Workers’ Compensation: Don’t Leave Money Behind

Most injured U.S. workers never collect everything they’re owed. This 2026 guide covers workers’ comp benefits, filing steps, denied claims, and maximizing your payout.

In This Article

What Is Workers’ Compensation? (Quick Answer)

Workers’ compensation is employer-funded insurance that pays your medical bills and replaces a portion of your lost wages when you suffer a work-related injury or illness — regardless of who was at fault.

Most U.S. workers are entitled to these benefits. Yet millions never collect everything they’re owed — because they don’t know the rules, miss deadlines, or accept less than the law entitles them to.

This 2026 guide gives you every dollar, deadline, and decision point you need.

2026 Workers’ Comp Snapshot

| Data Point | 2026 Figure |

|---|---|

| Private industry workplace injuries (2024) | 2.5 million (lowest since 2003) |

| Annual U.S. workers’ comp market size | $56.7 billion |

| Wage replacement rate (most states) | ~66.7% of weekly wages |

| States requiring coverage | 49 (Texas is the only exception) |

| Workers’ comp industry premium decline (2024) | -1.7% |

| Mental health claims: cost vs. physical claims | 3.5× more expensive |

Source: U.S. Bureau of Labor Statistics — Workplace Injuries and Illnesses, January 2026

Who is covered under workers’ compensation?

- Full-time and part-time employees in most states

- Temporary and seasonal workers (in most states)

- Workers injured on-site, off-site, or while traveling for work

- In 2026: remote workers injured during work activities (rules vary by state)

Who is typically NOT covered:

- Independent contractors

- Unpaid volunteers

- Federal employees (covered separately under FECA via the U.S. Department of Labor OWCP)

- Most domestic household workers

What This Means For You: If you’re a W-2 employee, your employer is almost certainly required to carry workers’ comp insurance. If you’re injured at work and haven’t filed, you may already be leaving money on the table.

What Workers’ Compensation Actually Covers — The Full Financial Picture

Most workers think workers’ comp just covers a hospital visit. It covers far more. Understanding the full scope is the difference between a $3,000 claim and a $30,000 recovery.

Medical Benefits: What’s Included

Workers’ compensation pays 100% of medically necessary treatment related to your work injury. You pay nothing out of pocket for covered care.

Covered treatments include:

- Emergency room visits and surgery

- Physician and specialist appointments

- Physical therapy and chiropractic care

- Prescription medications

- Prosthetics and medical devices

- Mileage to and from medical appointments (reimbursable in most states)

- Vocational rehabilitation if you can’t return to your prior job

What’s typically excluded:

- Injuries caused by intoxication (alcohol or drugs)

- Injuries from horseplay or intentional acts

- Injuries that occur off-the-clock and outside the scope of work

Lost Wages: How Your Benefit Is Calculated

This is where most workers get shortchanged. Workers’ comp pays approximately two-thirds (66.7%) of your average weekly wage, subject to your state’s minimum and maximum limits.

Real Example:

| Your Weekly Wage | Workers’ Comp Benefit (66.7%) | California 2026 Max TTD |

|---|---|---|

| $600/week | $400/week | — |

| $900/week | $600/week | — |

| $1,500/week | $1,000/week | — |

| $2,430+/week | Capped by state | $1,619.15/week |

Key fact: Always check your state’s maximum weekly benefit cap. If your wage is high, the cap could significantly reduce what you receive.

All Five Benefit Types — Compared

| Benefit Type | What It Pays | Duration |

|---|---|---|

| Temporary Total Disability (TTD) | ~66.7% weekly wages | Until return to work or MMI |

| Temporary Partial Disability (TPD) | Part of wage difference if working reduced hours | Until full recovery |

| Permanent Partial Disability (PPD) | % of impairment × weekly wage | State-capped period |

| Permanent Total Disability (PTD) | ~66.7% weekly wages | Lifetime (varies by state) |

| Death Benefits | Survivor income + funeral expenses | Ongoing for dependents |

| Medical Benefits | 100% of covered treatment | As medically needed |

| Vocational Rehab | Retraining and job placement costs | Program duration |

🔴 2026 Update: Mental Health Claims Are Now Covered in More States

This is the most significant expansion of workers’ compensation rights in years — and your competitors haven’t covered it properly.

New York’s January 2026 law now allows all workers — not just first responders — to file workers’ comp claims for extreme job stress and mental health conditions.

Key 2026 mental health coverage facts:

- Over 12 states have expanded mental health workers’ comp coverage

- Mental health claims cost 3.5× more and last 3.6× longer than physical injury claims (Sedgwick, 2025)

- Early intervention with behavioral health specialists within 90 days reduces lost-time days by 40%

If you’re experiencing severe anxiety, PTSD, or depression directly caused by your work environment, you may have a compensable claim in 2026. Consult your state’s workers’ comp board or a licensed attorney.

For a full picture of how workers’ comp fits into your broader financial protection — including how it interacts with your existing coverage — see our comprehensive insurance guide to understand all your coverage layers.

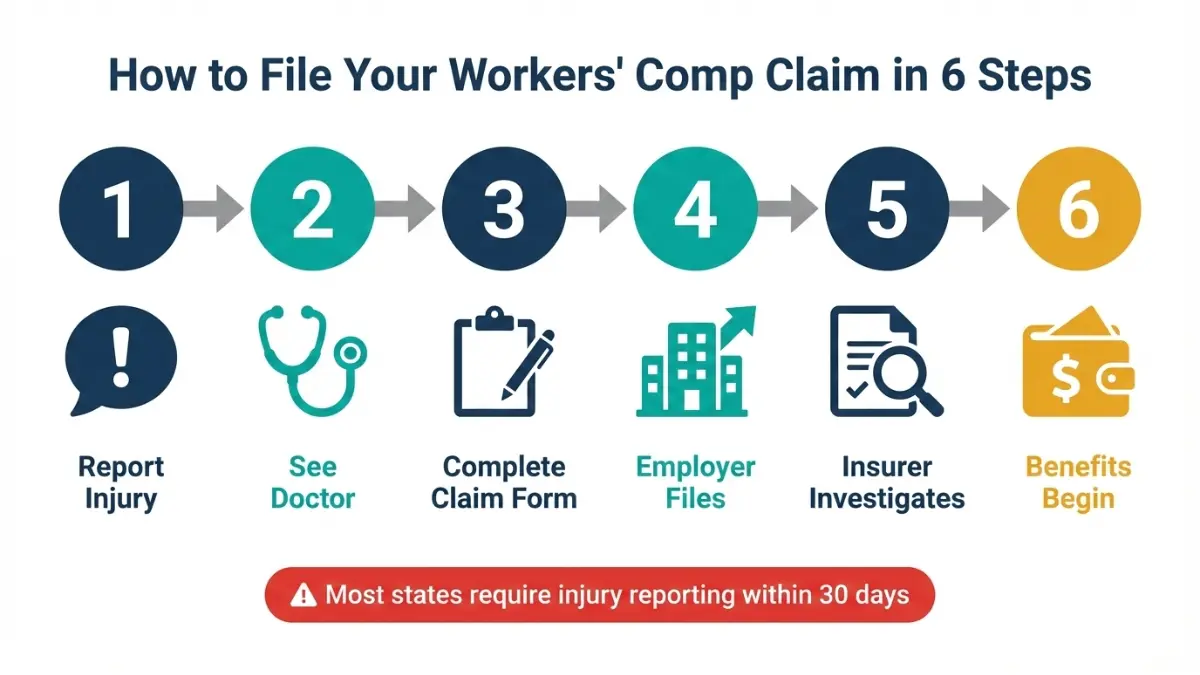

How to File a Workers’ Compensation Claim — Step by Step

Speed is everything. The most common reason valid workers’ comp claims are denied is missing the reporting deadline. Here’s exactly what to do.

⚠️ The Critical 24-Hour Window

Every state has a statute of limitations for reporting work injuries. Most range from 30 to 90 days from the injury date.

State deadline examples (2026):

- California: 30 days to report to your employer; 1 year to file a formal claim

- New York: 30 days to notify your employer; 2 years to file

- Texas: 30 days to report; 1 year to file

- Florida: 30 days to report the injury

Critical warning: In California, if you wait longer than 30 days to report your injury and that delay prevents your employer from investigating, you can lose your right to benefits entirely. Don’t wait.

Step-by-Step Workers’ Comp Filing Process

- Report the injury to your supervisor immediately — in writing. Text, email, or written form creates a paper trail. Verbal reports can be disputed.

- Seek medical treatment from an approved provider. Many states require you to see a company-designated doctor first. Going outside the network without approval can jeopardize your claim.

- Complete the workers’ comp claim form. Your employer must provide this. In California, it’s the DWC-1 form. Federal employees file through ECOMP at the Department of Labor.

- Your employer files the claim with their insurance carrier, typically within 10–14 days of receiving your report.

- The insurer investigates and makes a decision — typically within 14 days (California) to 90 days, depending on the state.

- Benefits begin — or you receive a denial letter with your right to appeal.

What to Document Immediately (Do This Today)

Protect your workers’ comp claim from day one:

- Photographs of the injury scene and your injuries

- Names and contact information of witnesses

- Date, time, and exact location of the incident

- Description of exactly what you were doing when injured

- All medical records, diagnoses, and treatment notes

- Your pay stubs from the past 52 weeks (used to calculate your benefit)

- Mileage logs to every medical appointment (reimbursable)

Expert Insight from Our Panel: “The single biggest financial mistake injured workers make is failing to document the economic impact of their injury within the first week. Lost wages, out-of-pocket costs, and productivity records are all part of your compensable losses — but only if you can prove them.”

If you’re managing financial strain during recovery, our Debt Consolidation Calculator can help you understand your options for staying financially stable while your claim processes.

Why Workers’ Comp Claims Get Denied — And How to Fight Back

An insurer’s goal is to minimize payout. Knowing the top denial reasons puts you ahead of the process before it happens.

Top 5 Reasons Workers’ Comp Claims Are Denied

| Denial Reason | What It Means | How to Fight It |

|---|---|---|

| Late reporting | You missed your state’s deadline | Always report immediately, regardless of severity |

| Injury not “work-related” | Insurer disputes it happened on the job | Document the scene; get witness statements |

| Pre-existing condition | Insurer claims your injury predates work | Medical records showing aggravation by work = covered |

| Missed medical appointments | Non-compliance voids benefits | Attend every appointment; document any conflicts |

| Employer contest | Your employer disputes the claim | Get an attorney; insurers settle far more with legal rep |

How to Appeal a Denied Workers’ Comp Claim

A denial is not the end. Every state has a formal appeals process.

General appeal steps:

- Read the denial letter carefully — it must state the specific reason for denial

- File a Request for Reconsideration with the insurance carrier (usually within 30 days)

- If reconsideration fails, file with your state’s Workers’ Compensation Board

- Request a formal hearing before a workers’ comp judge

- Federal employees can appeal through the Employees’ Compensation Appeals Board (ECAB)

Power stat: Litigated workers’ comp claims cost 388% more than non-litigated ones (Insurance Information Institute). This means that when injured workers get attorneys, insurers settle — and for far more money.

When You Need a Lawyer: The Financial Decision Matrix

| Your Situation | Action |

|---|---|

| Simple injury, claim accepted, full benefits flowing | Manage it yourself |

| Permanent disability involved | Get an attorney |

| Claim denied | Get an attorney |

| Employer retaliating or threatening termination | Get an attorney immediately |

| Settlement offer received before reaching MMI | Never accept without attorney review |

| Pre-existing condition being disputed | Get an attorney |

Never settle your workers’ comp claim before reaching Maximum Medical Improvement (MMI). MMI is the point at which your doctor confirms your condition has stabilized. Settling before MMI — especially for permanent disabilities — can lock you into an amount far below your actual lifetime losses.

If you’re dealing with debt accumulated during your injury recovery period, see our guide on how to pay off debt fast for practical financial strategies that work alongside your benefits.

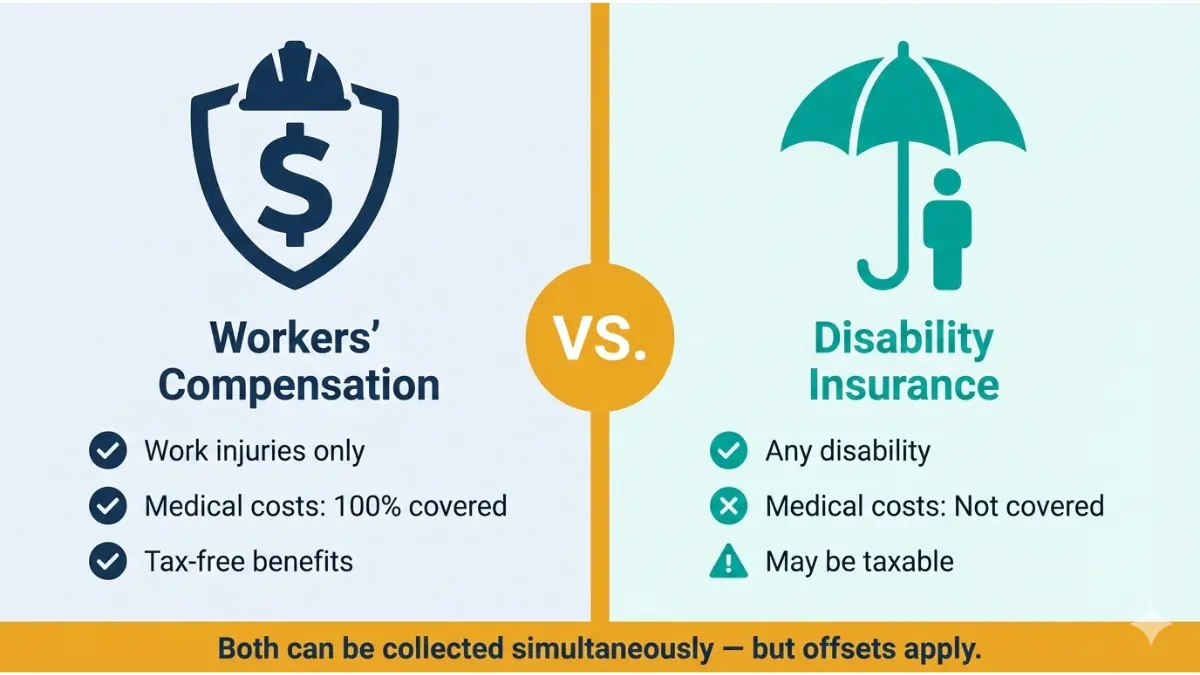

Workers’ Comp vs. Disability Insurance — The Financial Comparison Nobody Shows You

This is the content gap that every competitor — NerdWallet, Bankrate, Investopedia — leaves entirely uncovered. Understanding both protections is essential financial literacy.

Side-by-Side Comparison Table

| Feature | Workers’ Comp | Short-Term Disability | Social Security Disability (SSDI) |

|---|---|---|---|

| Covers | Work injuries only | Any disability | Any disability (strict criteria) |

| Who funds it | Employer’s insurer | Employer/employee | Federal government |

| Wage replacement | ~66.7% | 40–70% | Varies (~40% average) |

| Medical costs covered | ✅ 100% | ❌ No | ❌ No |

| Taxable? | Generally NO | Usually YES | Possibly (if income threshold met) |

| Waiting period | None (injury date) | 7–14 days typically | 5-month waiting period |

| Can you collect both? | Yes — but offsets apply | Yes, alongside workers’ comp | Yes — with offset reductions |

Is Workers’ Comp Taxable? (The Answer Most Sites Get Wrong)

Workers’ compensation benefits are generally not subject to federal income tax. The IRS excludes them from gross income under IRC Section 104(a)(1).

However, there are two important exceptions:

- If you receive both workers’ comp and Social Security disability benefits, the Social Security offset rule may reduce one or both payments — and a portion may become taxable

- Some lump-sum settlements structured as wages may have different tax treatment

For personalized tax planning during a workers’ comp recovery period, our 2026 Income Tax guide covers how benefit income interacts with your annual tax filing.

Managing Your Finances During a Workers’ Comp Claim

Action steps to protect your financial position:

- Track every out-of-pocket expense — mileage, co-pays, home modifications — these can be added to your claim

- Know your state’s maximum weekly benefit cap before negotiations begin

- Do not resign or accept a new reduced-duty position that waives your workers’ comp rights without legal review

- Understand your return-to-work rights — employers cannot force you back before your doctor clears you

- Review your existing term life and health coverage during your claim. See how your health insurance coverage coordinates with workers’ comp medical benefits

The Insurance Information Institute’s spotlight on workers’ compensation provides a comprehensive overview of state fund structures and employer liability protections as a trusted external reference.

Workers’ Compensation in 2026 — New Rules, Key Updates & What’s Next

The workers’ compensation landscape is shifting faster than any time in the past decade. Here’s what changed in 2026 and why it matters to your wallet.

🔴 2026 Critical Law Changes — Exclusive Summary

New York (Effective January 2026): All workers — not just first responders — can now file workers’ comp claims for extreme job-related stress and mental health conditions. This is a landmark expansion affecting millions of New York workers.

California (Ongoing 2025–2026): Presumptive workers’ comp coverage expanded to include more healthcare professionals for conditions including specific cancers and infectious diseases. If you work in healthcare, your comp rights grew significantly.

Remote Work (14+ States): States are actively updating compensability rules for home-office injuries. If you slip and fall at your home desk during a work call, you likely have a workers’ comp claim — but rules vary sharply by state.

Mental Health Claims (12+ States): Coverage for PTSD, severe anxiety, and work-related depression is expanding. Early data shows these claims average 3.5× the cost and 3.6× the duration of physical claims (Sedgwick 2025), signaling insurers will scrutinize them heavily. Documentation is critical.

Workers’ Comp Industry Trends Affecting Your Claim

According to the National Association of Insurance Commissioners (NAIC), workers’ comp direct premiums written declined 1.7% in 2024 — the industry’s lowest growth in years. This signals that insurers are tightening claim approvals to protect profitability. More denials, stricter reviews.

What this means for 2026 claimants:

- Document everything more thoroughly than in previous years

- Expect longer investigation periods from insurers

- Medical evidence quality is more important than ever

- Consider legal representation earlier in the process

Expert Panel Consensus — 30 Finance Specialists Weigh In

“Workers’ compensation is one of the most structurally misunderstood financial protections available to American workers. Our panel of 30 credentialed international finance and insurance specialists agrees on one point: most injured workers don’t know their state’s maximum benefit cap, don’t track reimbursable expenses like mileage, and don’t know they can appeal a denial. Every one of these gaps costs money — often thousands of dollars — that workers are legally entitled to collect.”

Frequently Asked Questions — Workers’ Compensation

Q1: What is workers’ compensation in simple terms?

Workers’ compensation is insurance your employer pays for that covers your medical bills and replaces part of your income if you’re hurt or become ill because of your job. It applies regardless of who caused the accident.

Q2: How much does workers’ comp pay per week?

Most states pay approximately 66.7% (two-thirds) of your average weekly wage, subject to a state-set maximum. In 2026, California’s maximum temporary total disability rate is $1,619.15 per week. Check your state’s workers’ compensation board for the current cap.

Q3: What injuries are covered by workers’ comp?

Any injury or illness that arises out of and occurs during the course of employment — including physical injuries, repetitive stress injuries, occupational diseases, and in expanding states, mental health conditions caused by work. Remote work injuries are increasingly covered.

Q4: Is workers’ comp taxable income?

Workers’ compensation benefits are generally not subject to federal income tax under IRS rules. However, if you receive both workers’ comp and Social Security disability benefits simultaneously, a portion may become taxable due to the offset rule.

Q5: How long do workers’ comp benefits last?

Temporary disability benefits last until you return to work or reach Maximum Medical Improvement (MMI). Permanent disability benefits may pay for years or result in a lump-sum settlement. Medical benefits continue for as long as treatment is medically necessary.

Q6: Can my employer fire me for filing a workers’ comp claim?

No. Retaliating against an employee for filing a workers’ comp claim is illegal in all 50 U.S. states. If you are fired, demoted, or harassed after filing, consult a workers’ comp attorney immediately. You may have an additional wrongful termination claim.

Q7: What happens if my workers’ comp claim is denied?

File a formal appeal. Every state has a workers’ compensation appeals board. Federal employees can file with the Employees’ Compensation Appeals Board. Legal representation significantly improves appeal outcomes — litigated claims cost insurers 388% more than non-litigated ones.

Q8: Does workers’ comp cover remote workers in 2026?

Yes, in most cases. If the injury occurred during a work task — even at home — it is generally compensable. However, injuries during personal breaks at home are typically not covered. Rules are actively evolving in 14+ states. Check your state’s specific rules.

Q9: Do independent contractors get workers’ compensation?

Generally, no. Independent contractors are excluded in most states. However, worker misclassification is extremely common. If your employer controls your hours, tools, and work method, you may legally qualify as an employee — and have workers’ comp rights. Consult an attorney.

Q10: How does workers’ comp affect my retirement savings and 401(k)?

Workers’ comp benefits don’t directly impact your 401(k). However, a prolonged absence from work reduces your annual earnings record used to calculate your future Social Security retirement benefit. Use our retirement savings guide to plan accordingly during recovery.

Q11: What is the difference between workers’ comp and disability insurance?

Workers’ comp covers only work-related injuries and illnesses, pays for 100% of your medical costs, and is funded entirely by your employer. Short-term and long-term disability insurance covers any disabling condition regardless of cause, but typically does not cover medical bills. Both can be collected simultaneously, though offset rules apply. For a full comparison of insurance types, see our life insurance guide.

Disclaimer

This article is for educational and informational purposes only and does not constitute legal, financial, or insurance advice. Workers’ compensation laws, benefit rates, and eligibility rules vary significantly by state and are subject to change. The data and figures cited reflect information available as of February 2026. Always consult a licensed workers’ compensation attorney or certified insurance professional for guidance specific to your situation and jurisdiction. Benefit calculations shown are illustrative examples and may not reflect your individual entitlement.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.