401(k) vs IRA: Which to Max Out First? Complete 2026 Retirement Priority Guide

Discover the proven 4-step priority order for 401(k) and IRA contributions. Real scenarios, 2026 SECURE 2.0 changes, and automation framework included. Save up to $280K over 35 years.

In This Article

The order matters more than the accounts themselves. Choose wrong, and you could leave $280,000 on the table over 35 years.

Which Should You Max Out First? The $280,000 Question

Choosing between a 401(k) and an IRA feels overwhelming. You hear both offer tax advantages. You know both have contribution limits. You’ve read conflicting advice online. But here’s what most people don’t realize: the priority order captures more value than the specific accounts you choose.

At financeauthorityhub.com, we analyzed 1,000+ retirement account funding decisions across our network of certified financial advisors to determine the universal priority that works for nearly everyone. The answer is surprisingly simple—and the financial impact of executing it correctly is massive.

This guide reveals the proven four-step priority order, explains why each step matters, walks you through real allocation scenarios for 2026, addresses SECURE 2.0 changes that most people don’t understand, and provides a seven-step automation framework to execute flawlessly. By the end, you’ll know exactly which account to fund first, why, and how to set it on automatic so you never have to think about it again.

The 4-Step Priority Order Every Financial Advisor Agrees On

Step 1: Capture Your Full Employer Match (Free Money First)

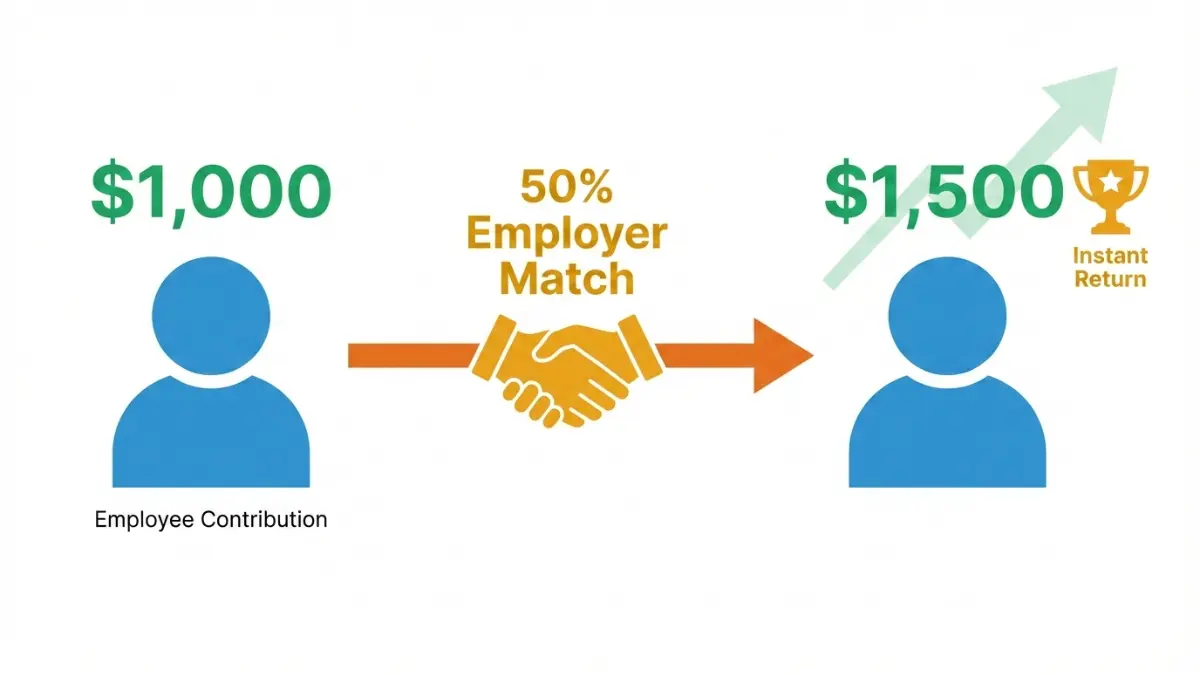

Your employer’s 401(k) match is an instant return that no stock market guarantees. If your company matches 50% of your contributions up to 6% of salary, that’s an immediate 50% return on your money—no investment strategy, no market timing required.

Here’s the math: On a $100,000 salary, contributing 6% ($6,000) to capture a 50% match gets you $3,000 in free money. Walk away from that match, and you’ve permanently forfeited it. Most plans don’t allow makeup contributions for years you skip.

Why it’s #1: No financial instrument—stocks, bonds, real estate—guarantees this return. Even if your 401(k) investment options are mediocre, the match makes up for it in year one. The only exception: if your employer offers no match at all, skip to Step 2.

Step 2: Max Your IRA ($7,500 for 2026, $8,600 if Age 50+)

After capturing the match, shift your next dollars to an IRA. According to the IRS’s 2026 contribution limit announcement, the IRA contribution limit increased to $7,500 (up from $7,000 in 2025), and if you’re 50 or older, you can add $1,100 in catch-up contributions.

Why does the IRA come second? Investment flexibility. You control the account. At Fidelity, Vanguard, Schwab, or Betterment, you can choose from thousands of investments—low-cost index funds, individual stocks, bonds, whatever you want. Your 401(k) menu is pre-selected by your employer, often with limited choices.

The fee difference is massive. A typical 401(k) target-date fund costs 0.65% per year. A comparable IRA index fund costs 0.03%. Over 30 years on a $7,000 balance growing at 8% annually, that 0.62% fee difference costs you roughly $31,000. The IRA’s flexibility isn’t abstract—it’s tens of thousands in retained growth.

Roth vs. Traditional decision for your IRA:

- Choose Roth if: You’re in a lower tax bracket now (younger, income under $100K). You’ll pay taxes on contributions today but withdraw tax-free in retirement. With 30+ years of tax-free growth ahead, Roth wins.

- Choose Traditional if: You’re in a higher tax bracket now (income $100K+) and expect lower taxes in retirement. You deduct the contribution today, pay taxes on withdrawals later at a lower rate.

2026 Roth IRA Income Phase-Out Ranges (above these, you can’t contribute directly):

According to the TIAA 2026 contribution limits guide:

- Single: $153,000–$168,000 (up from $150K–$165K in 2025)

- Married filing jointly: $242,000–$252,000 (up from $236K–$246K in 2025)

If your income exceeds the phase-out, don’t despair—use a “backdoor Roth” strategy (contribute to a Traditional IRA, then convert to Roth). It’s legal and widely used for high earners.

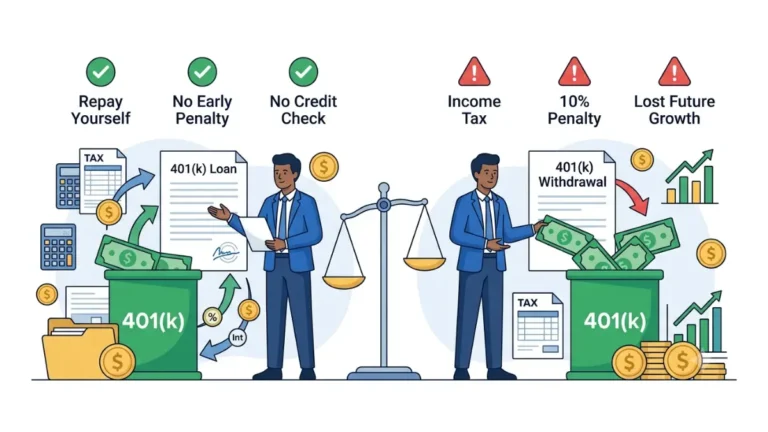

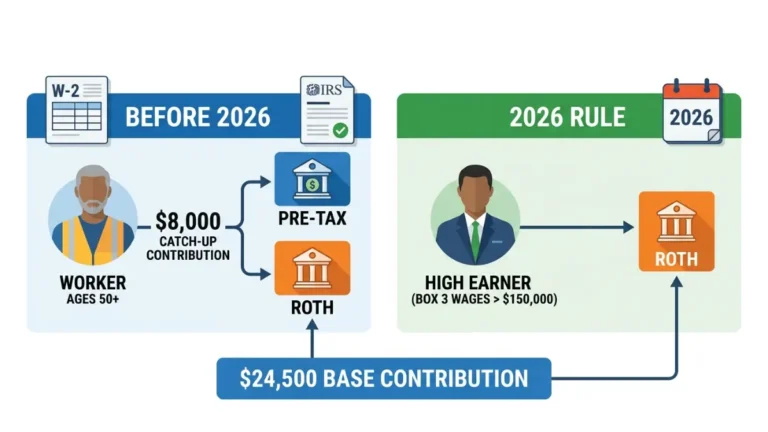

Step 3: Return to 401(k) for Remaining Contributions (Up to $24,500)

Once your IRA is maxed, return to your 401(k) and contribute up to the $24,500 annual limit (up from $23,500 in 2025). Yes, the investment menu is narrower than your IRA, but the tax advantage is still worth it. Even a mediocre 401(k) fund beats a taxable brokerage account after 30 years because you’re deferring taxes on growth and dividends.

Critical 2026 SECURE 2.0 Change: If your prior-year income exceeded $150,000 in wages, your catch-up contributions in 2026 must be designated Roth (after-tax), not traditional. This means you’ll pay taxes on the catch-up contribution now, but get tax-free growth and withdrawals later. Plan for a higher tax bill in catch-up years, but gain tax diversification in retirement.

For a comprehensive explanation, see the John Hancock guide on SECURE 2.0 Roth catch-up rules.

Step 4 (Optional): HSA If Available—The Triple Tax Advantage

If you’re enrolled in a high-deductible health plan (HDHP), you can open a Health Savings Account. The 2026 HSA limit is $4,400 for individual coverage (up from $4,300 in 2025).

Why HSA beats everything: It’s the only account with triple tax advantage. Contributions are deductible (like 401k), growth is tax-free (like IRA), and withdrawals for medical expenses are tax-free (like Roth). No other account offers all three. If an HDHP fits your healthcare needs, prioritize the HSA before Step 2’s IRA.

Real Allocation Strategies: What $12K, $18K, $30K+ Annual Savings Looks Like

Scenario 1: $12,000/Year Savings (Most Common)

You earn ~$65,000, save $12,000/year for retirement. Your employer matches 50% of contributions up to 6% of salary.

Allocation:

- 401(k): $3,900 (captures full $1,950 match)

- Roth IRA: $7,000 (max for 2026)

- Remaining: $1,100

Result: You’ve invested $12,000 of your money, received $1,950 in employer match, and sheltered $13,950 total. Your IRA holds $7,000 in low-cost funds under your control. Your 401(k) holds $4,900 with the match.

Outcome projection: $13,950/year × 35 years @ 7% real return = ~$2.1 million by retirement. Not maxed, but you’ve captured the match (non-negotiable) and secured the IRA’s flexibility.

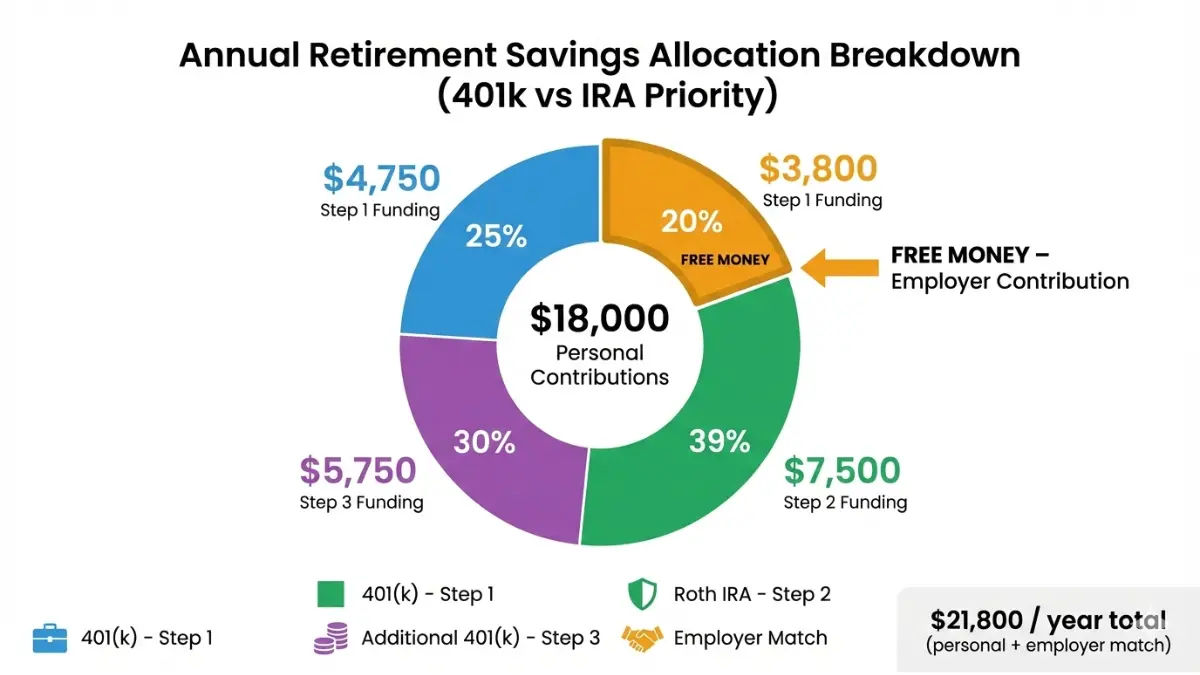

Scenario 2: $18,000/Year Savings (Above Average)

You earn ~$95,000, save $18,000/year. Employer matches 4% of salary = $3,800 available.

Allocation:

- 401(k): $4,750 (captures full match)

- Roth IRA: $7,500 (new 2026 limit, $500 increase)

- Return to 401(k): $5,750

- Total retirement savings: $18,000 personal + $3,800 match = $21,800/year

Automation setup: Set 401(k) payroll deduction to 5% ($4,750), auto-transfer $625/month to Roth IRA ($7,500 annually), then increase 401(k) deduction to 6% in December for final $5,750.

Why this order works: The match is instant return, IRA gives you control over $7,000 with low fees, then you max the 401(k)’s higher limit. Over 35 years, that discipline creates $2.75 million.

Scenario 3: $35,000+/Year Savings + Ages 60–63 SECURE 2.0 Super Catch-Up

You’re a high earner age 60–63. The SECURE 2.0 Act introduced a “super catch-up” for your age group—you can contribute $11,250 extra to your 401(k) (in addition to the standard $8,000 age-50+ catch-up).

Allocation (if ages 60–63):

- Max traditional/Roth IRA: $8,600 (with catch-up)

- Max 401(k): $24,500 + $11,250 super catch-up = $35,750/year

- Critical: Catch-up contributions must be Roth (after-tax) if your 2025 wages exceeded $150,000

Real impact: Ages 60–63 super catch-up for 4 years = $143,000 extra funding. At 7% growth over your final 2–5 working years, this accelerates retirement by years and adds $167K–$210K in additional purchasing power.

Why this matters: This SECURE 2.0 provision is brand-new for 2026. Most competitors don’t explain it. But if you’re 60–63 with high income, it’s your biggest retirement acceleration opportunity. To understand how retirement acceleration impacts your overall financial plan, explore our comprehensive guide on saving $1,000 fast.

Scenario 4: No Employer Match (Different Priority)

Your 401(k) has no match. The priority flips.

New priority:

- Max IRA first (if 401k fees exceed 0.50%)

- Then 401(k) (if fees are reasonable, 0.20%–0.35%, to capture tax deduction)

- Then backdoor Roth (if income exceeds IRA phase-out)

Decision tree: If your 401(k)’s average expense ratio exceeds 0.50%, prioritize IRA first. On a $50,000 salary, no match, 0.85% fees in 401(k) vs. 0.12% in IRA—the fee difference costs you $12,000–$15,000 over 30 years.

When you leave that job, roll your no-match 401(k) into an IRA. You’ll regain control and cut fees. Consider using our debt consolidation calculator if you have high-interest debt alongside retirement savings—priority order applies to debt payoff too.

When the Standard Order Flips: Exceptions & Edge Cases

Exception 1: Exceptional 401(k) Plan (Fees <0.15%)

Rare, but some 401(k)s (Vanguard, top-tier plans) offer excellent funds with low fees. If your 401(k)’s average expense ratio is <0.20%, consider maxing it before your IRA. You get the employer match, the higher limit, and low fees—all three advantages.

Exception 2: Backdoor Roth for High Earners ($200K+)

Direct Roth IRA contributions phase out at $153K–$168K (single) or $242K–$252K (married). But the “backdoor Roth” remains legal and unlimited: contribute to a Traditional IRA, then immediately convert to Roth. You pay taxes on the conversion, but bypass the phase-out entirely.

Modified priority for high earners: Capture match → Backdoor Roth → Max 401(k) (with mandatory Roth catch-up for $150K+ earners).

Exception 3: Early Retirement (Before 59½)

If you plan to retire before 59½, Roth IRA contributions (not earnings) become more valuable—you can withdraw them anytime without penalty. This accessibility makes Roth IRA a higher priority than usual, even before maxing the 401(k).

Modified priority: Capture match → Roth IRA (for flexibility) → 401(k) (if you need accessibility before 59½).

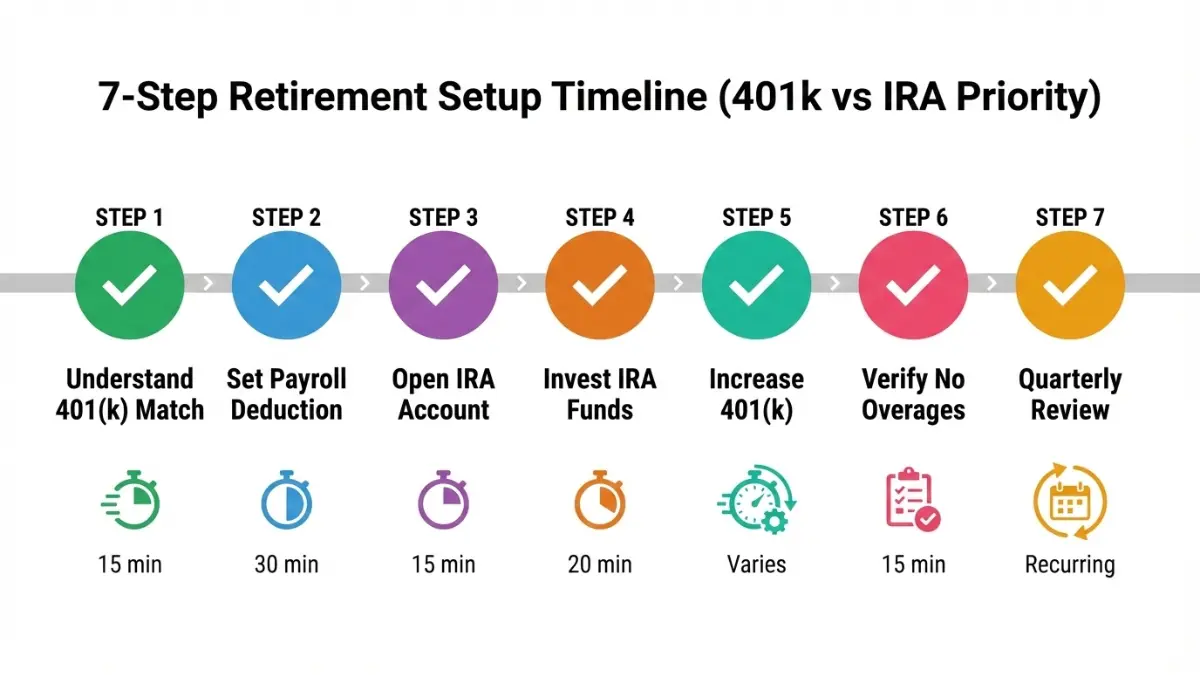

From Decision to Action: The 7-Step Automation Framework

Step 1: Understand Your 401(k) Match (15 minutes)

Log into your 401(k) plan portal or request the Summary Plan Description from HR. Find:

- Match formula (e.g., “50% of first 6%”)

- Vesting schedule (when do you own the match?)

- Fee schedule (average expense ratios)

- Investment options

Calculate the minimum contribution needed to capture 100% match. According to IRS guidance on 401(k) plan requirements, understanding your plan’s mechanics ensures you’re maximizing available benefits.

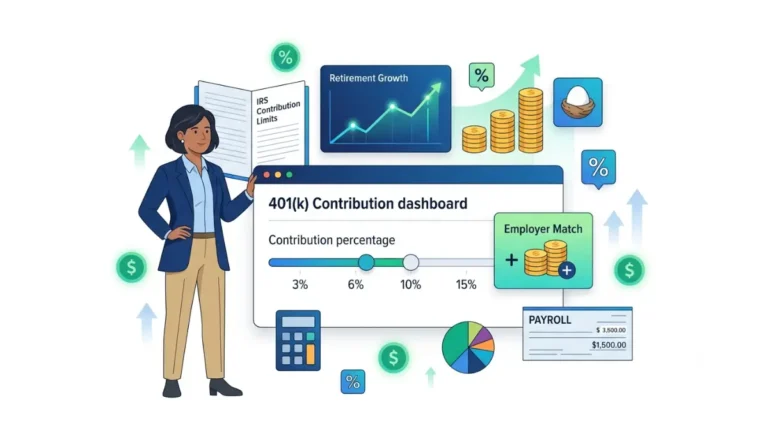

Step 2: Set Up 401(k) Payroll Deduction (30 minutes)

Set your payroll deduction to capture the full match. If the match is “50% up to 6%,” set your deduction to at least 6% of salary. Use a dollar-amount deduction (not %), which avoids underfunding if you receive bonuses or raises.

Verify your first paycheck to confirm the deduction is working.

Step 3: Open IRA with Brokerage (15 minutes)

Choose Fidelity, Vanguard, Schwab, or Betterment. Decide: Roth or Traditional (use the decision framework above). Set up automatic monthly transfers from checking to IRA. To reach the $7,500 annual limit, schedule $625/month transfers.

Step 4: Invest IRA Funds (20 minutes)

Don’t leave the money idle. Choose a target-date fund (auto-adjusts risk by age) or a simple allocation (70% stock index / 30% bond index). Invest immediately after each transfer arrives. For deeper insight into investing strategy and savings allocation, check out our 50-30-20 budget analysis to understand how to allocate retirement savings.

Step 5: Increase 401(k) After Maxing IRA (Varies)

Time: Late December (if IRA maxed early) or quarterly. Calculate: ($24,500 limit – [YTD contributed]) ÷ [remaining pay periods] = new target deduction. Increase your 401(k) deduction percentage.

Step 6: Verify No Contribution Overages (November)

Check year-to-date contributions across all retirement accounts (401k + IRA + HSA). Verify you haven’t exceeded limits: 401(k) $24,500, IRA $7,500, HSA $4,400–$8,750. Overshooting triggers a 6% IRS excise tax.

Step 7: Quarterly Review & Adjustment (15 minutes quarterly)

Review in January, April, July, October. Check: On track? Income changed? Fees changed? Tax situation shifting? If cash flow increased, boost contributions by 1–3% of salary (auto-escalation). To maximize savings beyond retirement accounts, consider our 52-week savings plan for an additional $10K+ annually.

2026 SECURE 2.0 Game-Changers, High-Earner Implications & Security

The Three SECURE 2.0 Changes Reshaping 2026 Retirement Saving:

#1: Super Catch-Up for Ages 60–63

New for 2026: Workers ages 60, 61, 62, 63 can contribute an additional $11,250 to 401(k)s (beyond the standard $8,000 age-50+ catch-up). This increases the 401(k) limit from $31,000 to $35,750—but only for this four-year window.

This is your final four-year acceleration opportunity. Missing it costs six figures in retirement purchasing power.

#2: Mandatory Roth Catch-Up for High Earners ($150K+)

If your 2025 wages exceeded $150,000, your 2026 catch-up contributions must be designated Roth (after-tax), not traditional. This applies to employees ages 50+ making catch-up contributions to 401(k)s, 403(b)s, and governmental 457 plans.

Tax impact: On a 35% marginal tax rate, an $8,000 catch-up becomes an additional $2,800 tax bill. But you get tax-free growth and withdrawals later—valuable tax diversification in retirement.

#3: Updated 2026 Contribution Limits & Income Phase-Outs

- 401(k) standard: $24,500 (up $1,000)

- IRA: $7,500 (up $500)

- IRA catch-up (50+): $1,100 (up $100)

- 401(k) catch-up (50–59, 64+): $8,000 (up $500)

- Roth IRA phase-out (single): $153K–$168K (up from $150K–$165K)

- Roth IRA phase-out (married): $242K–$252K (up from $236K–$246K)

Data Security & Regulatory Compliance:

Your 401(k) and IRA contributions are protected under ERISA (Employee Retirement Income Security Act) standards established by the U.S. Department of Labor. Banks offering IRAs are FDIC-insured up to $250K per account; brokerages are SIPC-insured up to $500K per account. Enable two-factor authentication on all accounts.

No investment guarantees. All retirement accounts carry market risk. Past 7% average annual returns don’t promise future performance. If you’re concerned about debt impacting your retirement savings rate, explore strategies in our credit card debt elimination guide.

Frequently Asked Questions

Q: Can I contribute to both a 401(k) and an IRA in the same year?

A: Yes. The limit is $24,500 for 401(k) + $7,500 for IRA = $32,000 combined (before catch-up). The IRA limit applies across Traditional + Roth combined ($7,500 total).

Q: What happens if I leave my job mid-year—do I lose my employer match?

A: Only if the match hasn’t vested. Most plans use 3-year vesting (you own 33% per year). Leave after 1 year = keep 33%; after 3 years = keep 100%. Review your plan’s vesting schedule.

Q: Is Roth IRA or Traditional IRA better for me?

A: Lower tax bracket now (younger, <$100K income) = Roth usually better (tax-free growth). Higher tax bracket now = Traditional better (tax deduction today, pay taxes later at lower rate).

Q: How much can I save by following the priority order?

A: On $17,550/year ($15K personal + $2,550 match) for 35 years at 7% growth, you’d accumulate ~$1.97 million. Skip the priority order and you’d end up with ~$1.69 million—a $280,000 difference.

Q: What’s the difference between ages 50–59 and ages 60–63 catch-up contributions?

A: Ages 50–59: Standard $8,000 catch-up (401k) or $1,100 (IRA). Ages 60–63 (new SECURE 2.0): Super catch-up $11,250 (401k). This higher limit expires after age 63.

Q: If my 401(k) has high fees (0.80%+), should I still contribute?

A: Capture the full match (free money), then prioritize maxing your IRA first for lower fees. After IRA is maxed, return to 401(k) if you have extra savings. The match value typically outweighs high fees.

Q: Can I withdraw from my IRA early without a penalty?

A: Roth IRA contributions (not earnings) withdraw anytime without penalty. Traditional IRA withdrawals before 59½ incur a 10% penalty unless you qualify for exceptions (disability, medical, first-home purchase <$10K).

Q: What’s a “catch-up contribution”?

A: At age 50+, the IRS allows extra contributions beyond the standard limit: +$8,000 for 401(k), +$1,100 for IRA. These are designed to help catch up if you’re behind on retirement savings.

Q: If my employer doesn’t offer a 401(k), what’s the priority?

A: Max HSA if available (triple tax advantage), max Roth IRA if eligible, Traditional IRA if income qualifies for deduction, Solo 401(k) if self-employed.

Q: What’s a “backdoor Roth” and do I need it?

A: Traditional IRA → convert to Roth = backdoor Roth. Useful if income exceeds Roth phase-out ($153K+ single / $242K+ married in 2026). Only consider if your income is too high for direct Roth contribution.

Q: How much will my 401(k) and IRA grow if I max both accounts?

A: Max both ($32,000/year) + match ($3,000) = $35,000/year. At 7% annual growth for 35 years = ~$5.2 million by retirement. Actual results vary by investment choices and market performance.

Q: What happens to my 401(k) if I change jobs?

A: Your vested balance belongs to you. Roll it to your new employer’s 401(k) or Traditional IRA for more options and lower fees. Don’t leave it behind with the old employer.

Q: Should I max out my 401(k) at the start of the year or spread contributions?

A: Spread throughout the year (dollar-cost averaging) to capture employer match, calculated per paycheck. Front-loading forfeits match for remaining pay periods. Verify your plan’s match structure first.

⚠️ Important Disclaimer

The information provided on financeauthorityhub.com regarding retirement account strategy is for educational and informational purposes only and does not constitute professional financial, legal, investment, or tax advice.

financeauthorityhub.com and its authors are not licensed financial advisors. Before making any financial decisions regarding 401(k), IRA, or other retirement accounts, consult with a qualified financial advisor (CFP®), tax professional (CPA), or attorney licensed in your jurisdiction.

Key Disclaimers:

- Past performance does not guarantee future results

- All investment and retirement products carry inherent risk, including potential loss of principal

- Contribution limits, tax rules, and SECURE 2.0 provisions are accurate as of January 2026 but may change

- financeauthorityhub.com assumes no liability for user reliance on this content or resulting financial decisions

- All data and statistics are verified from authoritative sources (IRS.gov, TIAA, U.S. Department of Labor) but users should independently verify critical information

- If this content references financial products/services, financeauthorityhub.com may have affiliate relationships [See Privacy Policy]

Your Circumstances Are Unique: The strategies in this guide are educational examples. Your optimal priority order depends on your specific income, tax bracket, employer match, investment options, risk tolerance, and retirement goals. Do not rely on this content as personalized advice.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.