How a Retiree Should Weigh Selling a Structured Settlement

Structured settlement payments of $1,500 a month feel safe—until a buyer offers cash. See the real cost, court approval, and keep-or-sell math.

Structured settlement payments of $1,500 a month feel safe—until a buyer offers cash. See the real cost, court approval, and keep-or-sell math.

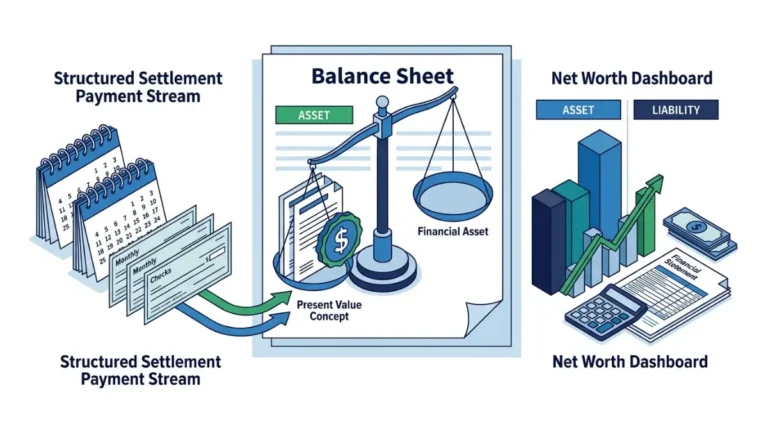

Structured settlement net worth confuses most people—it’s present value, not face total. Here’s the right number for every form you fill out.

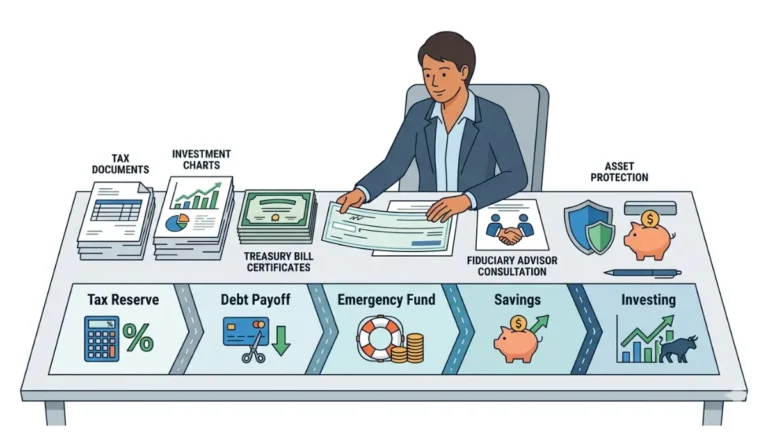

Large settlement money is protected only to $250,000 per bank, and punitive damages are taxable. Here’s the first-30-days plan most people skip.

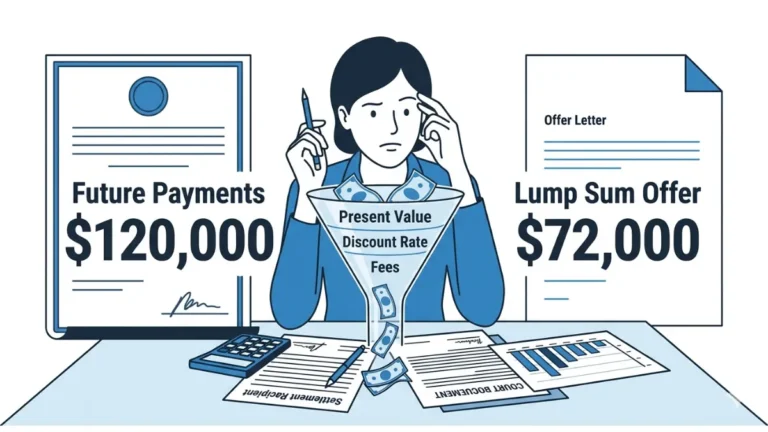

Structured settlement factoring requires court approval and a ‘best interest’ finding — see the four inputs that shape your lump-sum offer.

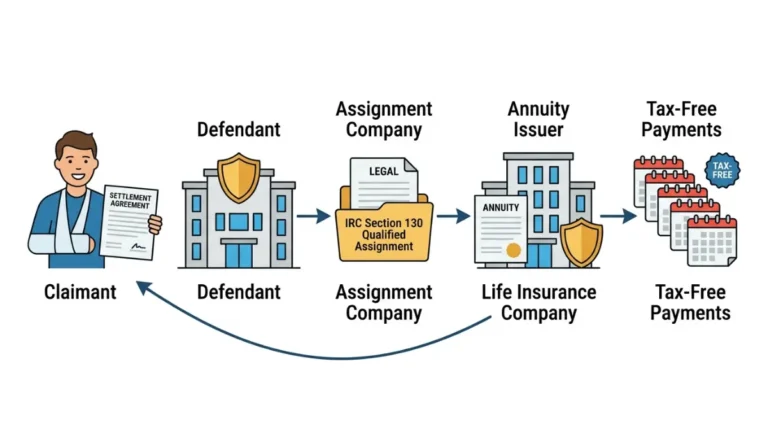

Structured settlement payments escape federal income tax because of one 1982 law—and a later rule decides who pays the 40% tax when you sell.

Florida structured settlement sales need court approval, and the payout runs well below face value. See the 45–90 day process and what you keep.

Qualified assignments make injury settlements tax-free under IRC 130—but selling those payments can trigger a 40% tax most sellers never see coming.

Structured settlement money never counts toward the $184,500 Social Security wage base or your self-employment tax—see why, and what still gets taxed.

A structured settlement cash advance is legal only with a judge’s approval — and a 2026 personal loan near 12% APR often costs far less.

Personal injury structured settlement talks involve five parties and one irreversible signature. Know who’s across the table before you negotiate.