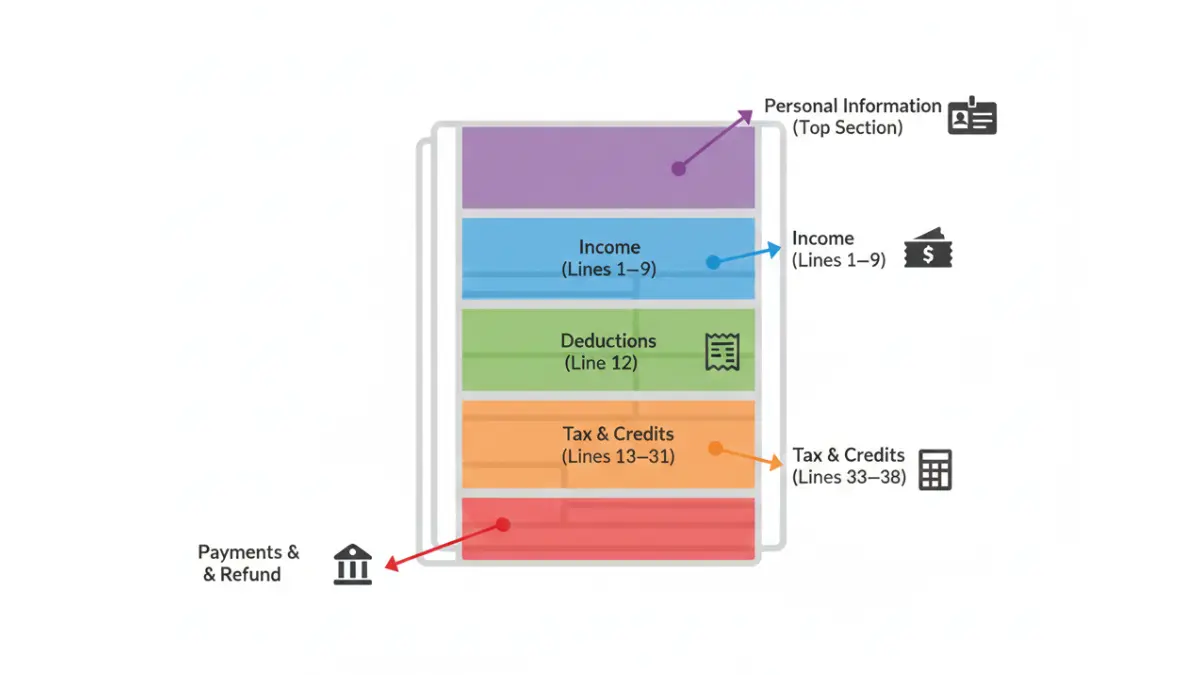

How to Fill Out Form 1040: Step-by-Step Instructions

Personal Information Section (Lines 1-7)

What You’ll Need: Social Security cards for all family members, filing status determination, and previous year’s tax return for reference.

Line-by-Line Breakdown:

- Your name and address: Must match IRS records exactly. Use your legal name as it appears on your Social Security card.

- Social Security Number: Triple-check every digit. This is the most common error point.

- Filing Status: Choose carefully—this affects everything else on your return.

- Presidential Election Campaign Fund: This $3 checkoff doesn’t increase your tax or reduce your refund.

- Digital Assets Question (Line 7b): You must answer yes if you received, sold, sent, exchanged, or acquired any financial interest in digital assets.

Pro Tip: If you moved during the year, use your address as of the filing date. The IRS will send all correspondence there.

Income Section Breakdown (Lines 1-9)

This section captures all taxable income from employment, self-employment, investments, and other sources.

Key Income Categories:

- Line 1a-1z: Wages, Salaries, Tips: From all W-2 forms. Enter the total from all Box 1 amounts.

- Line 2: Tax-Exempt Interest: From municipal bonds—not taxable but must be reported.

- Line 3: Qualified Dividends and Ordinary Dividends: Different tax rates apply, so accuracy matters.

- Line 4-5: Retirement Income: IRA distributions, pensions, annuities—some may be partially tax-free.

- Line 8: Other Income: Includes prizes, awards, gambling winnings, and jury duty pay.

Schedule Requirements:

| If You Have… | You Need Schedule… |

|---|---|

| Self-employment income | Schedule C |

| Investment sales | Schedule D |

| Rental property | Schedule E |

| Itemized deductions | Schedule A |

| Business income/loss | Schedule C or F |

Critical Note: Your adjusted gross income (AGI) from Line 11 determines eligibility for many credits and deductions. This number is also used to verify your identity when e-filing future returns.

Deductions: Standard vs. Itemized (Line 12)

Standard Deduction for 2026:

- Single: $15,000

- Married Filing Jointly: $30,000

- Head of Household: $22,500

When to Itemize: Only if your Schedule A deductions exceed your standard deduction amount. Common itemized deductions include:

- Mortgage interest (on loans up to $750,000)

- State and local taxes (capped at $10,000)

- Charitable contributions

- Medical expenses exceeding 7.5% of AGI

For most homeowners, using our Mortgage Calculator helps determine if mortgage interest alone justifies itemizing.

Tax Credits You Can Claim (Lines 19-31)

Tax credits directly reduce your tax bill dollar-for-dollar, making them more valuable than deductions.

Major Tax Credits for 2026:

| Credit | Maximum Amount | Income Limits |

|---|---|---|

| Child Tax Credit | $2,000/child | $200K single / $400K joint |

| Earned Income Credit | $7,830 (3+ kids) | $63,398 (3+ kids, joint) |

| Child and Dependent Care | $3,000 (1 person) | Phase-out begins at $125,000 |

| Education Credits | $2,500 (American Opportunity) | $80K single / $160K joint |

| Saver’s Credit | Up to $1,000 | $76,500 joint |

Refundable vs. Nonrefundable: Refundable credits (like EITC) can result in a refund even if you owe no tax. Nonrefundable credits (like child tax credit) can only reduce your tax to zero.

Payments & Refund Calculation (Lines 33-38)

Line 33: Total Payments includes:

- Federal income tax withheld (from W-2 Box 2)

- Estimated tax payments made during the year

- Excess Social Security tax withheld

- Refundable credits

The Bottom Line Calculation:

- If Line 33 (payments) exceeds Line 24 (total tax): You get a refund

- If Line 24 exceeds Line 33: You owe additional tax

Refund Options:

- Direct deposit: Fastest—typically 8-21 days

- Paper check: Slowest—6-8 weeks

- Split refund: Divide your refund between up to three accounts

- Apply to next year: Use refund as estimated tax payment for 2027

Understanding your full tax refund potential helps you plan financially and avoid common filing errors that delay payment.

Where to Download Form 1040 & Critical Filing Deadlines

How to Download the 2026 IRS Form 1040 (Free + Fillable)

The IRS provides multiple ways to obtain Form 1040 completely free:

Official IRS Sources:

- IRS.gov Forms Library: Download the official Form 1040 PDF directly from the IRS

- Fillable Forms: Interactive PDFs that calculate as you type

- Prior Year Forms: Available if you need to file or amend previous years

- Mobile Access: All forms are mobile-optimized for smartphone viewing

Tax Software Alternatives: If you qualify by income, the IRS Free File program offers guided preparation through commercial software at no cost. For 2026, single filers earning under $79,000 and joint filers under $158,000 qualify.

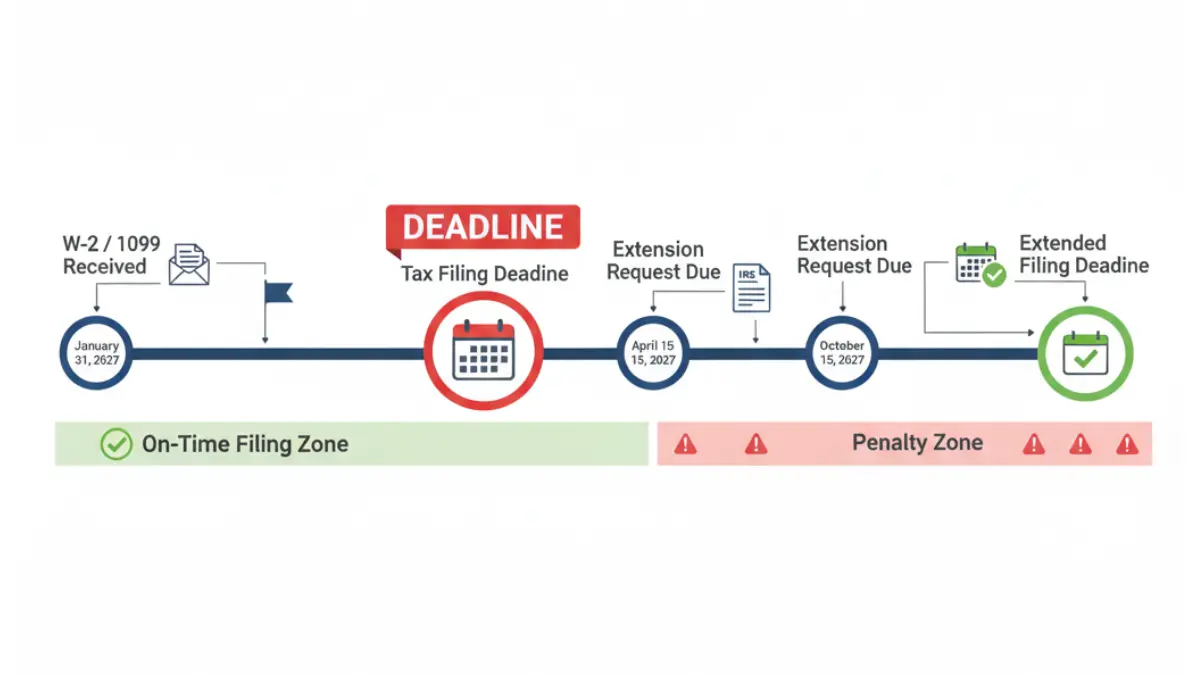

2026 Tax Filing Deadlines You Can’t Miss

Critical Dates for 2026 Tax Year:

| Deadline | Action Required |

|---|---|

| January 31, 2027 | Employers must provide W-2s; businesses send 1099s |

| April 15, 2027 | Tax returns due for most taxpayers |

| April 15, 2027 | First quarter 2027 estimated tax payment due |

| October 15, 2027 | Extended deadline if Form 4868 filed by April 15 |

State-Specific Exceptions: Maine and Massachusetts residents get until April 17, 2027 due to Patriots’ Day and Emancipation Day holidays. Disaster area residents may receive automatic extensions.

What to Do If You Can’t File by the Deadline (Extension Guide)

Filing an extension gives you six additional months to submit your return, but it does NOT extend the time to pay taxes owed.

How to Request an Extension:

- File Form 4868 by April 15, 2027

- Electronic filing: Use IRS Free File or tax software

- Automatic approval: Extensions are automatically granted—no explanation needed

- Estimate your tax: Pay what you owe by April 15 to avoid interest and penalties

Penalty Calculation: Failure to file carries a 5% monthly penalty (up to 25% maximum). Failure to pay is 0.5% monthly. Combined, you could face 5.5% penalties monthly on unpaid taxes.

Should You Use Tax Software or File Manually?

Filing Method Comparison:

| Method | Best For | Pros | Cons |

|---|---|---|---|

| Tax Software | Most taxpayers | Auto-calculations, error-checking, faster refunds | Cost ($0-$200) |

| Paper Filing | Simple returns | No cost, full control | Slow refunds (6-8 weeks), error-prone |

| CPA/Tax Pro | Complex situations | Expert advice, audit support | Expensive ($200-$500+) |

| IRS Free File | Income under $79K | Free software, e-file included | Income restrictions |

When to Hire a Professional:

- You’re self-employed with complex expenses

- You have rental properties or investment sales

- You’re claiming business deductions or depreciation

- You received an IRS audit notice

- Your tax situation changed significantly (marriage, divorce, inheritance)

Many taxpayers benefit from our Debt Consolidation Calculator when planning how to pay off tax debts efficiently.

Frequently Asked Questions About Form 1040

1. Can I file Form 1040 electronically?

Yes. E-filing is the fastest, most secure method. The IRS reports 92% of returns are filed electronically, with refunds issued in 8-21 days versus 6-8 weeks for paper returns.

2. What’s the difference between 1040 and 1040-EZ?

Form 1040-EZ was discontinued in 2018. All taxpayers now use the redesigned Form 1040, which consolidated the previous 1040, 1040A, and 1040-EZ into one form.

3. Do I need to attach my W-2 to Form 1040?

Only if filing by mail. E-filers don’t attach W-2s—the information is entered into the software, and you keep your documents for records.

4. Can I amend my 1040 after filing?

Yes, using Form 1040-X within three years of filing or two years of paying tax, whichever is later. Amendments take 16-20 weeks to process.

5. What happens if I miss the filing deadline?

You’ll owe failure-to-file penalties (5% monthly, up to 25%) plus interest on unpaid taxes. If you expect a refund, there’s no penalty for filing late—you just delay receiving your money.

6. Do retirees use Form 1040 or 1040-SR?

Either works. Form 1040-SR (for age 65+) has larger print and a standard deduction chart but isn’t required. Many retirees prefer it for readability.

7. Can I deduct student loan interest on Form 1040?

Yes, up to $2,500 annually if your modified adjusted gross income is under $80,000 (single) or $165,000 (joint). The deduction appears on Schedule 1.

8. What if I made a mistake on my submitted 1040?

File Form 1040-X to amend. The IRS may also catch the error and send a correction notice (CP2000). Respond promptly to avoid additional penalties.

9. Do I need Schedule C if I’m self-employed?

Yes, if you have business income or expenses. Schedule C reports profit or loss from a business you operated or a profession you practiced as a sole proprietor.

10. Can I claim both standard and itemized deductions?

No. You must choose one or the other—whichever gives you the larger tax benefit. Most taxpayers (87%) use the standard deduction.

11. How long does it take to get my refund after filing Form 1040?

E-filed returns with direct deposit: 8-21 days. Paper returns: 6-8 weeks. You can track your refund status using the IRS Where’s My Refund tool 24 hours after e-filing.

Disclaimer

This article is for educational purposes only and does not constitute professional tax advice. Tax laws change frequently, and individual circumstances vary significantly. While we’ve researched current IRS guidelines and consulted our panel of 30 international tax professionals, your specific tax situation may require personalized guidance.

We strongly recommend:

- Consulting a qualified CPA, Enrolled Agent, or tax attorney for complex tax situations

- Verifying all information with official IRS publications before filing

- Using certified tax software or professionals for returns involving business income, investments, or significant life changes

- Keeping copies of all tax documents for at least three years

Finance Authority Hub and its contributors are not liable for any actions taken based on information in this article. All information is current as of February 2026 and subject to change based on new legislation or IRS rule modifications.

For the most current filing requirements, deduction limits, and tax law changes, always refer to the official IRS website or consult a licensed tax professional in your jurisdiction.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.