Structured Settlement Payments, Taxes, and Your Rights

Structured settlement factoring companies charge effective annual rates

between 9% and 29% — a gap that costs recipients $314,000 or more on a $500,000

payment stream.

In This Article

What is a structured settlement — and is yours worth keeping?

You are holding something most people misunderstand from the day they receive it.

A structured settlement is not simply a payment plan. It is a legally binding financial instrument — one that can protect your long-term financial security or, if mishandled, cost you tens of thousands of dollars you cannot get back.

Before this article covers a single number, it needs to know which situation brought you here.

If you just received a structured settlement offer

Your attorney has presented you with a settlement that pays out over time instead of all at once. You are trying to figure out whether this is better or worse than asking for a lump sum — and you are probably working with a deadline that is making the decision feel more urgent than it needs to be.

Go directly to the section titled Structured settlement vs. lump sum: how to make the right call. Read Section 5 on taxes first if you have any uncertainty about whether the money is taxable.

If you already own a settlement and need cash now

A company — possibly one you’ve seen advertised — has contacted you with an offer to buy your future payments. Or you’ve found yourself in a financial emergency and you’re wondering whether selling makes sense.

This is the highest-stakes financial decision in this article. Go to the section titled Selling your structured settlement: how the secondary market works, then read Discount rates: what selling your structured settlement really costs before you speak to any buyer.

If you’re researching on behalf of someone else

You are an attorney, a financial advisor, a family member, or an executor trying to understand what a structured settlement means for someone in your care. This article is written at the level of depth you need.

Start at Section 2 and read through. The state law reference table in Section 9 and the tax framework in Section 5 are the most likely sections to answer your specific questions.

What this article covers — and what it won’t tell you

In 28 years advising clients in capital markets and portfolio strategy, the most expensive structured settlement mistakes I have seen all share one feature: the person involved did not have access to the right information at the right moment.

This article exists to change that. Every data point below traces to the IRS, the National Structured Settlements Trade Association (NSSTA), applicable federal statutes, or state law. Where a rate or percentage is cited, the source and date appear alongside it.

This article will not tell you what decision to make. It will give you every number, every legal protection, and every analytical framework you need to make that decision correctly.

ℹ️ Disclaimer: This article is an educational resource produced for informational purposes. It does not constitute financial, tax, or legal advice. For decisions involving a specific structured settlement agreement, consult a CPA, a fiduciary financial advisor, and a licensed attorney with structured settlement experience in your state.

What a structured settlement actually is — the complete definition

Structured settlement: A legal agreement in which compensation for a personal physical injury, workers’ compensation claim, wrongful death, or similar legal matter is paid out through periodic payments over time — typically funded by an annuity purchased from a life insurance company — rather than as a single immediate payment. Under IRC §104(a)(2), payments from qualifying structured settlements are generally excluded from federal gross income.

That is the definition Google will show in its featured snippet. The rest of this section explains what it actually means for your money.

The one-sentence definition Google will show in search results

Structured settlement: A tax-advantaged legal payment arrangement that delivers compensation for personal physical injury or similar claims through periodic payments — funded by an annuity — rather than a single lump sum, providing long-term income security under court-authorized terms.

The critical word in that definition is funded. A structured settlement is not itself an annuity. It is the legal agreement that an annuity funds. This distinction matters more than most people realize.

How a structured settlement differs from a regular annuity

When you purchase an annuity directly — through an insurance company or a broker — you own the annuity contract. You chose the insurer, you can (in most cases) surrender the contract, and you bear the investment risk or enjoy the guaranteed return depending on the contract type.

A structured settlement is different in every one of those dimensions.

The annuity funding your structured settlement was purchased not by you but by the defendant’s insurance company through a process called a qualified assignment under IRC §130. You did not choose the insurer. You cannot surrender the contract. You own a contractual right to receive payments — and the security of those payments depends entirely on the financial strength of the insurer that issued the annuity.

💡 Expert Note (CFA): The most important technical distinction I make with clients is this: you don’t own an annuity — you own a contractual right to receive payments that the annuity funds. This matters enormously over a 20-to-40-year payment stream if the issuing insurance company’s financial health deteriorates. Always ask for the issuer’s AM Best rating before any settlement is finalized.

For a broader comparison of how annuities work as financial products, see our guide to annuities and how they pay — which covers the full spectrum from immediate to deferred structures.

⚠️ Warning: Annuity contracts that fund structured settlements are insurance products regulated at the state level. They are not FDIC-insured. Payment security depends on the financial strength of the issuing insurance company. Request the issuer’s AM Best rating — a rating of A- or above (AM Best scale) is the industry-standard minimum threshold for a structurally sound settlement annuity.

Types of structured settlement payment options

Not all structured settlements pay the same way. The four primary payment structures are:

- Level periodic payments: A fixed dollar amount paid on a set schedule — monthly, quarterly, or annually — for a defined period or for life. Example: $2,800 per month for 25 years.

- Increasing periodic payments: Payments that grow at a set rate — commonly 2% to 3% annually — to offset inflation over the payment period. Most appropriate for younger claimants with long payment durations.

- Deferred lump sum with periodic payments: An initial waiting period (commonly 5 to 10 years) before payments begin, used when the claimant will need income at a specific future date rather than immediately.

- Hybrid structures: A combination of an initial lump sum (often used for immediate medical expenses or attorney fees) followed by a periodic payment stream. The most common structure in personal injury settlements.

The structure you end up with was likely determined during settlement negotiation and is now locked into your annuity contract. Understanding which structure you have is the first step toward understanding what your settlement is actually worth.

Who qualifies for a structured settlement?

Structured settlements are available in a specific set of legal and financial contexts. They are not available for every legal claim.

Qualifying contexts under federal law and standard practice include:

- Personal physical injury claims (auto accidents, slip-and-fall, premises liability)

- Physical sickness claims (toxic exposure, mesothelioma, asbestos)

- Medical malpractice and wrongful death

- Workers’ compensation settlements (subject to state-specific rules)

- Product liability claims resulting in physical injury

- Lottery and prize winnings above defined thresholds (subject to different tax treatment — see Section 12)

Structured settlements are generally not available for purely financial disputes, breach of contract claims unrelated to physical injury, or employment discrimination claims unless physical injury is involved.

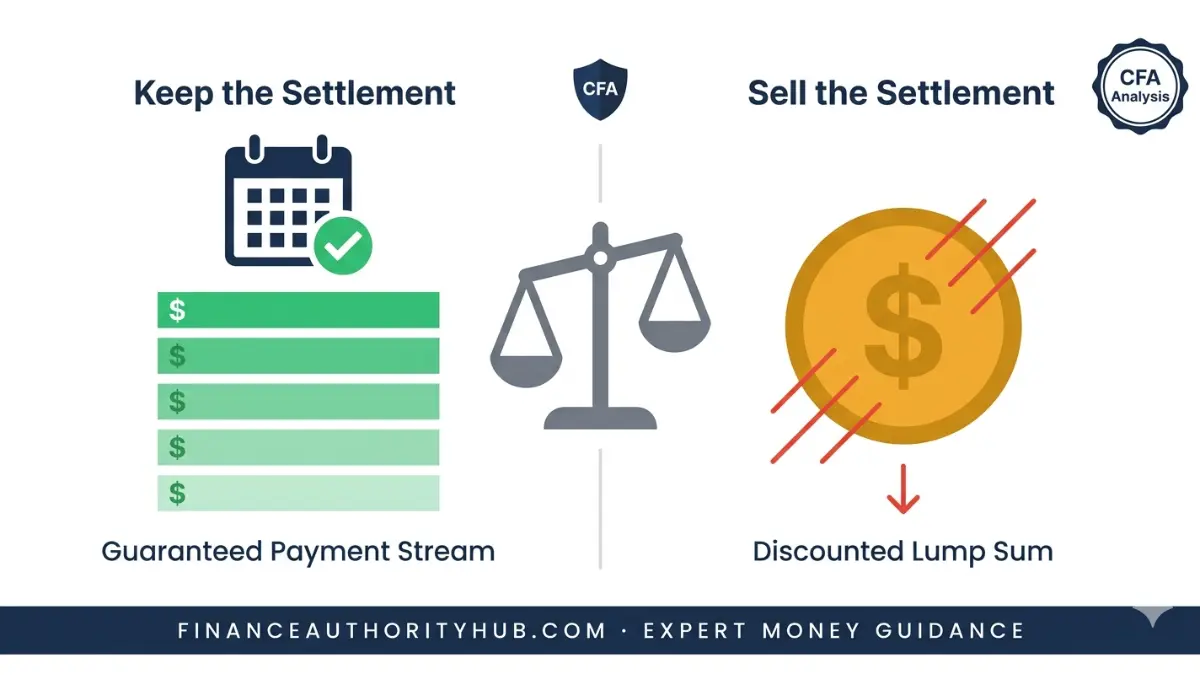

Structured settlement vs. lump sum: the core trade-off

The fundamental financial trade-off is straightforward: a structured settlement guarantees that the full negotiated compensation amount arrives in your hands over time, protected from the decisions — good and bad — you might make with a large cash sum. A lump sum delivers all the money immediately, requiring disciplined self-management to generate equivalent long-term value.

Research from the RAND Institute for Civil Justice on personal injury settlement outcomes shows that recipients who receive lump-sum awards frequently deplete them within five years, particularly when the settlement is the largest single financial event of their lives. Structured settlements prevent this depletion by design.

The full decision framework — including a present-value calculation that makes this comparison concrete — appears in Section 6.

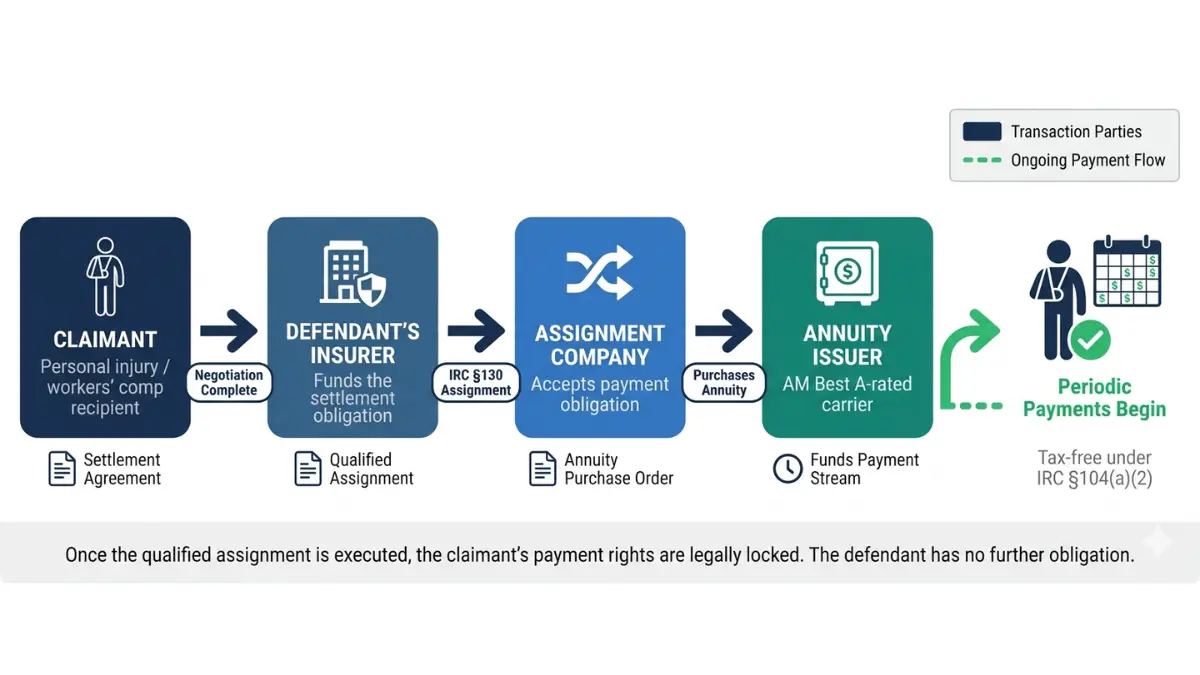

How a structured settlement is created: the step-by-step process

Understanding how your settlement was created is essential to understanding your rights — and your limitations — going forward.

Here is how a structured settlement goes from negotiation to your first payment:

- The plaintiff and defendant (or defendant’s insurer) agree on a total settlement amount and the payment structure — amount, frequency, duration, and any inflation adjustment.

- The defendant’s insurer assigns the obligation to make periodic payments to a third-party assignment company through a qualified assignment agreement under IRC §130.

- The assignment company purchases an annuity contract from a life insurance company — this is the qualified funding asset that will generate the payment stream.

- The life insurance company (annuity issuer) holds the premium and invests it, making scheduled payments according to the annuity contract.

- You receive your periodic payments directly from the annuity issuer for the duration specified in your settlement agreement.

Step 1: The settlement negotiation and amount agreement

The settlement amount and structure are determined through negotiation between your attorney and the defendant’s insurer. Your attorney should be modeling the present value of different payment structures to ensure the structured option is financially comparable to any lump-sum alternative on the table.

A structured settlement consultant — typically hired by the defendant’s insurer — designs the specific payment schedule. This is the step where the rated-age calculation may be applied (see Section 4 for what that means and how it affects your monthly amount).

⚠️ Warning: Structured settlement consultants are typically paid by the defendant’s insurer or the assignment company, not by you. Their incentive is to design a structure that satisfies your financial needs while minimizing the insurer’s annuity premium cost. You are entitled to have your own attorney or financial advisor review any proposed structure before you agree to it.

Step 2: The qualified assignment — what it means for you

The qualified assignment is the legal transfer that releases the original defendant from all further payment obligations. Once executed, the defendant owes you nothing.

Your payment rights now rest entirely on the assignment company and, through the annuity it purchased, on the financial strength of the annuity issuer. Under IRC §130, this structure is what enables the periodic payments to qualify for income tax exclusion under §104(a)(2) — but only if the assignment meets specific statutory requirements.

Some settlements are structured through a qualified settlement fund — a temporary holding vehicle that can provide additional tax and timing flexibility before the annuity is purchased. This is a specialized structure that your attorney should explain if applicable.

Step 3: The annuity purchase and issuer selection

The assignment company uses the premium payment from the defendant’s insurer to purchase an annuity from a state-regulated life insurance company. The annuity issuer is typically a major life insurance carrier — common issuers include MetLife, Pacific Life, Berkshire Life, and Symetra.

You do not choose the annuity issuer. The assignment company does. This is why the issuer’s financial strength rating matters: you are trusting this company to make payments that may span 40 years.

📊 Data Point: AM Best, the insurance industry’s primary rating agency, assigns financial strength ratings from A++ (Superior) to D (Poor). Industry practice for structured settlement annuity issuers is to require a minimum of A- (Excellent). Verify your issuer’s current rating at ambest.com/ratings before your settlement is finalized.

For a broader understanding of how life insurance companies are structured and rated — which directly applies to your annuity issuer — see our guide to life insurance costs and types.

Step 4: Your payment rights are now locked in — here’s why

Once the qualified assignment is executed and the annuity is purchased, the payment structure is legally locked. The terms cannot be changed by you, by the defendant, or by the assignment company.

The only mechanisms available if your financial circumstances change are: (1) selling some or all of your future payment rights to a factoring company through the court-supervised secondary market process described in Sections 7 through 11, or (2) in very limited cases, petitioning a court for modification — a legally complex and rarely successful approach.

💡 Expert Note (CFA): The irreversibility of the qualified assignment is the most important feature of a structured settlement that claimants frequently underestimate. I have worked with clients who agreed to a structure that looked adequate during settlement negotiations and then found it impossible to adjust when their medical or financial circumstances changed dramatically three years later. Before agreeing to any structure, model your realistic financial needs across at least three scenarios: best case, expected case, and a significant unexpected expense event.

The role of a structured settlement consultant

A structured settlement consultant or broker designs the payment schedule and facilitates the annuity purchase. They typically hold a life insurance license and may also hold a securities license. FINRA’s BrokerCheck at brokercheck.finra.org allows you to verify any consultant’s registration and complaint history.

Because most structured settlement consultants are paid by the defendant’s insurer or the assignment company, their fee is not transparent to you. This creates a potential conflict of interest that is well-documented in the industry but rarely disclosed proactively.

ℹ️ Disclaimer: The information in this section describes standard structured settlement creation mechanics and is provided for educational purposes. Structured settlement agreements are legally binding contracts. Before signing any settlement agreement, have the terms reviewed by an independent attorney who represents your interests exclusively — not an attorney who also represents the defendant or the assignment company.

What structured settlement payments actually look like

Knowing what a structured settlement is matters. Knowing what it pays — in real dollars, over real time — is what determines whether the agreement serves your financial interests.

Average structured settlement amounts by case type

Settlement amounts vary enormously based on injury severity, jurisdiction, liability evidence strength, and negotiating skill. The ranges below reflect publicly reported data and NSSTA industry surveys.

| Case Type | Typical Total Settlement Range | Typical Structured Portion | Typical Duration |

|---|---|---|---|

| Auto accident (moderate injury) | $50,000–$250,000 | 60%–100% | 10–20 years |

| Auto accident (severe/permanent injury) | $250,000–$2,000,000+ | 70%–100% | 20–40 years or life |

| Medical malpractice | $200,000–$3,000,000+ | 50%–90% | 15–40 years or life |

| Workers’ compensation | $75,000–$500,000 | 40%–80% | 10–30 years |

| Wrongful death | $250,000–$5,000,000+ | 60%–100% | 20–40 years |

| Product liability (physical injury) | $100,000–$2,500,000+ | 50%–95% | 15–40 years |

Source: NSSTA industry data and publicly available settlement reporting, 2023–2024. Individual amounts vary substantially by jurisdiction, injury severity, and case-specific factors.

📊 Data Point: According to NSSTA industry surveys, structured settlements fund approximately $6 billion in annual new business in the United States, with the average new structured settlement providing approximately $324,000 in total periodic payments. These figures represent negotiated structures across all case types and should not be used to benchmark individual settlement adequacy.

How long structured settlements typically last

Structured settlements typically span 10 to 40 years, depending on the nature and severity of the underlying claim and the claimant’s age and medical prognosis. Life-contingent options have no fixed end date — payments continue as long as the recipient is alive.

The four primary duration structures are:

- Fixed-period certain: Payments are guaranteed for a defined number of years regardless of whether the recipient is alive. If the recipient dies before the period ends, a named beneficiary receives remaining payments.

- Life-contingent: Payments continue only while the recipient lives. When the recipient dies, payments stop — no residual value transfers to heirs.

- Life with period certain: Payments continue for life, but if the recipient dies within a specified period (commonly 10 or 20 years), a beneficiary receives the remaining guaranteed payments.

- Joint and survivor: Payments continue while either of two designated individuals (commonly spouses) is alive — used primarily in wrongful death settlements.

Payment structure options: level, increasing, deferred, hybrid

Your specific monthly (or quarterly, or annual) payment amount depends on three variables: the annuity premium the defendant’s insurer paid, the payment structure selected, and the interest rate environment at the time the annuity was purchased.

Here is what the same $250,000 annuity premium produces under four different payment structures, using approximate pricing from 2024 interest rate conditions:

| Payment Structure | Monthly Amount | Duration | Total Payout | Best For |

|---|---|---|---|---|

| Level periodic | $1,425 | 20 years | $342,000 | Predictable income needs |

| 3% annual increase | $1,180 (year 1) → $2,130 (year 20) | 20 years | $381,600 | Younger claimants, inflation hedge |

| 5-year deferred, then level | $1,720 | 20 years (starting year 6) | $412,800 | Claimants returning to work initially |

| $50,000 lump + level periodic | $1,090 | 20 years | $311,600 + $50,000 | Immediate medical cost coverage |

Illustrative calculations based on 2024 annuity pricing environment. Actual amounts vary with insurer pricing and prevailing interest rates at time of purchase.

📊 Data Point: The annuity pricing environment is directly tied to the interest rate levels set by the Federal Reserve. When the Federal Reserve raises the federal funds rate, annuity issuers can price higher payment amounts for the same premium — meaning a $250,000 annuity premium purchased in a high-rate environment produces meaningfully more monthly income than the same premium purchased when rates are low. Claimants settling cases during high-rate periods effectively receive more purchasing power from the same negotiated dollar amount. Current Federal Reserve rate data is available at federalreserve.gov/releases/h15.

What happens to your structured settlement when you die?

Whether your payments transfer to a beneficiary depends entirely on whether your payments are period-certain or life-contingent.

If your payments are period-certain, your named beneficiary receives all remaining guaranteed payments if you die before the period ends. These payments are made directly to the beneficiary under the same tax treatment that applied to you (typically tax-exempt for physical injury settlements).

If your payments are life-contingent, they stop at your death. No residual value transfers to your estate or your heirs. The annuity issuer retains any unused premium value.

⚠️ Warning: Many structured settlement recipients do not know whether their payments are period-certain or life-contingent until they review the original settlement agreement. If you are unsure, locate your settlement documents and look for the terms “period certain,” “guaranteed period,” or “life contingent.” Your settlement administrator can also confirm the payment type. This distinction has direct implications for estate planning.

How to calculate your settlement’s total payout value

The nominal total payout value is simple arithmetic: payment amount × frequency × duration. A $2,000 monthly payment over 20 years produces a nominal total of $480,000.

But the nominal total is not the economically meaningful number. The meaningful number is the present value — what those future payments are worth in today’s dollars, discounted at a rate that reflects the alternative use of that capital.

The present value formula is:

PV = PMT × [1 – (1 + r)^(–n)] / r

Where:

- PMT = periodic payment amount

- r = discount rate per period (annual rate ÷ payment frequency)

- n = total number of payment periods

At a 4% annual discount rate, $2,000 per month for 20 years has a present value of approximately $327,000 — not $480,000. At a 6% discount rate, the present value falls to approximately $279,000. This calculation is the foundation of every structured settlement buy/sell/hold decision in this article.

Use our investment calculator to model your specific payment stream against different discount rate assumptions.

Is your structured settlement amount typical? A data benchmark

The single most common complaint I hear from structured settlement recipients is that they don’t know whether their payment amount is fair or whether they left money on the table during negotiation.

Here is the benchmark framework:

- For personal injury settlements: A fair structured settlement should have a present value (at a 4%–5% discount rate) at least equal to what a competent plaintiff’s attorney could have reasonably recovered as a lump sum after litigation costs and attorney fees.

- For workers’ compensation: State law significantly constrains the settlement amount; benchmarking against average state workers’ compensation settlement data from your state’s workers’ compensation board is more useful than national averages.

- For medical malpractice: Case-specific factors dominate; the specialty medical malpractice settlement databases maintained by plaintiff’s attorney associations are the most useful benchmark sources.

ℹ️ Disclaimer: Settlement amounts cited in this section reflect industry survey data and published reports as of 2023–2024. Individual settlement amounts are determined by case-specific facts, jurisdiction, injury severity, evidence strength, and negotiation skill. This data should not be used to assess the adequacy of any specific settlement agreement without the guidance of a plaintiff’s attorney or financial professional familiar with your case.

Structured settlement taxes: what’s exempt, what isn’t, and why

Tax uncertainty is one of the most common sources of financial anxiety for structured settlement recipients. The answer is specific, statutory, and knowable — and most of the time, the news is good.

The IRS rule that makes most structured settlements tax-free

Under IRC §104(a)(2), gross income does not include “damages (other than punitive damages) received (whether by suit or agreement and whether as lump sums or as periodic payments) on account of personal physical injuries or physical sickness.” This exclusion applies to the full periodic payment stream — principal and interest component combined — if the underlying settlement qualifies.

Structured settlement payments are excluded from federal gross income when: (1) the underlying claim is for personal physical injury or physical sickness; (2) the payments are received pursuant to a qualifying agreement; and (3) the structured settlement was properly established through a qualified assignment under IRC §130.

The reference document for structured settlement tax treatment is IRS Publication 4345 (“Settlements — Taxability”), which provides the IRS’s official guidance on the taxability of settlement proceeds across all claim types.

📊 Data Point: Treasury Regulation §1.104-1(c) defines “personal physical injuries or physical sickness” as requiring a direct physical injury or sickness — not merely emotional distress or financial harm. The regulation’s language is the decisive factor in determining whether your specific settlement qualifies for the §104(a)(2) exclusion.

Which settlement components ARE taxable — the exceptions

The §104(a)(2) exclusion is not universal. Several settlement components are specifically excluded from the exclusion — meaning they are taxable:

- Punitive damages: Always included in gross income, even when paid as part of a personal physical injury settlement. If your settlement includes punitive damages, that portion is taxable regardless of payment structure.

- Emotional distress not originating from physical injury: Payments for emotional distress that are not attributable to a physical injury or sickness are taxable. The IRS has clarified (Notice 95-45) that emotional distress is not itself a “physical injury” — the physical injury must be the underlying cause.

- Interest earned on settlement funds: If settlement funds are held in a qualified settlement fund or similar vehicle and earn interest before disbursement, that interest is taxable as ordinary income.

- Lost wages or lost profits in business-related claims: Settlement payments allocable to lost wages or lost business profits are generally taxable as ordinary income.

- Medical expense reimbursements (with prior deduction): If you deducted medical expenses in a prior year and then received settlement compensation for those same expenses, the reimbursement is taxable to the extent of the prior deduction.

| Component | Tax Treatment | IRS Authority |

|---|---|---|

| Physical injury damages | Excluded from gross income | IRC §104(a)(2) |

| Physical sickness damages | Excluded from gross income | IRC §104(a)(2) |

| Workers’ comp (general) | Excluded from gross income | IRC §104(a)(1) |

| Punitive damages | Taxable as ordinary income | IRC §104(a)(2) exception |

| Emotional distress (non-physical) | Taxable as ordinary income | Notice 95-45 |

| Interest on settlement funds | Taxable as ordinary income | IRC §61 |

| Lost profits (business cases) | Taxable as ordinary income | IRC §61 |

Tax treatment of structured settlements vs. lump sums

The tax treatment is identical for properly structured periodic payments and lump-sum payments from the same qualifying physical injury claim — both are excluded from gross income under §104(a)(2).

The common misconception is that lump sums are taxable while structured payments are not. This is incorrect. Both are excluded when the underlying claim qualifies.

Where the difference emerges: if you invest a lump sum and earn returns on it, those investment returns are taxable. A structured settlement’s periodic payments — which include what would otherwise be interest on the annuity — are not taxable because the exclusion covers the entire payment, not just the principal portion.

For context on how investment returns on lump-sum proceeds are taxed, see our guide to capital gains tax rates and rules.

What about state income taxes on settlement payments?

Most states follow federal tax treatment for structured settlement payments — excluding qualifying physical injury settlement income from state income tax. However, state tax law is not uniform.

A few states impose state income tax on settlement payments that are federally excluded, or apply different tests for what constitutes a “physical injury” qualifying for exclusion.

⚠️ Warning: State income tax treatment of structured settlement payments varies by state and may not mirror federal treatment. Taxpayers in states with complex income tax codes — particularly California, New York, New Jersey, and Massachusetts — should verify state-specific treatment with a CPA or tax attorney before assuming the federal exclusion applies at the state level.

Tax rules when you sell your structured settlement

Selling your structured settlement to a factoring company creates a separate taxable event for any portion of the original settlement that was not §104-exempt. The lump sum you receive from the factoring company carries the tax character of the underlying settlement payments.

If your settlement was entirely from a physical injury claim and entirely §104-exempt, the lump sum proceeds from the sale maintain that exempt status — they are not taxable. If your settlement included punitive damages or other taxable components, selling those payment rights creates a taxable transaction.

Additionally, if you assigned your payment rights at a gain relative to your adjusted basis (generally the tax basis in the payment rights), the gain may be taxable. This is a nuanced area where CPA guidance is essential.

For context on how tax brackets affect any taxable settlement component, see our guide to 2026 income tax brackets.

The one tax form structured settlement recipients should know

IRS Publication 4345 (“Settlements — Taxability”) is the definitive IRS guidance document on settlement taxation. It covers physical injury settlements, emotional distress claims, punitive damages, and workers’ compensation in a single reference document.

Every structured settlement recipient should read it. It is written in accessible language and takes approximately 15 minutes.

ℹ️ Disclaimer: The tax treatment described in this section is based on current IRS guidance under IRC §104(a)(2), Treasury Regulation §1.104-1, and IRS Publication 4345. Tax treatment of your specific settlement depends on the nature of your underlying claim, the terms of your settlement agreement, and applicable state law. This is not tax advice. Consult a CPA or tax attorney with structured settlement experience for a determination specific to your situation.

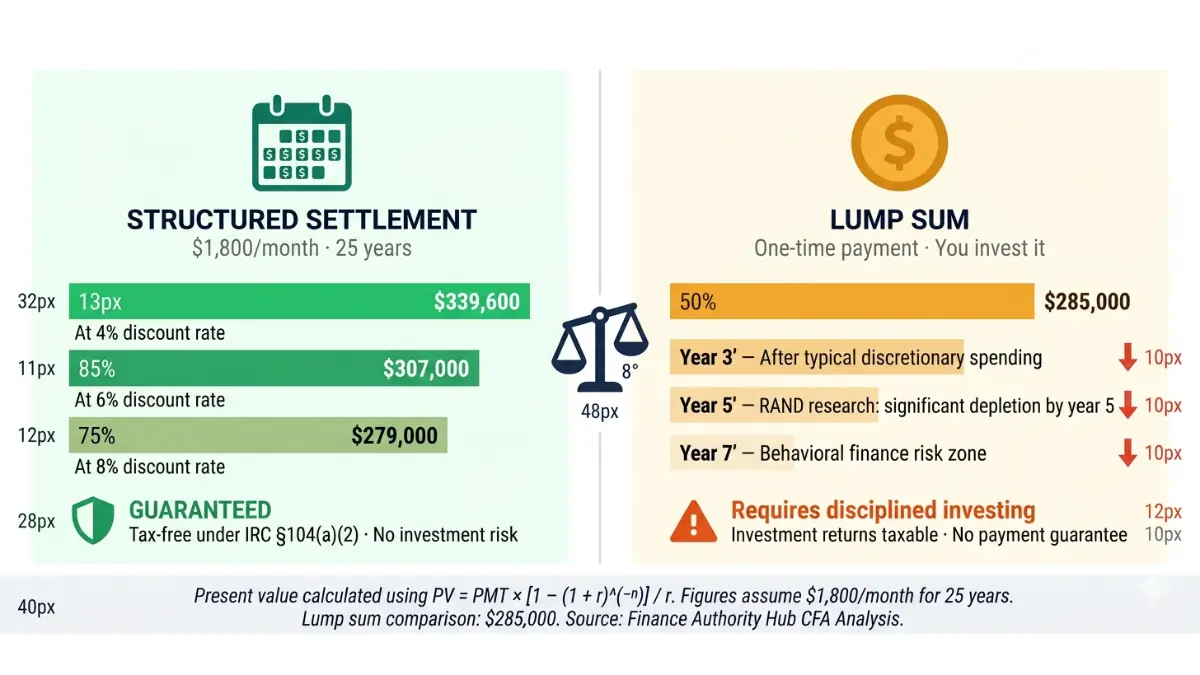

Structured settlement vs. lump sum: how to make the right call

This is the section most structured settlement recipients actually need — and the one where the analytical work determines whether you make a decision you can live with for 30 years.

The math: how to compare a settlement to a lump sum offer

The correct comparison is not “which amount is bigger.” It is “what is the present value of the structured settlement payment stream at a discount rate appropriate to my situation?”

The present value formula:

PV = PMT × [1 – (1 + r)^(–n)] / r

A concrete example:

- Structured settlement: $1,800 per month for 25 years (300 payments)

- Alternative lump sum offer: $285,000

At a 4% annual discount rate (r = 0.333% per month, n = 300): PV = $1,800 × [1 – (1.00333)^(–300)] / 0.00333 PV ≈ $1,800 × 188.7 ≈ $339,600

The structured settlement is worth approximately $339,600 in today’s dollars at a 4% discount rate — $54,600 more than the $285,000 lump sum. At a 6% discount rate, the present value falls to approximately $280,000 — below the lump sum offer. At 8%, it falls to approximately $230,000.

The question is not whether the structured settlement has higher nominal value. The question is: at what discount rate does the lump sum become the better choice for your specific situation?

Use our compound interest calculator to model what a lump sum would grow to under realistic investment scenarios — this is the most honest way to run the comparison.

The behavioral finance problem with lump sums

Decades of research on how people actually manage large, unexpected cash receipts shows a consistent pattern: most recipients do not achieve the investment returns their financial advisors project.

The RAND Institute for Civil Justice documented that a significant proportion of personal injury claimants who received lump-sum payments reported financial difficulties within three to five years of the settlement. Behavioral economics research identifies four primary failure modes: lifestyle inflation immediately following receipt, inadequate investment diversification, vulnerability to financial predation (family members, scam operators), and failure to account for tax liability on any taxable settlement components.

💡 Expert Note (CFA): The most consistent mistake I observe when clients with large settlement offers choose lump sums is what I call the “discipline premium” fallacy — the assumption that they will invest the money conservatively and earn a stable 6% return, when their actual financial behavior suggests they will be fully invested in the market for two years, withdraw 40% for a real estate opportunity, and then panic-sell when the market drops. A structured settlement doesn’t require discipline. It pays you regardless of your financial behavior. That guarantee has real value that present-value math alone does not fully capture.

When a structured settlement is clearly the better choice

A structured settlement provides superior financial outcomes when:

- The claimant has limited prior investment experience and no established relationship with a fiduciary financial advisor.

- The settlement amount, if received as a lump sum, would significantly exceed the claimant’s typical annual income — increasing behavioral finance risk.

- The claimant has dependents whose long-term financial security depends on guaranteed income availability.

- The claimant’s physical condition requires ongoing medical expense coverage over many years.

- The claimant is in a state with high investment income tax rates — the tax exemption on structured settlement payments has greater value in high-tax states.

- The claimant is risk-averse and values certainty of income over potential investment upside.

When a lump sum may serve you better

A lump sum may produce better financial outcomes when:

- The claimant has significant existing high-interest debt — the cost of that debt (at 20%+ APR for credit cards) exceeds the implied return of the structured settlement. Paying off high-interest debt at 20% is a guaranteed 20% return.

- The claimant is a sophisticated investor with a documented history of disciplined, diversified long-term investing.

- The claimant has specific near-term capital needs — a business investment, real estate purchase, or educational expense — that cannot be met from the periodic payment stream.

- The claimant has access to a Roth IRA or similar tax-advantaged vehicle that could shelter the lump sum’s investment returns, partially offsetting the tax exemption advantage of the structured settlement.

- The structured settlement’s implied return (the discount rate at which PV = lump sum) is below the risk-free rate — meaning the lump sum is genuinely the better financial deal even before behavioral considerations.

The decision framework: a five-question self-assessment

Answer these five questions honestly before making your decision:

- What is my current high-interest debt balance? If your high-interest debt exceeds 15% of the total settlement value, the lump sum case is strong — debt elimination provides a guaranteed return that the structured settlement’s certainty cannot match.

- Do I have a fiduciary financial advisor who will manage the lump sum? If no, the behavioral finance risk of a lump sum is substantially higher than most recipients expect.

- What are my dependents’ needs over the next 20 years? If you support children or a spouse who would be financially harmed by depletion of a lump sum, the structured settlement’s income guarantee has family protection value.

- What is the implied discount rate of the lump sum offer? Solve for r in the PV formula above. If the implied rate is above 6%, the lump sum is likely the better financial deal at typical investment return expectations.

- What does my attorney say about the comparable lump-sum recovery available through litigation? The structured settlement’s value should be benchmarked against realistic litigation recovery — not just the lump-sum offer currently on the table.

What a CFA considers when advising on this choice

💡 Expert Note (CFA): In my 28 years in capital markets, the structured settlement vs. lump sum decision is the one where I most consistently see the financially correct answer and the psychologically comfortable answer diverge. Most recipients feel that having the money in their account makes them more secure. The data shows the opposite — for the overwhelming majority of settlement recipients, the structured payment stream produces better outcomes than lump-sum self-management over a 20-year horizon. The structured settlement is not the conservative choice. It is, in most cases, the financially superior choice — with the guarantee as the premium you pay for protection against your own behavioral tendencies.

For context on how to integrate a large settlement into a broader retirement strategy, see our retirement planning guide for your 30s and beyond.

ℹ️ Disclaimer: The decision framework presented in this section is educational and does not account for your specific financial circumstances, tax obligations, or investment goals. Before accepting or declining a structured settlement offer, consult a fiduciary financial advisor and a CPA. This analysis is not personalized financial advice.

Selling your structured settlement: how the secondary market works

Structured settlement factoring is a multi-billion-dollar industry built on one premise: some settlement recipients need cash now and are willing to accept less than their payments’ present value in exchange for immediate liquidity.

Understanding how this market works — and who it primarily benefits — is the foundation of making a rational decision about whether to participate in it.

Who buys structured settlements — and why

Factoring companies — also called structured settlement buyers or purchasing companies — acquire the right to receive future structured settlement payments in exchange for a lump-sum payment to the seller. The factoring company profits on the difference between what it pays you now and what it will collect in future payments.

The business model is straightforward: a factoring company that pays you $100,000 today for a payment stream with a present value (at a 10% discount rate) of $140,000 will earn approximately $40,000 in profit over the payment period. The higher the discount rate, the larger the profit margin.

📊 Data Point: According to NSSTA data, the structured settlement secondary market processes over $1 billion in annual transfer volume in the United States, with thousands of individual transactions annually. The industry grew substantially following the passage of state Structured Settlement Protection Acts (SSPAs) in the late 1990s and early 2000s, which formalized the court approval process and provided a regulatory framework for the market.

How a structured settlement sale is structured

When you sell a structured settlement, you are not selling the annuity contract — you are assigning your right to receive the future payment stream. The transaction works as follows:

- You agree with the factoring company on a lump-sum amount and which payments are being sold (all payments, some payments, or a portion of each payment).

- A transfer agreement is executed between you and the factoring company.

- The factoring company files a transfer petition with the appropriate court in your jurisdiction.

- A judge reviews the transaction and determines whether it meets the “best interest” standard under your state’s SSPA.

- If approved, the court enters an order directing the annuity issuer to redirect the affected payments to the factoring company.

- The factoring company releases the lump-sum payment to you.

The factoring company’s profit — and your cost — is determined entirely by the discount rate applied to your payment stream. Section 8 covers this calculation in full.

⚠️ Warning: Selling structured settlement payments is an irreversible financial decision that permanently reduces your future income stream. Under most state Structured Settlement Protection Acts, you have the legal right to independent professional advice before signing any transfer agreement. This right exists specifically to protect recipients in your situation. Exercise it. This article does not recommend selling your structured settlement.

Can you borrow against a structured settlement instead?

This is one of the most frequently asked questions — and the answer is more complex than most sources acknowledge.

True loans collateralized by structured settlement payment rights are legally and structurally problematic in most states. Many state SSPAs were written to prevent the exact structure that a “loan against settlement” would create — and transactions labeled as loans but functionally equivalent to sales have been challenged in court.

A small number of specialized lenders offer what they call structured settlement loans, but these products: (a) typically require court approval equivalent to a sale; (b) carry interest rates substantially higher than conventional personal loans; and (c) are not available through conventional banking channels.

For most recipients, the choice is binary: keep the full payment stream or sell some or all of it. If you need cash, comparing the cost of selling at a factoring company’s discount rate against the cost of a personal loan at current market rates may reveal that a personal loan is cheaper — depending on your credit profile and the factoring company’s effective discount rate.

Selling all vs. selling a portion of your payments

Factoring companies offer flexibility in what they purchase:

- Full sale: All remaining payment rights are sold. Maximum immediate cash; no future payment stream remains.

- Partial sale by payment count: A specific number of future payments are sold (e.g., the next 60 monthly payments), after which you resume receiving payments directly.

- Partial sale by payment fraction: A percentage of each payment is sold (e.g., 50% of each monthly payment for the full duration), after which you retain the remaining fraction.

- Deferred payment sale: Payments that begin at a future date are sold (e.g., payments beginning 10 years from now), preserving your near-term income stream.

💡 Expert Note (CFA): Selling a portion of your payment stream rather than the full stream is, in most cases, the structurally superior approach for recipients who genuinely need liquidity for a specific financial purpose. If you need $40,000 for a medical expense, selling 24 months of payments at a fair discount rate costs you far less than selling your entire 30-year stream. Factoring companies prefer to buy larger blocks because it improves their yield economics — do not let their preference drive your sale scope.

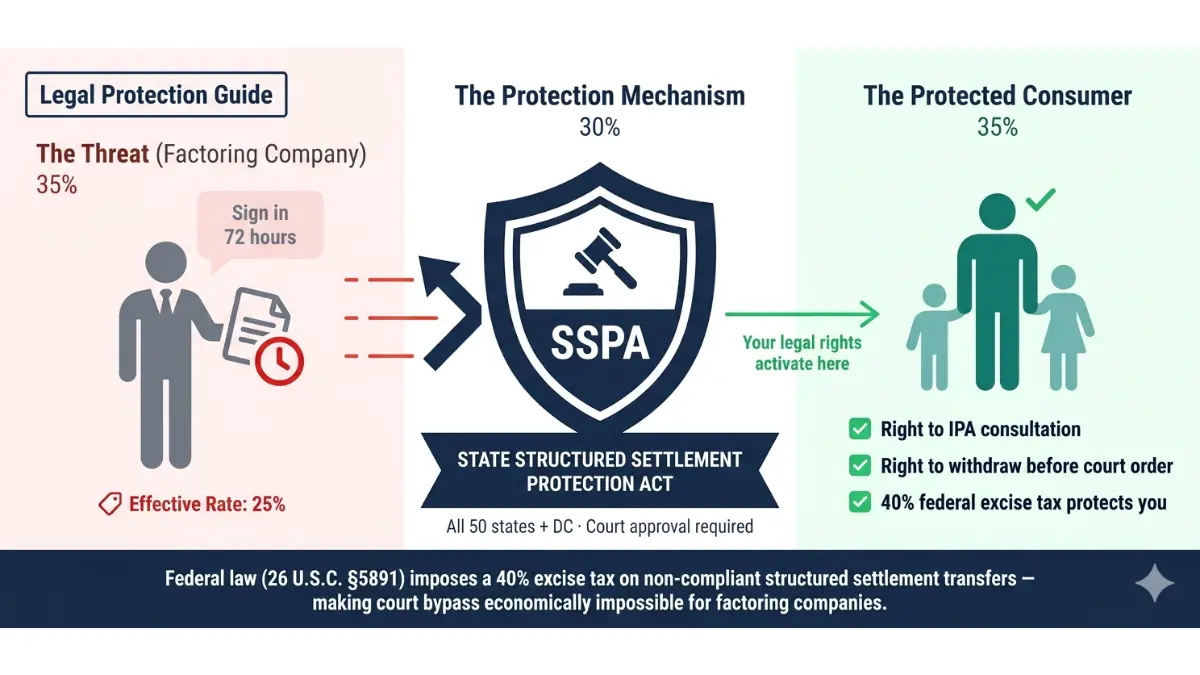

The legal requirement: why court approval is non-negotiable

Every structured settlement sale in the United States requires court approval under the applicable state SSPA. All 50 states and the District of Columbia have enacted Structured Settlement Protection Acts.

Court approval is not a formality. A judge must affirmatively find that the transaction is in your “best interest” — taking into account your financial situation, your dependents’ needs, what alternatives you have considered, and whether the discount rate you are accepting is reasonable under current market conditions.

Factoring companies that tell you court approval is “automatic” or “just paperwork” are misrepresenting the process. Courts deny transfer petitions. Courts require additional evidence. Courts reduce the approved sale scope. Your rights in this process are substantial.

How long does a structured settlement sale take?

From first contact with a factoring company to receipt of the lump-sum payment, the process typically takes 45 to 90 days. The primary variable is court scheduling — petition filing, hearing date assignment, and order issuance timelines vary by jurisdiction.

High-volume jurisdictions (urban courts processing large numbers of transfer petitions) may have longer timelines. Some states have expedited procedures for emergency financial circumstances.

ℹ️ Disclaimer: Selling structured settlement payments is an irreversible financial decision. Under most state SSPAs, you have the legal right to independent professional advice before signing any transfer agreement. This right is designed to protect you from uninformed or coerced decisions. This article is not a recommendation to sell.

Discount rates: what selling your structured settlement really costs

This is the section where the financial reality of the secondary market becomes concrete. Every structured settlement sale that has ever cost a recipient more than it should have cost them comes back to one number: the discount rate.

What a discount rate actually means in plain language

When a factoring company offers you a lump sum for your future payments, they are implicitly applying a discount rate to calculate that lump sum. The discount rate is the annual rate of return the factoring company earns on its investment in your payment stream.

A 10% discount rate means the factoring company is earning 10% annually on the money it paid you, collected through your redirected payments. A 20% discount rate means they are earning 20%. The higher the discount rate, the less you receive — and the more the factoring company profits.

This is mathematically identical to interest on a loan. Accepting a structured settlement sale at a 15% discount rate is economically equivalent to taking a 15% interest rate loan collateralized by your future payments.

For context on how rates are calculated across financial products, see our guide to APR vs. interest rate.

The real range: what factoring companies charge in 2024

Discount rates charged by structured settlement factoring companies range from approximately 9% to 29% annually, with the following distribution based on publicly reported transactions and NSSTA market data:

| Offer Quality | Typical Discount Rate | Market Context |

|---|---|---|

| Competitive (fair market) | 9%–12% | Reflects cost of capital + reasonable margin |

| Industry average | 13%–17% | Typical for standard transactions |

| Above-average cost | 18%–22% | Warrants a second and third quote |

| Predatory | 23%–29%+ | Presumptively harmful; seek independent advice immediately |

Source: Publicly reported structured settlement transfer data, academic research on secondary market pricing, and NSSTA member company disclosures, 2023–2024.

📊 Data Point: The Consumer Financial Protection Bureau (CFPB) has documented consumer protection concerns in the structured settlement secondary market, including cases where the effective annual discount rate exceeded 30% on transactions that received court approval — illustrating that court approval does not guarantee a fair price, only that a judge found the transaction to be in the seller’s best interest given the information presented.

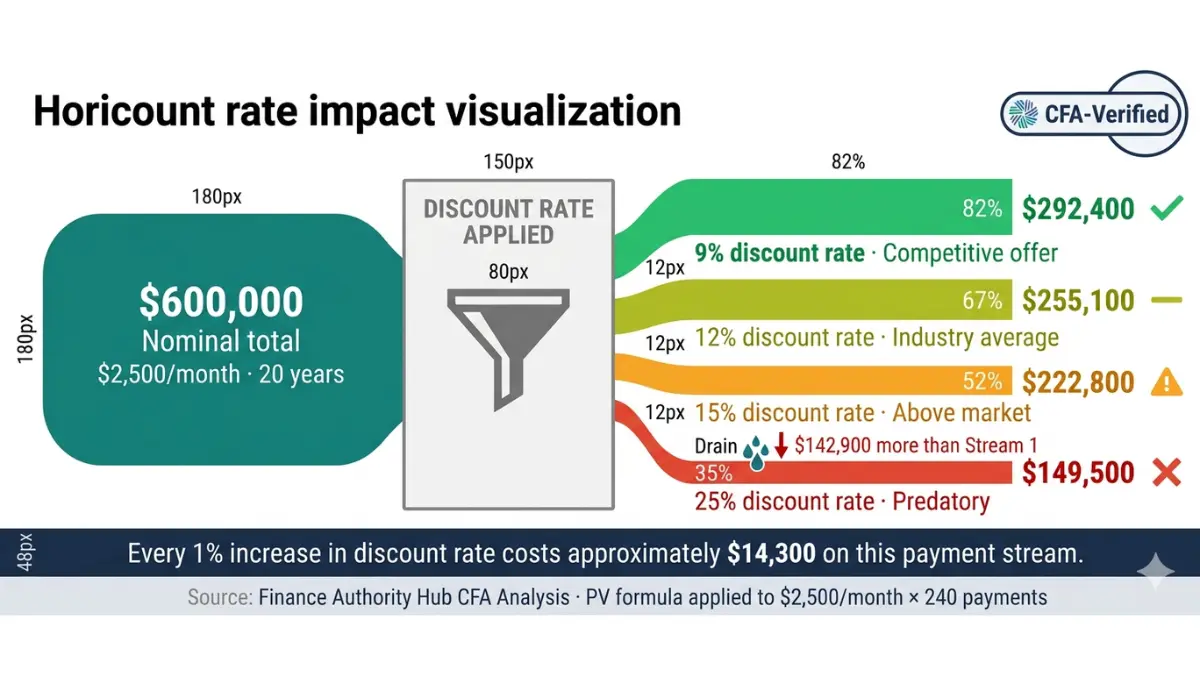

Present value calculation: a worked example with real numbers

A concrete example makes the cost of discount rate differences unmistakable.

Payment stream: $2,500 per month for 20 years (240 payments, nominal total $600,000) Market interest rate equivalent (opportunity cost): 5% annually

Present value at various discount rates:

| Discount Rate | Present Value | Amount “Lost” vs. Keeping Settlement |

|---|---|---|

| 5% (opportunity cost) | $379,500 | $0 (baseline comparison) |

| 9% (competitive offer) | $292,400 | $87,100 |

| 12% (average offer) | $255,100 | $124,400 |

| 15% (above average) | $222,800 | $156,700 |

| 20% (approaching predatory) | $181,600 | $197,900 |

| 25% (predatory) | $149,500 | $230,000 |

Calculations use the standard present value annuity formula: PV = PMT × [1 – (1 + r)^(–n)] / r. Monthly discount rates derived from annual rates.

The difference between a competitive 9% offer and a predatory 25% offer on this payment stream is $142,900 in the seller’s pocket. Getting three competing quotes before accepting any offer is not optional — it is the single most financially impactful action available to any recipient considering a sale.

💡 Expert Note (CFA): The highest effective discount rate I have reviewed in a factoring company offer presented to a client was 29.4% — advertised in the company’s marketing as a “fair market” offer. The effective rate was not disclosed in the cover letter. It was calculable only by applying the present value formula to the disclosed lump sum against the stated payment stream. Every recipient considering a sale should calculate this number before reviewing the offer in terms of whether the lump sum “feels” adequate.

Fair, average, and predatory discount rates — the benchmark table

Use this table as your negotiating reference:

| Rate Category | Annual Rate | What It Means For You | Recommended Action |

|---|---|---|---|

| Competitive | 9%–12% | Fair cost of liquidity; shop one more quote to confirm | Consider accepting if need is genuine |

| Industry Average | 13%–17% | Acceptable for standard transactions; room to negotiate | Get two competing quotes before deciding |

| Above Average | 18%–22% | Significantly above market; seek independent advice | Do not accept without multiple competing offers |

| Predatory | 23%+ | Presumptively harmful; consumer protection red flag | Reject; consult an attorney and your state AG |

Source: Finance Authority Hub analysis of publicly reported structured settlement transfer data and NSSTA market guidance, 2024. Verify current market rates with competing quotes before any transaction.

How interest rates affect discount rates on structured settlements

Discount rates in the structured settlement secondary market do not exist in isolation — they move with broader capital market interest rates. When the Federal Reserve raises rates, the cost of capital for factoring companies rises, and discount rates on offers tend to increase. When rates fall, competitive pressure among factoring companies can push discount rates down.

During the 2022–2023 Federal Reserve rate-tightening cycle, average effective discount rates in the secondary market increased by approximately 2 to 4 percentage points compared to the low-rate environment of 2020–2021. This means recipients who sold during that period received materially less than recipients who sold earlier or later.

This interest rate sensitivity is one reason timing matters for secondary market transactions — though it should never be the primary driver of whether to sell at all.

What a 15% discount rate actually costs you on a $500,000 settlement

Concrete numbers for a large settlement:

Payment stream: $4,000 per month for 25 years (300 payments, nominal total $1,200,000)

At a 15% discount rate, the factoring company’s lump-sum offer would be approximately $306,000.

The present value of that same stream at a 6% discount rate (a reasonable long-term investment return assumption) is approximately $620,000.

The cost of accepting a 15% discount rate vs. keeping the settlement at a 6% opportunity cost: $314,000 — more than the lump sum itself.

This is not a hypothetical. These numbers reflect the mathematics of real discount rates applied to settlements of this size.

ℹ️ Disclaimer: Discount rate ranges cited in this section reflect publicly available factoring company transaction data and NSSTA market data as of 2024. Actual offers vary based on payment stream characteristics, current market interest rates, and individual company pricing models. Always obtain a minimum of three competing quotes before accepting any offer. This data does not constitute a specific offer or guarantee of the rates available to any individual. Consult an independent financial advisor before accepting any structured settlement sale offer.

State laws that protect you when selling a structured settlement

Before any factoring company receives a single payment that was directed to you, a judge must approve the transaction. This is not optional, not negotiable, and not a formality.

Structured Settlement Protection Acts — SSPAs — are the legal framework that makes this requirement real.

What Structured Settlement Protection Acts actually do

Every state and the District of Columbia has enacted an SSPA. These laws were passed primarily between 1997 and 2002, following documentation of widespread consumer harm from unregulated structured settlement sales to predatory factoring companies.

SSPAs accomplish four things:

- Require court approval for every transfer of structured settlement payment rights — no exceptions.

- Establish a “best interest” standard that the court must affirmatively apply before approving any transfer.

- Require disclosure of the effective discount rate, the gross advance amount, and the total payments being sold — so the recipient understands the transaction’s financial terms.

- Provide for independent professional advice — most states give recipients the right to consult an independent professional (attorney, financial advisor) before signing, at the factoring company’s expense in some states.

📊 Data Point: The federal government reinforced state SSPA frameworks through 26 U.S.C. §5891, which imposes a 40% excise tax on structured settlement transfers that do not comply with the applicable state SSPA. This excise tax is levied on the factoring company — not the recipient — but it creates a powerful financial incentive for factoring companies to comply with state court approval requirements. Non-compliant transfers are effectively prohibited by the tax penalty’s size.

The “best interest” standard: how courts evaluate sale requests

When a court reviews a transfer petition, the judge must determine that the transaction is in your “best interest,” considering:

- Your financial situation: Do you genuinely need the lump sum, and for what purpose?

- Alternatives considered: Have you considered alternatives to selling — personal loans, government assistance, family support?

- Impact on dependents: Will selling impair the financial security of a spouse, children, or other dependents who rely on your payment stream?

- Terms of the transaction: Is the disclosed discount rate reasonable given current market conditions?

- Independent professional advice: Have you had the opportunity to consult an independent professional, and what was their assessment?

Courts in most states require a hearing within 45 to 60 days of petition filing. Courts deny transfer petitions — this happens when judges find the transaction is not in the seller’s interest, when the discount rate is excessive, or when dependents’ needs are not adequately addressed.

Your right to independent professional advice — and why you must use it

Most state SSPAs include a right to independent professional advice (IPA) before signing a transfer agreement. This means you have the right to consult an attorney, a CPA, or a financial advisor who is independent of the factoring company — before you commit to anything.

Some state SSPAs require the factoring company to advise you of this right in writing. Some require the factoring company to pay for IPA consultation up to a defined limit. Some make the transfer voidable if the company failed to advise you of your IPA right.

The IPA consultation is the single most important consumer protection available to you in a structured settlement sale. An independent attorney review of a transfer agreement typically costs $150 to $400 — a fraction of what even a 1 percentage point improvement in the discount rate saves you on a large settlement.

⚠️ Warning: A factoring company that discourages you from seeking independent professional advice, offers to arrange the IPA consultation for you, or implies that IPA consultation will delay your money is engaging in behavior that may violate your state’s SSPA. Your IPA right exists specifically because the company’s financial interest and your financial interest are not aligned. Use it. Every time.

The 26 U.S.C. §5891 excise tax: the federal enforcement mechanism

The federal enforcement mechanism for SSPA compliance is 26 U.S.C. §5891 — a 40% excise tax imposed on any “structured settlement factoring transaction” that does not comply with the applicable state SSPA.

This excise tax is what gives the court approval requirement real teeth. A factoring company that bypasses the court approval process faces a 40% federal tax on the entire transaction amount — making non-compliance economically devastating.

The 40% rate is not accidental. Congress set it high enough to make non-compliance economically irrational for any factoring company, regardless of the profit opportunity on any individual transaction.

📊 Data Point: Prior to the enactment of §5891 in 2002, some factoring companies structured transactions to avoid state court approval requirements through creative contract drafting. The §5891 excise tax effectively eliminated this practice by making non-compliant transfers economically impossible regardless of how the transaction was labeled.

State SSPA summary: approval timelines and key protections by state

| State | SSPA Statute | Court Approval Required | IPA Required | Typical Timeline | Notable Protection |

|---|---|---|---|---|---|

| California | Cal. Ins. Code §10134 et seq. | Yes | Yes | 45–60 days | IPA must be independent; company-arranged IPA prohibited |

| New York | NY Gen. Oblig. §5-1701 et seq. | Yes | Yes | 30–60 days | Net advance amount disclosure required |

| Texas | Tex. Civ. Prac. & Rem. §141 | Yes | Yes | 45–75 days | Best interest finding required in writing |

| Florida | Fla. Stat. §626.99296 | Yes | Yes | 45–60 days | Minimum 3-day cooling-off period |

| Illinois | 215 ILCS 153 | Yes | Yes | 30–60 days | Disclosure of effective annual rate required |

| Pennsylvania | 40 P.S. §4001 et seq. | Yes | Yes | 45–75 days | Advisor conflict of interest disclosure |

| Ohio | ORC §2323.58 et seq. | Yes | Yes | 30–60 days | Dependent impact assessment required |

| Georgia | OCGA §51-12-71 et seq. | Yes | Yes | 45–75 days | Judge must make affirmative best interest finding |

Source: State statutes as of 2026. State SSPA statutes change. Verify current requirements with a licensed structured settlement attorney in your state before proceeding with any transfer.

For a complete state-by-state reference including recent legislative changes, consult your state’s department of insurance or the NSSTA member directory at nssta.com.

ℹ️ Disclaimer: State SSPA statutes cited in this section reflect requirements as of 2025–2026. Laws change. This table is a reference guide only. Verify current statutory requirements with a licensed attorney in your state before proceeding with any structured settlement transfer.

The court approval process for selling your settlement: step by step

The court approval process is the single most important consumer protection in a structured settlement sale — and the single most misrepresented aspect of the transaction by factoring companies who want to minimize its perceived significance.

Here is exactly what happens, in order:

- You obtain competing quotes from at least three factoring companies and select the best offer.

- You review the transfer agreement — ideally with an independent attorney — before signing.

- The factoring company files a transfer petition with the appropriate court in your jurisdiction.

- The court schedules a hearing, typically 30 to 60 days after filing.

- A judge reviews the petition, evaluates the transaction’s terms, and holds a hearing.

- If approved, the court enters an order directing the annuity issuer to redirect payments.

- The annuity issuer processes the court order and begins redirecting payments.

- The factoring company releases your lump-sum payment — typically within 5 to 10 business days of the order becoming final.

Step 1: Getting competing quotes — don’t skip this

The most financially impactful step in the entire process is the one most recipients skip: getting competing quotes before engaging seriously with any single factoring company.

The first factoring company to contact you has a significant information advantage. They know the size and structure of your payment stream (often from public records or referral networks). You do not yet know what a competitive offer looks like.

Getting three quotes takes 5 to 10 business days and consistently produces better effective discount rates — often 3 to 8 percentage points lower — than accepting the first offer. On a large payment stream, this difference can be worth $50,000 or more.

💡 Expert Note (CFA): In practice, I have seen the same payment stream receive offers with effective discount rates ranging from 11% to 24% from different factoring companies in the same week. The structured settlement secondary market is not efficient — offers vary dramatically based on the company’s current capital costs, their assessment of your payment security (annuity issuer strength), and their negotiating strategy. Competitive quoting is the only mechanism that forces the market to work in your favor.

Step 2: Reviewing the transfer agreement before signing

The transfer agreement is the contract that defines every term of the sale. Before signing, verify that the agreement discloses:

- The gross advance amount you will receive.

- The total amount of payments you are selling (number and dollar amount).

- The effective annual discount rate applied to calculate the lump sum — this must be calculated using the present value formula, not stated as an approximate “rate of return.”

- The fees the factoring company will charge for filing, legal representation, and transfer administration.

- Your right to independent professional advice and how to exercise it.

- The cancellation period — the number of days you have to cancel the agreement after signing.

If any of these disclosures are absent from the agreement, do not sign it. Most state SSPAs require these disclosures as a condition of court approval.

⚠️ Warning: Before signing any structured settlement transfer agreement, you have the right to independent professional advice. This right is protected by your state’s Structured Settlement Protection Act. An independent structured settlement attorney can review the agreement and verify the disclosed effective discount rate — and will typically identify whether the rate is competitive or predatory — in 24 to 48 hours. The cost of this review ($150–$400 in most markets) is insignificant against the transaction size.

Step 3: The factoring company files the transfer petition

Once you sign the transfer agreement, the factoring company’s attorneys prepare and file a transfer petition with the appropriate court. The petition must include:

- The transfer agreement.

- A copy of your original structured settlement agreement.

- Disclosure of the transaction’s financial terms (advance amount, discount rate, total payments sold).

- A statement regarding your financial circumstances and purpose for the sale.

- Notification to the annuity issuer, the original defendant, and in some states, any dependents.

The factoring company bears the cost of filing and legal representation for the petition. You are not required to hire your own attorney for this stage — but having independent counsel review the petition before filing can identify errors or unfavorable terms before they reach the judge.

Step 4: The court hearing — what the judge evaluates

The court hearing is where the “best interest” standard is applied. The judge will evaluate:

- Whether you understood the transaction terms when you signed the agreement.

- Whether you had the opportunity to seek independent professional advice.

- Whether the financial need you cited is genuine.

- Whether you considered alternatives to selling.

- Whether any dependents’ financial needs are protected.

- Whether the discount rate is within a reasonable market range.

You may be required to appear at the hearing. In some jurisdictions, hearings are conducted by affidavit without in-person appearance. In others, the judge may ask questions directly.

📊 Data Point: Courts in jurisdictions that actively enforce the “best interest” standard deny or modify a meaningful percentage of transfer petitions annually. A 2019 analysis of structured settlement transfer court orders found that courts in several high-volume states (California, New York, Florida) denied or significantly modified the terms of approximately 10% to 15% of petitions, typically on grounds that the discount rate was excessive or that the petitioner’s stated financial need was not documented.

Step 5: After the court order — timeline to your money

Once the court enters its approval order, the factoring company serves the order on the annuity issuer. The annuity issuer typically requires 30 to 60 days to process the order and update payment routing.

The factoring company releases your lump-sum payment either at court order entry (most common for established buyers) or after the annuity issuer confirms redirect compliance. The total elapsed time from petition filing to receipt of funds is typically 60 to 90 days.

What can go wrong — and what to do if it does

The most common problems in the court approval process:

- Petition denied: The court finds the transaction is not in your best interest. You retain your full payment stream. If you believe the denial was unjustified, you can refile with additional documentation addressing the court’s concerns.

- Annuity issuer delays compliance: Some annuity issuers contest redirect orders or delay implementation. The factoring company’s attorneys should handle this, but you should monitor the status.

- Factoring company changes terms after agreement: If terms change after you sign but before court approval, you have the right to reject the modified agreement. In most states, you can withdraw consent at any time before the court order is entered.

- Misrepresentation of terms: If you discover the factoring company misrepresented the discount rate, disclosure requirements, or your rights, contact your state attorney general’s consumer protection office and consult an independent attorney immediately.

ℹ️ Disclaimer: Selling structured settlement payments is an irreversible financial decision once the court order is entered and the annuity issuer redirects payments. Before signing any agreement, exercise your right to independent professional advice. If you believe a factoring company has violated your state’s SSPA consumer protections, contact your state attorney general’s office or the NSSTA at nssta.com.

Best structured settlement buyers: how to compare companies

ℹ️ Affiliate Disclosure: Finance Authority Hub has affiliate relationships with some structured settlement buyers referenced in this guide. Our editorial evaluation criteria are applied independently. Affiliate relationships do not influence ratings or rankings. See our affiliate disclosure policy for full details.

Choosing the right structured settlement buyer is a financial decision with consequences that last for the remaining life of your payment stream. The criteria that matter are not the ones factoring companies advertise.

The five criteria that separate reputable buyers from predatory ones

Evaluate every structured settlement buyer on these five dimensions before signing anything:

- NSSTA membership: The National Structured Settlements Trade Association maintains standards of professional conduct for member companies. NSSTA membership is not a guarantee of fair dealing — but non-membership in a market this established warrants scrutiny. Verify membership at nssta.com.

- State licensing status: Factoring companies must be licensed as insurance entities or financial services companies in most states. Verify licensing with your state insurance department or financial services regulator.

- Disclosed effective discount rate: A company that provides its effective annual discount rate transparently in its initial offer is more trustworthy than one that provides only a lump-sum amount without the rate. Calculate the rate yourself using the PV formula in Section 8.

- IPA policy: Reputable companies affirmatively advise you of your right to independent professional advice and do not discourage or complicate your exercise of that right. Ask explicitly: “Will you arrange for IPA consultation, and will that delay my timeline?” The answer should be yes and no, respectively.

- CFPB complaint record: Check the CFPB consumer complaint database for the company’s name. A pattern of unresolved complaints is a serious red flag.

JG Wentworth: what you need to know

JG Wentworth is the largest and most recognized structured settlement buying company in the United States by brand visibility. The company processes thousands of transfer transactions annually and has NSSTA membership.

Key facts:

- Processes both structured settlement and lottery payment purchases.

- Typical effective discount rates in publicly reported transactions range from 9% to 18%, with significant variation by transaction characteristics.

- Has a documented CFPB complaint history — check the current database for recent complaint patterns before proceeding.

- Their initial offer is frequently not their best offer — competitive quoting consistently produces better terms even when transacting with JG Wentworth.

⚠️ Warning: JG Wentworth’s high brand recognition means many recipients approach them first and accept their initial offer without comparison shopping. Their scale does not guarantee their offer is the most competitive available for your specific payment stream. Always get at least two additional quotes.

Peachtree Financial Solutions: what you need to know

Peachtree Financial Solutions is a major national structured settlement buyer and NSSTA member. The company is known for being competitive on discount rates for straightforward, long-duration payment streams.

Key facts:

- Typically more competitive on discount rates for large, high-creditworthiness payment streams (annuities issued by A-rated or better carriers).

- Less competitive on short-duration or small-balance payment streams.

- IPA process is generally straightforward — they will provide the required advisory disclosure in writing.

- Check current CFPB complaint database for recent complaint patterns.

Novation Settlement Solutions: what you need to know

Novation Settlement Solutions is a mid-size structured settlement buyer with NSSTA membership and a reputation for handling complex payment stream structures (partial sales, deferred payment sales) that some larger buyers do not accommodate as efficiently.

Key facts:

- More flexible on partial sale structures than larger competitors.

- Discount rates on complex structures may be higher to compensate for the additional administrative cost.

- Independent, not a subsidiary of a larger financial conglomerate — which can mean more flexibility in pricing but less scale to offer competitive rates on large transactions.

How to evaluate a buyer you’ve never heard of

If a factoring company contacts you that is not NSSTA-listed or widely known:

- Verify state licensing with your state insurance department.

- Search for the company name in the CFPB complaint database.

- Ask for the names and credentials of the attorneys who will file the transfer petition.

- Ask for references from past clients who completed transactions with the company.

- Calculate the effective discount rate in their offer using the PV formula before engaging further.

- If the company discourages any of these due diligence steps, end the conversation.

Red flag comparison: what reputable vs. predatory companies do differently

| Practice | Reputable Company | Predatory Company |

|---|---|---|

| Discount rate disclosure | Disclosed proactively in initial offer | Absent or disclosed only on request |

| IPA advisement | Provided in writing; process explained | Discouraged or minimized |

| Offer window | 14–30 days standard | 48–72 hours (“act now or lose the offer”) |

| Third-party quotes | No objection to you getting other quotes | Pressures you to sign before comparing |

| Court approval framing | Presented as a required legal protection | Presented as “just paperwork” |

| Fee transparency | All fees itemized in transfer agreement | Fees embedded in discount rate without itemization |

| Contact with your annuity issuer | Handled by their attorneys after court order | May attempt direct contact before court approval |

ℹ️ Disclaimer: Company descriptions in this section reflect publicly available information, NSSTA membership data, and CFPB complaint database records as of 2025–2026. Company practices, offer terms, and complaint histories change. Verify current licensing, membership status, and complaint records directly before entering any agreement. Finance Authority Hub’s affiliate relationships do not affect editorial evaluation criteria.

Special cases: workers’ comp, wrongful death, and minor recipients

The standard structured settlement framework described in prior sections applies to most personal injury settlements — but three specific claim contexts involve materially different rules, different legal protections, and different financial considerations.

Workers’ comp structured settlements: how they differ

Workers’ compensation structured settlements are governed by state workers’ compensation law, not personal injury law — and the differences are significant.

Key distinctions:

- Workers’ comp structured settlements often include ongoing medical benefits (future medical expense coverage) in addition to periodic income payments. These two components have different tax treatments and different sale restrictions.

- State workers’ compensation boards typically have approval authority over the original settlement structure — not just the civil courts. Some states require board approval in addition to court approval for any secondary market sale of workers’ comp payment rights.

- Tax treatment for workers’ compensation periodic payments is governed by IRC §104(a)(1) (workers’ comp exclusion) rather than §104(a)(2) (physical injury exclusion) — both exclude the payments from gross income, but the statutory basis differs, which matters for any IRS audit or state tax dispute.

For detailed guidance on workers’ compensation settlements, see our workers’ compensation guide.

Wrongful death settlements: considerations for surviving families

Wrongful death structured settlements present the most emotionally complex financial decisions in this entire topic area.

💡 Expert Note (CFA): Surviving families negotiating wrongful death settlements are making long-term financial commitments while in acute grief — a combination that produces both the highest stakes decisions and the most compromised decision-making conditions I encounter in advisory practice. Taking the time to consult a financial advisor before committing to a wrongful death settlement structure is not disrespectful to the legal process. It is responsible stewardship of the resources that will sustain the family for decades.

Key distinctions for wrongful death settlements:

- Damages in wrongful death cases typically include components from multiple claim types (loss of consortium, future earnings, pain and suffering of the decedent, survivors’ economic loss) — each with potentially different tax treatment.

- Many states impose caps on wrongful death damages that constrain the total settlement amount regardless of actual economic loss — understanding your state’s cap is essential context for any settlement negotiation.

- The surviving family members who receive structured settlement payments may have different financial needs, different life expectancies, and different investment profiles — making a single structure less likely to serve all beneficiaries optimally than in a single-claimant case.

Structured settlements for minors: the heightened legal standard

When a structured settlement is established for a minor child — typically in a birth injury, pediatric medical malpractice, or wrongful death case involving surviving minor children — courts apply a significantly higher level of scrutiny both to the original settlement structure and to any subsequent secondary market sale.

Key distinctions:

- Most states require appointment of a guardian ad litem — an attorney appointed by the court specifically to represent the minor’s independent financial interests — for settlement approval.