How a Structured Settlement Broker Gets Paid and by Whom

Structured settlement brokers earn 3%–5% on every annuity — and the insurer pays all of it. Here’s who the broker actually works for.

In This Article

What is a structured settlement broker?

A structured settlement broker is a licensed insurance professional who designs the annuity that converts a personal injury settlement into guaranteed, tax-free periodic payments — and is compensated by the annuity-issuing life insurance company, not the plaintiff.

That single fact resolves the most common question plaintiffs carry into the settlement process.

The role no one explains at the settlement table

When a personal injury lawsuit settles, the defendant’s insurer engages a broker to design a payment plan — funded by an annuity from a rated life insurance carrier — that replaces a single payout with a long-term income stream.

The plaintiff receives tax-free payments over time, the defendant closes its liability exposure, and the broker manages the transaction between all parties.

For the full framework the broker operates within, how structured settlements work explains the complete sequence from offer to first payment.

Why this distinction matters for your financial outcome

The broker is engaged by the defendant’s insurer — not by the plaintiff.

NSSTA 2026 professional standards require the annuity structure to reflect the plaintiff’s documented financial needs, but the broker’s commercial relationship runs entirely to the insurer’s side of the table.

That distinction shapes whether the proposed payment schedule genuinely serves your long-term financial security or simply closes the defendant’s books.

ℹ️ Disclaimer: The structured settlement and insurance intermediary information in this article is intended for educational purposes only. Structured settlement brokers are licensed insurance producers regulated at the state level under individual state insurance codes; compensation structures, annuity pricing terms, and qualified assignment mechanics vary by carrier, case type, and state of jurisdiction as of 2026.

Any decision to accept or reject a structured settlement offer — or to respond to a factoring company solicitation — should be made in consultation with a licensed financial professional, a licensed personal injury attorney, and, where applicable, an independent settlement planner whose compensation is not tied to any annuity placement.

What a structured settlement broker actually does

The broker’s work covers three functions: designing the payment schedule, selecting the annuity issuer, and coordinating the qualified assignment that permanently transfers payment responsibility from the defendant to the life insurance carrier.

Each function shapes the financial outcome a plaintiff will live with for years — or decades.

Designing the payment schedule around your financial needs

The broker builds a payment timeline around documented plaintiff needs — medical care costs, income replacement, education milestones, or retirement timing.

Periodic payments can be structured as monthly income, deferred lump sums at defined future dates, or a hybrid of both. An investment return comparison tool can model how different structured schedules perform against a lump-sum alternative over time. For a deeper look at how annuity products are designed and administered, the annuity fundamentals guide covers the product mechanics in full.

Selecting the annuity issuer — and why carrier ratings matter

The broker selects the rated life insurance company that will fund and administer the annuity.

Carrier financial strength determines whether those payments arrive reliably in year 15, year 20, or year 30 — this is not an interchangeable decision. NSSTA 2026 member standards require disclosure of the selected carrier’s AM Best rating in every placement recommendation.

Do you need a broker, or can you negotiate directly?

The defendant’s insurer engages the broker — the plaintiff cannot hire or replace them.

A plaintiff can, however, retain an independent fee-only financial planner to review the proposed structure before signing, a decision analyzed directly in this structured settlement vs. lump sum comparison.

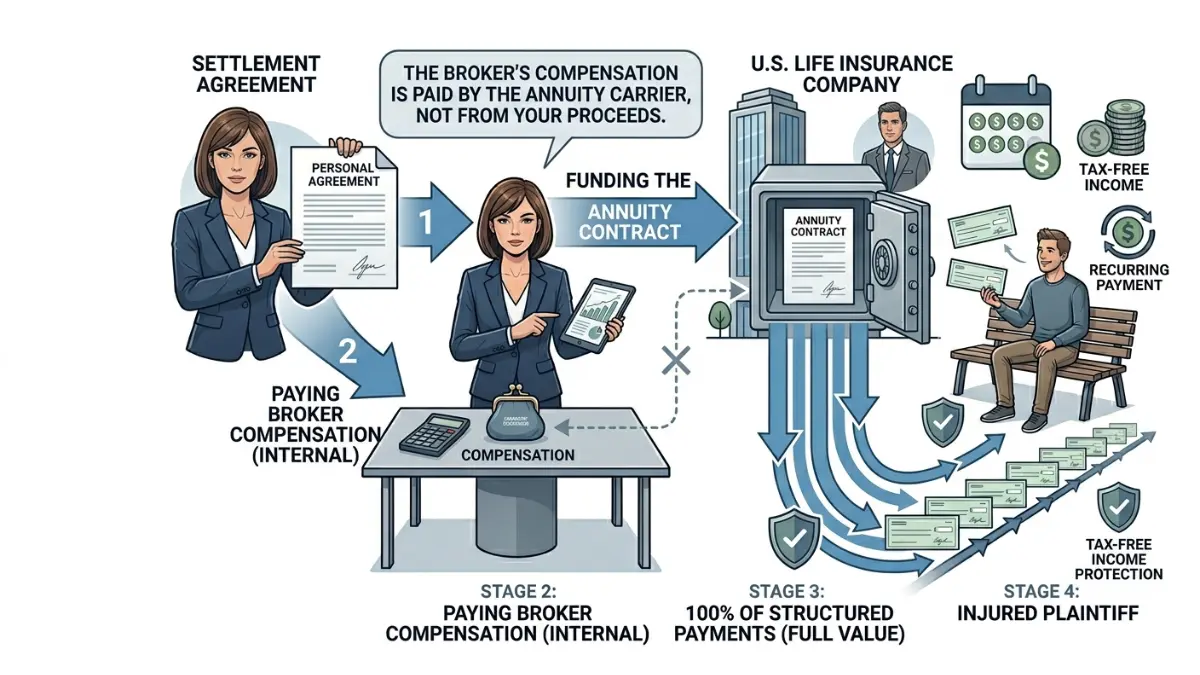

Who pays a structured settlement broker — and how much?

The annuity-issuing life insurance company pays the structured settlement broker — not the plaintiff. The commission is built into the annuity’s actuarial pricing at the time of purchase and never appears as a deduction from the plaintiff’s settlement amount.

No invoice reaches the plaintiff. No fee is subtracted from the award.

The insurer pays — not you: how the commission works

When the defendant’s insurer purchases the annuity, the life insurance carrier embeds the broker’s commission in the actuarial pricing — the same distribution mechanism governing all life insurance products.

The commission is structurally invisible to the plaintiff: fully absorbed by the carrier, priced into the premium, and never subtracted from proceeds.

💡 Expert Note (CFA): In 28 years of institutional annuity work and litigation finance transactions, the most consistent misconception I encounter is that the broker’s commission reduces the plaintiff’s recovery. It does not. The defendant’s insurer budgets the annuity premium; the carrier prices the broker’s commission into that premium — it is never carved from the plaintiff’s settlement figure.

What commission rates look like in 2026

📊 Data Point: Structured settlement broker commissions typically range from 3% to 5% of the annuity premium, paid by the issuing life insurance carrier. On a $500,000 annuity, that equals approximately $15,000–$25,000. On a $1,000,000 placement, the range is approximately $30,000–$50,000. Commission is embedded in carrier pricing and not separately invoiced. — Source: NSSTA 2026 member disclosure standards.

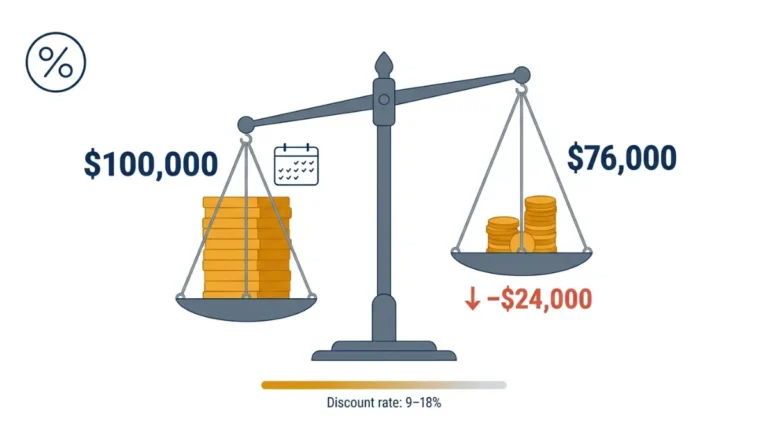

For the underlying pricing mechanics that interact with commission economics, the structured settlement discount rate guide explains how the annuity’s present-value calculation is constructed — and where long-term payment value is determined.

The one compensation question every plaintiff should ask

The CFPB’s structured settlement consumer guidance recommends requesting written broker compensation disclosure before any structure is finalized.

Any broker operating under 2026 NSSTA member standards must provide that disclosure on request — it is the professional minimum a plaintiff should expect before signing.

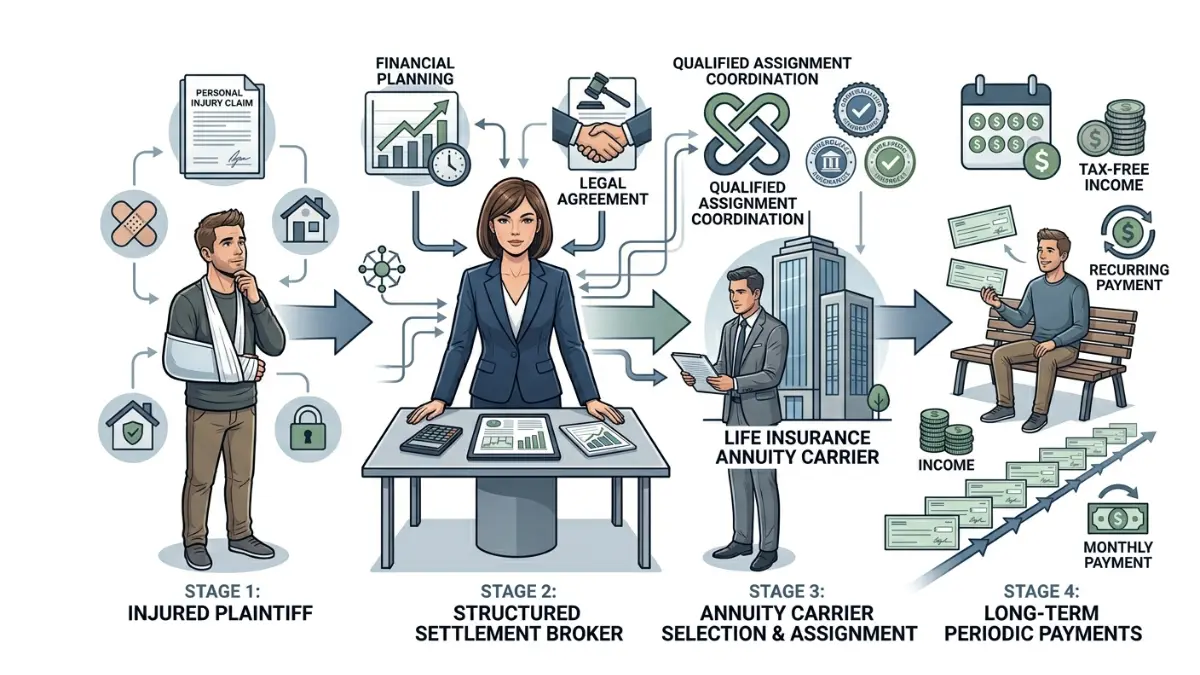

How the structured settlement process works, step by step

A structured settlement moves through six defined stages from agreement to first annuity payment — and the broker enters at stage two, not stage one.

Knowing this sequence tells a plaintiff exactly when their participation is required and what each document legally commits them to.

From settlement offer to qualified assignment: the 6 stages

- Settlement amount negotiated. The plaintiff’s attorney and defendant’s insurer agree on the total settlement value. The broker is not yet involved.

- Defendant engages the broker. The insurer retains a licensed structured settlement broker to design the annuity payment structure.

- Broker designs the annuity schedule. The broker proposes a payment plan — monthly income, lump-sum milestones, or a hybrid — matched to the plaintiff’s documented financial needs.

- Qualified assignment executed. Under IRC Section 130, the defendant assigns future payment obligations to a third-party qualified assignee — typically a life insurance affiliate — permanently releasing the defendant from liability.

- Annuity purchased and issued. The qualified assignee purchases an annuity from the selected rated carrier. That carrier, not the defendant, becomes solely responsible for all future payments.

- Plaintiff receives periodic payments. Payments begin per the agreed schedule, excluded from federal gross income under IRC Section 104(a)(2).

✅ Pro Tip: Between stages 4 and 5, ask the broker to confirm the carrier’s AM Best rating in writing. This is the last practical point in the process at which a carrier substitution can be requested.

What is a qualified assignment, and why does it protect you?

The qualified assignment under IRS Publication 4345 on settlement taxability does two things simultaneously: it releases the defendant from all future payment liability, and it preserves the plaintiff’s federal tax exclusion under IRC Section 104(a)(2).

Once executed, the assignment is irrevocable — the annuity issuer, not the defendant, becomes permanently responsible for every future payment.

The full tax framework governing periodic payment treatment is covered in the structured settlement payment tax rules guide.

How long does the process take in 2026?

Standard personal injury structured settlements take 45 to 90 days from the agreement date to the first annuity payment.

Cases involving minors, multi-party structures, or court-approval requirements typically run longer. An inflation-adjusted value calculator helps plaintiffs assess how the real purchasing power of fixed payments changes over a long payment horizon; a compound interest modeling tool can then compare that against a lump-sum investment scenario.

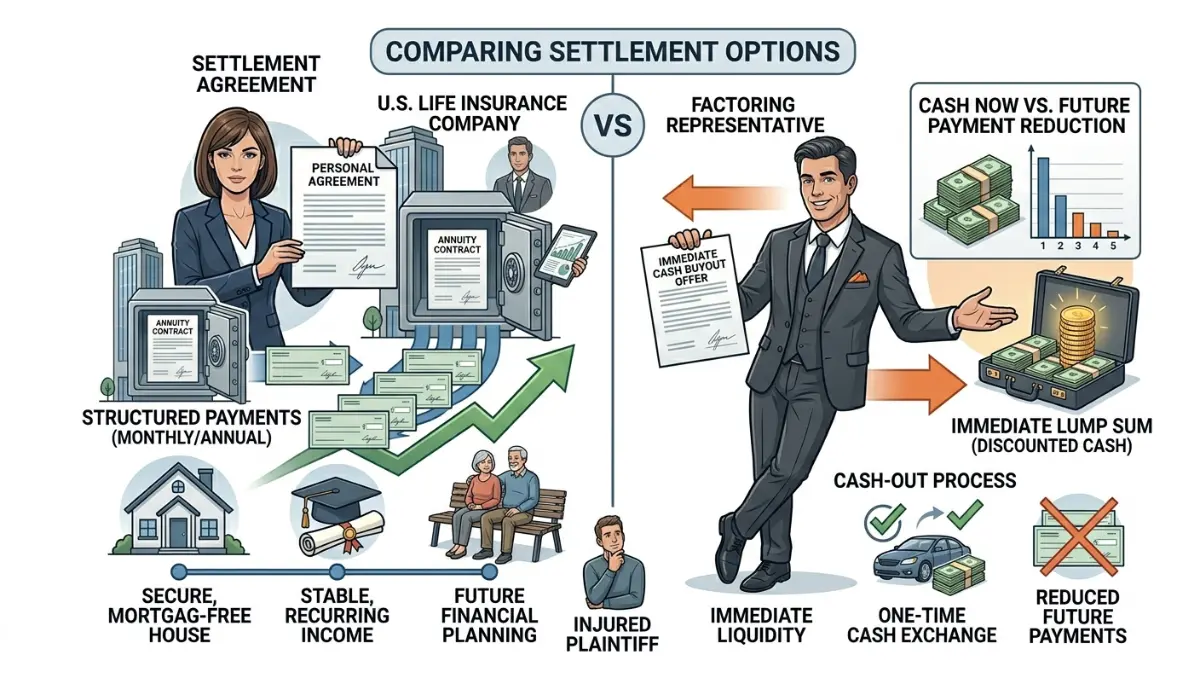

Structured settlement broker vs. factoring company: key differences

A structured settlement broker arranges the original annuity at the time of settlement. A factoring company — a separate entity entirely — later solicits the plaintiff to purchase those future payments for immediate cash, at a steep discount.

These are not the same transaction, the same party, or the same financial incentive.

What a factoring company actually offers — and what it costs

| Structured Settlement Broker | Factoring Company | |

|---|---|---|

| When They Enter | At settlement, before annuity is issued | After settlement — months or years later |

| Who They Represent | Defendant’s insurer (at placement) | Their own capital investors |

| How They Are Paid | Commission embedded in carrier pricing | Discount margin on the purchased payment stream |

| Impact on Plaintiff’s Payments | Designs the payment schedule | Eliminates part or all future payments permanently |

| Legal Oversight | State insurance licensing; NSSTA standards | Court approval required in all 50 states under SSPA |

| Tax Consequence | IRC 104(a)(2) exclusion preserved | IRC 104(a)(2) exclusion lost on all sold payments |

| Best For | Plaintiffs at time of original settlement | Rarely optimal — see excise tax note below |

⚠️ Warning: Factoring solicitations frequently arrive by mail or phone shortly after a settlement is finalized, targeting plaintiffs with urgent cash needs. Before responding to any buyout offer, review the consumer protections and disclosure requirements detailed in the CFPB’s guidance on structured settlement factoring transactions.

The 26 USC 5891 excise tax: who pays and what it means for you

Federal law imposes a 40% excise tax on structured settlement factoring transactions under 26 USC 5891 when the transaction falls outside court-approval safe-harbor requirements.

This tax is technically levied on the factoring company — but the economic cost is routinely passed through to the plaintiff in the form of a lower buyout price. A factoring company offering $180,000 for a $300,000 payment stream may be pricing that federal tax exposure directly into the discount.

For the full financial and legal mechanics of any potential sale, the true cost of selling structured settlement payments and the structured settlement court-approval process guide provide the detail every plaintiff should review before responding to any solicitation.

How structured settlement brokers are licensed and regulated

Structured settlement brokers are licensed insurance producers regulated at the state level — not under SEC or FINRA authority.

Each state’s insurance commissioner governs licensing requirements, renewal, and professional conduct. The NSSTA provides a voluntary professional overlay above the state minimum, including the CSSC (Certified Structured Settlement Consultant) designation.

State insurance licensing: what to look for in 2026

Every practicing broker must hold a current life and annuity insurance producer license in each state where they conduct business.

This license is issued and overseen by the state insurance department — not any federal body. Verify any broker’s active license through your state’s insurance department producer registry before signing any settlement document. The top-rated structured settlement companies guide covers what to look for when evaluating broker-affiliated carriers.

NSSTA membership and what it signals about a broker’s conduct

NSSTA membership is voluntary — but it signals a commitment to professional standards that exceed state licensing minimums.

Member brokers under 2026 NSSTA standards are expected to disclose carrier selection rationale, provide written compensation disclosure on request, and recommend only carriers meeting defined AM Best financial strength thresholds.

Three steps to verify a broker before you sign

- Search your state’s insurance producer registry. Confirm the license is active, the state of issue is correct, and no disciplinary actions appear on record.

- Check NSSTA membership. The NSSTA maintains a public member directory at nssta.com. Current membership signals voluntary adherence to 2026 professional conduct standards above and beyond the state licensing floor.

- Request written compensation disclosure. A broker who declines to put compensation terms in writing before you sign is not meeting 2026 professional standards — regardless of license status.

💡 Expert Note (CFA): FINRA’s BrokerCheck tool for investment professional verification is the standard resource most plaintiffs reach for first — but it does not cover insurance-only producers. A structured settlement broker who is not dually registered as an investment advisor will not appear in BrokerCheck results at all. Use your state’s insurance department producer registry. That is the authoritative and correct source for insurance producer licensing status.

The bottom line on structured settlement brokers

When a structured settlement offer arrives, the broker is already on the other side of the table — engaged by the defendant’s insurer, not by the plaintiff.

The compensation question resolves cleanly: the life insurance carrier pays the broker’s commission. The plaintiff pays nothing directly.

Three things to do before your settlement is finalized

- Verify the broker’s state insurance producer license. Search your state’s insurance department producer registry — confirm the license is active, current, and free of disciplinary action. Do not rely on FINRA BrokerCheck for this search.

- Request written compensation disclosure. Any broker operating under 2026 NSSTA member standards must provide this on request. A refusal to provide it is itself a signal worth taking seriously.

- Get an independent review. Retain a fee-only financial planner or plaintiff attorney whose compensation is not tied to any annuity placement. An income tax impact calculator can model the after-tax value of different payment structures as part of that independent review.

A structured settlement designed around your documented financial needs is a durable, tax-efficient asset.

One structured around the insurer’s liability timeline is a document you will live with for decades.

Frequently asked questions about structured settlement brokers

The following questions address the most common points of confusion about what a structured settlement broker does, how they are compensated, and how to evaluate one before accepting any settlement offer.

1. What does a structured settlement broker do?

A structured settlement broker is a licensed insurance professional who designs the annuity payment schedule converting a personal injury settlement into tax-free periodic income, selects the rated life insurance carrier to fund the annuity, and coordinates the qualified assignment that permanently transfers payment responsibility from the defendant to the carrier. Consult a licensed financial professional before accepting any settlement structure.

2. Who pays a structured settlement broker?

The annuity-issuing life insurance carrier pays the structured settlement broker — not the plaintiff. The commission is embedded in the annuity’s actuarial pricing at the time of purchase and does not appear as a line-item deduction from the settlement amount. No invoice is sent to the plaintiff, and no fee is subtracted from the award. Consult a licensed financial professional before finalizing.

3. How much does a structured settlement broker earn per case?

Structured settlement broker commissions typically range from 3% to 5% of the annuity premium, paid entirely by the life insurance carrier. On a $500,000 annuity that equals approximately $15,000–$25,000; on a $1,000,000 placement, approximately $30,000–$50,000. All commission figures are embedded in carrier pricing and are not separately invoiced to the plaintiff. Source: NSSTA 2026 standards. Consult a licensed financial professional before finalizing your settlement structure.

4. Do I need a structured settlement broker?

The defendant’s insurer engages the structured settlement broker — the plaintiff does not hire or fire them. Plaintiffs have no direct authority over broker selection. A plaintiff can independently retain a fee-only financial planner with no compensation tied to any annuity placement to provide an objective review of the proposed structure before signing. Consult a licensed financial professional before agreeing to any settlement terms.

5. What is the difference between a structured settlement broker and a factoring company?

A structured settlement broker arranges the original annuity at settlement, paid by the life insurance carrier. A factoring company later offers to purchase the plaintiff’s future payments for immediate cash at a steep discount. These are separate entities with opposing financial incentives. Factoring transactions require court approval in all 50 states and carry a 40% federal excise tax under 26 USC 5891. Consult a licensed attorney before accepting any buyout offer.

6. Are structured settlement brokers regulated?

Structured settlement brokers are regulated at the state level as licensed insurance producers — not under SEC or FINRA authority. Each state’s insurance commissioner oversees licensing, conduct standards, and renewal requirements. The NSSTA adds a voluntary professional conduct layer above state minimums. Verify any broker’s license through your state’s insurance department producer registry before finalizing any settlement agreement. Consult a licensed financial professional.

7. What licenses does a structured settlement broker need?

A structured settlement broker must hold a current state-issued life and annuity insurance producer license in each state where they conduct business. Many also hold the CSSC (Certified Structured Settlement Consultant) designation from the NSSTA, which requires demonstrated expertise in settlement mechanics, IRC tax law, and annuity product structures. Verify license status through your state’s insurance department producer registry. Consult a licensed financial professional.

8. Can a structured settlement broker negotiate my settlement amount?

No. A structured settlement broker cannot alter the total settlement dollar amount, which is negotiated between the plaintiff’s attorney and the defendant before the broker enters the process. The broker designs how that agreed amount is paid — via an annuity payment schedule — but has no authority over the settlement figure itself. Your attorney negotiates the amount. The broker arranges delivery. Consult a licensed attorney.

9. How long does it take to set up a structured settlement in 2026?

Most standard personal injury structured settlements take 45 to 90 days from the agreement date to the first annuity payment. Cases involving minors or court-approval requirements typically run longer. Processing timelines depend on carrier internal review speed and qualified assignment complexity. Confirm expected timelines with both the broker and the carrier in writing before signing any settlement document. Consult a licensed financial professional.

10. What is a qualified assignment in a structured settlement?

A qualified assignment under IRC Section 130 allows the defendant to permanently transfer future payment obligations to a third-party assignee — typically a life insurance affiliate — releasing the defendant from all liability. This transfer simultaneously preserves the plaintiff’s federal tax exclusion under IRC Section 104(a)(2). Once executed, the assignment is irrevocable; the carrier, not the defendant, becomes solely responsible for all future payments. Consult a licensed financial professional before signing.

11. What questions should I ask a structured settlement broker before signing?

Ask your structured settlement broker four questions before finalizing: Which carriers did you evaluate, and why did you select this one? What is your commission and who pays it? What is the carrier’s current AM Best financial strength rating? What protections exist if the issuing carrier faces financial difficulty? Request written answers to all four — documented responses are standard professional practice under 2026 NSSTA member standards. Consult a licensed financial professional.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.