Does a Structured Settlement Count Toward Your Net Worth?

Structured settlement net worth confuses most people—it’s present value, not face total. Here’s the right number for every form you fill out.

In This Article

You are filling out a form — a loan application, a benefits worksheet, a divorce disclosure — and it asks for your total assets. You receive monthly payments from a structured settlement, and you have no idea whether to enter them, or at what number.

That single question is where most people get the math wrong.

The short answer: yes, a structured settlement counts toward your net worth — but as the present value of the remaining payments, not their face value, and the way it “counts” changes completely depending on who is asking.

This guide gives you the right figure for each situation, the calculation behind it, and the mistakes that quietly cost people thousands. Every figure reflects rules current in 2026.

ℹ️ Disclaimer: The investing, tax, and benefits-eligibility information in this article is for educational purposes only and reflects U.S. federal rules in effect as of 2026. How a structured settlement is valued, reported, taxed, or sold depends on your state and personal circumstances and can affect needs-based benefits such as SSI and Medicaid. Consult a licensed financial advisor, a CPA or tax attorney, or a benefits/elder-law attorney before making any decision involving your settlement.

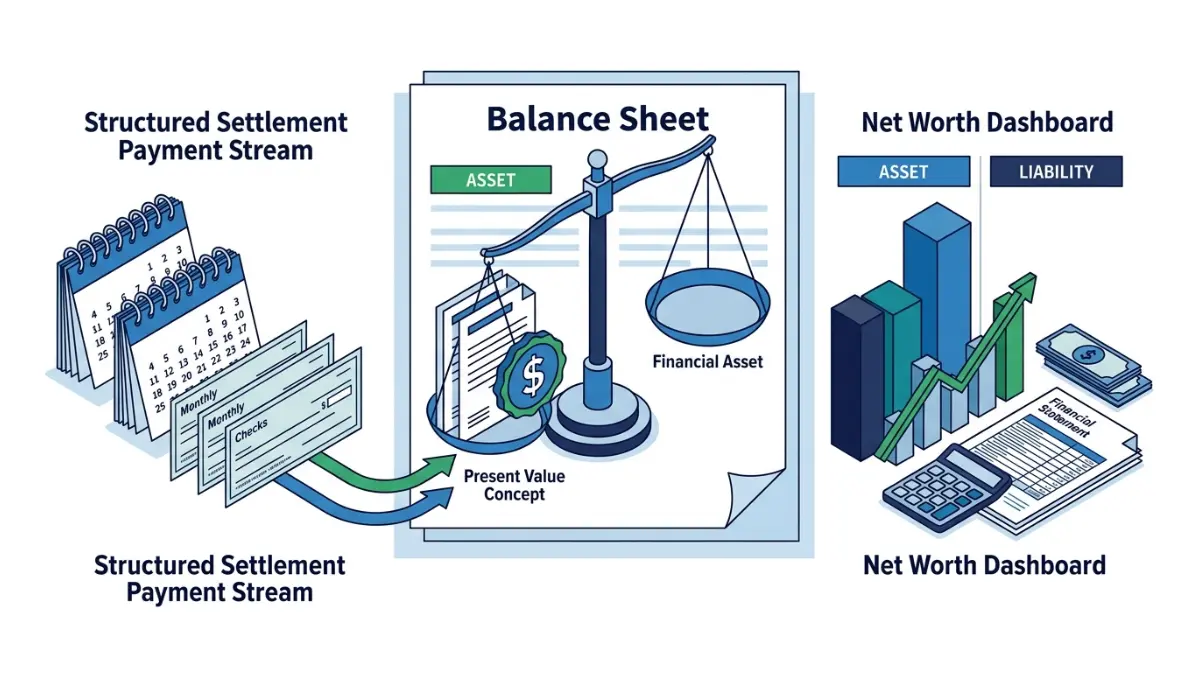

Is a structured settlement an asset on your net worth?

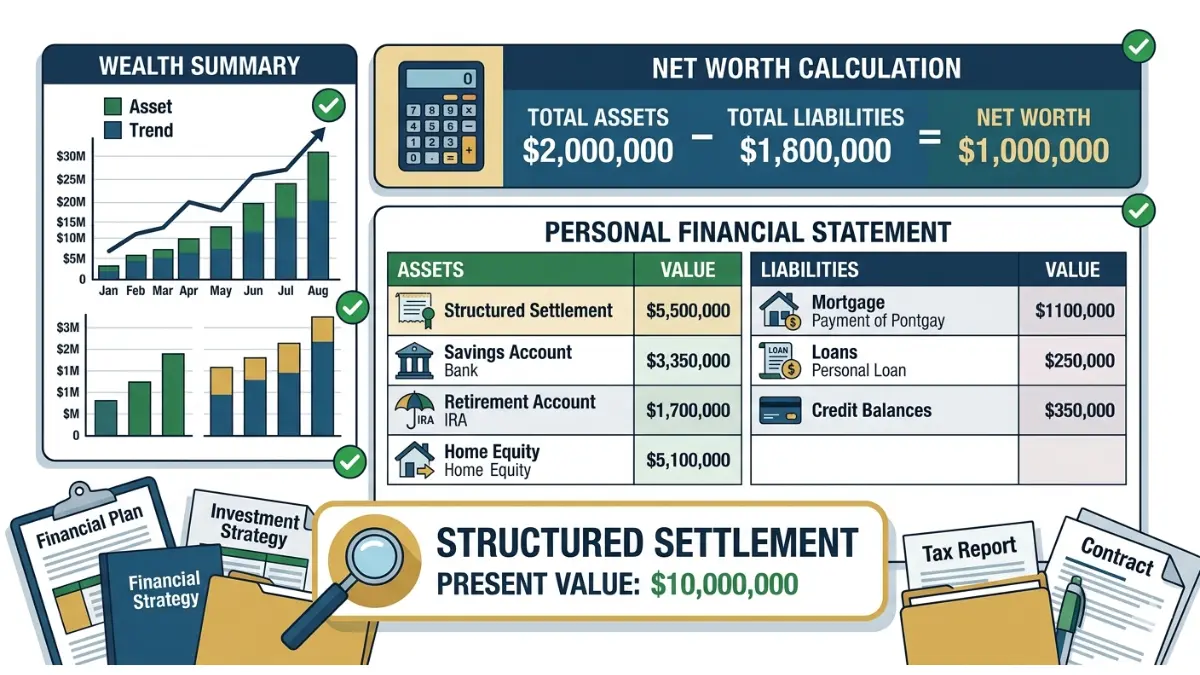

Yes. A structured settlement is an asset, and its value belongs on your personal balance sheet at the present value of the payments you have left to collect.

Net worth is a simple subtraction: total assets minus total liabilities. Your settlement sits on the asset side, alongside cash, retirement accounts, and home equity.

The catch is that it is an illiquid asset. You cannot withdraw the balance the way you tap a savings account, because the money is paid out on a fixed schedule through an annuity.

Asset versus income: the distinction that trips people up

People confuse two separate questions. One is whether the payments are taxable income; the other is whether the settlement is an asset on your net worth.

They are not the same thing. The payments can be entirely tax-free and still represent a real asset worth six figures.

💡 Expert Note (CFA): The most common balance-sheet error here is recording the sum of every remaining check as the asset’s value. On a long-dated stream, that overstates net worth by tens of thousands and distorts every ratio a lender, planner, or court later calculates.

If you want context on the size of these streams, our breakdown of what a structured settlement actually pays out over its term walks through typical payout structures. To see how a steady income stream fits a long-range plan, you can model that income against your other retirement assets.

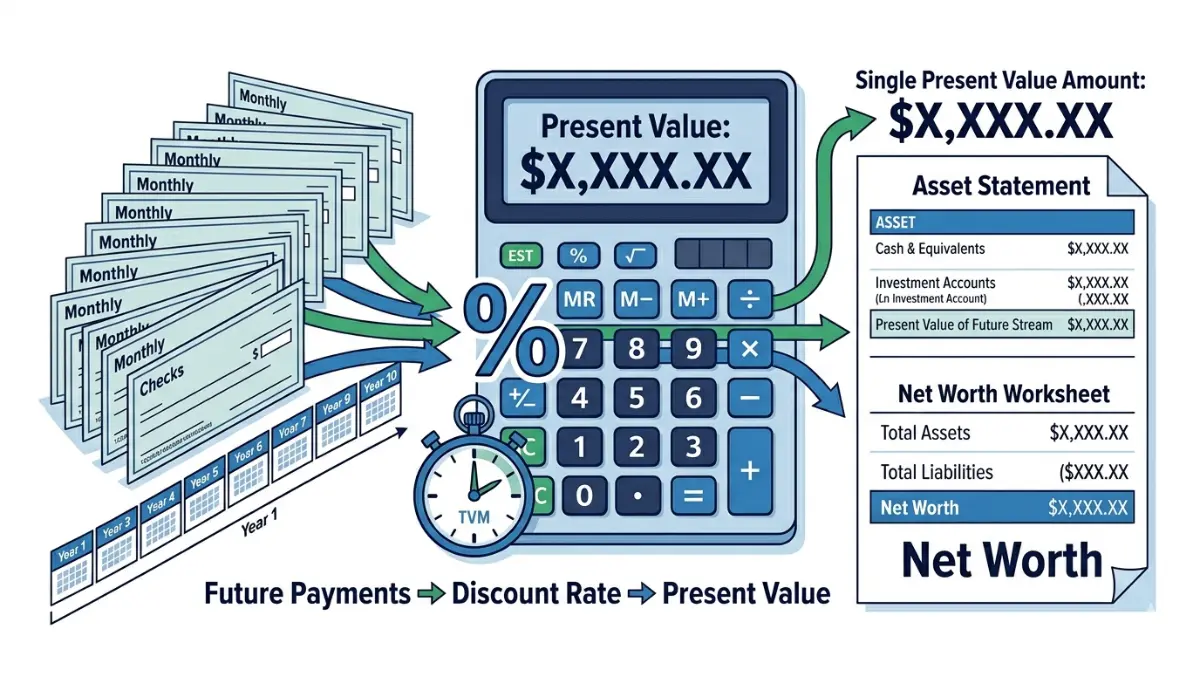

How to value your structured settlement for a net worth statement

Use the present value of an annuity — today’s worth of all your future payments, discounted for the time value of money.

Here is the method in four steps:

- List your remaining payment amount and how often it arrives (monthly, quarterly, or annually).

- Count the total number of payments left until the schedule ends.

- Choose a discount rate that reflects current rates of return — a conservative range in 2026 is roughly 3% to 6% for personal planning purposes.

- Apply the present-value formula, or use a calculator, to convert the stream into a single figure.

The discount rate is the lever that changes everything. A higher rate produces a lower present value, because future dollars are worth less today.

A worked example: face value versus present value

Consider a stream of $2,000 per month for 10 years. The numbers below are illustrative, using a 10% annual discount rate to show the gap.

| Metric | Amount |

|---|---|

| Face value (120 payments × $2,000) | $240,000 |

| Present value (10% annual discount rate) | ~$151,400 |

| Overstatement if you list face value | ~$88,600 |

Illustrative calculation; actual present value depends on your payment terms and the rate used.

Listing $240,000 instead of $151,400 would inflate your reported net worth by nearly $89,000.

Why the discount rate and inflation both matter

Fixed payments lose buying power every year that prices rise. A check that covers your costs today buys less a decade out.

You can see how inflation erodes a fixed payment over time using current CPI data, and our piece on present-value math for settlements goes deeper on rate selection. For the official inflation series behind these calculations, the Bureau of Labor Statistics CPI Inflation Calculator is the primary source.

When your settlement counts — and when it counts against you

Whether your settlement helps or hurts depends entirely on who is reviewing it. The same asset is treated three different ways.

On your own net-worth statement

Here it is a straightforward illiquid asset, entered at present value. It raises your net worth, but you cannot spend it on demand, so it should never be counted as an emergency reserve.

For a mortgage or loan

Lenders care less about the asset and more about the income. Steady settlement payments can support a debt-to-income ratio, but underwriters typically want proof the payments will continue for at least three more years.

You can estimate how a lender would weigh those monthly payments before you apply.

⚠️ Warning: Because the asset is illiquid, many lenders will not count it toward the cash reserves they require at closing. Confirm how a specific lender treats settlement income before you rely on it to qualify.

For SSI, Medicaid, and financial aid

This is the highest-stakes context. For means-tested benefits like SSI and Medicaid, settlement payments can count as income or as a countable resource — and that can reduce or eliminate eligibility.

Treatment varies by state, and the rules are unforgiving. A special needs trust is the standard tool families use to hold a settlement without losing benefit eligibility.

💡 Expert Note (CFA): Eligibility loss is the most expensive and most avoidable mistake in this entire topic. Anyone receiving needs-based benefits should map the settlement’s effect with a benefits or elder-law attorney before payments begin, not after a redetermination notice arrives.

For the state-specific picture, see how settlement payments affect Medicaid eligibility.

Are structured settlement payments taxable?

Usually not. Payments from a physical-injury or wrongful-death case are excluded from federal income tax under IRC Section 104(a)(2), whether you receive them as a lump sum or as periodic payments.

📊 Data Point: Federal law excludes damages received on account of personal physical injuries or physical sickness from gross income — IRC §104(a)(2). Source: Internal Revenue Service.

That exclusion is settled law, not a temporary rate, so it does not change your net-worth math. A tax-free asset is still an asset.

When part of a settlement is taxable

Not every dollar is exempt. Punitive damages, interest, and settlements that are not tied to physical injury — such as employment or discrimination claims — are generally taxable.

If your settlement mixes exempt and taxable elements, the allocation in the agreement controls the outcome. You can estimate the tax on any non-exempt portion and read more on which parts of a settlement are taxable.

The federal rules are laid out in the IRS guidance on the tax implications of settlements and judgments.

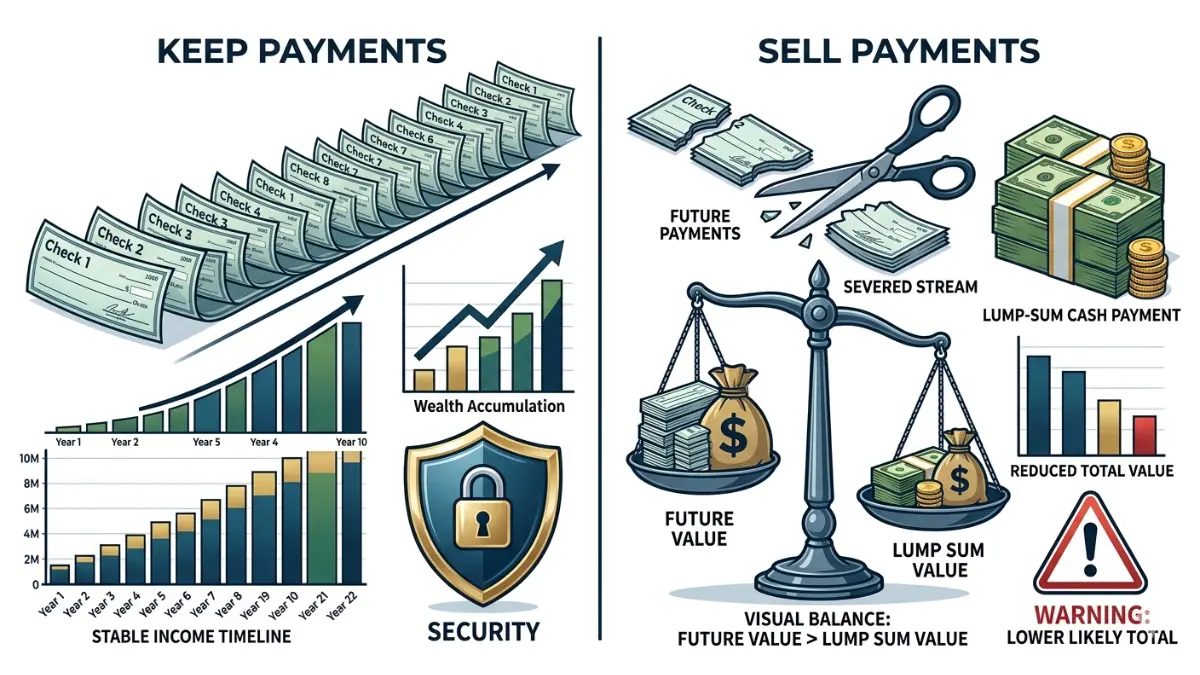

Cashing out: what selling does to your real net worth

Selling — also called factoring — converts your future payments into a lump sum today, and it almost always lowers your total wealth.

A buyer applies a discount rate to your remaining payments, and in 2026 that rate commonly runs from 9% to 20%. The higher the rate, the less cash you receive.

⚠️ Warning: A $50,000 stream of remaining payments might convert to only $40,000 to $45,500 in cash after the discount. You trade long-term value for short-term liquidity, and the decision is permanent.

Court approval and the rules that protect you

You cannot simply sign a form and cash out. Every state’s Structured Settlement Protection Act requires a judge to approve the transfer and confirm it serves your interest.

📊 Data Point: Federal law imposes a 40% excise tax on the purchase of structured-settlement payment rights without a court-approved qualified order — IRC §5891. Source: Internal Revenue Code.

These safeguards exist because the sector has a history of abuse. Regulators have penalized firms for misleading sellers, as shown in the CFPB’s enforcement action against Access Funding, and the agency’s guidance on trading future payments for a lump sum is worth reading before any offer.

Before selling, compare what a lump sum could earn if invested against keeping the payments, and review the full process of selling future payments.

The bottom line on your settlement and your net worth

Yes, your settlement is an asset — enter it at present value, never face value. And remember that “counts” means something different to you, to a lender, and to a benefits agency.

✅ Pro Tip: Within the next 48 hours, calculate the present value of your remaining payments and add a line to your net-worth statement labeled “structured settlement — illiquid.” That single edit gives you an accurate number for every form you face.

For decisions involving benefits eligibility, taxes, or a sale, the cost of getting it wrong far exceeds the cost of an hour with a licensed professional.

Structured settlement and net worth: frequently asked questions

1. Does a structured settlement count as income?

A structured settlement counts as income in some contexts but not all. Payments from physical-injury cases are not taxable income, yet lenders may treat them as qualifying income, and means-tested benefit programs may count them as income that affects your eligibility.

2. Is a structured settlement an asset?

Yes, a structured settlement is an asset and belongs on your net worth at the present value of your remaining payments. It is an illiquid asset, meaning you cannot access the full balance on demand, so it should not be treated as available cash or an emergency reserve.

3. How do I value my structured settlement for a net-worth statement?

Value your structured settlement using the present value of an annuity, not the sum of remaining checks. Take your payment amount, the number of payments left, and a reasonable discount rate, then convert the stream to one figure that reflects today’s dollars.

4. Do I report a structured settlement on a mortgage application?

Yes, report your structured settlement on a mortgage application. Lenders generally treat the payments as qualifying income for your debt-to-income ratio if you can document at least three years of continuation, though the illiquid asset itself may not count toward required cash reserves.

5. Does a structured settlement affect Medicaid or SSI eligibility?

A structured settlement can affect Medicaid or SSI eligibility because payments may count as income or a resource. Treatment varies by state, and exceeding program limits can reduce or end benefits. A special needs trust is the common tool used to preserve eligibility.

6. Are structured settlement payments taxable?

Most structured settlement payments are not taxable. Compensation for physical injury or wrongful death is excluded from federal income tax under IRC Section 104(a)(2). Punitive damages, interest, and non-injury settlements such as employment claims are generally taxable as ordinary income.

7. Can I cash out a structured settlement?

You can cash out a structured settlement by selling future payments to a factoring company for a lump sum. The sale is permanent and requires court approval under your state’s Structured Settlement Protection Act, and you receive less than the full value of the payments you give up.

8. How much will I lose if I sell my structured settlement?

When you sell a structured settlement, the buyer applies a discount rate that in 2026 commonly ranges from 9% to 20%. On a $50,000 stream of remaining payments, that can mean receiving roughly $40,000 to $45,500 in cash, losing thousands in total value.

9. Is a structured settlement part of my estate?

Yes, a structured settlement is part of your estate. Remaining guaranteed payments pass to your named beneficiary and are included in the value of your estate. If the estate exceeds the federal exemption, those assets may be subject to estate tax.

10. Does a structured settlement count in a divorce?

A structured settlement can count in a divorce depending on state law and when the claim arose. Courts examine whether the payments are marital or separate property, and the portion compensating for future losses is often treated differently from amounts already received.

11. Should I list face value or present value as my net worth?

List present value, not face value, as the structured settlement figure on your net worth. Face value sums every remaining payment and ignores the time value of money, overstating your true net worth — sometimes by tens of thousands of dollars on a long-dated stream.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.