The Legal Reason Your Structured Settlement Loan Was Refused

Structured settlement loans aren’t loans — factoring companies charge 45% APR while quoting 13%. A CFA breaks down the legal block and the true cost.

In This Article

Why banks refuse structured settlement loans — and what to do instead

You described your structured settlement payments to a loan officer.

They declined — without a clear explanation.

You legally own those payments — so why can’t you borrow against them?

The answer has nothing to do with your credit score.

Structured settlement payments are encumbered by a specific legal mechanism that prevents them from functioning as conventional loan collateral — regardless of how large or reliable your payment stream is.

The term “structured settlement loan” is the wrong name

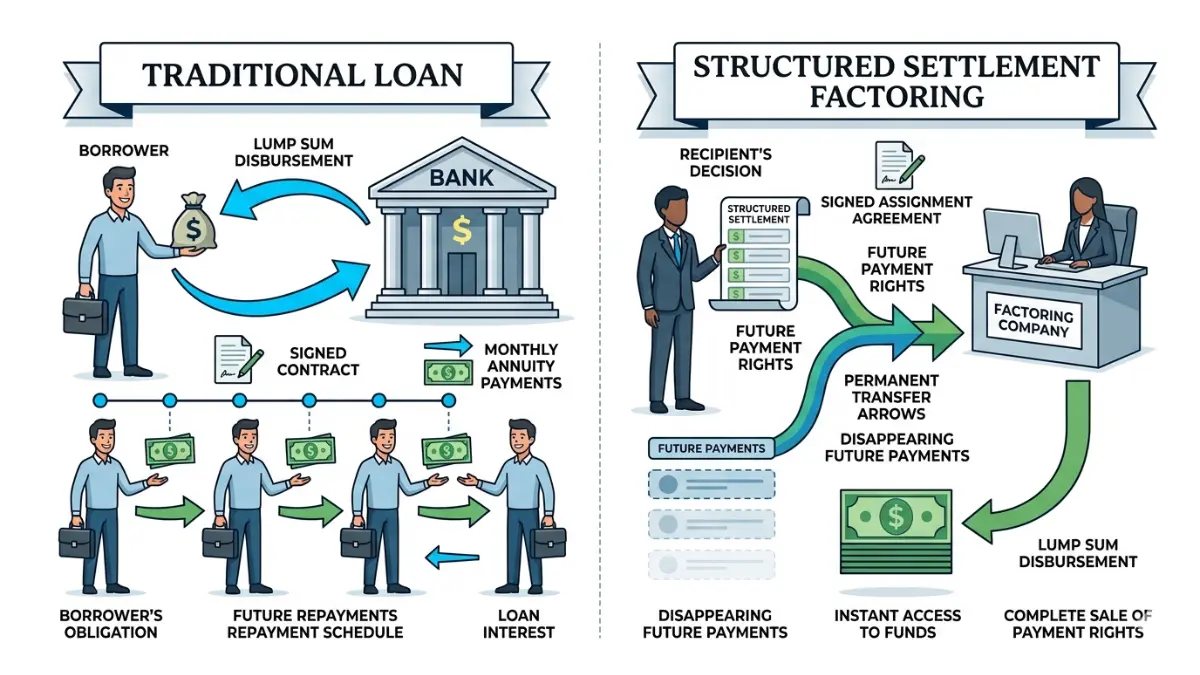

What the financial industry calls a structured settlement loan is not a loan in any legal sense.

It is a factoring arrangement — the permanent sale of future payment rights — and that distinction determines every financial and legal consequence you face before, during, and after the transaction.

This article explains the specific law banks cannot work around, what factoring truly costs when you apply real present-value math, and the decision framework a CFA with 28 years of capital markets experience applies with real clients.

Our full guide to structured settlement costs and what companies pay covers the complete payment landscape for recipients evaluating this decision.

ℹ️ Disclaimer: The lending and legal information in this article is provided for educational purposes only. Structured settlement factoring transactions are regulated under state-specific Structured Settlement Protection Acts and require mandatory court approval in most U.S. jurisdictions. All discount rates, effective APR ranges, and cost figures reflect 2026 market data and are illustrative — they do not constitute an offer, solicitation, or guarantee of terms. Tax treatment of structured settlement proceeds depends on the specific terms of the original settlement and IRS guidance, including Publication 4345. Consult a licensed structured settlement consultant, an independent attorney, and a credentialed financial professional — CFA, CFP, or CPA — before signing any transfer agreement.

Structured settlement “loan” vs. factoring — the distinction that changes everything

A structured settlement “loan” is not a loan — it is a factoring transaction in which a recipient permanently transfers the legal right to future periodic payments to a third-party company in exchange for an immediate lump sum.

There is no repayment schedule.

There is no outstanding debt.

The payment rights are permanently gone.

Why the word “loan” is legally wrong — and what that costs you

Factoring companies use the word “loan” because it feels familiar and lower-stakes.

The problem: it obscures the fact that you are selling a permanent asset, not borrowing against it — and the financial consequences of that confusion are severe.

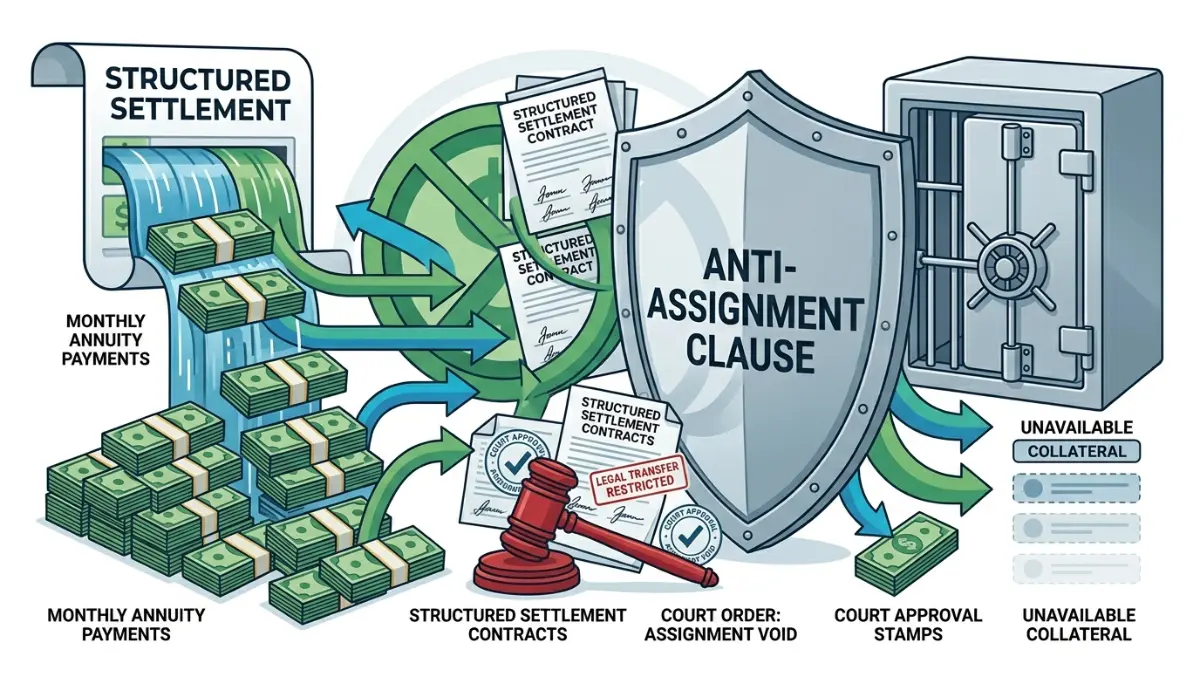

How the qualified assignment creates the legal wall banks can’t cross

When your settlement was established, a qualified assignment transferred the legal obligation to make your payments from the defendant to an annuity issuer under IRC Section 130.

That structure formally separates you from the underlying payment stream — you receive the payments, but you do not hold the underlying asset as collateralizable property.

Understanding how annuity payment streams are structured clarifies why conventional collateral rules produce a different result here than with any other income source.

Before treating a factoring offer as equivalent to a loan, review our structured settlement vs. lump sum comparison — the long-term financial trade-off is typically more significant than the immediate cash gap.

Why banks refuse structured settlement loans: the legal mechanism

Banks do not decline structured settlement applications because the payments are unreliable.

They decline because the anti-assignment clause makes the payment stream legally unavailable as collateral — a distinction most loan officers do not take the time to explain.

The anti-assignment clause: why your payments cannot be pledged as collateral

An anti-assignment clause is embedded in virtually every structured settlement agreement.

It legally prohibits the recipient from assigning, transferring, or pledging future payment rights to any third party without prior court approval — a process no conventional bank underwriting model can accommodate.

⚠️ Warning: If a bank tells you they “just don’t do these loans,” that answer is incomplete. The more accurate reason is that your settlement agreement legally prevents the payment stream from serving as collateral until a court approves a transfer — and that process eliminates banks from the equation entirely.

How the SSPA removed conventional lenders from the equation

The Structured Settlement Protection Act (SSPA), adopted in 49 states as of 2026, codified the court-approval requirement into state law.

Any transfer of structured settlement payment rights — including any attempt to use them as collateral — requires a judge to review and approve the transaction before it becomes legally effective.

📊 Data Point: As of 2026, 49 U.S. states have enacted a version of the Structured Settlement Protection Act, requiring prior court approval for any transfer of structured settlement payment rights — Source: National Structured Settlements Trade Association (NSSTA), 2026 State Law Compliance Summary.

Before engaging any factoring company, review what the structured settlement payment transfer process actually involves and the risks recipients most commonly overlook.

The CFPB’s consumer tools and resources include guidance on structured payment transfers and your rights as a consumer before you engage any third party.

💡 Expert Note (CFA): In my 28 years of portfolio work, I’ve reviewed structured settlement transfer offers with clients who were blindsided when their bank said no. The mechanism is identical every time: the anti-assignment clause made the payment stream legally non-collateralizable — and no bank credit committee can override a contract provision baked into the original settlement agreement.

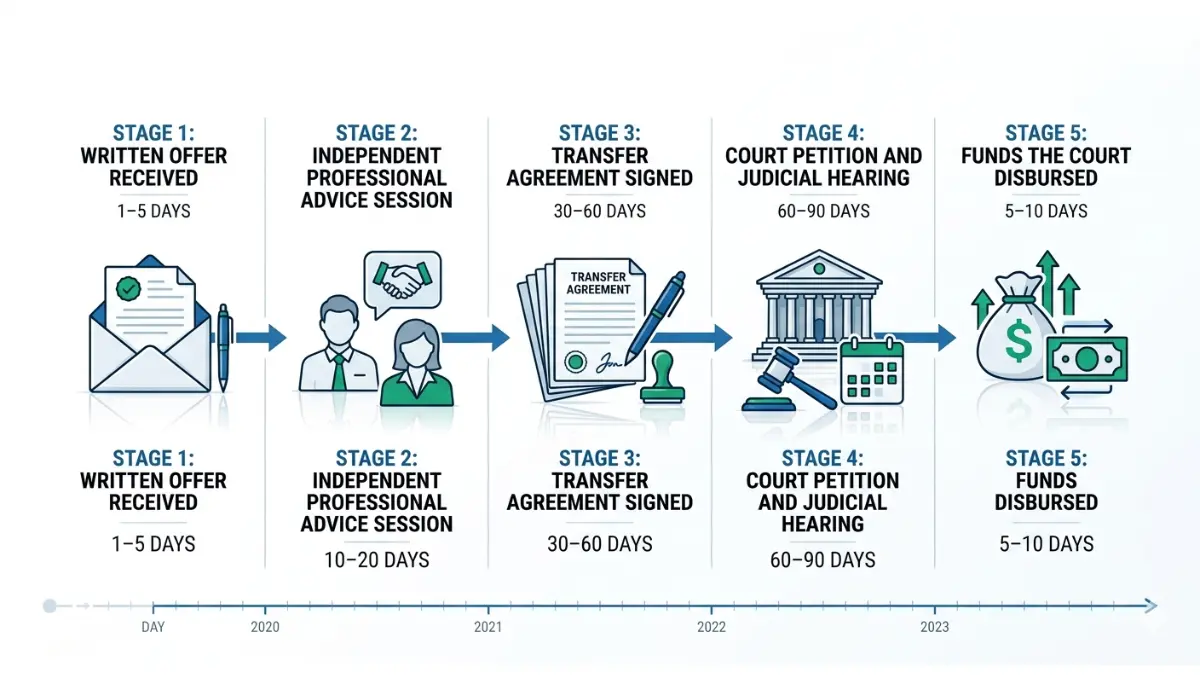

How structured settlement factoring actually works — step by step

The complete structured settlement factoring process takes a minimum of 45–90 days in most states — not the “quick cash” timeline factoring company marketing materials typically suggest.

From first inquiry to funded: the five stages every transfer goes through

- Written offer received — Factoring company delivers a written lump-sum offer specifying payment stream, quoted discount rate, and transfer terms. (1–5 business days)

- Independent Professional Advice (IPA) session — Most states legally require the recipient to receive independent financial or legal advice before signing. (5–10 business days)

- Transfer agreement signed — Recipient reviews and executes the transfer agreement only after the IPA session is documented. (3–7 business days)

- Court petition filed and hearing scheduled — The factoring company files the SSPA petition; the court sets a hearing date. (30–60 days in most states)

- Funds disbursed — After the court issues its written approval order, the lump-sum payment is released. (3–10 business days)

The court approval hearing: what judges actually evaluate

A court approval hearing is not a formality.

Judges applying the SSPA “best interest” standard review whether genuine financial hardship exists, whether the recipient considered alternatives, whether dependents are affected, and whether the quoted discount rate falls within a reasonable market range.

💡 Expert Note (CFA): The IPA requirement exists because factoring companies use urgency to close deals before recipients fully understand what they are giving up. A client once came to me after signing a transfer agreement without completing the required IPA session — the court rejection that followed was the best outcome available to her at that point.

Our detailed breakdown of what the structured settlement court approval process requires covers every stage of the judicial review in plain language.

What structured settlement factoring really costs: discount rate vs. true APR

Factoring companies in 2026 quote discount rates in the range of 9–18% — but a discount rate and an effective APR are not the same calculation, and the gap between them is where recipients lose the most money.

Discount rate vs. effective APR: why these numbers are not interchangeable

A discount rate reduces the stated present value of your payment stream by a percentage.

An effective APR expresses that same cost as an annualized rate — the only number that makes a valid comparison to any other borrowing option.

| Quoted Discount Rate | Effective APR Equivalent | Lost Value on $50,000 PV |

|---|---|---|

| 9% | ~28–32% APR | ~$14,000–$16,000 |

| 13% | ~42–48% APR | ~$21,000–$24,000 |

| 18% | ~58–65% APR | ~$29,000–$32,500 |

Illustrative calculations based on 2026 NSSTA market rate range. Actual costs vary by offer terms.

📊 Data Point: Factoring company discount rates in 2026 range from 9% to 18% of the present value of transferred payments — Source: National Structured Settlements Trade Association (NSSTA), 2026 Market Rate Survey. Recipients should request the effective APR equivalent before evaluating any offer.

A worked example: what a 13% discount rate actually costs

Assume your settlement pays $600 per month for 15 years — a present value of approximately $82,000 at a 5% discount rate.

A factoring company offers $60,000, quoting a “13% discount rate.”

The actual loss is $22,000 of present-value dollars — and when annualized over the remaining payment term using standard present-value mechanics, the effective APR on that transaction exceeds 45%.

Use our APR calculator to convert any factoring offer’s discount rate into its true annualized cost before comparing it to any alternative borrowing option.

⚠️ Warning: FINRA’s investor alerts on high-cost financial transactions specifically flag the gap between quoted rates and true annualized costs in structured payment sale agreements. Review the alert before accepting any offer.

The full analysis of what it costs to sell structured settlement payments breaks down every fee recipients typically discover only after signing.

For the foundational mechanics behind discount rate calculations, our structured settlement discount rate guide works through the math from first principles.

💡 Expert Note (CFA): The single most important number in any factoring offer is the effective APR — not the discount rate. In 28 years of advising clients on capital allocation decisions, I have never seen a factoring company volunteer that figure unprompted. You have to calculate it yourself, or work with a credentialed professional who will do it for you.

The Structured Settlement Protection Act: what the law requires

The Structured Settlement Protection Act (SSPA), adopted in some form by 49 states as of 2026, requires that any transfer of structured settlement payment rights receive prior court approval based on a judicial finding that the transfer is in the recipient’s best interest.

No court order means no valid transfer — in most states, a transfer that bypasses court approval is legally void.

What the SSPA requires — and what voids a transfer if the company skips it

A compliant SSPA transfer must include all of the following:

- Written offer delivered at least three business days before signing

- Independent Professional Advice session from an advisor not recommended by the factoring company

- Court petition filed by the factoring company, not the recipient

- Judicial hearing in which the “best interest” standard is applied

- Written court order issued before any funds change hands

⚠️ Warning: If a factoring company pressures you to sign before the IPA session is complete or suggests the court process can be shortened or skipped, terminate the conversation. Non-compliant transfers are void in most states — and the legal harm to the recipient typically outlasts the transaction itself.

IRS treatment of structured settlement transfer proceeds in 2026

Original structured settlement payments received for physical injury are excluded from gross income under IRC Section 104.

The lump sum received from a factoring sale may not carry the same exclusion — the IRS treatment depends on the nature of the underlying claims in the original settlement.

📊 Data Point: IRS Publication 4345’s treatment of structured settlement proceeds governs taxability of both original payments and any amounts received in connection with a transfer. Recipients should confirm the tax treatment of their specific settlement type with a CPA before completing any transaction — Source: IRS Publication 4345, Settlements — Taxability, 2026 edition.

Whether the transfer proceeds are taxable materially affects the net value of any offer — our guide to when structured settlement payments become taxable covers the key thresholds and exceptions.

Use our income tax calculator to estimate how a taxable lump-sum receipt would affect your 2026 tax liability before accepting any factoring offer.

Should you pursue a structured settlement transfer? A CFA’s honest framework

Before signing any transfer agreement, apply three questions.

One: Have you genuinely exhausted every lower-cost borrowing option — personal loan, home equity line, debt consolidation, or a negotiated payment plan with your creditor?

Two: Have you calculated the effective APR of the specific offer in front of you — not just the discount rate the company quoted?

Three: Has an independent attorney reviewed the transfer agreement — not one the factoring company suggested?

If the answer to any of these is no, you are not ready to sign.

Three questions to ask before signing any transfer agreement

The factoring decision is not primarily a cost question — it is an irreversibility question.

Once a court order is issued and funds are disbursed, the transferred payment rights are permanently gone.

Your next step based on where you are in the process

If you have not compared personal loan rates to the effective APR of your factoring offer, start there — our 2026 personal loan rates and comparison guide shows current market rates for recipients with a range of credit profiles.

Use our debt consolidation calculator to model whether consolidating existing debt eliminates the cash need without touching your payment stream.

The CFPB’s financial well-being assessment tools can help you identify the actual source of the cash pressure before committing to an irreversible transaction.

💡 Expert Note (CFA): In my experience working with clients facing this decision, the ones who fared best treated the structured settlement transfer as an option of absolute last resort — not a first response to short-term cash pressure. The 45–65% effective APR range on most 2026 factoring offers represents one of the highest costs of capital available to a private individual outside of unsecured payday lending.

Frequently asked questions about structured settlement loans

1. Can you actually get a loan against a structured settlement?

No traditional loan product exists for structured settlements. What factoring companies offer is a purchase of your payment rights — not a lending arrangement. Since structured settlement payments are protected by anti-assignment clauses and the Structured Settlement Protection Act in 49 states as of 2026, conventional banks cannot lend against them. Consult a licensed structured settlement consultant before proceeding.

2. Why exactly won’t banks loan against structured settlements?

Banks refuse because the anti-assignment clause in virtually every structured settlement agreement legally prohibits pledging future payment rights as collateral without prior court approval. No conventional underwriting model accommodates a court-contingent collateral process. As of 2026, the Structured Settlement Protection Act in 49 states reinforces this barrier. Consult a licensed financial professional to explore your alternatives.

3. What is the difference between a structured settlement loan and selling your payments?

A structured settlement “loan” is technically a permanent sale — not a borrowing arrangement. The recipient transfers the legal right to future payments to a factoring company in exchange for a lump sum. There is no repayment obligation, but the structured settlement payment stream is permanently transferred. Consult a licensed structured settlement consultant before signing any transfer agreement.

4. How much does it cost to cash out a structured settlement?

Factoring companies quote discount rates of 9–18% as of 2026, but the true effective APR typically ranges from 28–65%. On a structured settlement with a $50,000 present value, a 13% discount rate translates to approximately $21,000–$24,000 in lost value. Consult a licensed financial professional to calculate the full effective APR before accepting any offer.

5. Is a structured settlement transfer legal?

Yes — structured settlement transfers are legal when they comply with state law. The Structured Settlement Protection Act, enacted in 49 states as of 2026, requires prior court approval and a judicial finding that the transfer serves the recipient’s best interest. Bypassing court approval makes the transfer void in most states. Consult a licensed structured settlement attorney before proceeding.

6. What is the Structured Settlement Protection Act?

The Structured Settlement Protection Act (SSPA) is a state statute requiring court approval before any structured settlement payment rights can be transferred. Adopted in 49 states as of 2026, it mandates that a judge find the transfer is in the recipient’s best interest before it takes legal effect. Consult a licensed attorney to review your state’s specific SSPA requirements.

7. How long does it take to get money from a structured settlement?

The complete process takes a minimum of 45–90 days in most states as of 2026. Required stages include a written offer, an Independent Professional Advice session, a signed transfer agreement, a court petition, and a judicial hearing. The court approval stage alone typically takes 30–60 days. Consult a licensed structured settlement consultant for your state’s specific timeline.

8. Can a structured settlement be used as collateral for a bank loan?

No. The anti-assignment clause in your agreement legally prohibits pledging future structured settlement payments as collateral. The Structured Settlement Protection Act, enacted in 49 states as of 2026, reinforces this barrier by requiring court approval for any payment rights transfer. No conventional bank underwrites a court-contingent collateral process. Consult a licensed financial professional to explore alternative secured financing.

9. What are the best alternatives to cashing out a structured settlement?

Before factoring a structured settlement, recipients should evaluate personal loans, home equity lines of credit, debt consolidation, and negotiated payment arrangements with creditors. In 2026, personal loan APRs are typically well below the 28–65% effective cost range of most structured settlement factoring offers. Consult a licensed CFP or financial advisor to compare the total cost of each option.

10. Are structured settlement transfer proceeds taxable?

Original structured settlement payments from physical injury cases are excluded from gross income under IRC Section 104. Proceeds received in a factoring transaction may be treated differently depending on the nature of the original settlement claims. IRS Publication 4345, updated for 2026, governs this treatment specifically. Consult a licensed CPA or tax professional before completing any structured settlement transfer.

11. What happens to your payments after you sell them to a factoring company?

Once court-approved, the factoring company permanently acquires the legal right to receive the transferred structured settlement payments directly from the annuity issuer. The original recipient receives the agreed lump sum and loses all rights to those future payments. The transfer is irrevocable after the court order is issued. Consult a licensed structured settlement consultant before agreeing to any transfer.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.