1099 Form: Types, Deadlines + $340 Penalty (2026)

Master 1099 filing for 2026: Understand all 22 form types, critical Feb 2 deadline, tiered penalties ($70-$340), and e-filing requirements. Expert guide to avoid IRS fines.

In This Article

A 1099 form is an IRS information return that reports income you received outside of traditional employment—including freelance payments, interest, dividends, and rental income. For 2026, the critical filing deadline is February 2 (shifted from January 31 due to the weekend), and missing it triggers penalties starting at $70 per form, escalating to $340 after August 1. With 57 million gig workers in the U.S. and new threshold changes taking effect, understanding your 1099 obligations can save you thousands in penalties and ensure IRS compliance.

Whether you’re a freelancer managing multiple income streams or a small business owner paying contractors, this guide covers all 22 types of 1099 forms, the new 2026 penalty structure, and filing requirements updated for tax year 2025.

What Is a 1099 Form and Who Needs One?

The 1099 tax form is a series of information returns used to report various types of income paid to individuals and businesses throughout the tax year. Unlike a W-2 form which reports employee wages, the 1099 form tracks payments made to independent contractors, interest from bank accounts, investment dividends, and other non-wage income sources.

The IRS requires payers to issue a 1099 form when they’ve paid $600 or more to a non-employee during the calendar year. This threshold applies to most 1099 variants, though some forms like the 1099-INT (interest income) have lower thresholds of just $10.

1099 vs W-2: Understanding the Difference

The fundamental distinction between these tax documents determines your filing obligations and tax responsibilities.

| Feature | 1099 Form | W-2 Form | 1040 Form |

|---|---|---|---|

| Used For | Non-employee income | Employee wages | Personal tax return |

| Tax Withholding | No automatic withholding | Automatic withholding | N/A |

| Self-Employment Tax | 15.3% (you pay both halves) | 7.65% (employer pays half) | Reports all income |

| Who Issues | Clients, banks, brokerages | Your employer | Filed by taxpayer |

| Deadline (2026) | Feb 2 – Mar 31 (varies) | Jan 31 | April 15 |

For freelancers and contractors, understanding this distinction is crucial. When you receive a 1099 form instead of a W-2, you’re responsible for the full 15.3% self-employment tax—both the employee and employer portions. If you’re navigating these tax obligations while managing debt, our debt consolidation calculator can help you balance tax payments with debt repayment strategies.

New 2026 Reporting Threshold Changes

The One Big Beautiful Bill Act (OBBBA) significantly impacts 1099 reporting requirements starting in 2026. For tax year 2025 (filed in 2026), the reporting threshold remains at $600. However, beginning January 1, 2027 (for tax year 2026 filings in 2027), the threshold increases to $2,000 for most 1099 forms.

Timeline breakdown:

- 2025 tax year (filed 2026): $600 threshold

- 2026 tax year (filed 2027): $2,000 threshold

- 2027 and beyond: Adjusted annually for inflation

This change affects Form 1099-NEC (nonemployee compensation) and Form 1099-MISC (miscellaneous income) primarily. The IRS has confirmed these adjusted thresholds will reduce administrative burden on small businesses while maintaining tax compliance.

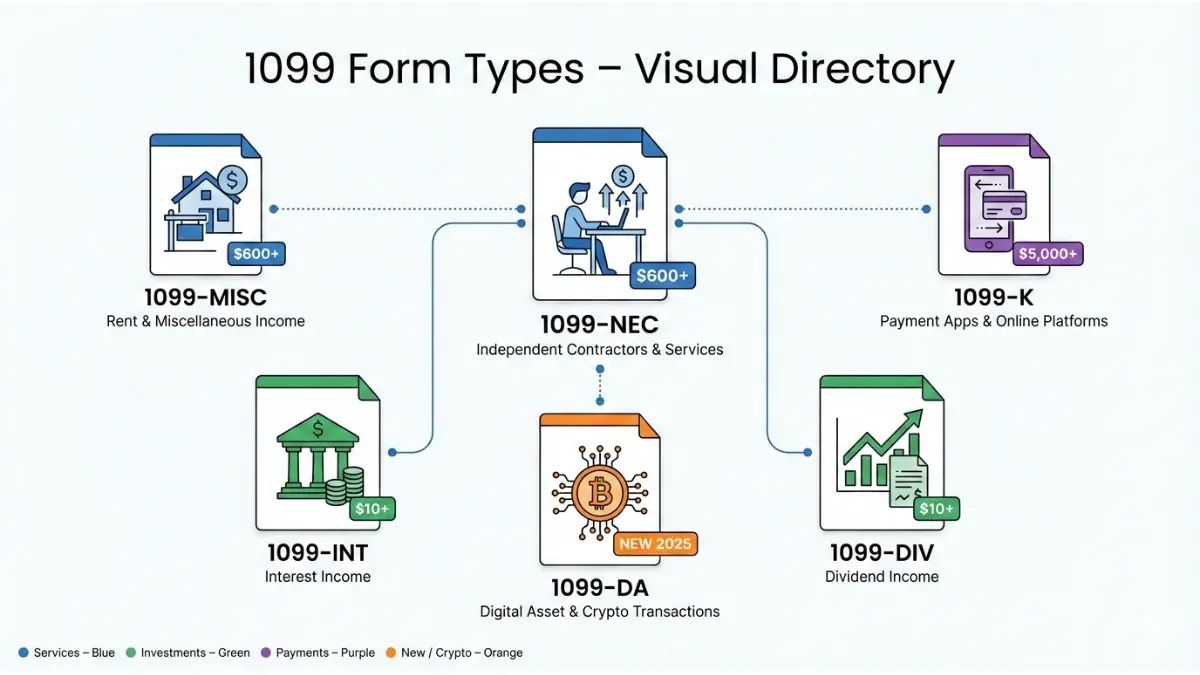

Complete Guide to All 22 Types of 1099 Forms (2026)

The IRS maintains 22 different versions of the 1099 form, each designed to report specific types of income. Understanding which form applies to your situation prevents filing errors and potential penalties.

Most Common 1099 Forms for Freelancers & Contractors

Form 1099-NEC: Nonemployee Compensation

This is the primary form for reporting payments to independent contractors, freelancers, and self-employed individuals. If you paid someone $600 or more for services performed in your trade or business, you must file Form 1099-NEC.

Key details for 2026:

- Threshold: $600 or more

- Deadline: February 2, 2026 (both IRS filing and recipient copy)

- No extension available (unlike other 1099 forms)

- New Box 3: Now tracks excess golden parachute payments for executives

The 1099-NEC was reintroduced in 2020 after being retired in 1982. The IRS separated nonemployee compensation from the 1099-MISC to establish a stricter filing deadline, helping combat tax fraud and improve income verification.

Form 1099-MISC: Miscellaneous Income

After the 1099-NEC was reintroduced, the 1099-MISC now reports payments including:

- Rent ($600 or more)

- Prizes and awards ($600 or more)

- Royalties ($10 or more)

- Medical and health care payments ($600 or more)

- Crop insurance proceeds ($600 or more)

- Gross proceeds to attorneys ($600 or more)

The filing deadline differs from 1099-NEC:

- Recipients: February 2, 2026

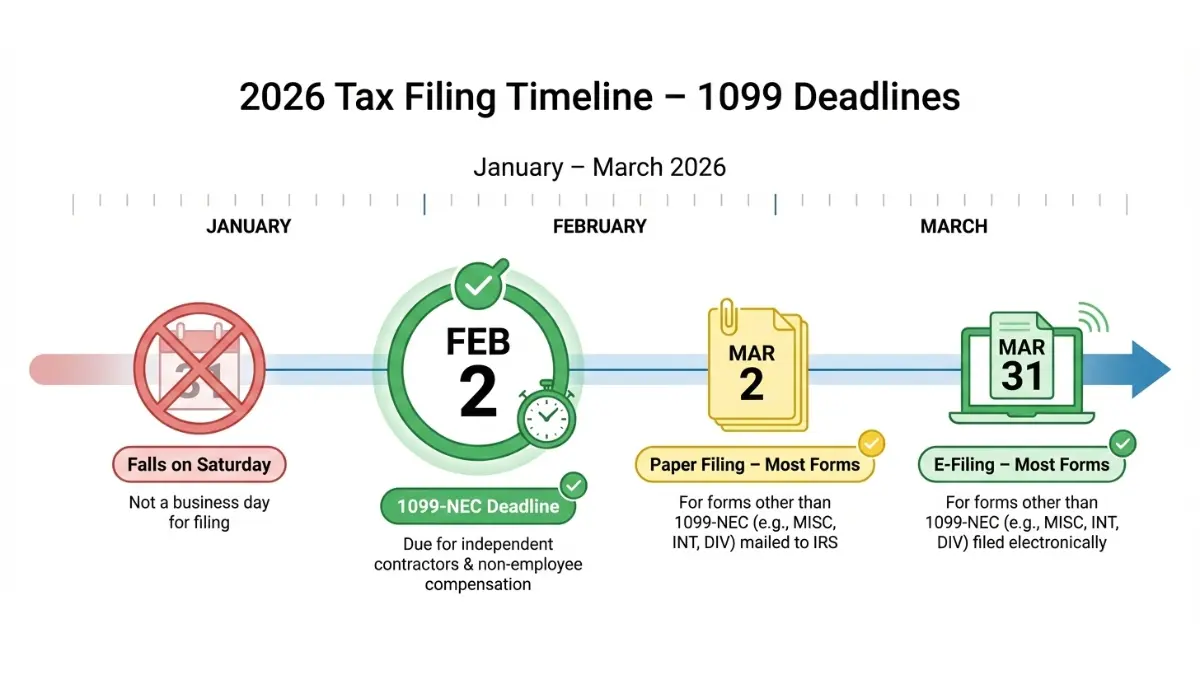

- IRS (paper): March 2, 2026 (February 28 falls on Saturday)

- IRS (e-file): March 31, 2026

Special rule: If boxes 8 or 10 contain amounts, recipient copies must be furnished by February 17, 2026, due to the additional time needed to aggregate data from multiple sources.

Form 1099-K: Payment Card and Third-Party Network Transactions

This form has undergone significant changes affecting gig economy workers and online sellers. Payment settlement entities like PayPal, Venmo, Cash App, and Stripe use Form 1099-K to report payment card transactions and third-party network payments.

2026 threshold timeline:

- For 2025 tax year: $2,500 in gross payments (transition relief)

- For 2026 tax year: $2,000 in gross payments

- For 2027 and beyond: $600 in gross payments

According to IRS Notice 2024-85, this phased implementation gives taxpayers and payment processors time to adapt. If you’re an Uber driver, DoorDash delivery person, or Etsy seller receiving payments through third-party platforms, understanding when you’ll receive a 1099-K is essential for tax planning.

Form 1099-INT: Interest Income

Banks, credit unions, and other financial institutions issue Form 1099-INT when you’ve earned $10 or more in interest during the tax year. This includes:

- Interest from savings accounts

- Interest from checking accounts

- U.S. Savings Bond interest

- Treasury obligations

- Bond premiums

Even if you don’t receive a physical form (because interest was under $10), you must still report all interest income on your tax return.

Form 1099-DIV: Dividends and Distributions

Investment firms and brokerages file Form 1099-DIV to report:

- Ordinary dividends

- Qualified dividends (taxed at lower capital gains rates)

- Capital gain distributions

- Nontaxable distributions

- Foreign tax paid

Understanding the difference between ordinary and qualified dividends is crucial—qualified dividends receive preferential tax treatment, with rates of 0%, 15%, or 20% depending on your income tax bracket.

Specialized 1099 Forms You Should Know

NEW: Form 1099-DA (Digital Assets)

Starting with the 2025 tax year (filed in 2026), the IRS introduced Form 1099-DA to report digital asset transactions. This includes cryptocurrency sales, NFT transfers, and other blockchain-based asset transactions.

Brokers must report:

- Sale proceeds from digital asset transactions

- Cost basis information

- Gain or loss calculations

- Date of acquisition and sale

De minimis exceptions:

- $600 threshold for payment processors handling digital assets

- $10,000 threshold for qualifying stablecoin sales

- $600 threshold for specified NFT sales

This new form addresses the growing crypto economy and ensures proper tax reporting as digital asset adoption increases.

Form 1099-B: Proceeds from Broker Transactions

Brokers and barter exchanges use this form to report:

- Stock sales

- Bond transactions

- Commodity futures

- Barter exchange transactions

- Regulated futures contracts

The 1099-B provides essential information for calculating capital gains and losses on Schedule D of your tax return.

Form 1099-R: Distributions from Retirement Accounts

Retirement plan administrators issue Form 1099-R for distributions from:

- IRAs (Traditional and Roth)

- 401(k) plans

- Pension plans

- Annuities

- Profit-sharing plans

The form indicates whether distributions are taxable, subject to early withdrawal penalties, or qualify for special tax treatment. If you’re strategizing retirement withdrawals, our guide on 401(k) vs IRA can help optimize your tax situation.

Form 1099-S: Proceeds from Real Estate Transactions

Real estate closing agents file Form 1099-S when reporting gross proceeds from real estate sales. The form reports the full sale price, not your taxable gain.

You’ll subtract your cost basis (original purchase price plus improvements) to calculate actual gain. For primary residence sales, you may exclude up to $250,000 ($500,000 for married couples) if you meet the ownership and use tests.

Quick Reference: All 22 Form Types

| Form | Reports | Threshold | 2026 Deadline |

|---|---|---|---|

| 1099-A | Acquisition/abandonment of secured property | Any amount | Mar 31 (e-file) |

| 1099-B | Broker/barter transactions | Any amount | Feb 17 (recipient) |

| 1099-C | Cancellation of debt | $600+ | Mar 31 (e-file) |

| 1099-CAP | Corporate control changes | Any amount | Mar 31 (e-file) |

| 1099-DA | Digital assets (NEW 2025) | Varies | Mar 31 (e-file) |

| 1099-DIV | Dividends/distributions | $10+ | Mar 31 (e-file) |

| 1099-G | Government payments | $10+ | Mar 31 (e-file) |

| 1099-H | Health coverage tax credit | Any amount | Mar 31 (e-file) |

| 1099-INT | Interest income | $10+ | Mar 31 (e-file) |

| 1099-K | Payment card transactions | $2,500+ (2025) | Mar 31 (e-file) |

| 1099-LS | Life insurance contract sales | Any amount | Mar 31 (e-file) |

| 1099-LTC | Long-term care benefits | Any amount | Mar 31 (e-file) |

| 1099-MISC | Miscellaneous income | $600+ | Mar 31 (e-file) |

| 1099-NEC | Nonemployee compensation | $600+ | Feb 2 (no extension) |

| 1099-OID | Original issue discount | $10+ | Mar 31 (e-file) |

| 1099-PATR | Taxable distributions from cooperatives | $10+ | Mar 31 (e-file) |

| 1099-Q | Qualified education programs | Any amount | Mar 31 (e-file) |

| 1099-QA | ABLE account distributions | Any amount | Mar 31 (e-file) |

| 1099-R | Retirement account distributions | $10+ | Mar 31 (e-file) |

| 1099-S | Real estate transaction proceeds | Any amount | Feb 17 (recipient) |

| 1099-SA | HSA/MSA distributions | Any amount | Mar 31 (e-file) |

| 1099-SB | Seller’s investment in life insurance | Any amount | Mar 31 (e-file) |

Critical 1099 Deadlines for 2026 Tax Season

Missing a 1099 deadline triggers automatic penalties that escalate based on how late you file. Understanding the specific dates and requirements for each form type is essential for compliance.

February 2, 2026: The Most Important Date

The standard January 31 deadline falls on Saturday in 2026, automatically extending the due date to the next business day: Monday, February 2, 2026.

This date is critical for:

- Form 1099-NEC: Must be filed with the IRS AND furnished to recipients by Feb 2

- Most other 1099 forms: Recipient copies must be provided by Feb 2

- Form W-2: Employee copies and SSA filing both due Feb 2

The 1099-NEC deadline is particularly strict. Unlike other 1099 forms that allow later IRS filing via e-file, the 1099-NEC must be submitted to the IRS by February 2 whether you file electronically or on paper. This alignment ensures the IRS can verify nonemployee income early in the filing season, reducing refund fraud.

Complete 2026 Filing Calendar

Different 1099 forms have different deadlines depending on the filing method and form type. Here’s the comprehensive breakdown:

| Form Type | Recipient Copy | IRS Paper Filing | IRS E-Filing |

|---|---|---|---|

| 1099-NEC | Feb 2, 2026 | Feb 2, 2026 | Feb 2, 2026 |

| 1099-MISC | Feb 2, 2026 | Mar 2, 2026 | Mar 31, 2026 |

| 1099-INT | Feb 2, 2026 | Mar 2, 2026 | Mar 31, 2026 |

| 1099-DIV | Feb 2, 2026 | Mar 2, 2026 | Mar 31, 2026 |

| 1099-K | Feb 2, 2026 | Mar 2, 2026 | Mar 31, 2026 |

| 1099-R | Feb 2, 2026 | Mar 2, 2026 | Mar 31, 2026 |

| 1099-B | Feb 17, 2026 | Mar 2, 2026 | Mar 31, 2026 |

| 1099-S | Feb 17, 2026 | Mar 2, 2026 | Mar 31, 2026 |

| 1099-MISC (Box 8/10) | Feb 17, 2026 | Mar 2, 2026 | Mar 31, 2026 |

Note: February 28, 2026 falls on Saturday, moving the paper filing deadline to Monday, March 2, 2026.

E-Filing Requirements: The 10-Form Rule

The IRS lowered the electronic filing threshold from 250 forms to just 10 forms starting with returns filed in 2024. This applies to the aggregate total of ALL information returns you file, including:

- All 1099 variants (NEC, MISC, INT, DIV, etc.)

- W-2 forms

- 1098 forms

- Any other information returns

Example: If you file 6 Forms 1099-NEC and 5 Forms W-2, you’ve exceeded the 10-form threshold and MUST e-file everything.

Failing to e-file when required triggers an additional penalty of up to $340 per form, applied only to forms exceeding the 10-form threshold. The IRS Information Returns Intake System (IRIS) provides free e-filing for businesses of all sizes.

Extension Requests Using Form 8809

You can request a 30-day automatic extension for most 1099 forms by filing Form 8809 before the original due date.

Critical limitations:

- Extensions do NOT apply to Form 1099-NEC (must file by Feb 2 regardless)

- Extensions only cover IRS filing, not recipient copies

- Recipient copies must still be provided by the original deadline

- Additional 30-day extensions may be granted for extraordinary circumstances

To qualify for extension relief, you must demonstrate reasonable cause, such as:

- Natural disasters affecting your business location

- Unavoidable delays in receiving necessary information

- System failures beyond your control

File Form 8809 electronically through the IRIS system or mail it to the IRS address specified in the instructions. Even with an extension, aim to file as early as possible—the sooner you correct errors or submit late forms, the lower your penalties.

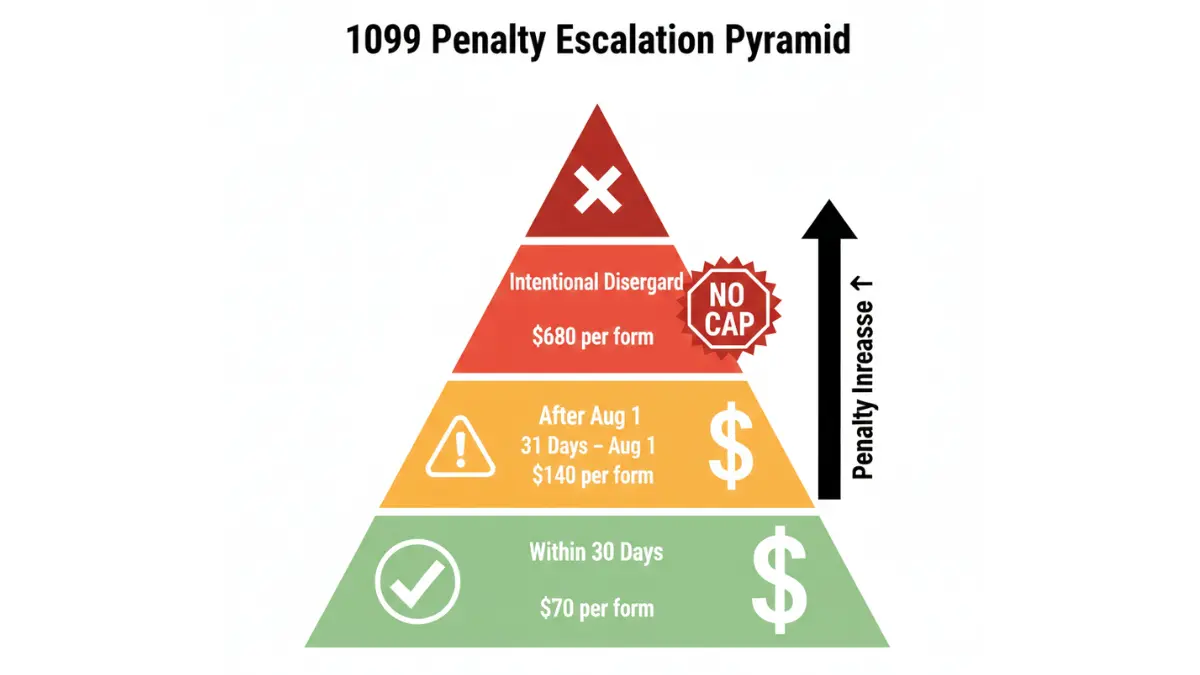

$340 Penalty: Complete 2026 Penalty Breakdown

The IRS imposes escalating penalties for late or incorrect 1099 filings. Understanding this tiered structure helps you prioritize compliance and minimize financial exposure.

Tiered Penalty System Explained

Penalties are assessed per form, not per batch. The amount depends on how quickly you correct the issue after the deadline.

2026 Penalty Structure (for tax year 2025 filings):

| Filing Timeframe | Penalty Per Form | Maximum Cap (Small Business) | Maximum Cap (Large Business) |

|---|---|---|---|

| Within 30 days | $70 | $299,000 | $1,177,500 |

| 31 days to August 1 | $140 | $598,500 | $2,355,000 |

| After August 1 or never filed | $340 | $1,366,000 | $3,532,500 |

| Intentional disregard | $680 | NO CAP | NO CAP |

Small businesses are defined as those with average annual gross receipts of $5 million or less over the most recent three tax years. All others are classified as large businesses.

These penalty amounts are adjusted annually for inflation per Revenue Procedure 2025-32, meaning they increase slightly each year.

Real-World Penalty Calculations

Example 1: Small consulting firm files 35 Forms 1099-NEC 45 days late

Filing timeframe: 31 days to August 1

Penalty per form: $140

Total forms: 35

Penalty calculation: 35 × $140 = $4,900

This mid-tier penalty applies because the firm filed after the 30-day window but before August 1. Had they filed within 30 days, the penalty would have been only $2,450 (35 × $70).

Example 2: E-commerce seller intentionally ignores 8 Forms 1099-K

The IRS determines the seller deliberately failed to file required forms despite multiple notices.

Penalty per form: $680

Total forms: 8

Penalty calculation: 8 × $680 = $5,440

Additional exposure: No maximum cap applies to intentional disregard penalties, and the IRS may pursue criminal charges for willful tax evasion.

Example 3: Large corporation files 200 Forms 1099-MISC 5 months late

Filing timeframe: After August 1

Penalty per form: $340

Total forms: 200

Penalty calculation: 200 × $340 = $68,000

Maximum cap (large business): $3,532,500

Final penalty: $68,000

While the calculated penalty ($68,000) falls well below the cap, it demonstrates how quickly costs escalate with high-volume filings.

Most Common Filing Mistakes That Trigger Penalties

1. Wrong or Missing Taxpayer Identification Number (TIN)

Submitting forms with incorrect TINs is the most frequent error. When a TIN doesn’t match IRS records, you’ll receive a CP2100 or CP2100A notice requesting correction.

Consequences:

- 24% backup withholding requirement on future payments

- Failure to furnish correct payee statement penalties

- Potential “B” notices requiring TIN verification

Solution: Use the IRS TIN Matching service to verify TINs before filing. Collect Form W-9 from all payees before making payments, ensuring you have accurate information from the start.

2. Using the Wrong 1099 Form Type

The distinction between 1099-NEC and 1099-MISC confuses many filers. Reporting nonemployee compensation on a 1099-MISC instead of 1099-NEC violates IRS requirements.

Common misclassifications:

- Service payments (should be 1099-NEC) reported on 1099-MISC

- Credit card payments (should be 1099-K) reported on 1099-NEC

- Rent payments (should be 1099-MISC) reported on 1099-NEC

Always review IRS instructions for each form type before filing.

3. Missing State Filing Requirements

Many states require separate 1099 filings beyond federal obligations. Failing to file state forms triggers state-level penalties in addition to federal penalties.

States with 1099 filing requirements include:

- California (requires Forms 1099-NEC, 1099-MISC, 1099-K)

- Massachusetts (requires Form 1099-NEC)

- Vermont (requires Forms 1099-NEC, 1099-MISC)

- Connecticut (requires Forms 1099-NEC, 1099-MISC)

Check your state’s Department of Revenue website for specific filing requirements and deadlines.

4. Paper Filing When E-Filing Is Required

As mentioned earlier, filing 10 or more information returns requires electronic submission. Paper filing when you should e-file results in an additional penalty.

Penalty: Up to $340 per form, applied only to forms exceeding the 10-form threshold

If you file 15 forms on paper when required to e-file, you’d face penalties on 5 forms (the number exceeding 10), not all 15 forms.

How to Correct 1099 Errors

Discovering mistakes after filing doesn’t mean you’re automatically subject to maximum penalties. The IRS rewards quick corrections with reduced penalty tiers.

Void vs. Corrected Returns:

- Void: Use when the entire form was filed in error (wrong recipient, duplicate filing)

- Corrected: Use when information on the form is incorrect (wrong amount, wrong TIN)

Correction process:

- Prepare a new 1099 with correct information

- Check the “CORRECTED” box (or mark as void if appropriate)

- File with the IRS using the same method as original (paper or electronic)

- Furnish a corrected copy to the recipient

- Submit Form 1096 if filing paper corrections

File corrections as soon as you discover errors. Corrections submitted within 30 days of the original deadline receive the lowest penalty tier ($70 per form).

Penalty Waiver and Reasonable Cause

The IRS may waive or reduce penalties if you can demonstrate reasonable cause for the failure and show you acted in good faith.

Qualifying reasonable cause scenarios:

- Natural disasters (fires, floods, hurricanes)

- Serious illness or death of person responsible for filing

- Unavoidable absence of the person responsible

- Destruction of records due to circumstances beyond your control

- Inability to obtain necessary information despite timely requests

How to request abatement:

When you receive Notice 972CG (proposed penalty assessment), respond within 45 days (60 days for foreign filers) with:

- Detailed explanation of reasonable cause

- Supporting documentation (medical records, disaster declarations, etc.)

- Evidence of good-faith efforts to comply

- Corrected forms (if applicable)

The IRS evaluates each request individually. Meeting the reasonable cause standard requires more than ordinary business care—you must show extraordinary circumstances prevented timely filing despite your best efforts.

For complex penalty situations or high-dollar assessments, consider consulting a tax professional. If you’re managing penalties alongside other debt obligations, exploring debt consolidation strategies may provide relief.

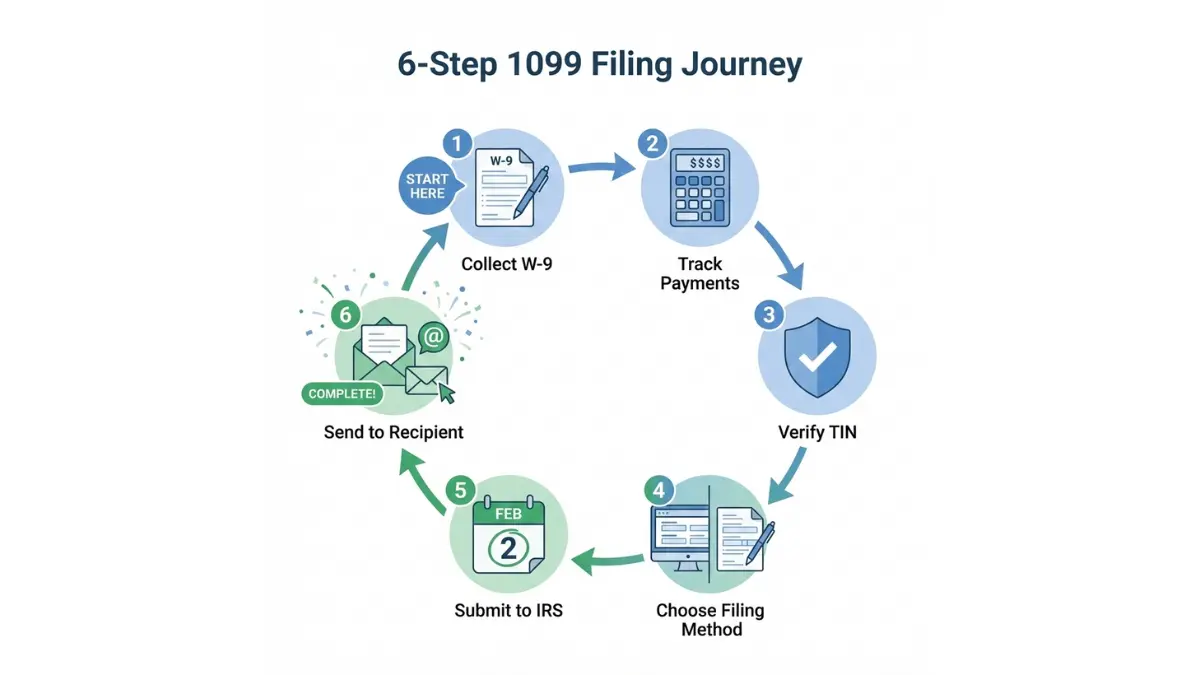

How to File Your 1099 Forms: Step-by-Step Guide

Filing 1099 forms correctly requires systematic preparation throughout the year, not just scrambling at year-end. Follow this comprehensive process to ensure compliance.

Step 1: Collect Form W-9 from All Payees (Before Making First Payment)

Form W-9 (Request for Taxpayer Identification Number and Certification) provides essential information for 1099 preparation:

- Legal name

- Business name (if different)

- Taxpayer Identification Number (TIN) or Social Security Number (SSN)

- Address

- Business entity classification

Best practices:

- Obtain W-9 before issuing first payment

- Store securely (contains sensitive tax information)

- Update annually or when payee information changes

- Use electronic W-9 collection systems for efficiency

Failing to obtain a valid W-9 subjects you to 24% backup withholding on all payments. Withhold this amount and remit to the IRS quarterly using Form 945.

Step 2: Track Payments Throughout the Year

Don’t wait until December to calculate annual totals. Implement systems to track payments in real-time:

Accounting software options:

- QuickBooks (automatically flags 1099-eligible payments)

- FreshBooks (tracks contractor payments separately)

- Wave (free option with 1099 tracking)

Manual tracking considerations:

- Maintain separate accounts payable records for 1099 vendors

- Flag payments exceeding $600 threshold

- Note payment method (credit card payments don’t require 1099-NEC)

- Document payment purposes to determine correct form type

Remember: The $600 threshold is cumulative for the calendar year, not per transaction. If you pay a contractor $200 in March, $200 in July, and $250 in November, you’ve exceeded the threshold and must file a 1099.

Step 3: Verify TIN Accuracy (Before Filing Deadline)

Use the IRS TIN Matching service to validate name-TIN combinations before submitting forms. This free service, available through IRS e-Services, prevents the most common filing error.

TIN Matching process:

- Register for IRS e-Services account

- Upload payee information (name and TIN)

- Receive real-time verification results

- Correct mismatches before filing

If TIN Matching reveals discrepancies, contact the payee immediately to obtain correct information. Don’t guess or estimate—using incorrect TINs triggers penalties even if amounts are correct.

Step 4: Choose Your Filing Method

Option A: E-Filing (Required for 10+ Forms)

The IRS offers two free e-filing platforms:

- IRIS (Information Returns Intake System): Free for all filers, regardless of volume

- FIRE (Filing Information Returns Electronically): Legacy system being phased out

IRIS advantages:

- User-friendly interface

- Accepts PDF uploads

- Immediate acknowledgment

- Supports corrections and voids

- No registration fees or per-form charges

Option B: Paper Filing (Under 10 Forms)

If you file fewer than 10 information returns total, you may file on paper:

- Order official red-ink scannable forms from the IRS (don’t print from website)

- Complete using typewriter or clearly printed hand-written entries

- Submit Form 1096 as transmittal cover sheet

- Mail to IRS processing center for your state (addresses in Form 1096 instructions)

Paper filing takes longer to process and increases error risk. Even if you qualify, e-filing offers faster processing, immediate confirmation, and reduced error rates.

Step 5: Submit by February 2 Deadline

For 1099-NEC forms, both IRS filing AND recipient copies are due February 2, 2026. For other forms, recipient copies are due February 2, but IRS filing deadlines vary (March 2 for paper, March 31 for e-file).

Submission checklist:

- ✓ All required boxes completed

- ✓ Dollar amounts match your records

- ✓ TINs verified through TIN Matching

- ✓ Payer information (your business) is accurate

- ✓ Form 1096 included (if paper filing)

- ✓ Correct IRS processing center address (if mailing)

Step 6: Furnish Recipient Copies

Providing copies to recipients is a separate requirement from filing with the IRS. You must furnish Copy B to each recipient by the deadline.

Delivery methods:

- Mail: Postmark by deadline date

- Hand delivery: Obtain signature as proof

- Electronic delivery: Requires recipient consent

For electronic delivery, recipients must affirmatively consent (opt-in) and have ability to access, print, and retain forms. Many e-filing platforms offer automated recipient delivery services.

What This Means For You: Action Steps

If you’re a business owner who pays contractors:

- Start collecting W-9 forms now for any vendors you’ve paid in 2025

- Review your accounting records to identify all payments exceeding $600

- Set up IRIS account at IRS.gov if you haven’t already

- Mark February 2, 2026 on your calendar with alerts starting January 15

If you’re a freelancer or contractor:

- Expect to receive 1099 forms by early February

- Don’t wait for forms to file your tax return—report all income regardless

- Make quarterly estimated tax payments to avoid underpayment penalties

- Consider using budgeting strategies to set aside 25-30% for taxes

If you’re tracking both business income and personal finances: Our mortgage calculator can help you determine affordability when 1099 income varies month-to-month. For comprehensive tax planning guidance, review our 2026 tax brackets guide.

Frequently Asked Questions

Q1: What is a 1099 form used for?

A 1099 form reports various types of income paid to individuals and businesses outside of traditional employment. The IRS requires these information returns for payments including freelance work ($600+), interest income ($10+), dividends ($10+), rental income ($600+), and numerous other payment types. Payers must file 1099s with the IRS and furnish copies to recipients, enabling the IRS to verify reported income on tax returns.

Q2: Do I need to file a 1099 for credit card payments to contractors?

No. When you pay contractors via credit card or payment apps like PayPal, the payment processor is responsible for issuing Form 1099-K, not you. This prevents double reporting. However, if you pay the same contractor $400 by credit card and $300 by check, you must file a 1099-NEC for the $300 check payment (exceeds $600 threshold cumulatively). Track payment methods carefully to avoid duplicate reporting.

Q3: What happens if I miss the February 2, 2026 deadline?

Missing the deadline triggers escalating penalties: $70 per form if you file within 30 days, $140 per form between 31 days and August 1, and $340 per form after August 1. These penalties apply to each late form, not your total filing. For example, filing 20 forms 45 days late costs $2,800 (20 × $140). File corrections immediately when you discover errors—the sooner you correct, the lower your penalty tier.

Q4: Can I get an extension for Form 1099-NEC?

No. Form 1099-NEC has no extension option, unlike other 1099 variants. You must file with the IRS and furnish recipient copies by February 2, 2026, regardless of circumstances. Form 8809 (Extension Request) explicitly excludes 1099-NEC from extension relief. Other 1099 forms qualify for 30-day automatic extensions if filed before the original deadline.

Q5: What’s the difference between 1099-NEC and 1099-MISC?

Form 1099-NEC reports payments for services performed by non-employees (freelancers, contractors, consultants). Form 1099-MISC reports miscellaneous income including rent, prizes, awards, royalties, and medical payments. The key distinction: 1099-NEC is exclusively for service-related payments, while 1099-MISC covers other payment types. They also have different IRS filing deadlines—1099-NEC requires February 2 filing, while 1099-MISC allows March 31 e-filing.

Q6: Do corporations receive 1099 forms?

Generally no. Payments to C corporations and S corporations are exempt from 1099 reporting, with exceptions for attorney payments (reported on 1099-MISC regardless of entity type) and medical/health care payments. However, payments to LLCs, partnerships, and sole proprietors DO require 1099 filing when thresholds are met. Always check the business entity classification on Form W-9 before determining filing obligations.

Q7: How do I correct an incorrect 1099 I already filed?

File a corrected return as soon as you discover the error. Prepare a new 1099 with accurate information, check the “CORRECTED” box, and submit to the IRS using the same method as your original filing (paper or electronic). Furnish a corrected copy to the recipient with clear indication it supersedes the previous version. The faster you correct, the lower your penalty—corrections within 30 days of the original deadline incur only $70 per form.

Q8: What is the new 1099-K threshold for 2026?

For 2025 tax year reporting (filed in 2026), the threshold is $2,500 in gross payments. For 2026 tax year reporting (filed in 2027), it drops to $2,000. Starting with 2027 tax year reporting (filed in 2028), the threshold becomes $600 with annual inflation adjustments. This phased implementation gives payment processors and taxpayers time to adapt. The transaction count requirement (previously 200 transactions) has been eliminated.

Q9: Do I need to report cryptocurrency transactions on a 1099?

Yes. Starting with 2025 tax year reporting, brokers and payment processors must file Form 1099-DA for digital asset transactions including cryptocurrency sales, NFT transfers, and other blockchain-based assets. The form reports sale proceeds, cost basis, and gain/loss calculations. Even without receiving a 1099-DA, you must report all crypto transactions on your tax return—the IRS treats cryptocurrency as property subject to capital gains tax.

Q10: Can IRS penalties for late 1099 filing be waived?

Yes, if you demonstrate reasonable cause and good faith. Qualifying circumstances include natural disasters, serious illness, unavoidable absence, or destruction of records beyond your control. When you receive Notice 972CG (proposed penalty), respond within 45 days (60 days for foreign filers) with detailed explanation and supporting documentation. The IRS evaluates each request individually—meeting the standard requires showing extraordinary circumstances prevented compliance despite reasonable business care.

Q11: Where do I mail paper 1099 forms?

The mailing address depends on your state location. IRS maintains separate processing centers for different regions. Find your correct address in the IRS Form 1096 instructions, which lists addresses for each state. Using the wrong address delays processing and may result in late filing penalties even if you mailed by the deadline. E-filing through IRIS eliminates mailing concerns and provides immediate confirmation of receipt.

Disclaimer

This article provides educational information about IRS Form 1099 requirements, deadlines, and penalties based on 2026 tax year guidelines. It does not constitute financial, tax, or legal advice. Tax laws and IRS regulations change frequently—always verify current requirements at IRS.gov or consult a certified tax professional, CPA, or enrolled agent for guidance specific to your situation.

Penalty amounts, thresholds, and deadlines mentioned are based on information available as of February 2026 and may be subject to change through IRS announcements or legislative action. For official forms, instructions, and the most current filing requirements, visit the IRS Forms and Publications page.

Internal links to Finance Authority Hub calculators and guides are provided for informational purposes to help readers explore related financial topics. External links to IRS.gov and other .gov, .edu, and .org resources are current as of publication but may change over time.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.