Travel Insurance: Don’t Buy Until You Read This

Travel insurance costs 4–10% of your trip — but 8 common events are silently excluded. Our 30 credentialed experts reveal exactly what’s covered before you buy.

In This Article

Quick Answer: Travel insurance protects your trip investment against cancellations, medical emergencies abroad, lost baggage, and flight delays. In 2026, comprehensive policies cost 4%–10% of your total trip cost. But 8 common events are silently excluded — and most travelers only discover this after a denied claim. Here’s exactly what you need to know before spending a single dollar.

What Is Travel Insurance — And Why 2026 Changed Everything

Travel insurance is a financial safety net that reimburses you for specific, pre-defined losses that occur before or during a trip. It is not a blanket “anything goes wrong” guarantee — and that distinction costs travelers thousands every year.

In 2026, the stakes are higher than ever. A recent U.S. News survey found that 65% of American consumers now consider travel insurance important, with roughly 50% of Americans now purchasing a policy before travel — a figure that has risen steadily since the COVID-19 pandemic. That shift reflects hard experience: delayed flights, hurricanes, pilot strikes, and medical crises abroad have taught a generation of travelers that the unexpected is not rare — it is the norm.

The travel insurance market now exceeds $8.2 billion in North America alone, growing at a CAGR of 15.61%. Yet the majority of policyholders still misunderstand what they’ve actually purchased.

The 3 Questions to Ask Before You Buy Anything

Before comparing a single policy, answer these three questions honestly:

- What nonrefundable costs am I risking? Add up flights, hotels, tours, and cruise deposits that are not refundable.

- Does my health insurance cover me abroad? Most U.S. plans — including Medicare and Medicaid — provide little to no international emergency coverage.

- What does my credit card already cover? Cards like Chase Sapphire Preferred and Capital One Venture X include some travel protections — but rarely enough for medical emergencies or high-value trips.

If your answers reveal meaningful financial exposure, travel insurance is worth serious evaluation. If you’re taking a short domestic trip with fully refundable bookings, you may not need it at all.

What This Means For You: Don’t buy travel insurance reflexively. Buy it strategically — after calculating your true at-risk dollars. Use our Debt Consolidation Calculator to model how unexpected trip losses could impact your broader financial picture.

What Travel Insurance Actually Covers in 2026 — The Complete Breakdown

Most travelers read the marketing brochure, not the Certificate of Insurance. Here’s a plain-English breakdown of every major coverage type available in 2026.

Core Coverage Types — At a Glance

| Coverage Type | What It Pays For | Typical Limit |

|---|---|---|

| Trip Cancellation | Prepaid nonrefundable costs if you cancel for a covered reason | Up to 100% of trip cost |

| Trip Interruption | Unused trip portion + cost to return home early | 100%–150% of trip cost |

| Emergency Medical | Doctor visits, hospital stays, treatment abroad | $50,000–$500,000 |

| Medical Evacuation | Emergency transport to nearest adequate facility | $250,000–$1,000,000+ |

| Baggage Loss/Delay | Lost, stolen, or delayed luggage and personal items | $500–$3,000 |

| Trip Delay | Hotel, meals, transportation during covered delays | $500–$2,000 |

| Cancel For Any Reason (CFAR) | Cancel for virtually any reason, not covered in base plan | 50%–75% reimbursement |

| Accidental Death & Dismemberment | Lump sum paid to beneficiary if you die or lose a limb | $10,000–$500,000 |

| Rental Car Damage | Collision/theft damage to a rental vehicle | Varies by plan |

Travel Medical Insurance — The #1 Reason Most Americans Actually Need It

Here is a fact that surprises most travelers: the CDC explicitly states that travelers should verify whether their current health care covers emergencies while traveling and consider a short-term supplemental policy if it does not.

The reason matters. According to the U.S. Department of State, U.S. Medicare and Medicaid do not pay for medical care outside the United States. Even strong employer-sponsored plans offer limited or zero international coverage. A single hospitalization in Japan, Germany, or Australia can run $20,000–$100,000+ out of pocket.

Travel medical insurance fills this gap directly. Minimum recommended coverage for international trips is $50,000 in emergency medical and $250,000 in medical evacuation. For high-risk or remote destinations, leading policies now offer up to $1,000,000 in evacuation coverage.

This is also worth comparing alongside your overall health insurance strategy for 2026 — especially if you travel frequently.

Cancel For Any Reason (CFAR) — Is the Upgrade Worth It?

CFAR is the most powerful — and most misunderstood — coverage available. According to the National Association of Insurance Commissioners (NAIC), CFAR allows you to cancel for any reason not covered in your base policy and receive a partial refund of 50%–75% of total prepaid costs.

Standard trip cancellation policies only reimburse you for a specific list of “covered reasons” — illness, death, extreme weather, and similar events. CFAR removes that list entirely.

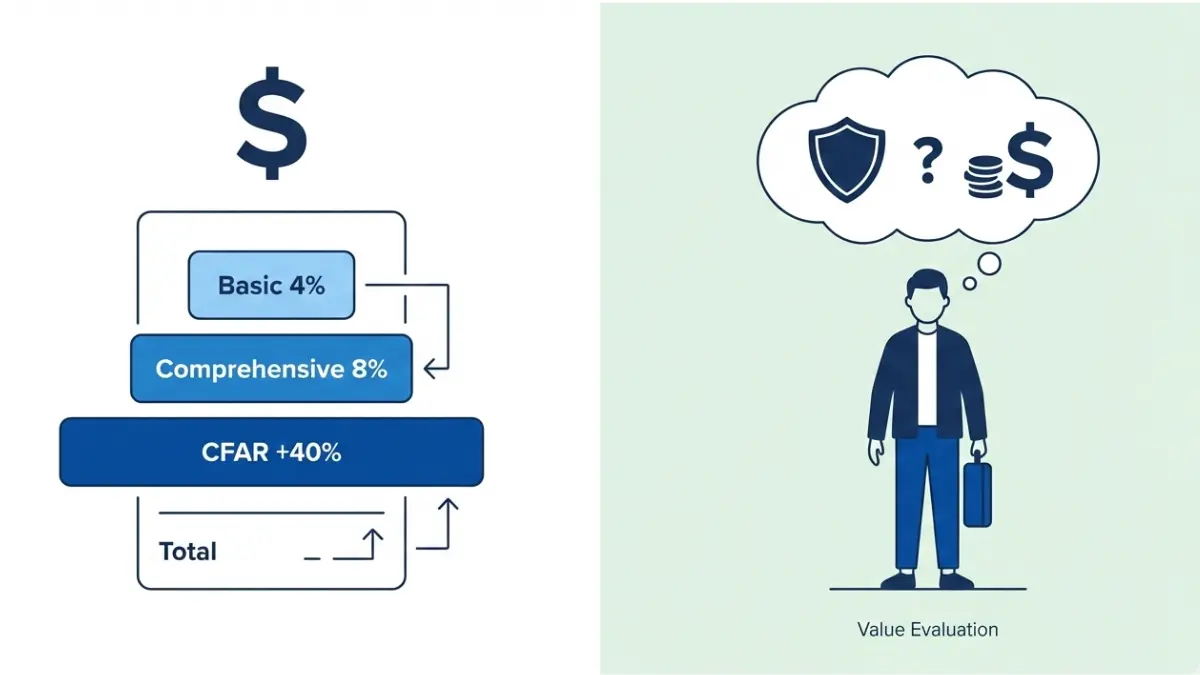

The cost? CFAR adds approximately 40% to your base premium. On a $400 comprehensive plan, that’s an extra $160. For a $10,000 international trip with full nonrefundable bookings, most financial experts agree it’s money well spent.

Who should add CFAR:

- First-time international travelers

- Anyone booking 9+ months in advance

- Travelers with unpredictable work schedules

- High-value trips over $5,000 in nonrefundable costs

8 Things Travel Insurance Won’t Cover — The Silent Exclusions

This is the section your insurer’s brochure hopes you never read. Every claim denial starts here. According to the NAIC, the most common reason travelers are denied claims is lack of awareness of standard policy exclusions.

Here are the 8 exclusions that catch Americans most off-guard:

1. Pre-Existing Medical Conditions

If you had a diagnosed condition before purchasing your policy — heart disease, diabetes, asthma — standard plans exclude related claims unless you bought within the insurer’s Pre-Existing Condition Waiver window (typically 14–21 days after your first trip deposit).

2. Change of Mind Cancellations

Decided the destination isn’t right for you anymore? Changed your plans after a bad week? Standard trip cancellation covers only listed covered reasons — not personal preference. Only CFAR covers this.

3. Named Storms and Foreseeable Events

If a hurricane, tropical storm, or major weather event has already been named or publicly announced before you buy your policy, you cannot claim it as an unexpected event. Buy before storms are named — or you’re unprotected.

4. Pandemic Fear and Epidemic-Related Cancellations

COVID-19 taught this lesson to millions. Most policies exclude cancellations due to fear of travel, government advisories, or pandemic/epidemic events — unless your policy specifically includes epidemic coverage as a named benefit. Always read the covered reasons list.

5. Extreme Sports and Adventure Activities

Standard policies typically exclude injuries sustained during activities like skydiving, base jumping, scuba diving, mountaineering, and motorsports. If your trip includes adventure activities, you must add a sports rider or purchase a specialty adventure policy.

6. Pregnancy-Related Complications

Many standard plans exclude complications that arise from pregnancy unless you purchased a medical rider that specifically covers obstetric emergencies. Travelers who are pregnant should verify this explicitly before departure.

7. Vendor or Supplier Bankruptcy

If your airline, cruise line, or tour operator goes bankrupt after you’ve paid, standard plans may not cover this loss. You need a policy that specifically includes “supplier default” coverage — a separate listed benefit, not a standard inclusion.

8. Travel to High-Risk or Restricted Destinations

If the U.S. State Department has issued a Level 4 “Do Not Travel” advisory for your destination, your insurer may void coverage entirely. The State Department travel advisory system is the definitive source — always cross-check your destination before buying.

Expert Callout: Always read the Certificate of Insurance — the full legal policy document — not the summary brochure. The brochure highlights benefits. The Certificate defines exclusions.

This is why our experts also recommend reviewing your life insurance coverage and car insurance optimization strategies as part of a comprehensive personal risk review before any major trip.

How Much Does Travel Insurance Cost in 2026 — Real Pricing Data

Direct Answer: Travel insurance costs 4%–10% of your total prepaid, nonrefundable trip costs for a comprehensive policy. CFAR adds roughly 40% on top of that.

According to data from Squaremouth, travelers spent an average of $414 for comprehensive coverage and $92 for medical-only policies from June 2024 to June 2025.

2026 Travel Insurance Cost by Trip Budget

| Trip Cost | Basic Plan (~4%) | Comprehensive (~8%) | With CFAR (+40%) |

|---|---|---|---|

| $1,000 | ~$40 | ~$80 | ~$112 |

| $2,500 | ~$100 | ~$200 | ~$280 |

| $5,000 | ~$200 | ~$400 | ~$560 |

| $7,500 | ~$300 | ~$600 | ~$840 |

| $10,000 | ~$400 | ~$800 | ~$1,120 |

| $15,000 | ~$600 | ~$1,200 | ~$1,680 |

4 Factors That Raise Your Travel Insurance Premium

- Your age: Travelers aged 60+ pay significantly more due to higher medical risk. A 65-year-old may pay 3x the premium of a 30-year-old for identical coverage.

- International vs. domestic travel: International trips trigger higher medical coverage requirements, raising premiums substantially.

- Trip length: The longer the trip, the greater the statistical risk exposure — and the higher the cost.

- Pre-existing condition coverage: Adding a waiver for pre-existing conditions increases your premium by 15%–30% on average.

When to Skip Travel Insurance Entirely

Travel insurance is not always necessary. Consider skipping it if:

- Your entire trip is booked with fully refundable rates (flights, hotels, activities)

- You are taking a domestic drive trip under $500 in total costs

- Your premium travel credit card already covers trip cancellation and adequate emergency medical

- Your destination is low-risk and your personal health insurance includes international coverage

For frequent travelers taking 3+ trips per year, an annual multi-trip policy almost always costs less than buying individual plans per trip. The break-even point is typically 3 international trips annually.

Understanding your insurance costs in context of your overall financial health matters. Many of our readers use our Emergency Fund Calculator to understand how an unexpected $10,000 medical bill abroad would impact their financial stability — a useful exercise before skipping coverage.

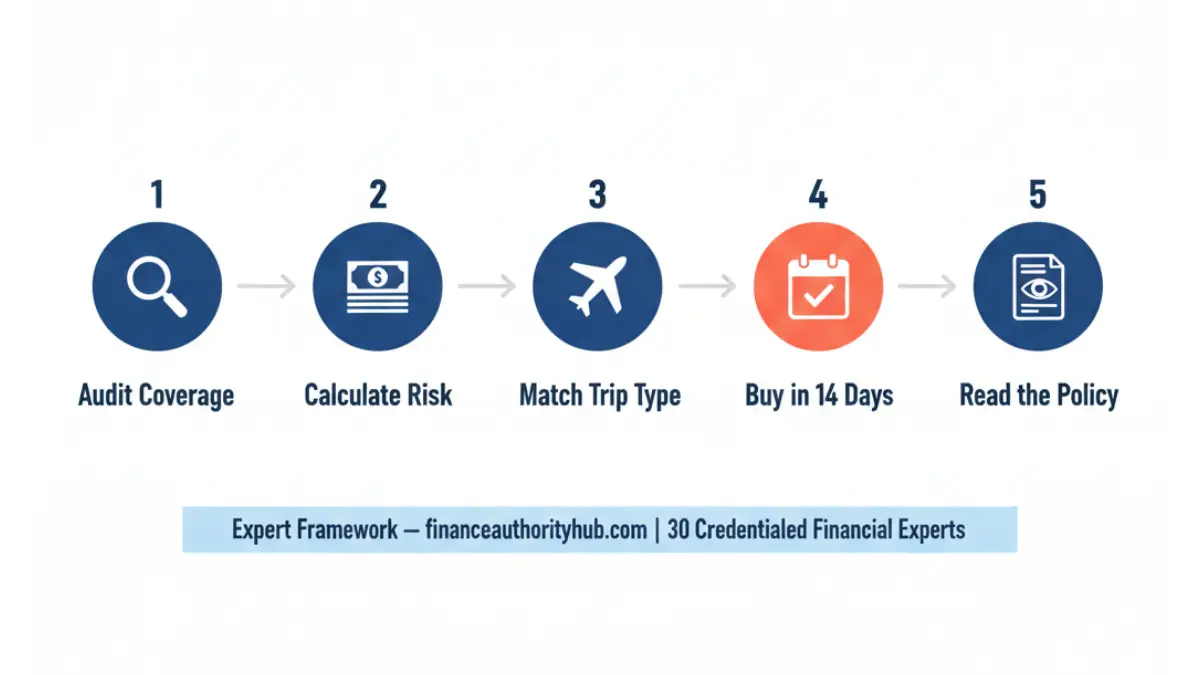

How to Choose the Right Travel Insurance — Expert 5-Step Framework

Our panel of 30 credentialed financial experts distilled the travel insurance decision into a replicable, 5-step framework. This replaces the generic “compare quotes” advice that dominates competitor articles.

Step 1 — Audit Your Existing Coverage First

Before spending a dollar, check what you already have:

- Credit card benefits portal: Cards like Chase Sapphire Preferred, Capital One Venture X, and Amex Platinum include trip cancellation, trip delay, and some medical coverage. Log in and read the benefits guide — not the marketing page.

- Health insurance international coverage: Call your insurer and ask directly: “Does my plan cover emergency hospitalization in [destination]?” Get the answer in writing.

- Homeowner’s or renter’s insurance: Some policies cover stolen personal items while traveling.

Rule of thumb: If you have $0 in nonrefundable costs and confirmed health coverage abroad, a standalone policy may be unnecessary.

Step 2 — Calculate Your True At-Risk Dollars

Your insurable amount = the total of all nonrefundable, prepaid trip costs:

- Nonrefundable flights

- Hotel deposits

- Tour and excursion pre-payments

- Cruise deposits

- Event tickets

Only insure what you cannot afford to lose. Use our financial planning tools to model your exposure before comparing policies.

Step 3 — Match Coverage to Your Trip Profile

| Trip Type | Recommended Coverage |

|---|---|

| International trip, high cost | Comprehensive + medical + CFAR |

| Domestic trip, nonrefundable bookings | Trip cancellation only |

| Frequent traveler (3+ trips/year) | Annual multi-trip plan |

| Senior traveler (65+) | Comprehensive with pre-existing waiver |

| Adventure or extreme sports trip | Standard plan + adventure sports rider |

| Cruise vacation | Cruise-specific policy |

| Short domestic drive under $500 | Consider skipping entirely |

Step 4 — Buy Within 14–21 Days of Your First Deposit

This is the single most important timing rule in travel insurance — and the one most travelers miss.

Purchasing within this window unlocks two critical benefits that disappear if you wait:

- Pre-existing condition waiver: Removes the standard exclusion for pre-existing medical conditions

- Cancel For Any Reason eligibility: Most CFAR upgrades require purchase within this window

The NAIC’s official guidance confirms that timing of purchase is one of the most consequential decisions in travel insurance. Buy early — even if your full trip isn’t booked yet.

Step 5 — Read the Certificate of Insurance Before You Buy

Every travel insurer provides two documents: a summary brochure and a Certificate of Insurance. The brochure is marketing. The Certificate is the legal contract.

Before clicking “purchase,” read:

- The “Covered Reasons” list (for trip cancellation) — if your cancellation reason isn’t on this list, you won’t be paid

- The Exclusions section — this is where your claim will be denied

- The Claims process and filing window — most policies require claim filing within 20–90 days of the incident

Countries That Require Travel Insurance in 2026

Some destinations mandate coverage before entry:

- Qatar: Requires travel insurance covering emergency medical treatment and transportation

- Cuba: Requires non-U.S. medical insurance (often included in airline ticket cost)

- Ukraine: Requires foreigners to have medical insurance; the State Department also recommends evacuation coverage

Always verify entry requirements at the U.S. State Department’s destination-specific pages before departure.

This type of financial preparedness aligns with broader risk management — including term life insurance planning for 2026 and understanding your full personal loan rates and traps before taking on travel debt.

FAQs — 11 Expert Answers to the Most Searched Travel Insurance Questions

Q1: Is travel insurance worth it in 2026?

Yes — if you have nonrefundable trip costs over $500 or are traveling internationally. Skip it if your bookings are fully refundable, your credit card covers trip cancellation, or your health insurance provides international emergency coverage.

Q2: What does travel insurance NOT cover?

Pre-existing conditions (without a timely waiver), change-of-mind cancellations, named storms after your purchase date, fear of travel or pandemic worry, extreme sports without a rider, and trips to destinations under a State Department Level 4 advisory.

Q3: When should I buy travel insurance?

Within 14–21 days of your first trip deposit. This unlocks pre-existing condition waivers and CFAR eligibility — both disappear if you purchase later.

Q4: How much does travel insurance cost?

Between 4%–8% of your total nonrefundable trip costs for a standard comprehensive plan. CFAR adds roughly 40% to the premium. A $5,000 trip will run approximately $200–$400 for comprehensive coverage.

Q5: Does travel insurance cover COVID-19?

Most policies cover COVID if you test positive and cannot travel. General fear of COVID, destination lockdowns, or government travel advisories are typically excluded. Always look for “epidemic coverage” as a named benefit if this matters to you.

Q6: Is my credit card’s travel insurance enough?

For domestic trips with limited nonrefundable costs, often yes. For international travel, credit cards rarely provide sufficient emergency medical or evacuation coverage — typically capped at $2,500–$10,000 for medical, far below the $50,000+ recommended minimum.

Q7: What is Cancel For Any Reason (CFAR) travel insurance?

CFAR allows you to cancel your trip for virtually any reason and receive 50%–75% of your prepaid, nonrefundable costs back. It must typically be purchased within 14–21 days of your first trip deposit and adds roughly 40% to your base premium.

Q8: Does travel insurance cover pre-existing medical conditions?

Only if you purchase within the insurer’s waiver window — usually 14–21 days after your initial deposit. After that window closes, pre-existing conditions are permanently excluded from your policy.

Q9: Which countries require travel insurance for entry in 2026?

Qatar, Cuba, and Ukraine all require some form of medical or travel insurance for entry. Requirements evolve — always verify through the CDC Travelers’ Health page and State Department advisories before booking.

Q10: What is an annual travel insurance plan?

A policy covering all trips within a 12-month period, regardless of how many trips you take. Each insurer sets a maximum per-trip duration (typically 30–90 days per trip). Ideal if you travel internationally 3 or more times per year — usually less expensive than buying individual policies per trip.

Q11: How do I file a travel insurance claim?

Step 1: Contact your insurer immediately after the incident — before arranging alternative travel if possible

Step 2: Document everything: original receipts, medical reports, airline delay notices, police reports for theft

Step 3: File your claim within the policy’s window — typically 20–90 days after the incident

Step 4: Submit via the insurer’s online claims portal with all supporting documentation

Step 5: Follow up weekly — most reputable insurers process claims within 7–30 business days

Expert Verdict — Should YOU Buy Travel Insurance in 2026?

Buy it if: You have meaningful nonrefundable trip costs, you’re traveling internationally, or your health insurance doesn’t cover you abroad.

Skip it if: All bookings are refundable, you’re taking a short domestic trip, or your premium credit card already covers your key risks.

Always: Buy within 14–21 days of your first deposit. Read the Certificate, not the brochure. And never assume your claim will be paid — verify it before you travel.

Travel insurance is one layer of a complete financial protection strategy. Review your full insurance portfolio alongside your retirement savings plan and emergency fund — because financial resilience starts long before you board the plane.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.