Life Insurance: Costs, Types & What You Must Know

Most Americans overpay for life insurance — or skip it entirely. See real 2026 costs by age, all 4 policy types explained, and how much coverage you actually need.

In This Article

Quick Answer: Life insurance is a legal contract where you pay regular premiums to an insurer, and in return, the insurer pays a lump-sum death benefit to your chosen beneficiaries when you die. U.S. life expectancy is now 79.0 years (CDC, 2024), making this the single most important financial safety net most families will ever own.

What Is Life Insurance?

Life insurance is one of the most powerful financial protection tools available — yet most Americans misunderstand how it works, how much it costs, and whether they need it.

At its core, a life insurance policy is a simple promise: you pay a premium, and if you die during the policy period, your insurer pays a death benefit to your beneficiaries — tax-free in almost every case.

How Does a Life Insurance Policy Work?

The process breaks down into three clean steps:

- Step 1 — Apply: You submit a health questionnaire or take a medical exam. Your age, health, lifestyle, and coverage amount determine your premium.

- Step 2 — Pay Premiums: You pay monthly, quarterly, or annually. Missing payments can lapse your coverage.

- Step 3 — Death Benefit Pays Out: When you die, your named beneficiaries submit a claim. The insurer pays the agreed amount — typically within 30–60 days.

Key Takeaway: Life insurance replaces your income so your family can cover expenses, pay off debts, fund college, and maintain their standard of living — even after you’re gone.

According to the latest CDC mortality data, U.S. average life expectancy rose to 79.0 years in 2024. But the risk of dying unexpectedly before retirement remains real — and that’s exactly the financial gap that life insurance fills. To understand how your debts factor into your coverage calculation, explore our Debt Consolidation Calculator.

4 Main Types of Life Insurance — Which One Is Right for You?

Not all life insurance policies work the same way. Your choice depends on your age, budget, financial goals, and how long you need coverage.

Here is the full comparison — the one table competitors refuse to put on their pillar pages:

| Type | Coverage Period | Cash Value? | Avg. Monthly Cost (Age 35) | Best For |

|---|---|---|---|---|

| Term Life | 10–30 years | ❌ No | $25–$35 | Families, mortgages, budget-focused buyers |

| Whole Life | Lifetime | ✅ Yes (guaranteed) | $200–$400 | Estate planning, lifelong needs |

| Universal Life | Lifetime (flexible) | ✅ Yes (adjustable) | $150–$300 | Flexible premium needs |

| Indexed Universal Life (IUL) | Lifetime | ✅ Yes (market-linked) | $200–$350 | Wealth building + protection |

Term Life Insurance

Term life insurance is the most affordable and most widely purchased type in the U.S. — 48% of American policyholders own a term policy. It covers you for a fixed period (10, 15, 20, or 30 years) and pays out only if you die during that term.

- Pros: Lowest premiums, simple structure, easy to understand

- Cons: No cash value; coverage ends when the term expires

- Best for: New parents, homeowners with a mortgage, anyone needing maximum coverage at minimum cost

Our dedicated Term Life Insurance Rates Guide breaks down real 2026 premium data by age, health tier, and coverage amount.

Whole Life Insurance

Whole life insurance lasts your entire lifetime and builds cash value — a savings component that grows at a guaranteed rate (typically 2–3.75%). You can borrow against it or use it to pay premiums.

- Pros: Permanent coverage, predictable premiums, cash value growth

- Cons: Premiums are 5–10x higher than comparable term coverage

- Best for: High-net-worth individuals, parents with lifelong dependents, estate planning strategies

Universal Life Insurance

Universal life insurance is a permanent policy that offers premium flexibility. You can increase or decrease premiums within limits, and the death benefit can be adjusted over time.

- Pros: Flexible premiums, cash value potential, lifelong coverage

- Cons: More complex; poor management can cause policy lapse

- Best for: Business owners, individuals with variable income

Indexed Universal Life Insurance (IUL)

Indexed universal life (IUL) links your cash value growth to a stock market index like the S&P 500 — without direct market exposure. Returns are capped but protected from losses.

- Pros: Higher growth potential than whole life, downside protection

- Cons: Complex fee structures, capped returns, can be oversold

- Best for: Long-term wealth building combined with death benefit protection

What This Means For You: For most Americans under 50, term life insurance is the smartest starting point. If you’re building an estate or need lifelong coverage, consult a licensed advisor about permanent options.

Life Insurance Costs in 2026 — Real Numbers by Age

Here is the number every competitor buries or links away from. You deserve it upfront.

The #1 Myth Busted: According to LIMRA’s 2025 Insurance Barometer Study, more than half of Americans believe a $250,000 term life policy costs over $500 per year. The real cost for a healthy 30-year-old? Under $200 per year. People overestimate the price of life insurance by 3 to 5 times — and that misconception is why millions remain uninsured.

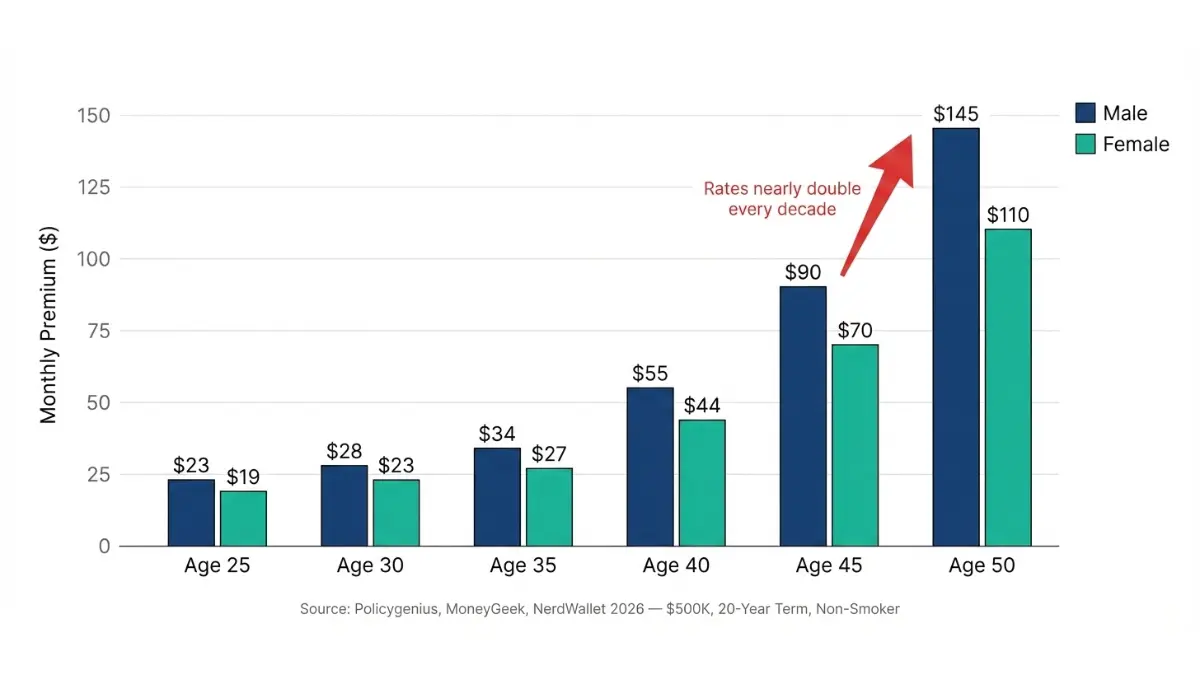

2026 Average Monthly Cost: $500K 20-Year Term Life (Non-Smoker)

| Age | Monthly Cost (Male) | Monthly Cost (Female) |

|---|---|---|

| 25 | ~$23 | ~$19 |

| 30 | ~$28 | ~$23 |

| 35 | ~$34 | ~$27 |

| 40 | ~$55 | ~$44 |

| 45 | ~$90 | ~$70 |

| 50 | ~$145 | ~$110 |

Sources: Policygenius 2026, MoneyGeek 2026, NerdWallet Average Rates Data

Note: Women consistently pay less because their life expectancy (81.4 years in 2024 per CDC) is higher than men’s (76.7 years), making them statistically lower-risk for insurers.

Whole Life Insurance vs. Term: The Real Cost Gap

A 40-year-old male pays approximately $55/month for $500K in term life coverage. The same man would pay $607–$679/month for whole life with the same death benefit — more than 10 times the cost.

What Factors Determine Your Life Insurance Premium?

Your insurer evaluates these risk factors before quoting your rate:

- Age — Rates nearly double every decade. Buying at 30 vs. 40 can save you $200+/month.

- Health status — Pre-existing conditions (diabetes, heart disease) raise premiums significantly

- Smoking status — Smokers pay 6 to 10 times more than non-smokers for life insurance

- Gender — Women pay less due to longer average life expectancy

- Coverage amount — More coverage = higher premium, but not always proportionally

- Term length — A 30-year term costs more than a 10-year term for the same coverage

- Occupation — High-risk jobs (firefighter, pilot, construction) can significantly increase rates

- Driving record — DUIs and major violations flag you as a higher-risk applicant

- Family medical history — Hereditary conditions can raise your premium tier

How to Lower Your Life Insurance Costs

- Buy early — The single biggest lever. A 25-year-old pays half what a 35-year-old pays for identical coverage

- Quit smoking — Non-smoker rates kick in after 12 months tobacco-free with most insurers

- Compare at least 3–5 quotes — Rates vary up to 40% between insurers for identical coverage

- Choose the right term length — Don’t over-insure; match your term to your actual financial obligations

- Get healthy before applying — Blood pressure, cholesterol, and BMI all affect your health classification

If you’re carrying debt that affects your coverage calculation, our Debt Consolidation Guide can help you reduce your financial obligations before applying.

How Much Life Insurance Do You Need? (3 Expert Formulas)

Most people guess their coverage amount. Financial experts calculate it. Here are the three methods advisors actually use — and a real case example that competitors never include.

Formula 1: The 10x Income Rule

Multiply your annual gross income by 10. This is the simplest starting point.

- Annual income: $75,000 × 10 = $750,000 in coverage

- Add $100,000 per child for education costs

This rule is quick but imprecise. Use it only as a floor, not a ceiling.

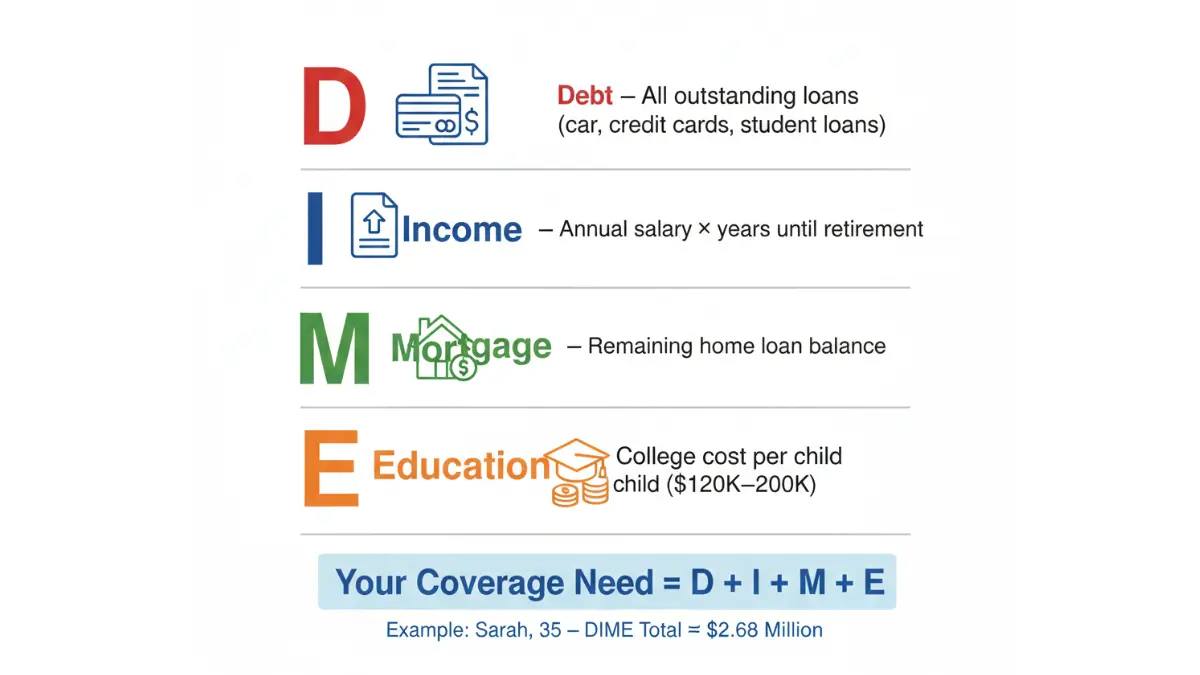

Formula 2: The DIME Formula (Most Recommended)

The DIME formula is the most comprehensive method used by licensed financial planners:

- D — Debt: All outstanding debts excluding your mortgage (car loans, credit cards, student loans)

- I — Income: Annual income × years until retirement

- M — Mortgage: Remaining balance on your home loan

- E — Education: Estimated college cost per child ($120,000–$200,000 each, 2026 estimates)

Real Case Example:

Sarah is 35, earns $80,000/year, has 25 years until retirement, a $320,000 mortgage balance, $40,000 in non-mortgage debt, and two kids. Her DIME calculation:

- D: $40,000

- I: $80,000 × 25 = $2,000,000

- M: $320,000

- E: $160,000 × 2 = $320,000

- Total: ~$2.68 million in life insurance coverage

Use our Mortgage Calculator to get your exact outstanding mortgage balance, and our Home Affordability Calculator to factor in your full housing obligations.

Formula 3: The Human Life Value Method

This method calculates the present value of your future earnings — essentially, how much your income stream is worth to your dependents if you were gone today.

- A 35-year-old earning $80,000 with 30 working years remaining has a human life value of approximately $1.8–$2.4 million (discounted at 3–4% annually).

What This Means For You: Most financial experts agree that the DIME formula gives the most accurate coverage target. At minimum, never buy less than 10x your annual income.

Life Insurance in 2026 — 4 Major Shifts You Need to Know

This is the section that zero competitors cover on their pillar pages — and it’s exactly what Google Discover audiences in the US, UK, Canada, and Australia are searching for right now.

1. AI Is Transforming Life Insurance Underwriting

In 2026, 87% of life insurance carriers are using artificial intelligence in at least one operational area, according to LIMRA and UCT research. The biggest shift: accelerated underwriting now allows some carriers to approve policies up to $5 million with zero medical exam required.

What this means for buyers: faster approvals (sometimes same-day), more accessible coverage for those with borderline health profiles, and increasingly competitive pricing.

2. Record Dividend Payouts Are Benefiting Whole Life Holders

2026 is a record year for life insurance dividends:

- Northwestern Mutual: $9.2 billion in policyholder dividends — the largest payout in the industry’s history

- MassMutual: $2.9 billion in dividends

- New York Life: $2.78 billion in dividends

If you hold a whole life insurance policy with a mutual insurer, 2026 is one of the strongest years on record for cash value growth. For those exploring similar long-term wealth strategies, our Retirement Planning Guide for Your 30s and the Roth IRA Complete Guide offer complementary strategies.

3. Millennials Are Now the Largest Life Insurance Buyers

The 2025 LIMRA Insurance Barometer Study — the most authoritative annual survey of U.S. insurance behavior — found that 50% of millennials intend to purchase life insurance within 12 months. The top triggers: a new baby (the #1 catalyst), buying a first home, and getting married.

Yet 40% of American adults remain underinsured or completely uninsured. The gap between intention and action is known as the “intention-behavior gap” — the most documented challenge in life insurance adoption.

4. Life Insurance as a Wealth Transfer Vehicle

With an estimated $124 trillion in generational wealth expected to transfer between 2025 and 2048, life insurance is no longer just a death benefit tool. Indexed universal life (IUL) and whole life policies are now cornerstone instruments in multi-generational estate planning strategies.

Key Takeaway: Life insurance in 2026 is not just protection — it is an active financial strategy. Whether you are 25 or 55, the right life insurance policy can serve as income replacement, debt coverage, education funding, retirement supplementation, and generational wealth transfer simultaneously.

For a broader view of how life insurance fits into your full financial picture, read our comprehensive Life Insurance Rates, Types & Savings Guide and our Health Insurance Expert Math Guide.

How to Buy Life Insurance — 5 Expert Steps

The process of getting life insurance coverage is faster in 2026 than at any point in history. Many carriers can issue a policy within 24 hours for qualifying applicants.

Step 1: Calculate Your Coverage Need

Use the DIME formula (Section 4) or multiply your annual income by 10 as a floor. Factor in your mortgage balance — use our Mortgage Refinance Calculator to understand your full home loan obligations before locking in a coverage amount.

Step 2: Choose Your Policy Type

- Term life if you have a mortgage, young children, or a tight budget

- Whole life if you need lifelong coverage or are building a cash-value estate plan

- Universal or IUL if you want flexibility and long-term wealth accumulation

Step 3: Compare Quotes from Multiple Insurers

Rates for identical coverage vary by up to 40% between insurers. Never accept a single quote. Use licensed comparison platforms and request at least 3 to 5 quotes. The FTC’s insurance consumer guidance outlines your consumer rights when evaluating and purchasing insurance products.

Step 4: Complete Your Application

You will need:

- Government-issued ID

- Social Security number

- Health history (prescriptions, diagnoses, surgeries)

- Beneficiary information

- Medical exam (or health questionnaire for no-exam policies)

Step 5: Activate Your Policy and Store Documents

- Name your beneficiaries clearly — and update them after any major life event (marriage, divorce, new child)

- Set your payment schedule — monthly or annual (annual payments often carry a 2–5% discount)

- Store your policy documents securely — and inform your beneficiaries where to find them

Common Mistakes That Cost Families Thousands

- Buying too little coverage — Employer group life insurance (typically 1–2x salary) is not a replacement for personal coverage

- Waiting too long — Every decade you delay, your premiums nearly double

- Not naming a beneficiary — Without one, the death benefit goes to your estate, triggering probate

- Ignoring rider options — Riders like accelerated death benefit, waiver of premium, and child term riders add significant value at low cost

For a broader financial protection plan, pair your life insurance with a strong Emergency Fund Strategy and a structured approach to paying off debt fast.

Frequently Asked Questions About Life Insurance

1. What is life insurance in simple terms?

Life insurance is a contract between you and an insurer. You pay regular premiums, and the insurer pays a death benefit (a lump sum) to your named beneficiaries when you die. It is a financial safety net for anyone who depends on your income.

2. How much does life insurance cost per month in 2026?

The average cost is $26/month for a 40-year-old purchasing a $500K, 20-year term life policy. A healthy 30-year-old typically pays $18–$25/month for the same coverage. Whole life insurance costs significantly more — often $200–$400/month for comparable coverage.

3. What is the difference between term and whole life insurance?

Term life insurance covers you for a fixed period (10–30 years) with no cash value. Whole life insurance covers you for life and builds guaranteed cash value. Term is cheaper; whole life is permanent and more expensive. For most people under 50, term is the smarter starting choice.

4. How much life insurance coverage do I need?

The widely recommended starting point is 10 times your annual income. For a more precise figure, use the DIME formula: add up your Debt, Income replacement need, Mortgage balance, and Education costs for children.

5. Is life insurance payout taxable?

In nearly all cases, death benefits are paid tax-free to beneficiaries. Interest earned on a delayed payout may be taxable. Estate taxes can apply if the total estate exceeds the federal exemption threshold ($15 million per person in 2026 following the new estate tax changes).

6. Can I get life insurance with a pre-existing condition?

Yes. Many insurers offer guaranteed-issue or no-medical-exam life insurance policies for those with health conditions. Premiums will be higher, but coverage is accessible. Accelerated underwriting in 2026 has expanded options significantly.

7. When should I buy life insurance?

As early as possible. Life insurance rates are lowest in your 20s and 30s. Every decade you delay, your monthly premium for the same coverage nearly doubles. The best time to buy is before you need it.

8. What happens if I miss a premium payment?

Most policies include a 30-day grace period. After that, your policy may lapse. Some permanent life insurance policies allow you to use accumulated cash value to cover missed payments automatically.

9. Can I have multiple life insurance policies?

Yes. Many financial advisors recommend “laddering” multiple term policies — buying several overlapping policies with different term lengths to match your changing financial obligations over time. This strategy can lower your overall premium cost.

10. Does life insurance cover suicide?

Most life insurance policies include a suicide exclusion for the first two years of the policy. After that, death by suicide is typically covered. Policy terms vary — always review your specific exclusions before purchasing.

11. What is accelerated underwriting in life insurance?

Accelerated underwriting uses AI and data analytics to evaluate your risk profile without a traditional medical exam. In 2026, some carriers approve coverage up to $5 million through this process — with decisions delivered in hours rather than weeks.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.