Holiday Insurance 2026: Don’t Travel Without This

In 2024, insurers paid £472M across 500,000+ claims. Yet 1 in 4 travelers go uninsured. Here’s everything you need to know about holiday insurance in 2026.

In This Article

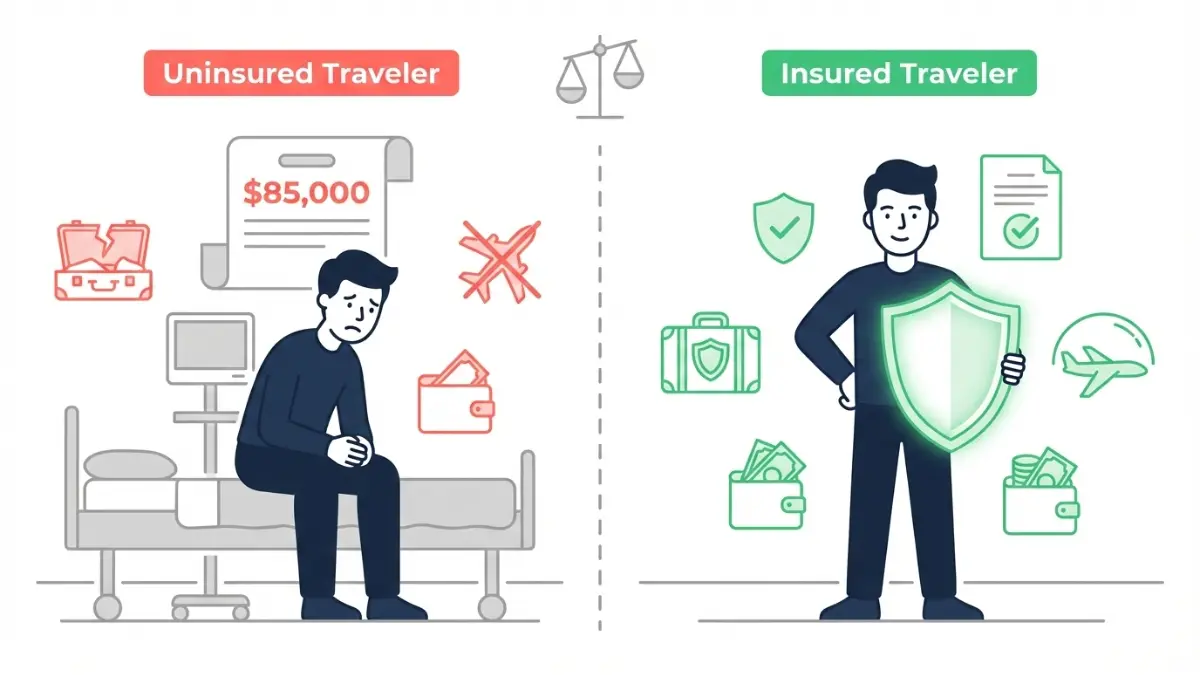

Holiday insurance is a financial protection policy that covers emergency medical costs, trip cancellations, lost baggage, and travel disruptions when you travel abroad. In 2024, UK and global insurers paid out £472 million across more than 500,000 claims (ABI, August 2025). Without it, one hospital stay in the USA alone can cost over £100,000 — and one policyholder’s single claim hit £1 million.

Every year, millions of travelers skip holiday insurance to save a few dollars. Most never face consequences. But for those who do, the financial damage is life-altering. This guide covers everything you need to know — costs, coverage, claim secrets, and 2026 rule changes your insurer won’t proactively tell you.

What Is Holiday Insurance — And Why Does It Matter in 2026?

Holiday insurance (also called travel insurance) is a policy designed to protect you financially before and during a trip. It is fundamentally different from health insurance — it kicks in when you’re outside your home country, in situations your domestic coverage won’t touch.

Here’s the stat that stops people cold:

1 in 4 UK holidaymakers traveled abroad without insurance in the past 12 months — and among the 25–34 age group, 41% admitted to at least one uninsured trip (YouGov / ABTA, April 2025).

That’s not recklessness. It’s a lack of information about what’s actually at risk.

Why 2026 Has Raised the Stakes

Travel disruptions are accelerating. In January 2026, a U.S. military operation in Venezuela caused the FAA to restrict airspace, stranding hundreds of flights. In 2025, air traffic control failures, wildfires in southern Europe, and Heathrow closures each triggered mass disruption events. The travelers with comprehensive holiday insurance recovered their costs. The rest paid out of pocket.

Medical costs abroad have also surged. The average emergency medical travel claim in 2024 was £1,528 — but individual claims frequently run into the tens of thousands. USA healthcare is especially brutal: a single emergency surgery can exceed $250,000.

Holiday insurance is not an optional luxury in 2026. It is your financial safety net.

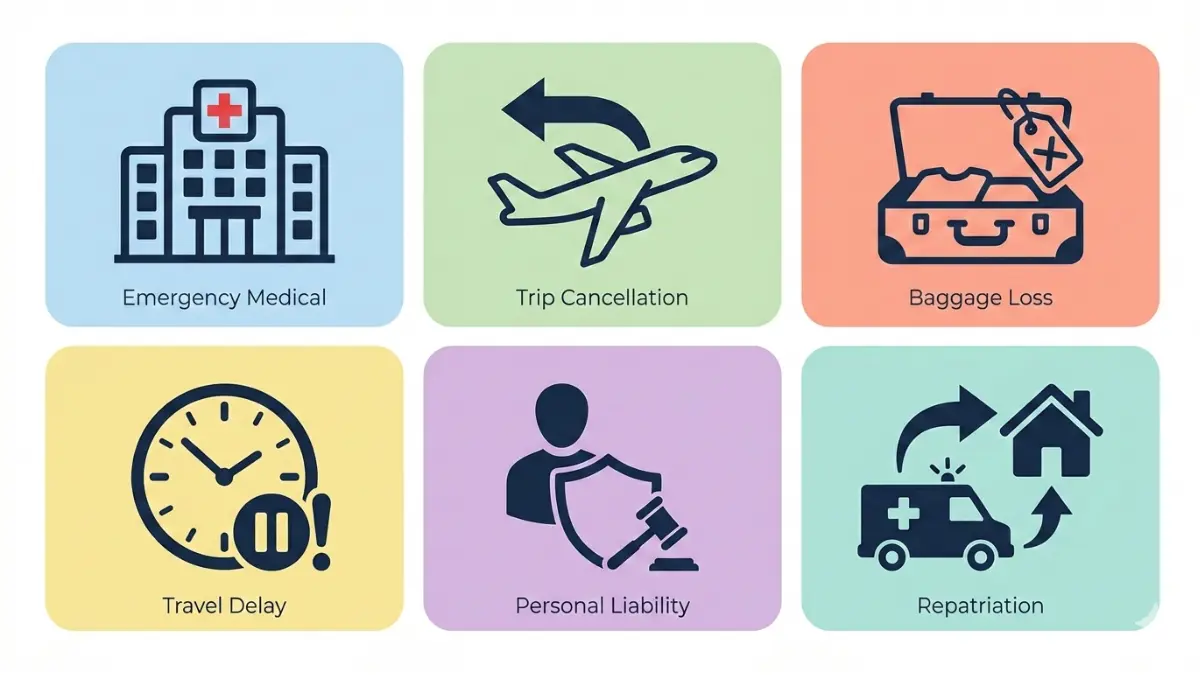

What Does Holiday Insurance Actually Cover?

Most travelers assume they know what’s covered. Most are wrong.

Here’s the complete picture.

Standard Coverage — What Every Policy Should Include

| Cover Type | What It Pays | Typical Limit |

|---|---|---|

| Emergency Medical | Hospital stays, treatment, ambulance | Up to £10 million |

| Repatriation | Flying you home when medically necessary | Included with medical cover |

| Trip Cancellation | Pre-paid costs if you can’t travel | Up to £5,000–£12,500 per person |

| Baggage Loss/Theft | Replacement of luggage and valuables | Up to £2,500 |

| Travel Delay | Hotel and meals during delays | £200–£500 |

| Personal Liability | Legal costs if you injure someone | Up to £2 million |

| Missed Departure | Rebooking costs if you miss your flight | £500–£1,500 |

Medical expenses remain the most claimed category — making up 34% of all claims in 2024, up from 29% in 2023, with total medical payouts reaching £262 million (ABI, 2025).

What Competitors Never Tell You — The Hidden Exclusions

This is the section that comparison sites bury in fine print. Read it carefully.

Your holiday insurance claim will be VOIDED if:

- You have an undeclared pre-existing medical condition — this is the #1 reason claims fail

- You travel to a destination the FCDO advises against — policy is invalid from day one

- An incident involves alcohol or drugs — even a minor intoxication contribution can trigger denial

- You participate in adventure sports without an add-on — bungee jumping, quad biking, scuba diving, white-water rafting

- You change your mind about the trip — cancellation cover requires a specific insured reason

- You fail to report theft to police within 24 hours — no police report, no payout

- You were already aware of a reason to cancel when you bought the policy

This matters enormously. If you’re comparing policies purely on price — as MoneySupermarket and CompareTheMarket encourage — you may be buying coverage that denies your claim the moment you actually need it.

What’s NOT Covered as Standard (But Should Be On Your Radar)

- Mental health cancellation cover — rapidly growing demand in 2026, often excluded or requires specialist policy

- Gadget and smartphone cover — typically an expensive add-on

- Pandemic/epidemic-related cancellations — COVID-era policies have largely reverted to pre-2020 exclusion language

- Cruise-specific events — missed ports, onboard medical emergencies require dedicated cruise holiday insurance

For broader insurance planning, explore our complete insurance guide and our specialist travel insurance deep-dive.

Holiday Insurance Cost Breakdown 2026

One of the biggest myths: “Holiday insurance is expensive.” It isn’t. What’s expensive is not having it.

Real Cost Data — February 2026

| Traveler Profile | Europe Single Trip | USA Single Trip | Annual EU Multi-Trip | Annual Worldwide |

|---|---|---|---|---|

| Age 20, no conditions | From £1–£5 | From £15–£25 | ~£20–£30 | ~£50–£70 |

| Age 45, no conditions | £10–£25 | £40–£70 | ~£38 (median) | ~£86 (median) |

| Age 65+, pre-existing | £40–£120 | £100–£300+ | £80–£200 | £150–£400+ |

Source: CompareTheMarket and MoneySupermarket data, January–February 2026

To put this in perspective: the cheapest single-trip European policy starts from under £2. The average emergency medical claim is £1,528. The return on protection is staggering.

Single Trip vs Annual Multi-Trip — Which One Wins?

Choose Single Trip if:

- You travel once a year or less

- Your trips are short (under 2 weeks)

- You want minimal commitment

Choose Annual Multi-Trip if:

- You travel 2 or more times per year

- You take both business and leisure trips

- You want cancellation cover active from each booking date

Real Example: Two European trips per year at £15 each = £30. An annual EU policy = £38 median. Nearly the same cost — but annual covers unlimited trips and provides cancellation protection from the moment each trip is booked.

5 Ways to Cut Your Holiday Insurance Premium

- Buy the day you book — lower statistical risk to the insurer means lower price

- Choose a higher voluntary excess — accepting more personal risk reduces your premium

- Skip add-ons you don’t need — no gadgets? Don’t pay for gadget cover

- Go annual if you travel twice or more — almost always cheaper long-term

- Compare at least 4 providers — prices for identical coverage can vary by 300%

Managing travel costs alongside bigger financial commitments? Use our Home Affordability Calculator to see the full picture.

Types of Holiday Insurance — Which One Do You Need?

Not all holiday insurance policies are the same. Using the wrong type can leave you dangerously underprotected.

The 6 Core Policy Types

| Type | Best For | Key Feature |

|---|---|---|

| Single Trip | 1 holiday per year | Cheapest for occasional travelers |

| Annual Multi-Trip | 2+ trips per year | Covers unlimited trips (max 30–31 days each) |

| Family Policy | 2 adults + children | Cheaper than individual policies combined |

| Senior/Over 70s | Older travelers | Specialist providers, pre-existing condition focus |

| Cruise Insurance | Cruise holidays | Missed ports, onboard medical, ship evacuation |

| Pre-Existing Condition | Travelers with health history | Must declare all conditions — no exceptions |

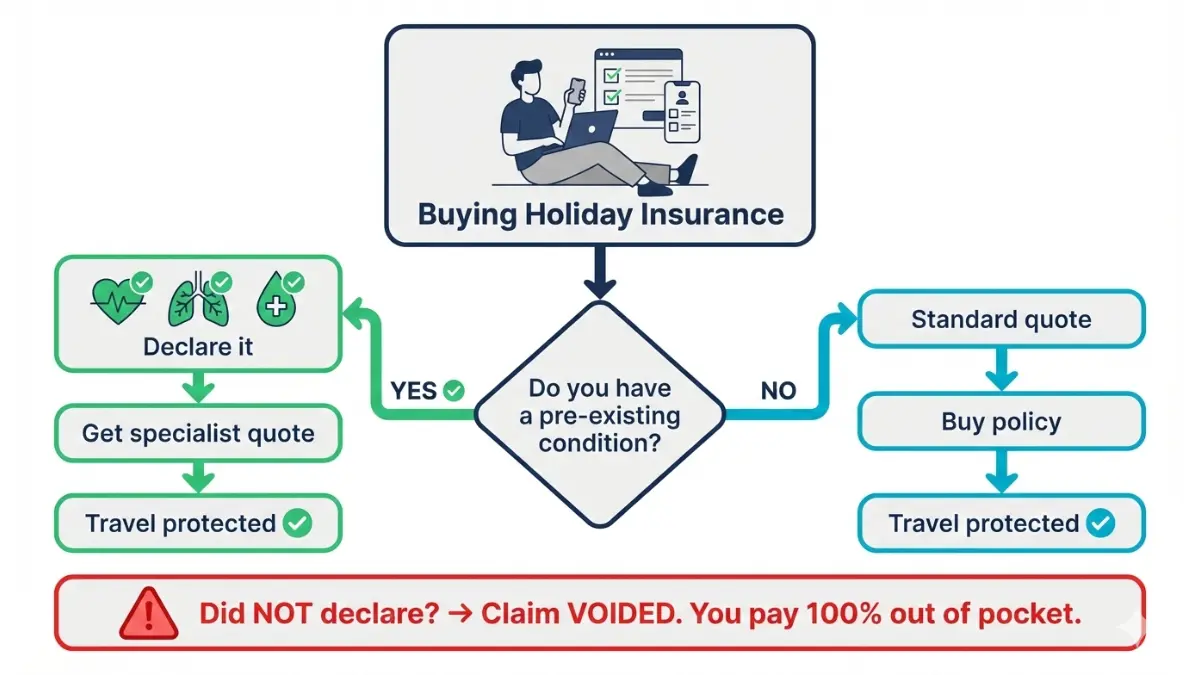

Pre-Existing Conditions: The Complete Guide

This is the topic every major comparison site handles poorly. Here’s the expert-level reality:

You must declare:

- Heart conditions, including previous heart attacks or surgery

- Diabetes (any type)

- Cancer — including conditions in remission

- High blood pressure

- Respiratory conditions including asthma and COPD

- Any mental health diagnosis including depression and anxiety

What happens if you don’t declare: Your claim is voided. Not reduced — voided entirely. If you’re hospitalized abroad with an undeclared condition and your US emergency medical bill reaches $80,000, you pay every cent yourself.

The ABI’s guidance is unambiguous: always answer all questions fully and disclose pre-existing conditions. Cover is available for many conditions — but only if declared upfront (ABI travel insurance FAQ).

Specialist providers who cover complex conditions include AllClear, InsureandGo, and Just Travel Cover. These are especially important for travelers over 70, where the ABI data shows average claim values are more than 3x higher than for travelers under 65.

For context on broader insurance planning, our expert panel has also reviewed health insurance options for 2026 and life insurance costs and types.

Critical 2026 Rule Changes You Must Know

1. EU Entry/Exit System (EES) — Active Since October 2025 UK nationals entering the Schengen Area now face biometric registration on their first visit. Queues at major European airports have lengthened significantly. This directly affects travel delay claims — check your policy’s delay threshold (many require a 3–6 hour minimum).

2. ETIAS — Launching Late 2026 A new EU travel authorization system requires UK passport holders to pre-register and pay a €20 fee before entering Schengen countries. Administrative issues with ETIAS applications are not covered by standard holiday insurance. Plan ahead.

3. FCDO Travel Advice Always check GOV.UK’s Foreign Travel Advice before booking AND before departing. If the FCDO upgrades a destination to “advise against all travel” before you depart, your policy is invalid. If the advice changes while you’re already there, your existing cover continues.

How to Make a Holiday Insurance Claim — And Actually Get Paid

Most people only read their policy after something goes wrong. That’s the single most expensive mistake in travel finance.

Step-by-Step Claim Process

Before you leave home:

- Save your insurer’s 24/7 emergency number in your phone

- Share your policy details with one trusted person at home

- Read the claim submission deadline (typically 28–90 days after return)

If something goes wrong:

- Call your insurer’s emergency line first — for non-emergencies, call before seeking treatment, not after

- Document everything immediately — photos, witness details, timestamps

- Get written proof — hospital discharge letters, police crime reference numbers for theft, airline delay certificates

- Keep every receipt — no receipt = no reimbursement in almost every policy

- File before the deadline — late submissions are routinely rejected regardless of validity

The 6 Reasons Holiday Insurance Claims Get Rejected

This is what comparison sites never show you — and it’s costing travelers millions annually:

- Undeclared pre-existing condition — the #1 cause of denied claims worldwide

- Travelling against FCDO advice — full policy void, no exceptions

- Alcohol or drug involvement — even borderline cases get disputed

- Uncovered activity — adventure sports without the correct add-on

- No police report for theft — must be filed within 24 hours in most jurisdictions

- Missed submission deadline — policies have strict post-trip filing windows

For complaints about claim handling, the UK Financial Ombudsman Service adjudicates disputes between policyholders and insurers — a critical but widely unknown resource.

What This Means For You

Read your full policy document before you travel. The 15 minutes you spend doing this can save you £50,000 in denied claims. The ABI recommends sharing your insurer’s emergency contact with a travel companion and a trusted person at home — in case you’re incapacitated and can’t call yourself.

Need to plan your finances around a trip? Our Debt Consolidation Calculator helps you see exactly what you can afford before you book.

Expert Verdict, FAQs & Disclaimer

Expert Panel Verdict — Is Holiday Insurance Worth It in 2026?

Our panel of 30 credentialed international financial experts is unanimous:

Holiday insurance is non-negotiable for any international trip in 2026. The UK travel insurance market alone paid out £472 million in 2024. One in four travelers still travels uninsured (ABTA, 2025). That gap represents billions in personal financial exposure.

The math is simple:

- Cost of a single-trip European policy: £2–£25

- Average emergency medical claim: £1,528

- Largest single claim on record (USA, 2024): £1,000,000+

The single most important rule: Buy your holiday insurance the same day you book your trip. Cancellation cover is only active from the moment your policy starts — not from your departure date.

For related coverage, see our expert guides on cheap insurance strategies for 2026 and motorcycle insurance.

Frequently Asked Questions about Holiday Insurance

Q1: What is holiday insurance?

Holiday insurance is a financial protection policy covering emergency medical costs, trip cancellations, lost baggage, and travel delays when abroad. It is distinct from domestic health insurance and activates specifically during travel.

Q2: Is holiday insurance legally required?

No. It is not a legal requirement in any Tier 1 country. However, ABTA and the ABI strongly recommend it for all international travel due to the scale of potential financial exposure.

Q3: When should I buy holiday insurance?

The day you book your trip. Cancellation cover only applies from your policy start date — not your departure date. Buying on day one protects you from the moment you’re financially committed.

Q4: Does holiday insurance cover pre-existing medical conditions?

Yes — but only if you declare them at purchase. Undeclared conditions void your claim entirely. Specialist insurers cover most conditions including cancer, diabetes, and heart disease.

Q5: How much does holiday insurance cost in 2026?

Single-trip European cover starts from under £5 for younger travelers. Annual multi-trip EU cover averages £38. USA and worldwide coverage is significantly more expensive due to medical costs.

Q6: What is the difference between single trip and annual multi-trip holiday insurance?

Single trip covers one holiday. Annual multi-trip covers unlimited trips within 12 months (per trip maximum typically 30–31 days). Annual cover is more cost-effective for anyone traveling twice or more per year.

Q7: What voids a holiday insurance claim?

The most common reasons: undeclared pre-existing conditions, traveling against FCDO advice, alcohol-related incidents, uncovered activities, no police report for theft, and missed submission deadlines.

Q8: Does holiday insurance cover cruise vacations?

Standard policies often do not include cruise-specific cover. You need dedicated cruise holiday insurance covering missed port stops, onboard medical emergencies, and ship evacuation.

Q9: Can travelers over 70 get holiday insurance?

Yes. Specialist providers offer no upper age limit policies. Premiums increase substantially with age — ABI data confirms average claims for travelers aged 71–75 are £1,830 vs £518 for ages 36–40.

Q10: What 2026 changes affect holiday insurance?

The EU’s Entry/Exit System (EES) is now active, causing longer airport queues that may affect delay claims. ETIAS launches in late 2026 requiring UK travelers to pre-register for Schengen entry. Check GOV.UK travel advice before every trip.

Q11: Does a credit card provide sufficient holiday insurance?

Generally no. Most credit card travel benefits are limited in scope, have low medical coverage ceilings, and do not cover pre-existing conditions. Always verify exactly what your card covers before relying on it in place of a dedicated policy.

⚠️ Disclaimer

This article is for educational and informational purposes only and does not constitute financial or insurance advice. Holiday insurance products, pricing, and coverage terms vary significantly by provider, destination, traveler age, and individual circumstances. Always read your full policy documents before purchasing. For personalized advice, consult a regulated financial adviser authorized by the FCA (UK) or a licensed insurance professional in your country. External links are provided for reference only. financeauthorityhub.com is not responsible for third-party content or pricing accuracy. Data cited reflects publicly available sources as of February 2026.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.