How to Evaluate Your Structured Settlement Discount Rate

Structured settlement discount rates above 11% are negotiable in 2026. Most recipients don’t know where their offer stands — you should before responding.

In This Article

You got an offer. Here’s what that discount rate actually means.

A structured settlement buyer sent you paperwork, and somewhere inside it is the discount rate — the single figure that determines how much of your future payment stream’s total value you permanently surrender in exchange for a check today.

Most recipients sign without understanding what that percentage means in real dollars. That gap is exactly what buyers count on.

Why the discount rate is the most important number in your offer

The discount rate is not a processing fee or a line-item charge. It is the annual percentage the buyer applies to reduce the present value of every scheduled future payment down to the lump sum they are willing to pay.

One percentage point is not cosmetic. On a $120,000 payment stream, a single point can shift the offer by $4,000 to $6,000.

What this article will show you before you decide

Our pillar guide explains what structured settlements pay and how they work if you need the foundational structure first. Here, we focus on the offer: how to calculate your rate, how to benchmark it against 2026 market data, and what to do before you respond to any buyer.

ℹ️ Disclaimer: The structured settlement and discount rate information in this article is for educational purposes only. Structured settlement transfers are regulated financial transactions governed by state Structured Settlement Protection Acts, mandatory court approval requirements, and tax treatment determined by IRS rules specific to your individual settlement agreement. Consult a licensed Chartered Financial Analyst (CFA) or Certified Financial Planner (CFP) and a structured settlement attorney licensed in your state before accepting, negotiating, or rejecting any buyout offer.

What a structured settlement discount rate really is

A structured settlement discount rate is the annual percentage a factoring company applies to convert your future scheduled payments into a present-value lump sum offer. It represents the buyer’s effective annual return — built directly into the gap between what they pay you today and what they collect from your payment stream over time.

This is not the same as an interest rate on a loan. An interest rate measures your cost to borrow money; the discount rate measures what you permanently surrender to access money you are already owed.

Discount rate vs. interest rate: the difference that costs people money

When a buyer quotes a 10% discount rate, they earn 10% annually on the spread between the lump sum they hand you and the full value of your payment stream. You are not borrowing from them — you are selling them payments worth more than the check they are writing, with the rate controlling how far below market that check falls.

Your settlement functions on the same mathematical foundation as an annuity payment structure. Each future payment carries a distinct present value, and the discount rate controls how aggressively that value shrinks the further the payment falls from today.

Why the rate determines how much of your settlement’s value you keep

At a 9% discount rate, $15,000 per year for 8 years has a present value of approximately $83,000. At 14%, that same stream produces roughly $69,600 for the buyer — meaning they offer you that much less.

The $13,400 gap between those two numbers is not fees or taxes. It is entirely the financial cost of a higher rate, and you can model your own payment dates using the compound interest calculator before responding to any offer.

💡 Expert Note (CFA): The framing error I see most often is recipients mentally treating the discount rate as a flat cut — believing a 10% rate simply reduces $100,000 by $10,000. It does not work that way. The rate compounds annually against the present value of each individual payment. Payments due in years 6, 7, and 8 are discounted far more aggressively than near-term payments. This compounding structure is why a 5-percentage-point rate spread between two offers produces a dollar gap that consistently surprises clients when they see the math laid out.

How to calculate the discount rate on your offer

To calculate the effective annual discount rate on a structured settlement buyout offer, complete these four steps:

- Collect your complete payment schedule. Obtain every payment date and amount from your original settlement documents or the annuity issuer — not the buyer’s summary, which may omit or reorder payments.

- Get the net lump sum in writing. Request a formal written offer letter that shows the gross lump sum and all disclosed fees, so you are calculating the actual dollars reaching your account.

- Solve for the implied rate. Enter your payment amounts, payment dates, and net lump sum into a financial present value calculator or spreadsheet and solve for the internal rate of return. This is the effective annual discount rate the buyer is applying.

- Compare it to the 2026 benchmark. Take the rate you calculated and measure it against the market ranges in Section 5. That comparison tells you whether your offer is competitive, negotiable, or below market.

The investment calculator can help you model what your lump sum could grow to if invested at a competitive return — a useful comparison when weighing lump sum versus keeping your payments. For the time value calculation behind step three, the inflation calculator illustrates how purchasing power shifts over your payment term.

The four-step calculation: a worked example

| Input | Value |

|---|---|

| Annual payment amount | $15,000 |

| Payment term | 8 years |

| Total future payments | $120,000 |

| Buyer’s lump sum offer | $83,000 |

| Effective annual discount rate | ≈ 9.0% |

Calculation basis: Standard present value annuity formula — PV = PMT × [(1−(1+r)^−n) / r]. Solve for r using a financial calculator or spreadsheet.

Using the calculation to verify what your buyer told you

If the rate you calculate differs materially from the rate the buyer disclosed — or if the buyer did not disclose a specific rate — that is a red flag requiring a written clarification before any further conversation.

⚠️ Warning: Some factoring companies present an offer as a percentage of total payments rather than as an effective annual discount rate. These are not the same figure. A “20% discount” on $100,000 in total payments sounds like a flat $20,000 reduction — but the effective annual rate may be significantly higher or lower depending on the payment timeline. Always calculate the effective annual rate using your actual payment schedule before evaluating the offer.

Should you accept, negotiate, or walk away from the offer?

Before responding to any structured settlement buyer, answer three questions: What is the effective annual discount rate on this offer? Does that rate fall within the 2026 competitive range? Have you obtained at least one competing written offer from a different licensed buyer?

If any answer is “no,” you are not ready to respond yet. This framework tells you why.

Three questions to answer before you respond to any buyer

Path 1 — Offer rate is below 11%: The offer is in the competitive range for 2026. Consult a licensed financial advisor to confirm the lump sum serves your immediate need better than your remaining payment stream before signing.

Path 2 — Offer rate is between 11% and 14%: This is negotiable territory. Obtaining one or two competing written offers from other licensed buyers gives you direct leverage to request a lower rate — buyers facing competition routinely reduce their rate by 1 to 3 percentage points rather than lose the transaction.

Path 3 — Offer rate is above 14%: This is a below-market offer. Either reject it and request a revised offer with a disclosed methodology, or contact multiple competing buyers before responding. The full process of how to sell your structured settlement payments walks through what a properly structured competitive sale looks like.

💡 Expert Note (CFA): In my experience, the most financially damaging decision recipients make is responding to urgency. Buyers who set short offer expiration windows — “this offer expires in 72 hours” — are creating pressure to prevent you from doing exactly what protects you: getting competing quotes. No court in any state with a Structured Settlement Protection Act will close a transfer in 72 hours. The urgency is manufactured. The competing quote process takes 48 to 96 hours and frequently adds thousands of dollars to the offer you ultimately accept.

When to get competing quotes (and how to do it in 48 hours)

Contact at least three licensed factoring companies simultaneously. Provide each with the same complete payment schedule and request a formal written offer letter that includes the gross lump sum, the effective annual discount rate, and all disclosed transaction fees. Present the best written offer to your preferred buyer as a negotiating anchor.

A list of best-reviewed structured settlement companies with licensing and complaint history is a reliable starting point for building your comparison list. A fiduciary financial advisor can independently evaluate the offers you receive — the cost of that consultation is typically recovered many times over in the improved rate it produces.

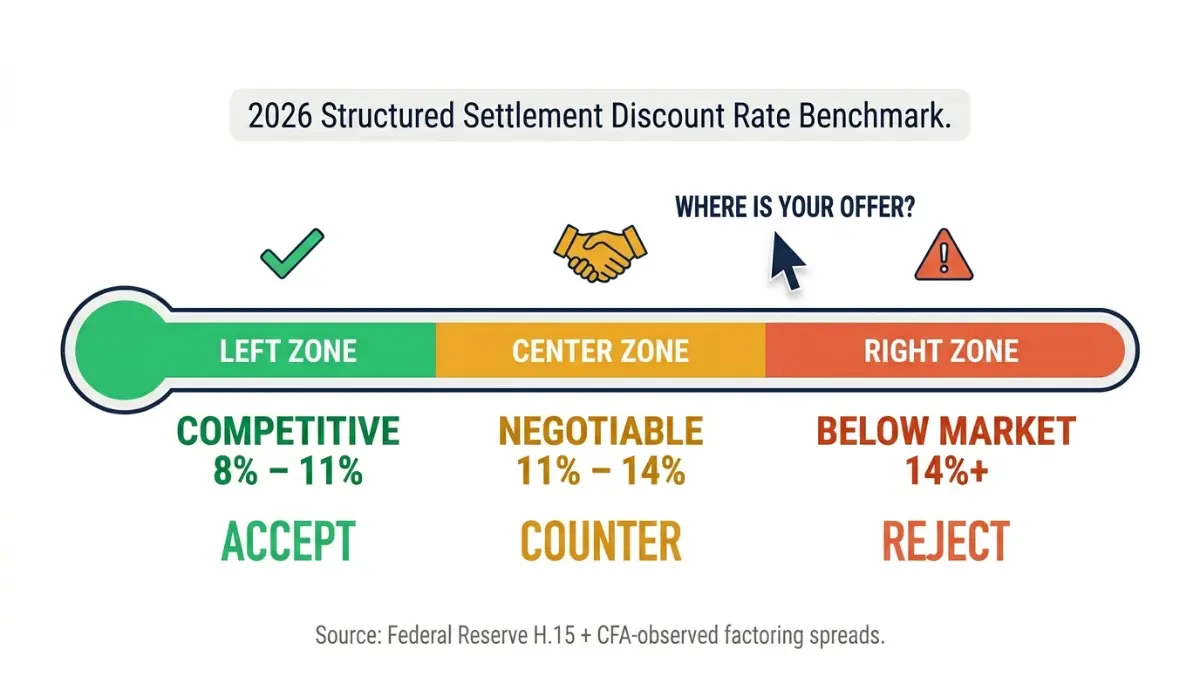

What structured settlement discount rates actually look like in 2026

In 2026, competitive structured settlement discount rates range from 8% to 11%, standard market offers fall between 11% and 14%, and any rate above 14% represents a below-market offer that warrants negotiation or rejection. These ranges are derived from CFA analysis of the Federal Reserve’s 2026 benchmark rate environment and reported factoring transaction spreads.

📊 Data Point: The Federal Reserve’s H.15 Selected Interest Rates release shows the 10-year Treasury yield averaging approximately 4.3% in Q1–Q2 2026. Structured settlement factoring companies in competitive transactions typically apply a spread of 4 to 7 percentage points above this benchmark, producing effective discount rates in the 8%–11% range for well-structured offers. — Source: Federal Reserve H.15 Selected Interest Rates, 2026. Verify current rates before using these figures in any specific offer evaluation.

The 2026 discount rate benchmark table: low, fair, and high offers

| Offer Tier | Effective Annual Discount Rate | What It Signals | Action |

|---|---|---|---|

| Competitive | 8% – 11% | Near-market pricing; buyer is within the fair range | Accept with attorney review |

| Standard / Negotiable | 11% – 14% | Above competitive; room to reduce rate with competing quotes | Request competing offers before responding |

| Below Market | 14%+ | Buyer applying excess spread above the Fed benchmark | Reject or counter with written competing offers |

Methodology: Rate tiers derived from Federal Reserve H.15 benchmark rate environment (Q1–Q2 2026) plus CFA-observed factoring transaction spreads. Individual offer terms vary by payment stream composition, remaining term, and the financial strength of the original annuity issuer. Always verify current Federal Reserve benchmark rates directly.

Why buyers charge above the Federal Reserve benchmark (and by how much)

A factoring company’s discount rate premium above the Treasury benchmark reflects four cost layers: their own cost of capital, regulatory compliance and legal costs, administrative expenses for the court process, and profit margin.

Of those four, profit margin is the one that negotiation directly compresses. Understanding the full cost of selling a structured settlement — including transaction fees that may sit outside the stated discount rate — gives you a complete picture of what you are actually paying to access your money. Use the APR calculator to convert any quoted rate into an annual percentage rate comparable to other financial products.

The real dollar cost of a high discount rate — before you sign

The dollar loss from accepting a high structured settlement discount rate does not feel abstract when you calculate it on your specific payment stream. On a $120,000 total stream, the difference between a competitive 9% offer and a below-market 14% offer is approximately $13,400 — money you surrender permanently at the moment you sign.

That gap compounds further on larger payment streams and longer remaining terms.

What a 3-point rate difference means over a $120,000 payment stream

| Scenario | Total Future Payments | Discount Rate | Lump Sum Received | Value Surrendered |

|---|---|---|---|---|

| Competitive offer | $120,000 | 9.0% | ~$83,000 | ~$37,000 |

| Below-market offer | $120,000 | 14.0% | ~$69,600 | ~$50,400 |

| Cost of high rate | — | — | ~$13,400 less | — |

Assumptions: $15,000 annual payment, 8-year term, standard present value annuity formula.

Alternatives worth considering before selling your full settlement

Before finalizing any sale, review our analysis of keeping your payments versus taking a lump sum — particularly if your immediate liquidity need is smaller than the full value of your settlement. A partial sale at a competitive discount rate is available from most licensed buyers and allows you to preserve the majority of your payment stream.

If you do take a lump sum at a competitive rate, running that amount through the savings calculator shows what it earns in a high-yield account over your original payment term — a useful reference point for comparing outcomes.

⚠️ Warning: Once a structured settlement transfer is court-approved and funded, the transaction is permanent. You cannot reverse the sale or reclaim future payments after funding. Any decision to sell — even a partial sale at a competitive rate — should be made with a full understanding of what you are surrendering on a dollar-for-dollar basis, not on a percentage-of-total-payments basis.

Your legal protections and the court approval process explained

Every state with a Structured Settlement Protection Act — currently 48 states — requires that a judge review and approve any structured settlement transfer before the buyer can legally close the transaction. This is not a formality. The court applies a best-interest standard and can reject a transfer it determines to be financially harmful to the recipient.

No licensed buyer can legally fund a purchase without this court order.

Why every state requires court approval before a sale can close

The mandatory court approval process exists precisely because the discount rate creates an information asymmetry that buyers can exploit. The court review is your structural protection against accepting a below-market offer under pressure — and you have the right to present competing offers to the presiding judge as evidence of market rate.

The CFPB’s consumer financial protection resources outline the disclosure requirements buyers must meet before any transfer agreement is signed. Before signing any purchase agreement, reviewing whether structured settlement payments are taxable under your specific settlement terms is also a required step — the tax treatment of your original payments and any lump sum proceeds are governed by IRS rules that vary by settlement type.

📊 Data Point: IRS Publication 4345 governs the tax treatment of structured settlement payments and their transfer. The publication clarifies the conditions under which periodic payment proceeds qualify for income exclusion and how lump sum transfers may be treated differently. — Source: IRS Publication 4345 — Settlements: Taxability, reviewed 2026. Consult a licensed tax professional for your specific settlement circumstances.

What the Structured Settlement Protection Acts mean for you

The Structured Settlement Protection Acts give you three practical rights: the right to time to seek competing quotes, the right to independent legal counsel before signing, and the right to have the court reject a transaction that does not serve your best interest.

The FINRA investor protection resources cover your options if a buyer engages in deceptive practices during the offer process. A structured settlement attorney licensed in your state can advise on the specific procedural requirements and timelines that apply to your court jurisdiction — this is the category of professional guidance that most directly protects the dollar value of your settlement.

Structured settlement discount rate: your questions answered

1. What is a structured settlement discount rate?

A structured settlement discount rate is the annual percentage a factoring company applies to convert your future scheduled payments into a lump sum offer. It functions as the buyer’s effective annual return on the gap between what they pay and what they collect. In 2026, competitive structured settlement discount rates range from 8% to 11% for most standard payment streams.

2. How do structured settlement companies calculate their offers?

Buyers apply their chosen discount rate to the present value of your future payment stream to arrive at a lump sum figure. A higher structured settlement discount rate produces a lower offer for you. On a $120,000 payment stream, the difference between a 9% and a 14% discount rate exceeds $13,000 in lump sum value.

3. What is a fair discount rate for a structured settlement in 2026?

Based on CFA analysis of the 2026 Federal Reserve rate environment, a fair structured settlement discount rate falls between 8% and 11%. Rates between 11% and 14% are negotiable with competing written offers. Any structured settlement discount rate above 14% signals a below-market offer that warrants rejection or a formal counter with competing quotes.

4. Why is the discount rate so high on structured settlement offers?

Buyers build their structured settlement discount rate from their own cost of capital, court-process compliance costs, and profit margin — then add a spread of 4 to 7 percentage points above the 2026 Federal Reserve benchmark. That spread is the buyer’s profit. It is compressible when you present competing written offers from other licensed factoring companies.

5. Can I negotiate the discount rate on my structured settlement?

Yes. The structured settlement discount rate in any offer is the buyer’s opening position, not a fixed number. Obtaining written competing offers from at least three licensed factoring companies is the most direct path to negotiating leverage. Buyers facing competition routinely reduce their rate by 1 to 3 percentage points rather than lose the transaction.

6. How much money will I lose by selling at a high discount rate?

On a $120,000 structured settlement payment stream, the difference between a competitive 9% discount rate and a below-market 14% rate is approximately $13,400 in lump sum value surrendered. That gap increases proportionally with larger payment streams and longer remaining terms. The dollar loss is permanent once the court-approved transfer is funded.

7. What is the difference between a discount rate and an interest rate?

An interest rate is what you pay to borrow money. A structured settlement discount rate is the effective annual return a buyer earns by paying you less than the full present value of your payment stream. Both use the time value of money, but the discount rate works against your payout rather than a borrowing cost.

8. Do I need court approval to sell my structured settlement?

Yes. Every state with a Structured Settlement Protection Act — currently 48 states — requires a judge to approve any structured settlement transfer before the buyer can legally fund the purchase. The court applies a best-interest standard and can reject a transaction. No licensed buyer can close a structured settlement transfer without a court order.

9. How long does it take to sell a structured settlement?

The full structured settlement discount rate transfer process — from signed application to funded lump sum — typically takes 45 to 90 days in most states. Court filing schedules, hearing availability, and the annuity issuer’s response time each affect total timeline. Buyers quoting timelines shorter than 30 days should be asked how they satisfy the mandatory court approval requirement.

10. What companies buy structured settlements?

The largest licensed structured settlement buyers in the United States include JG Wentworth, Peachtree Financial Solutions, SenecaOne, and Fairfield Funding, among others. Each company applies its own structured settlement discount rate methodology. Obtaining written competing offers from at least three licensed buyers is the most reliable way to identify the competitive market rate for your payment stream.

11. Is selling a structured settlement a good idea?

Selling makes financial sense only when the structured settlement discount rate is competitive and no better liquidity option exists. For most recipients, the cumulative value of keeping all scheduled payments exceeds any lump sum a buyer will offer at current 2026 rates. A licensed financial professional can model the true cost of selling before you commit.

12. What is the Structured Settlement Protection Act?

The Structured Settlement Protection Acts, enacted in 48 states, require court approval before any structured settlement transfer can close. A judge applies a best-interest standard to protect recipients from below-market discount rate offers. Federal law additionally imposes excise tax penalties on transfers completed without court review, giving recipients a meaningful legal protection during the sale process.

13. How do I get multiple quotes for my structured settlement?

Contact at least three licensed factoring companies simultaneously, providing each with your complete payment schedule. Request a formal written offer including the net lump sum, the effective annual structured settlement discount rate, and all disclosed transaction fees. Presenting competing written offers to your preferred buyer is the most direct mechanism for negotiating a lower discount rate.

14. What are typical structured settlement discount rates in 2026?

Based on CFA analysis of Federal Reserve H.15 benchmark data and current factoring market conditions, typical structured settlement discount rates in 2026 range from 8% to 11% for competitive buyers, 11% to 14% for standard market offers, and above 14% for below-market transactions. These figures are derived from the 2026 rate environment and individual terms will vary.

15. Can I sell only part of my structured settlement?

Most licensed structured settlement buyers will purchase a defined portion of your payment stream rather than all future payments. You can sell a specific number of payments, a date range, or a percentage of each scheduled payment. A partial sale at a competitive structured settlement discount rate provides immediate liquidity without permanently surrendering the full value of your settlement.

16. What happens after court approves my structured settlement sale?

After court approval, the buyer typically funds your lump sum within 3 to 10 business days. The court order is forwarded to the original annuity issuer, which redirects your structured settlement payments to the buyer going forward. You receive the net lump sum agreed upon at the court-approved discount rate, and the buyer collects the transferred payment stream.

17. Are structured settlement buyout payments taxable?

The original structured settlement payments you receive are generally excluded from gross income under Section 104 of the Internal Revenue Code. The tax treatment of lump sum proceeds from selling those payments depends on the specific structure of your original settlement agreement. A licensed tax professional or CPA can determine whether your transfer creates a taxable event under 2026 IRS rules.

What to do with your offer in the next 48 hours

You now have three things most structured settlement recipients do not have before they respond to a buyer: the math to calculate your discount rate, a 2026 benchmark range to evaluate it against, and a three-path decision framework that tells you whether to accept, negotiate, or walk away.

If your calculated discount rate falls above 11%, the next 48 hours have one priority: obtain competing written offers from at least two other licensed buyers before responding. The court approval process takes weeks regardless — the time cost of getting competing quotes is negligible, and the dollar recovery is not.

If your rate is below 11%, the decision is closer. A licensed financial advisor or structured settlement attorney can model the specific dollar trade-off between your lump sum and your remaining payment stream before you sign anything.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.