Retirement Savings by Age: 2026 Catch-Up Strategies

Saving for retirement is overwhelming if you’re behind. This guide covers 2026 benchmarks, income-stratified targets, psychological barriers, and a 7-step catch-up playbook most savers miss.

In This Article

Saving for retirement can feel overwhelming, especially if you feel behind. But here’s the truth: 88% of Americans worry about retirement preparedness—and if you’re one of them, new 2026 rules just changed the game. This guide walks you through exactly where you should be, why benchmarks matter, and the specific catch-up strategies most savers don’t know about.

Why Retirement Savings by Age Matters (Even More in 2026)

Retirement benchmarks aren’t one-size-fits-all mandates—they’re evidence-based targets based on decades of financial data. According to the Federal Reserve Survey of Consumer Finances, the median American at 45-54 has saved $115,000, while the average is $313,220. The gap? Income level matters enormously.

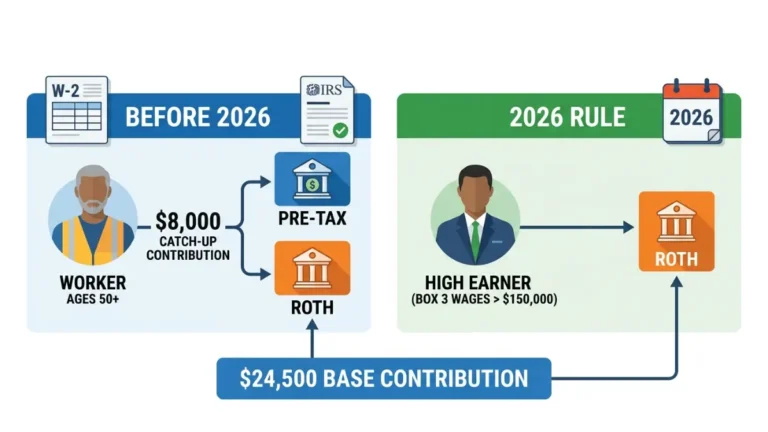

What’s changed in 2026? The IRS introduced a “super-catch-up” provision—workers aged 60-63 can now contribute an additional $11,250 to their 401(k), on top of the standard $24,500 limit. That’s $35,750 total annually. For late starters, this could mean the difference between “behind” and “on track” within 5-10 years.

This guide covers 2026-updated benchmarks, income-stratified targets, psychological barriers competitors ignore, and a step-by-step catch-up playbook. We analyzed Federal Reserve data, IRS rules, and real-world scenarios to answer: “Where should I actually be, and how do I get there?”

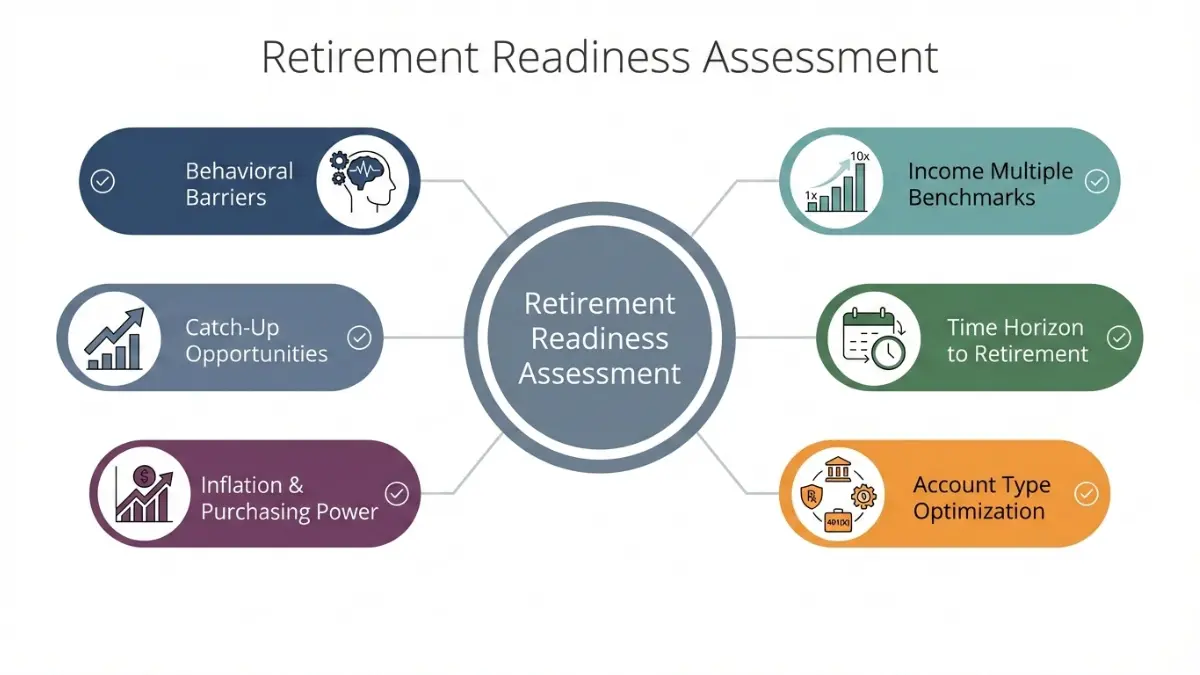

How to Evaluate Your Retirement Readiness: The Framework

Before you panic about numbers, understand what matters:

1. Income Multiple Benchmarks

The most cited framework comes from Fidelity’s research: save 1x your salary by 30, 3x by 40, 6x by 50, 8x by 60, and 10x by 67. This assumes you earn the same throughout (you’ll likely earn more), so these are conservative estimates.

2. Time Horizon to Retirement

A 40-year-old and a 55-year-old face different math. The 55-year-old needs aggressive strategies; the 40-year-old benefits from compound growth.

3. Account Type Optimization

Not all savings are equal. A $50,000 balance split between a taxable account and Roth IRA yields different tax outcomes than $50,000 in a 401(k). Strategic account selection matters.

4. Inflation and Purchasing Power

Federal Reserve data shows historical inflation averages 2-3% annually. Your retirement target needs adjustment for future dollars, not today’s dollars. A million dollars in 2026 buys less in 2045.

5. Catch-Up Opportunities

At 50, you unlock $8,000 extra annually in 401(k) catch-up contributions. At 60-63, that jumps to $11,250. These aren’t bonuses—they’re strategic levers that can close a $200K gap in 5 years.

6. Behavioral Barriers

Psychology research shows smart people under-save due to present bias (today feels more real than retirement), loss aversion (the pain of “giving up” money now), and hyperbolic discounting (distant benefits feel less valuable). Awareness is your first defense.

Retirement Savings Benchmarks by Age (2026 Federal Reserve Data + Income Stratification)

Federal Reserve Median vs. Average Data

The Federal Reserve’s 2023 Survey shows stark income inequality:

| Age Group | Median Savings | Average Savings |

|---|---|---|

| 35-44 | $45,000 | $145,000 |

| 45-54 | $115,000 | $313,220 |

| 55-64 | $185,000 | $537,560 |

| 65-74 | $200,000 | $609,230 |

What does this mean? Half of 55-64-year-olds have less than $185K saved. The median is realistic; the average is inflated by high-income earners.

Fidelity’s 10x Rule Explained

Fidelity’s benchmarks assume consistent saving of ~15% of gross income from age 25-67. If you earn $70,000 at age 50 and save 15% annually, you’d aim for ~$420,000 (6x × $70K). But most people don’t save consistently, so these become targets requiring catch-up strategies.

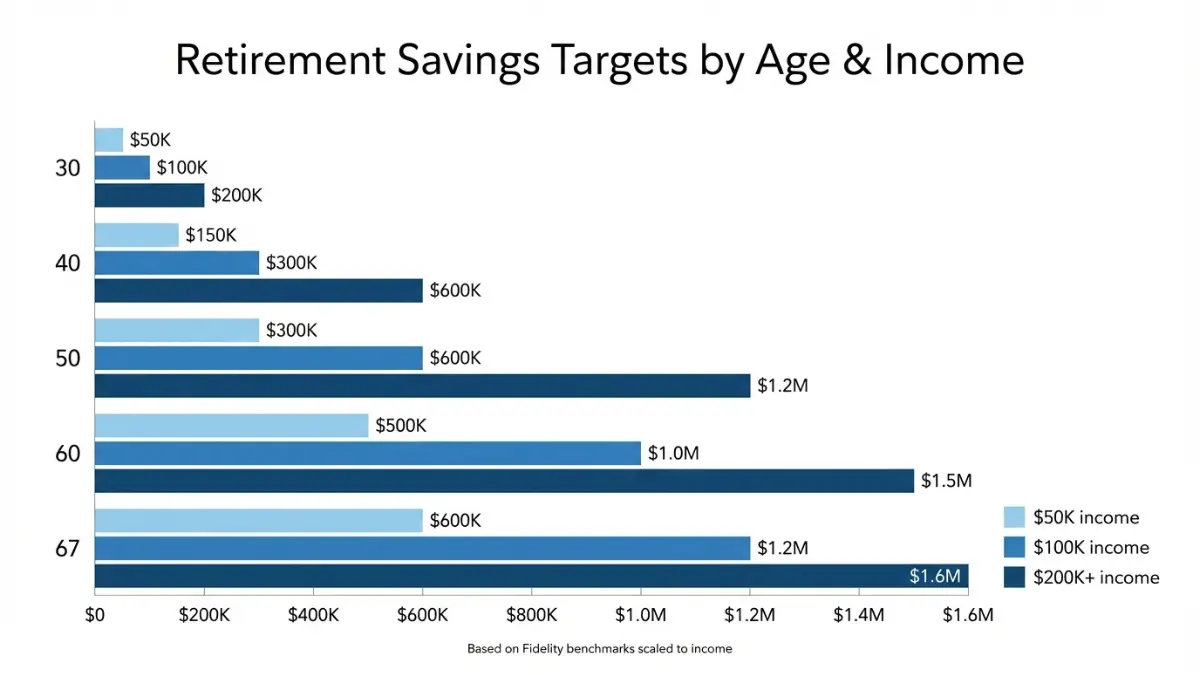

Income-Stratified Retirement Savings Targets (Your Real Situation)

Benchmarks should scale with income. Here’s what actual target-setting looks like:

For $50K Annual Earners:

- Age 30: Target $50K (1x)

- Age 40: Target $150K (3x)

- Age 50: Target $300K (6x)

- Age 60: Target $400K (8x) — Catch-up Gap: -$200K? Use super-catch-up for 5 years @ $11.25K/year = $56K + growth

For $100K Annual Earners:

- Age 30: Target $100K (1x)

- Age 40: Target $300K (3x)

- Age 50: Target $600K (6x)

- Age 60: Target $800K (8x)

For $200K+ Annual Earners:

- Age 30: Target $200K+ (1x)

- Age 40: Target $600K+ (3x)

- Age 50: Target $1.2M+ (6x)

- Age 60: Target $1.6M+ (8x) — High earners can use mega backdoor Roth + super-catch-up for tax efficiency

Real-Dollar Scenarios by Life Stage

Ages 25-35: Building the Foundation

A 28-year-old earning $55K should target $55K saved by 30. If they’re behind, they have 37 years of compound growth—time is their biggest asset. Contributing $500/month yields $180K by age 65 (assuming 7% returns).

Ages 35-45: Acceleration Phase

A 40-year-old earning $80K should aim for $240K (3x) saved. If they’ve only saved $100K, they’re behind but recoverable. Increasing contributions to $800/month for 10 years, plus 7% returns = $152K additional growth, reaching ~$252K by 50.

Ages 45-55: The Catch-Up Window

This is where catch-up contributions shine. A 48-year-old with $250K saved, earning $90K, should have $540K by 50 (6x). Using catch-up contributions ($8,000 401k + employer match + IRA contributions) can add $25K+ annually, closing the gap within 2-3 years.

Ages 55-65: Final Sprint

A 60-year-old earning $100K with $500K saved is on track for the 8x benchmark ($800K). But with the new super-catch-up ($11,250), they can add $56K+ over 5 years before retirement, building a comfortable cushion.

Retirement Savings: Benchmarks vs. Rules of Thumb vs. Real Needs

No single framework works for everyone. Here are three approaches:

Benchmark Approach (Fidelity 10x Rule)

- Pros: Simple, based on historical data, easy to track

- Cons: Assumes consistent saving, ignores personal spending, doesn’t account for pension/Social Security nuances

- Best for: Employees with steady income and employer 401(k) match

Percentage-of-Income Approach (Save 15-20% Annually)

- Pros: Flexible, scales with salary growth, accounts for lifestyle

- Cons: Requires discipline, easy to deprioritize

- Best for: Self-employed, freelancers, high-variable-income earners

Real-Needs Approach (Calculate Actual Retirement Expense)

- Pros: Personalized to your lifestyle, addresses actual anxiety

- Cons: Requires detailed planning, can be pessimistic

- Best for: Early retirees, those with specific retirement plans

Which matters most? Research shows the benchmark approach builds confidence (validation), the percentage approach drives consistent behavior, and the real-needs approach reduces regret. Ideally, use all three: aim for benchmarks, commit to percentages, and validate against real needs.

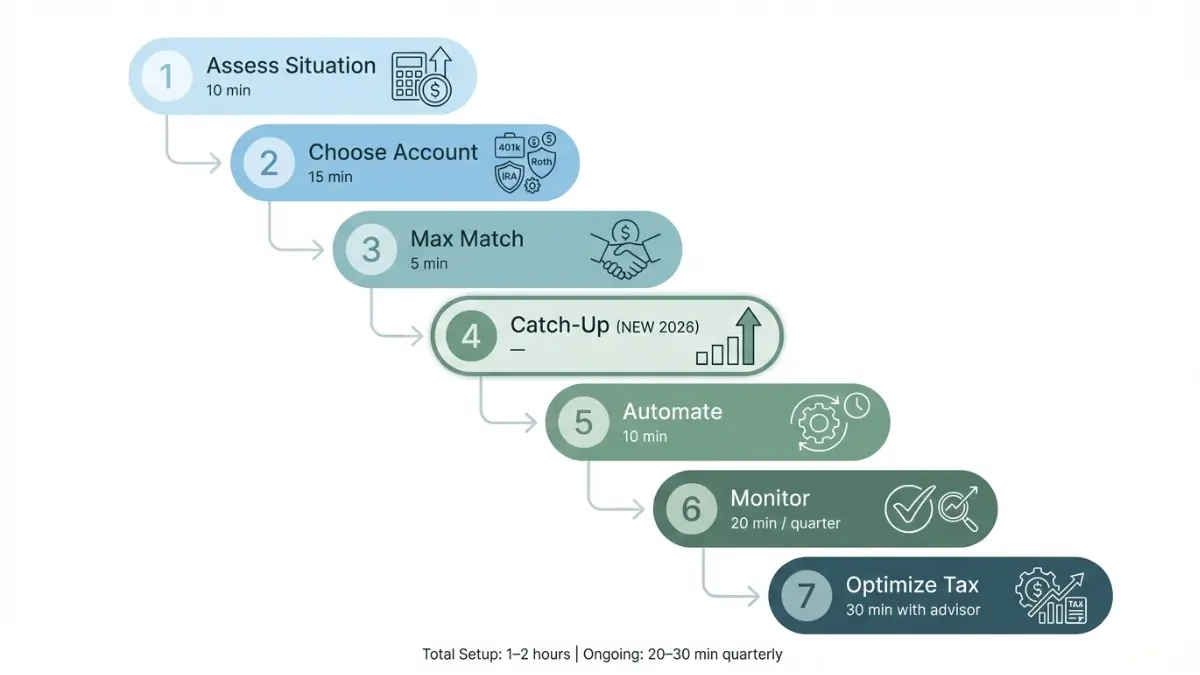

Your 7-Step Retirement Catch-Up Playbook

If you’re behind, here’s your tactical roadmap:

Step 1: Assess Your Current Situation (10 minutes)

Calculate net retirement savings = 401(k) balance + IRA balance + taxable brokerage savings. Compare to benchmarks above. If you’re 30% behind, you need a 10-15% annual contribution increase. Behind 50%? You need 20%+ increases plus extended work or lifestyle adjustment.

Step 2: Choose Your Primary Account Vehicle (15 minutes)

If your employer offers a 401(k) with match: max the match first (free money). Then max your 401(k) contribution for the year. Then open a backdoor Roth IRA (if income allows) for tax-free growth. See our detailed 401(k) vs. IRA guide for nuanced decisions.

Step 3: Maximize Employer Match (5 minutes)

If your employer matches 50% of contributions up to 6%, contribute at least 6%. That’s an instant 50% return. Never leave it on the table.

Step 4: Leverage Catch-Up Contributions (NEW 2026 angle)

- At 50+: Contribute an extra $8,000/year (2026 limit)

- At 60-63: Contribute an extra $11,250/year (super-catch-up)

- Strategy: If you’re 50 with $300K saved but need $600K by 60, the super-catch-up ($11.25K × 5 years = $56K) plus employer match growth can close the gap

Step 5: Automate & Set Reminders (10 minutes)

Behavioral research proves automation works. Set up automatic transfers to your 401(k) or IRA on payday. Increase contributions by 1-2% annually with raises. This removes willpower from the equation.

Step 6: Monitor & Adjust Quarterly (20 minutes/quarter)

Track progress quarterly, not obsessively monthly. Review: Am I on pace? Has my salary changed? Do I need to increase contributions? Market volatility is normal; adjusting behavior isn’t.

Step 7: Optimize Tax Efficiency (30 minutes with advisor)

High earners should explore mega backdoor Roth (after-tax 401(k) contributions converted to Roth) and HSA strategies (triple-tax-advantaged health savings account). See our Roth IRA tax-free guide for deeper strategies.

Why Trust Matters: Security, Compliance, and Psychological Validation

Retirement savings requires trust in several areas:

Security & Compliance

Your 401(k) is protected by FDIC insurance (up to employer plan limits). IRAs are similarly protected. Check your provider’s security certifications (look for SOC 2 compliance). Ask: Is my data encrypted? What’s their data breach history?

Regulatory Safety

The SEC oversees investment advisors, the IRS sets contribution limits, and FINRA regulates broker-dealers. If something feels sketchy (promises of guaranteed returns, pressure to move funds, unregistered advisors), it probably is.

Psychological Validation

Research shows people who benchmark against peers feel more confident. Here’s the psychological truth: most Americans are behind benchmarks. That’s normal, not shameful. If you’re taking action now—reading this, understanding catch-up strategies, automating contributions—you’re ahead of 60% of people who do nothing.

Realistic Outcomes

These strategies help, but they don’t replace your discipline. Tools enable behavior; you drive results. Saving $11,250/year at 60-63 is powerful, but only if you commit for 5 years.

Frequently Asked Questions

Q1: How much retirement savings is considered “on track” for my age?

A: Median benchmarks: Age 45-54 should aim for $115K-$300K (depending on income). Age 55-64 should aim for $185K-$540K. But “on track” is personal—calculate your real retirement expense first.

Q2: Is it too late to catch up if I’m behind?

A: No. If you’re 50+ with 15-17 years to retirement, catch-up contributions ($8,000-$11,250/year) plus compound growth can close 30-50% gaps. The earlier you act, the better, but 50+ strategies exist specifically for late starters.

Q3: What’s the difference between Fidelity’s 10x rule and Federal Reserve data?

A: Fidelity assumes consistent 15% annual savings from age 25. Federal Reserve data shows actual savings (people who save less, save later, or pause savings). Fidelity’s is aspirational; Fed data is realistic.

Q4: Should I max my 401(k) or Roth IRA first?

A: If your employer matches 401(k), capture the match first (free money). Then contribute to Roth IRA up to the limit ($7,500 in 2026). Then return to 401(k). See our detailed 401(k) vs. IRA article.

Q5: How much should I save at age 50 to retire at 67?

A: For a $100K earner, aim for $600K+ by age 50 (6x rule). If you have $400K, increase contributions $15-20K annually for 5 years, then standard contributions for the final 12 years. Catch-up helps significantly.

Q6: What’s the 2026 super-catch-up rule for ages 60-63?

A: NEW: Workers 60-63 can contribute $11,250 extra annually (on top of $24,500 base), totaling $35,750/year. This replaces the standard $8,000 catch-up for that age group. Plan to max this if eligible.

Q7: Can I use home equity as retirement savings?

A: Home equity is illiquid. Focus retirement accounts on liquid assets (401k, IRA). Home equity is a backup—useful for downsizing, reverse mortgages, or emergencies, but not primary retirement income.

Q8: How does inflation affect retirement targets?

A: Inflation reduces purchasing power. Target retirement balances today’s dollars. A $1M retirement target today is worth ~$800K in 20 years (assuming 3% inflation). Inflate your targets 2-3% annually.

Q9: Are benchmarks different for women?

A: Women statistically earn less ($0.82 per male dollar), take caregiving gaps, and live longer. Benchmarks apply, but career context matters. Catch-up contributions at 50+ are especially valuable for women recovering from income gaps.

Q10: What if I’m self-employed or freelance?

A: You can open a Solo 401(k) (up to $72,000 contribution limit in 2026) or SEP IRA (~25% of net income). Catch-up provisions apply equally. Self-employed? Consult a tax professional for optimization.

Q11: How often should I review my retirement plan?

A: Annually minimum (especially after job changes, salary increases, or major life events). If aggressive catch-up, review quarterly. Quarterly reviews take 20 minutes; annual reviews take 1-2 hours but drive better decisions.

Important Financial Services Disclaimer

The information provided on financeauthorityhub.com is for educational and informational purposes only. This content does NOT constitute professional financial, investment, legal, or tax advice.

financeauthorityhub.com and its authors are NOT licensed financial advisors. Before making any financial decisions, consult with a qualified financial advisor, tax professional, or attorney licensed in your jurisdiction.

Key Disclaimers:

- Retirement savings targets are benchmarks, not guarantees

- Past performance does not guarantee future results

- All investments carry risk, including potential loss of principal

- Federal Reserve data is historical; your actual retirement needs may differ based on inflation, healthcare, and lifestyle

- 2026 contribution limits are per IRS as of January 2026; verify current limits at IRS.gov

- financeauthorityhub.com assumes no liability for user reliance on this content

See our Terms of Service and Privacy Policy for complete disclosures.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.