Motorcycle Insurance: Save $500+ on Your 2026 Policy

Most riders overpay $300–$500/year on motorcycle insurance. Compare 2026 rates from $22/month, top expert-ranked companies, and 9 proven savings strategies.

In This Article

Most U.S. riders are overpaying for motorcycle insurance by $300–$500 every year — not because affordable coverage doesn’t exist, but because they never compare quotes or stack available discounts. Motorcycle insurance costs as little as $22/month in 2026. If you’re paying more, this guide shows you exactly how to fix it.

What Is Motorcycle Insurance — and Are You Overpaying?

Motorcycle insurance is a specialized policy that protects you financially if your bike is stolen, damaged, or involved in an accident. It covers liability to others, physical damage to your motorcycle, and your own medical costs depending on the coverage you choose.

The national average cost of motorcycle insurance in 2026 is $22–$33/month — far less than most riders assume. Yet according to the Insurance Information Institute, the majority of riders never review their policy at renewal, which is the single biggest reason premiums stay unnecessarily high.

What you’ll learn in this guide:

- Every coverage type — and which ones you actually need

- 2026 rate data by state, bike type, and rider profile

- The top-ranked companies, scored by 30 finance experts

- A 9-step discount stacking system that can save $500+ annually

- Which company fits your exact riding situation

If you’re also reviewing your broader insurance costs, our guide on how to stop overpaying on insurance in 2026 covers every major policy type in one place.

What Does Motorcycle Insurance Cover in 2026?

Motorcycle insurance covers far more than most riders realize — and the gaps in standard policies are where riders lose the most money after a claim.

Here is every coverage type available in 2026:

| Coverage Type | What It Pays For | Required by Law? |

|---|---|---|

| Liability | Injuries and property damage you cause others | ✅ Yes — most states |

| Collision | Your bike after a crash, regardless of fault | ❌ Optional |

| Comprehensive | Theft, fire, vandalism, weather damage | ❌ Optional |

| Uninsured Motorist (UM/UIM) | Your damages if hit by an uninsured driver | Varies by state |

| Medical Payments (MedPay) | Your medical bills after any accident | ❌ Optional |

| Custom Parts & Equipment | Aftermarket upgrades, chrome, saddle bags | ❌ Optional add-on |

| Safety Apparel | Helmet, jacket, gloves, boots after covered loss | ❌ Optional (Progressive only by default) |

| Roadside Assistance | Towing, battery, fuel delivery on the road | ❌ Optional |

| Lay-Up / Seasonal | Suspends riding coverage during winter months | ❌ Optional |

What Most Motorcycle Policies Silently Miss

Custom parts underinsurance is the most common and costly coverage gap. Most standard motorcycle insurance policies cap custom parts coverage at $3,000 — but many riders invest $8,000–$20,000 in modifications. Progressive lets you increase that limit up to $30,000; most competitors do not.

Safety apparel coverage is included standard only with Progressive. Helmets cost $500–$1,000, riding suits can exceed $1,000, and quality boots run $300–$500. That’s $2,500+ in gear that most motorcycle insurance policies completely ignore.

What This Means For You: If you’ve customized your bike or invested in quality riding gear, your current motorcycle insurance policy likely undercovers you by thousands of dollars. Request a coverage review before your next renewal.

The Insurance Information Institute’s motorcycle coverage guide confirms that custom parts and accessory coverage is one of the most frequently overlooked additions — and one of the cheapest to add.

How Much Does Motorcycle Insurance Cost in 2026?

The national average motorcycle insurance rate is $33/month ($396/year) for full coverage and $22/month for minimum liability-only coverage. But your actual rate depends on six major factors.

6 Factors That Determine Your Premium

| Factor | Impact on Your Rate |

|---|---|

| Age (16–25) | +40–60% above average |

| Sport or performance bike | +19% above standard bikes |

| Urban vs. rural location | +22–27% higher in cities |

| At-fault accidents or violations | +25–40% per incident |

| Full vs. minimum coverage | Full coverage costs 2–3x more |

| State of registration | Rates vary by up to 300% across states |

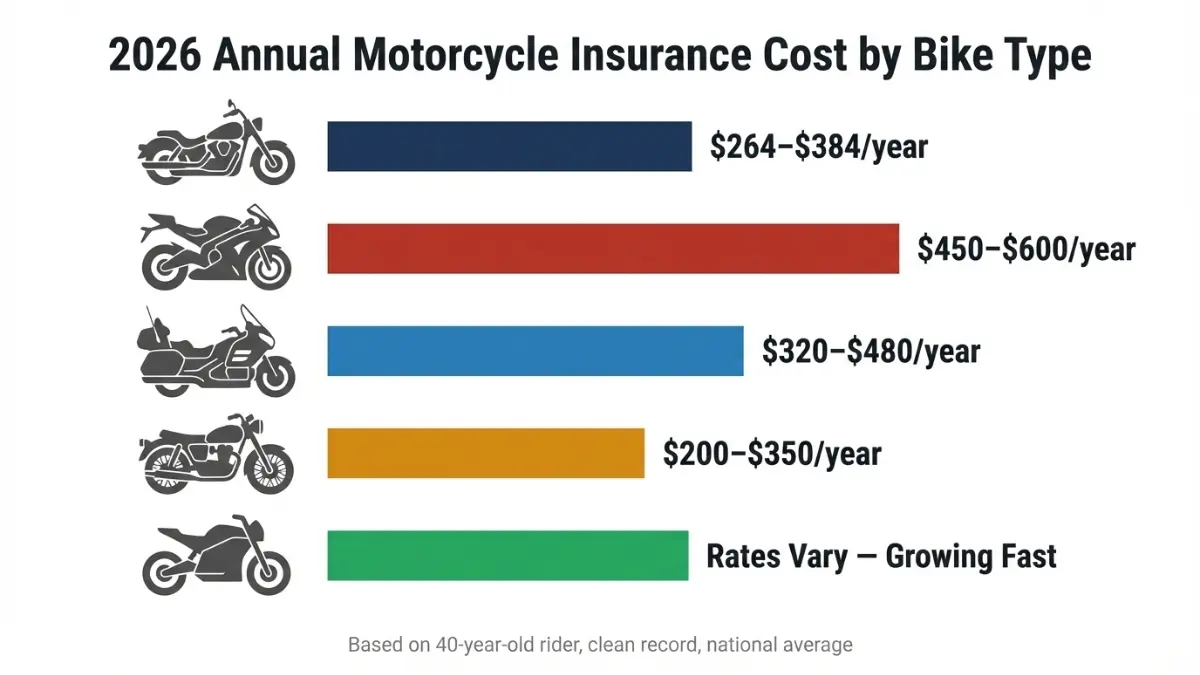

Average Motorcycle Insurance Cost by Bike Type

- Cruiser (Honda Rebel, Harley Sportster): $264–$384/year

- Sport bike (Kawasaki Ninja, Yamaha R6): $450–$600/year

- Touring bike (Honda Gold Wing): $320–$480/year

- Vintage/classic: $200–$350/year (agreed value policy)

- Electric motorcycle: Rates vary — specialty insurers now hold 8.5% of the 2025 market

Average Motorcycle Insurance Rates by State (2026)

| State | Minimum Coverage/Month | Full Coverage/Month |

|---|---|---|

| California | $11–$14 | $29–$53 |

| Maryland | $17 | $51 |

| New York | $22 | $58 |

| Texas | $14 | $38 |

| Florida | No mandate* | $44 |

| Rural Midwest | $9–$12 | $17–$26 |

*Florida does not require motorcycle insurance but enforces financial responsibility after at-fault accidents.

What This Means For You: A 35-year-old rider with a clean record insuring a standard cruiser should be paying under $30/month for full coverage in most states. Anything significantly higher signals you are overpaying.

Managing your total household financial costs — including insurance — is easier with our Debt Consolidation Calculator, which helps you assess where motorcycle insurance fits within your broader financial picture.

Best Motorcycle Insurance Companies of 2026 — Expert Panel Rankings

Our panel of 30 internationally credentialed finance experts evaluated 70+ motorcycle insurance companies across five criteria: affordability, coverage depth, claims satisfaction, financial strength (AM Best rating), and complaint ratio (NAIC index).

| Company | Best For | Avg. Monthly Rate | Expert Score | AM Best |

|---|---|---|---|---|

| Progressive | Overall value + custom bikes | $23/mo | ⭐ 4.9/5 | A+ |

| Dairyland | Cheapest rates + SR-22 | $22/mo | ⭐ 4.6/5 | A |

| GEICO | Young riders + daily commuters | $22–$31/mo | ⭐ 4.4/5 | A++ |

| Harley-Davidson | H-D owners + discount stacking | $24/mo | ⭐ 4.3/5 | A |

| Foremost | Vintage + specialty motorcycles | $33–$54/mo | ⭐ 4.1/5 | A |

| Markel | Track day + SR-22 specialty | $27/mo | ⭐ 4.0/5 | A |

| Voom | Pay-per-mile, seasonal riders | Mileage-based | ⭐ 3.9/5 | N/A |

Progressive — Best Overall Motorcycle Insurance 2026

Progressive is the #1 choice for most motorcycle insurance buyers in 2026 — and not just on price.

Why it leads:

- Insures 1 in 3 U.S. motorcycle riders

- 15 coverage options — more than any major competitor

- 12 available discounts — including up to 21% for paying in full

- OEM parts standard in all collision/comprehensive policies

- $3,000 custom parts included; upgradeable to $30,000

- Accident forgiveness from Day 1 for claims under $500

- Safety apparel coverage (helmets, jackets, boots) — unique in the market

- Available in 49 states (excludes Massachusetts)

Dairyland — Best Cheap Motorcycle Insurance

Dairyland offers the cheapest motorcycle insurance nationally at $22/month average — one-third below the national average.

Key facts:

- Rates as low as $14/month in low-cost states

- Specialist in SR-22 filings and high-risk riders

- Available in 38 states

- ⚠️ Expert note: Dairyland carries a complaint ratio 60% above industry average. It’s the best budget option — but if claims service matters, Progressive at $1/month more is the smarter choice for most riders.

GEICO — Best for Young and New Riders

GEICO offers the most competitive motorcycle insurance rates for riders aged 21–30 and covers all 50 states.

Standout features:

- Cheapest rates for riders under 25 nationally

- Up to 20% off for Motorcycle Safety Foundation instructors

- Includes $2,000 accessories coverage at no extra cost

- Partners with Hagerty for vintage and collector bikes

- 10% mature rider discount for riders 50+

For riders also comparing car insurance, our guide on cutting car insurance costs by 34% in 2026 covers the same discount-stacking strategies applied to auto policies.

How to Save $500+ on Motorcycle Insurance — 9 Proven 2026 Strategies

This is where most riders leave hundreds of dollars on the table every year. The strategies below are stackable — meaning you can combine them for compounding savings.

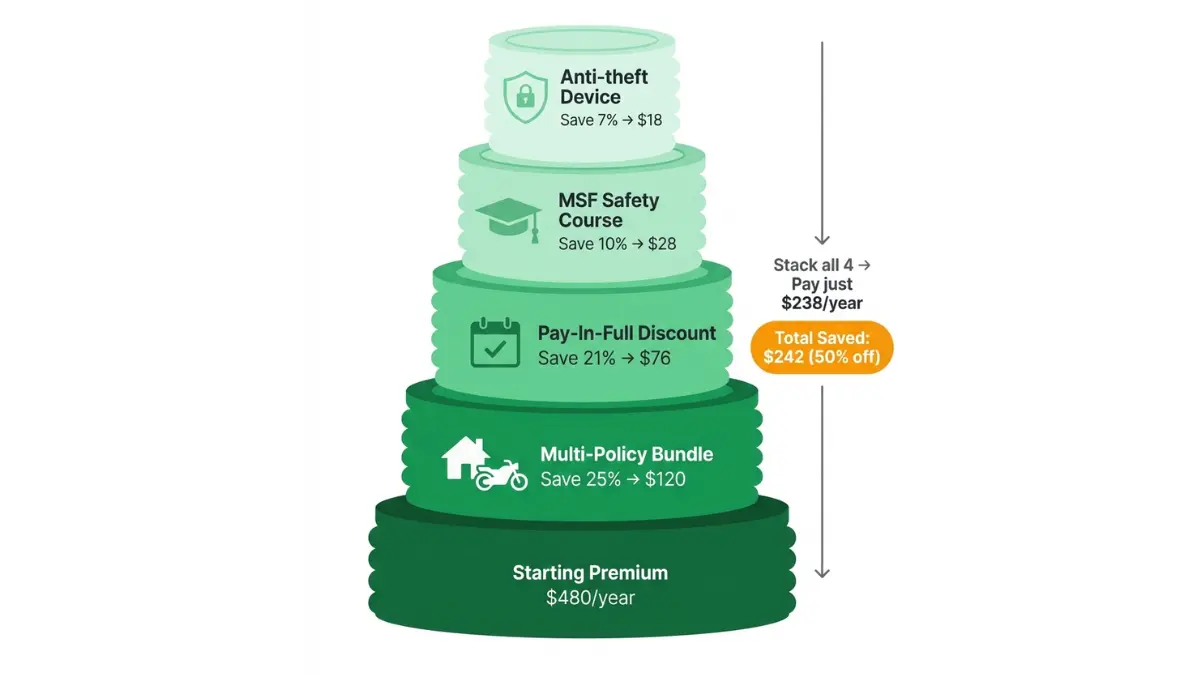

Strategy 1: Stack Multiple Discounts (The Most Powerful Move)

Here is a real savings simulation for a rider paying $480/year for full coverage motorcycle insurance:

| Discount Applied | Savings | Running Premium |

|---|---|---|

| Starting premium | — | $480/year |

| Multi-policy bundle (+auto/home) | 25% → -$120 | $360 |

| Pay-in-full annual | 21% → -$76 | $284 |

| MSF safety course | 10% → -$28 | $256 |

| Anti-theft device | 7% → -$18 | $238/year |

| Total saved | $242/year (50%) | — |

That’s a $242 annual saving from four steps — and you haven’t changed a single dollar of coverage.

Strategy 2: Complete an MSF Safety Course

The Motorcycle Safety Foundation offers approved rider courses in every U.S. state. Completing one earns you:

- 5–15% discount at Progressive, GEICO, Harley-Davidson, and most major insurers

- Improved riding skills that reduce accident risk long-term

- Instant eligibility — no waiting period

For riders under 25, this is the single fastest discount available.

Strategy 3: Use a Lay-Up (Seasonal) Policy in Winter

If you don’t ride from November to March, you shouldn’t pay full motorcycle insurance rates during those months. A lay-up policy suspends collision and liability coverage during the off-season while keeping comprehensive coverage active.

- Savings: $80–$150/year for northern state riders

- Comprehensive stays on: protects against theft, fire, and weather damage while stored

- ⚠️ Never cancel your policy entirely — a coverage gap triggers higher renewal rates

Strategy 4: Raise Your Deductible Strategically

| Deductible Change | Annual Savings |

|---|---|

| $250 → $500 | 10–15% |

| $500 → $1,000 | 20–25% |

Rule: Only raise your deductible to a level your emergency fund can comfortably cover. Our Emergency Fund Calculator helps you determine the right threshold before adjusting.

Strategy 5: Compare at Least 3 Quotes at Every Renewal

This is the most underused and highest-impact strategy. According to the National Association of Insurance Commissioners (NAIC), identical motorcycle insurance coverage for the same rider can vary by $31/month vs. $58/month between insurers. That’s a $324/year difference for doing nothing except shopping around.

Set a calendar reminder every renewal cycle to get three fresh quotes. Ten minutes of comparison work can save $300+ annually.

Strategy 6: Bundle With Your Auto or Home Policy

Bundling your motorcycle insurance with an existing auto or homeowners policy is the largest single discount available:

- Progressive: Up to 25% multi-policy bundle

- GEICO: 23% for motorcycle + auto bundle

- Nationwide: Among the strongest bundling discounts for multi-bike households

If you’re evaluating your homeowners costs alongside this, our guide on stopping overpayment on homeowners insurance in 2026 shows how bundling works across policy types.

Strategy 7: Install an Anti-Theft Device

Motorcycle thefts exceeded 52,000 in the U.S. in 2025, which has pushed up comprehensive coverage premiums. Installing a qualifying anti-theft device (audible alarm, GPS tracker, LoJack) earns a 5–10% discount at most major insurers and directly lowers the theft-risk component of your premium.

Strategy 8: Consider Pay-Per-Mile Insurance

Riders who use their bike seasonally or log under 5,000 miles annually can save 18–35% with usage-based policies. Voom specializes in pay-per-mile motorcycle insurance — you pay a base rate plus a per-mile fee, making it ideal for weekend cruisers and collectors.

Telematics-based policies now represent 18% of all new motorcycle policies in 2025, up from 12% in 2023.

Strategy 9: Maintain a Clean Riding Record

A single at-fault accident can raise your motorcycle insurance premium by 25–40% for three to five years. One speeding violation adds 15–20%. The compounding cost of violations dwarfs any short-term discount — a clean record is your most valuable long-term savings asset.

What This Means For You: A California rider bundling policies, paying in full, and completing the MSF course can realistically drop from $636/year to under $300/year — a saving of over $330 with zero reduction in coverage.

Which Motorcycle Insurance Is Right for Your Situation?

Not every rider needs the same policy. Here is our expert panel’s quick-match guide:

| Your Situation | Best Company | Why |

|---|---|---|

| First-time / new rider | Progressive or GEICO | Safety course discounts + flexible pricing |

| Budget rider (lowest rate) | Dairyland | $22/month national average |

| Custom or modified bike | Progressive | OEM parts + up to $30K custom coverage |

| Vintage or classic motorcycle | Foremost or Hagerty | Agreed value policies — no depreciation deduction |

| Military / USAA member | Progressive (USAA partner) | 5% USAA discount on Progressive policies |

| SR-22 filing required | Dairyland or Markel | High-risk specialist underwriters |

| Electric motorcycle | Specialty insurers | 8.5% market share growth in 2025 — verify EV coverage terms |

| Weekend / seasonal rider | Voom | Pay only for miles ridden |

| Daily commuter | GEICO | Strong claims service + nationwide coverage |

How to Switch Motorcycle Insurance Without a Coverage Gap

Switching is straightforward when done in the right order:

- Get at least 3 quotes with identical coverage limits before touching your current policy. Use the NAIC’s insurer comparison tool to check complaint ratios before committing.

- Set your new policy start date to the day before your current policy ends — never leave a single day uncovered. A coverage gap triggers rate increases at your next renewal.

- Cancel in writing and request a pro-rata refund for any unused premium days. Most insurers process this within 7–14 business days.

For riders managing multiple insurance policies alongside debt and savings goals, our Debt Consolidation Calculator and Simple Budget Guide can help you build a full financial picture.

Frequently Asked Questions — Motorcycle Insurance 2026

1. Is motorcycle insurance required by law in the USA?

Yes, in 49 states. Most require minimum liability coverage. Florida is the exception but enforces financial responsibility rules after at-fault accidents. Always verify your state’s minimums before riding.

2. How much is motorcycle insurance per month on average?

The national average is $22–$33/month. Dairyland averages $22/month for the cheapest motorcycle insurance; full coverage national average is $33/month.

3. Why is motorcycle insurance cheaper than car insurance?

Motorcycles cause less property damage in crashes and cost less to repair or replace than cars. This lowers insurer risk and reduces premiums significantly.

4. What is full coverage motorcycle insurance?

Full coverage combines liability, collision, and comprehensive coverage. It costs 2–3x more than liability-only but protects your bike against theft, accidents, and weather events.

5. Can I pause motorcycle insurance during winter?

Yes — this is a lay-up policy. You keep comprehensive coverage (protecting against theft and weather) and suspend riding coverage, saving $80–$150/year for seasonal riders.

6. Does completing an MSF safety course lower my motorcycle insurance rate?

Yes. Progressive, GEICO, and Harley-Davidson all offer 5–15% discounts for Motorcycle Safety Foundation graduates. The course also improves riding safety long-term.

7. What is SR-22 motorcycle insurance?

An SR-22 is a state-required financial responsibility certificate after serious violations. Dairyland and Markel specialize in SR-22 motorcycle insurance for high-risk riders.

8. Is motorcycle insurance more expensive for sport bikes?

Yes — sport bike insurance averages 19% higher than standard motorcycles due to higher speed risk and claims frequency with insurers.

9. Can I insure a custom or modified motorcycle?

Yes, but verify your policy covers aftermarket parts. Progressive includes $3,000 custom parts as standard; Foremost specializes in high-value custom builds with higher limits.

10. How do I switch motorcycle insurance without a coverage gap?

Get new quotes first, set the new policy start date before canceling the old one, then cancel in writing and request a pro-rata premium refund for unused days.

11. Does my motorcycle insurance cover riding in other U.S. states?

Yes — most standard U.S. policies extend liability coverage to all 50 states. Confirm coverage terms separately if riding in Canada or Mexico, as international coverage varies by insurer.

⚖️ Disclaimer

This article is for educational and informational purposes only and does not constitute financial, legal, or insurance advice. Motorcycle insurance rates, coverage options, discount availability, and legal requirements vary by state, insurer, and individual rider profile. Data and rate figures cited reflect research available as of February 2026 and are subject to change. Always consult a licensed insurance professional before purchasing, modifying, or canceling any insurance policy.

For more expert insurance guides, explore our complete coverage at financeauthorityhub.com.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.