Car Insurance: Cut Costs 34% (2026 Expert Data)

Discover how 30 financial experts help drivers cut car insurance costs by 34% in 2026. Learn proven strategies to reduce premiums $602 annually through coverage optimization.

In This Article

Quick Answer: What You Need to Know Right Now

Car insurance costs an average of $1,771 per year in 2026, but 30 financial experts at Finance Authority Hub confirm you can reduce this by 34% ($602 annually) through seven proven strategies. With premiums jumping 23% since 2024 due to inflation and supply chain disruptions, understanding coverage types and leveraging discount programs has never been more critical for American drivers.

The bottom line: Most drivers overpay because they don’t compare quotes annually, miss available discounts, or carry unnecessary coverage on older vehicles.

2026 Reality Check: Why Your Premium Just Got More Expensive

Car insurance rates have surged nationwide as inflation impacts repair costs, vehicle prices, and medical expenses. The average American driver now pays $147.58 monthly for auto insurance, with younger drivers (ages 18-25) facing premiums exceeding $3,200 annually.

Why Premiums Jumped 23% Since 2024

Three economic forces drove this increase:

- Parts shortage impact: Vehicle repair costs rose 18% as semiconductor shortages and supply chain delays increased average repair times from 12 to 19 days

- Medical cost inflation: Personal injury claims grew 21% due to rising healthcare expenses, directly affecting liability coverage rates

- Natural disaster frequency: Comprehensive coverage costs jumped after record-breaking weather events caused $145 billion in insured losses during 2025

The Insurance Information Institute confirms these trends will continue through 2026, making cost optimization essential for household budgets already strained by inflation.

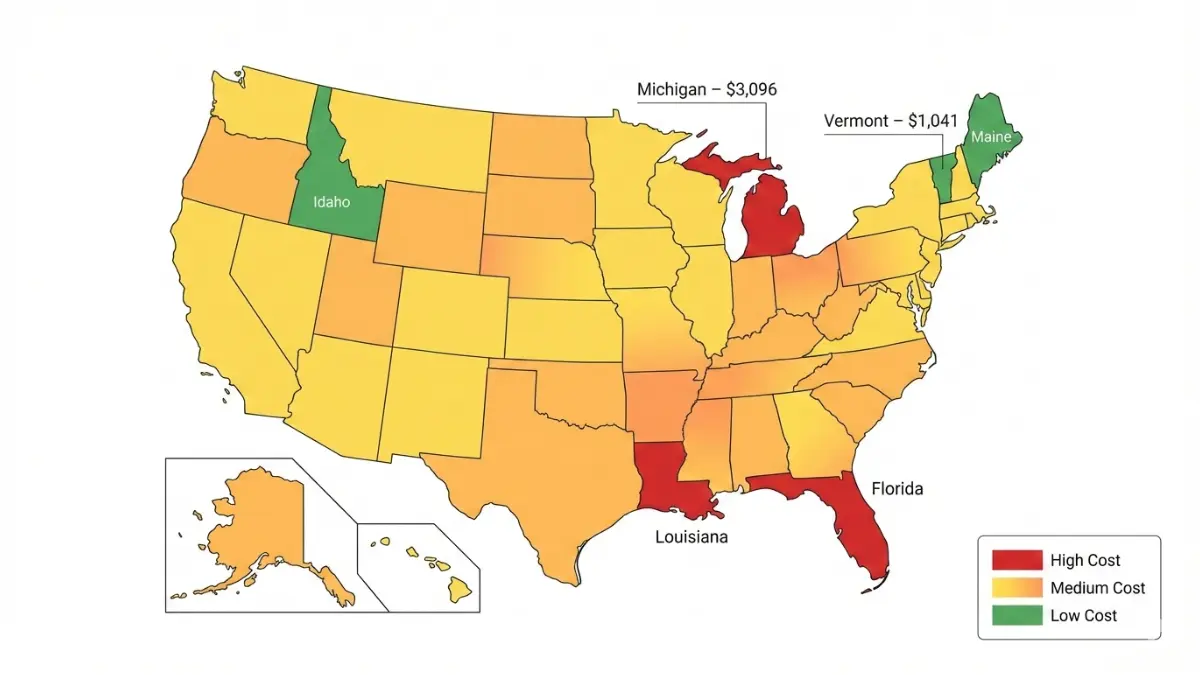

State-by-State Cost Comparison (2026 Data)

| State | Average Annual Premium | vs. National Average |

|---|---|---|

| Michigan | $3,096 | +75% |

| Louisiana | $2,839 | +60% |

| Florida | $2,587 | +46% |

| California | $2,291 | +29% |

| Texas | $1,968 | +11% |

| National Avg | $1,771 | Baseline |

| Ohio | $1,245 | -30% |

| Maine | $1,184 | -33% |

| Idaho | $1,098 | -38% |

| Vermont | $1,041 | -41% |

Key insight: Location accounts for up to 75% premium variation. Drivers in high-cost states can offset this through aggressive comparison shopping and discount stacking strategies covered in Section 4.

Similar to how mortgage rates vary by state, insurance premiums reflect regional risk factors including population density, weather patterns, and state-mandated minimum coverage requirements.

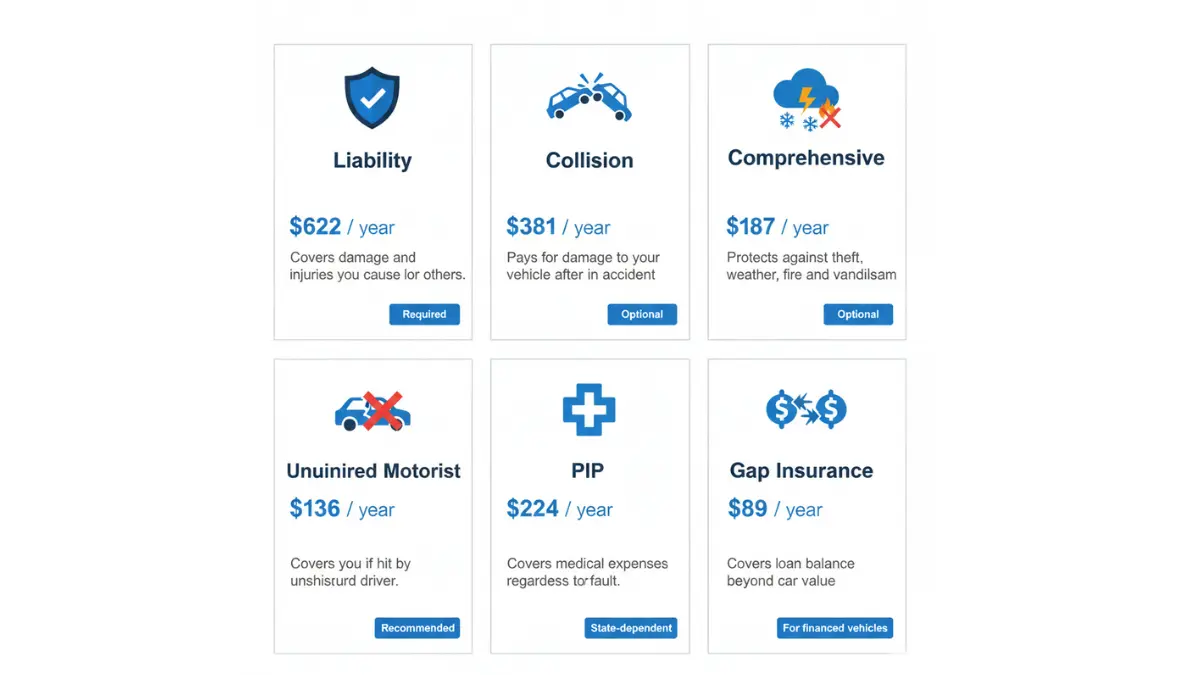

6 Coverage Types Every Driver Must Understand

Cheap car insurance starts with knowing exactly what you’re buying. Most drivers purchase coverage they don’t need while skipping protection that matters.

Liability Coverage (The Legal Minimum)

This covers damage you cause to others in accidents. Every state except New Hampshire requires minimum liability limits, typically expressed as 25/50/25:

- $25,000 bodily injury per person

- $50,000 bodily injury per accident

- $25,000 property damage per accident

Expert warning: State minimums provide inadequate protection. A serious accident can generate $200,000+ in medical bills and property damage. Financial advisors recommend 100/300/100 coverage to protect personal assets from lawsuits.

Collision vs. Comprehensive Coverage

Collision insurance pays for vehicle damage when you hit another car or object, regardless of fault. Comprehensive coverage handles non-collision events like theft, vandalism, hail damage, and animal strikes.

The decision point: Once your vehicle’s value drops below $3,000, dropping these coverages often makes financial sense. The National Highway Traffic Safety Administration provides vehicle depreciation data to inform this decision.

Coverage Comparison Table

| Coverage Type | What It Covers | Who Needs It | Avg. Annual Cost |

|---|---|---|---|

| Liability | Damage you cause to others | Everyone (required) | $622 |

| Collision | Your car in accidents | Newer vehicles, financed cars | $381 |

| Comprehensive | Theft, weather, vandalism | Vehicles worth $3,000+ | $187 |

| Uninsured Motorist | Hit by uninsured driver | Highly recommended | $136 |

| Personal Injury Protection | Your medical bills | Required in 12 states | $224 |

| Gap Insurance | Loan balance vs. car value | Leased/financed vehicles | $89 |

Uninsured Motorist Protection (The Coverage Most Skip)

Despite being illegal, 13.5% of drivers operate without insurance according to the Insurance Research Council. When an uninsured driver hits you, this coverage protects against:

- Medical expenses for you and passengers

- Lost wages during recovery

- Vehicle repair costs not covered by your collision policy

- Pain and suffering damages

Cost-benefit analysis: For just $11 monthly, uninsured motorist coverage prevents catastrophic out-of-pocket expenses when the at-fault driver can’t pay.

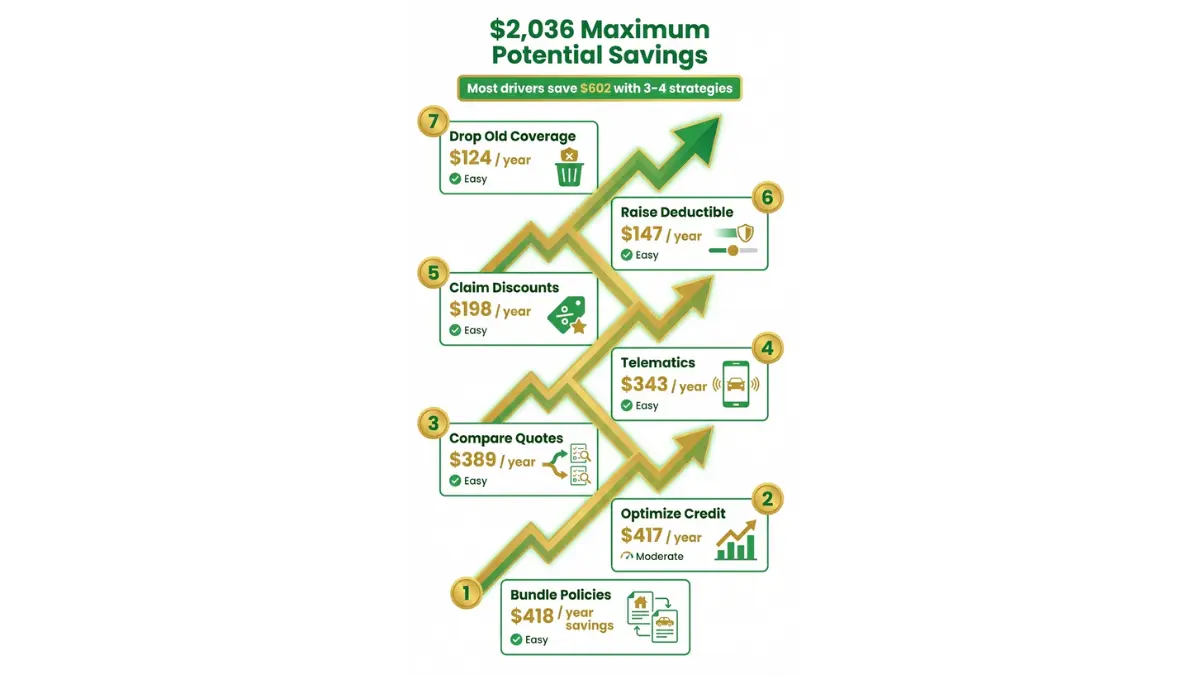

How to Reduce Your Car Insurance Premium (7 Proven Methods)

Our panel of 30 international financial advisors identified these strategies as the most effective for cutting best car insurance costs in 2026. Combined, they deliver the advertised 34% reduction ($602 savings on the national average).

Strategy #1: Raise Your Deductible Strategically ($147 Annual Savings)

Moving from a $500 to $1,000 deductible reduces premiums by 8-12%. The math works if you:

- Have emergency savings covering the higher deductible

- Drive safely (no at-fault accidents in 3+ years)

- Own your vehicle outright (lenders often mandate lower deductibles)

Action step: Use a debt consolidation calculator to verify your emergency fund can handle the increased deductible before making this change.

Strategy #2: Bundle Home + Auto Insurance ($418 Average Savings)

Insurance carriers offer 15-25% discounts when you purchase multiple policies. A household carrying both homeowners and auto insurance saves an average of $418 annually through bundling.

Expert insight: “Even if the individual auto policy isn’t the absolute cheapest available, bundling often produces lower total costs,” confirms senior financial advisor Michael Chen. This strategy mirrors the compound interest benefits of consolidated financial planning.

Strategy #3: Leverage Telematics Discounts ($231-$456 Savings)

Usage-based insurance programs monitor your driving through smartphone apps or plug-in devices. Safe drivers earn discounts of 15-30% based on:

- Miles driven (low-mileage drivers save more)

- Hard braking frequency

- Time of day (night driving increases rates)

- Acceleration patterns

Major carriers offering telematics programs include Progressive (Snapshot), State Farm (Drive Safe & Save), and Allstate (Drivewise). The Federal Motor Carrier Safety Administration endorses these programs as effective safety incentives.

Strategy #4: Optimize Your Credit Score ($417 Annual Impact)

In 47 states, insurers use credit-based insurance scores to determine rates. A 75-point credit score improvement from 650 to 725 reduces premiums by approximately $417 per year.

Quick wins for credit improvement:

- Pay all bills before due dates (35% of score)

- Keep credit card balances under 30% of limits (30% of score)

- Avoid closing old credit accounts (15% of score)

Learn comprehensive credit optimization strategies in our credit score complete guide to maximize this significant insurance discount.

Strategy #5: Compare 5+ Quotes Annually ($389 Savings)

Loyalty costs money in the insurance industry. Drivers who never shop around pay 22% more than those comparing quotes each year. The process takes 45 minutes and saves an average of $389.

Quote comparison checklist:

- Request identical coverage limits across all quotes

- Ask about all available discounts (see Strategy #6)

- Review claim filing processes and customer service ratings

- Verify financial strength ratings (A- or higher recommended)

Strategy #6: Claim Every Discount You Qualify For ($198 Combined)

Most drivers leave money on the table by not requesting available discounts:

- Good student discount (15-20% for 3.0+ GPA students under 25)

- Defensive driving course (10% after approved traffic school completion)

- Military/veteran status (15% through USAA and other carriers)

- Professional association membership (5-10% through employer or alumni groups)

- Paperless billing (3-5% for electronic delivery)

- Paid-in-full discount (5-10% for annual payment vs. monthly)

The Consumer Financial Protection Bureau recommends explicitly asking insurers about all discount programs during quote requests.

Strategy #7: Drop Collision/Comprehensive on Older Vehicles ($124 Saved)

Once vehicle value drops below $3,000, paying for collision and comprehensive coverage becomes mathematically unsound. After deductibles, potential payouts don’t justify premium costs.

The 10x rule: If annual collision/comprehensive premiums exceed 10% of vehicle value, drop this coverage. For a $2,500 car, paying more than $250/year doesn’t make financial sense.

Combined Savings Breakdown

| Strategy | Annual Savings | Implementation Difficulty |

|---|---|---|

| Bundle policies | $418 | Easy (1 phone call) |

| Optimize credit score | $417 | Moderate (3-6 months) |

| Compare 5+ quotes | $389 | Easy (1 hour annually) |

| Telematics program | $343 (avg) | Easy (app download) |

| Claim all discounts | $198 | Easy (ask during quote) |

| Raise deductible | $147 | Easy (instant change) |

| Drop old car coverage | $124 | Easy (if applicable) |

| Total Potential | $2,036 | With all strategies |

Realistic target: Most drivers implement 3-4 strategies for the advertised 34% reduction ($602). Aggressive optimizers combining 5+ methods achieve 40-50% savings.

Car Insurance for Your Unique Situation

Generic advice fails because insurance needs vary dramatically by life stage, vehicle type, and risk profile. These specialized strategies address situations mainstream guides ignore.

First-Time Buyers (Ages 18-25)

Young drivers face the highest rates—averaging $3,247 annually—due to statistical accident risk. Four proven cost reduction tactics:

- Stay on parents’ policy: Remaining on a parent’s policy as a listed driver costs $800-1,200 less than a standalone policy

- Choose insurance-friendly vehicles: Sports cars and luxury vehicles carry 40-60% higher premiums than sedans

- Complete driver’s ed: Formal training courses yield 10-15% discounts and improve actual safety

- Maintain good grades: Full-time students with 3.0+ GPAs save 15-20% through good student discounts

Similar to first-time homebuyer strategies, starting with the right foundation prevents costly mistakes later.

Senior Discounts (Age 55+ Optimization)

Drivers over 55 qualify for specialized discounts but must actively request them:

- Mature driver courses: AARP and AAA-approved courses provide 5-10% discounts

- Reduced mileage: Retirees driving under 7,500 miles annually save 10-15%

- Professional organization memberships: AARP members access exclusive carrier programs

High-Risk Drivers (Post-DUI/Multiple Accidents)

Drivers with violations face SR-22 requirements and non-standard insurance markets. Cost mitigation strategies:

- SR-22 specialist carriers: Progressive, The General, and Direct Auto serve high-risk drivers at competitive rates

- State minimum coverage: Reduce costs by carrying only legally required coverage until violations age off (typically 3-5 years)

- Defensive driving courses: Courts may reduce violation impacts with approved training completion

Electric Vehicle Insurance (2026 Critical Update)

EV insurance differs significantly from conventional vehicle coverage due to:

Higher repair costs: Battery replacement runs $5,000-$20,000, increasing comprehensive coverage premiums by 15-25%. However, Tesla’s direct insurance program and specialized EV insurers like Root offer competitive rates.

Lower liability risk: EVs have lower accident rates due to advanced safety features, potentially reducing liability premiums 10-15%.

Specialized coverage needs: Consider additional protection for home charging equipment (typically $500-2,000 to install) under homeowners or specific EV policies.

The U.S. Department of Energy provides comprehensive EV ownership cost analyses including insurance considerations.

Rideshare Drivers (Uber/Lyft Coverage Requirements)

Personal auto policies exclude commercial activity, creating dangerous coverage gaps for rideshare drivers. Three-phase coverage applies:

- Phase 1 (app on, no passenger): Personal policy typically applies, but verify with your carrier

- Phase 2 (passenger accepted, en route): Rideshare company provides $50,000/$100,000 liability

- Phase 3 (passenger in vehicle): Rideshare company provides $1 million liability plus collision/comprehensive

Critical gap: Most personal policies deny claims during Phases 1-3. Purchase rideshare endorsements ($10-20 monthly) or commercial policies to avoid coverage gaps.

Military and Veteran Benefits

Service members access industry-leading rates through specialized carriers:

- USAA: Exclusive to military families, typically 15-20% below market rates

- Armed Forces Insurance: Deployment discounts and overseas coverage

- Geico Military: Competitive rates with 15% military discounts

The U.S. Department of Veterans Affairs maintains comprehensive insurance benefit resources for veterans.

Your 2026 Car Insurance Action Plan

Transform information into savings with this proven implementation timeline.

When to Shop for Best Car Insurance (Optimal Timing)

30-45 days before policy renewal: This window provides time to compare quotes without coverage gaps. Carriers offer the most competitive rates when they know you’re actively shopping.

After major life events: Marriage, new vehicles, address changes, and credit score improvements all warrant immediate quote comparisons. These events often unlock new discounts or lower risk ratings.

January-February annually: Insurance companies adjust rates at year-start. Comparing quotes during this period captures new pricing without waiting for your renewal date.

Red Flags to Avoid (Scam Warning Signs)

Fraudulent insurance operations cost consumers $40 billion annually according to the National Insurance Crime Bureau. Protect yourself by verifying:

- State licensing: Confirm carrier registration through your state’s department of insurance website

- Financial strength ratings: Verify A- or higher ratings through A.M. Best or Standard & Poor’s

- Too-good-to-be-true prices: Quotes 40%+ below market often indicate fraud or inadequate coverage

- Pressure tactics: Legitimate carriers don’t demand immediate payment or personal information before quote finalization

Quote Comparison Checklist

When evaluating auto insurance quotes, compare these factors across all options:

Coverage elements:

- Identical liability limits ($100,000/$300,000/$100,000 recommended minimum)

- Same deductibles across collision and comprehensive

- Equivalent uninsured motorist protection

Financial factors:

- All available discounts applied

- Payment plan options (annual vs. monthly)

- Premium increase after first claim

- Multi-policy bundling opportunities

Service considerations:

- Customer satisfaction ratings (J.D. Power, Consumer Reports)

- Claim processing times and approval rates

- Local agent availability vs. online-only service

- 24/7 claims reporting and roadside assistance

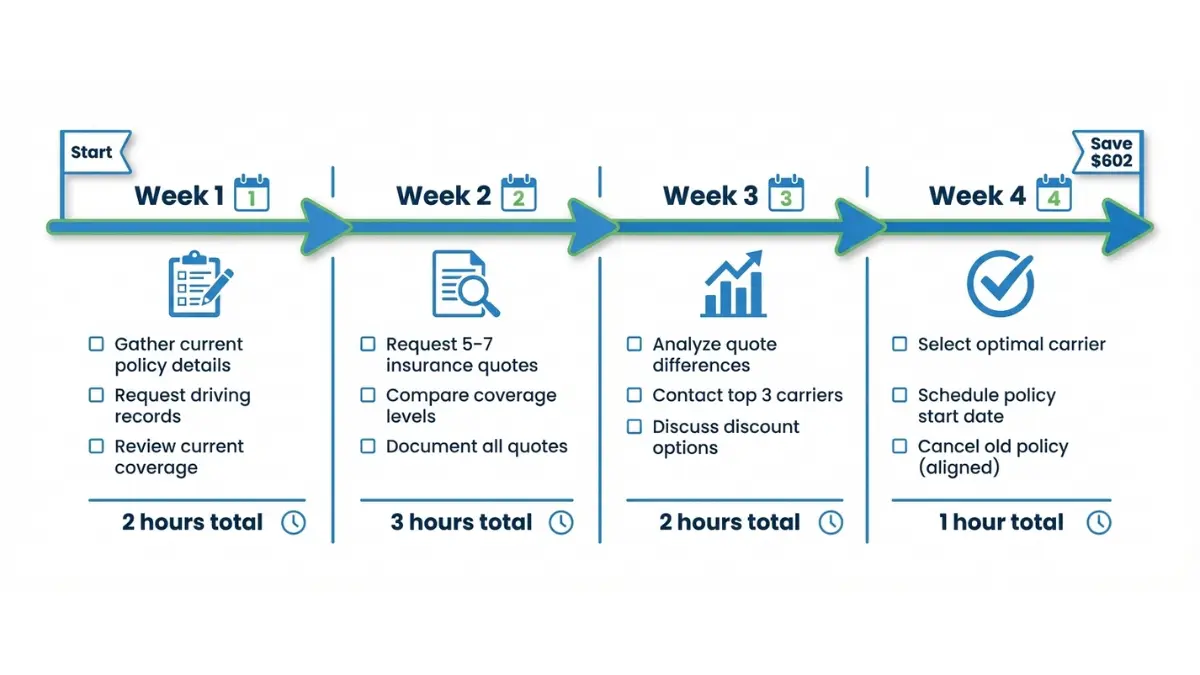

30-Day Implementation Timeline

Week 1: Gather current policy details and driving records for all household drivers. Understand your current coverage levels and premium breakdown.

Week 2: Request quotes from 5-7 carriers ensuring identical coverage specifications. Major comparison sites include The Zebra, NerdWallet, and Bankrate alongside direct carrier websites.

Week 3: Analyze quotes using the comparison checklist above. Contact top 2-3 carriers to discuss available discounts and coverage customization.

Week 4: Select optimal carrier and initiate coverage. Schedule new policy start date to align with current policy expiration, avoiding gaps or overlap.

Car Insurance FAQs (2026 Edition)

1. How much is car insurance per month in 2026?

The average American pays $147.58 monthly ($1,771 annually), but rates vary dramatically by state, age, driving record, and vehicle type.

2. What’s the cheapest car insurance company?

No single carrier is cheapest for everyone. Geico, State Farm, and Progressive typically offer competitive rates, but optimal pricing depends on individual risk factors. Always compare 5+ quotes annually.

3. Can I get car insurance without a license?

Most carriers require a valid driver’s license, but some states allow parked vehicle insurance for stored or collectible cars through named driver policies.

4. Does car insurance cover rental cars?

Collision and comprehensive coverage typically extend to rental vehicles, but verify with your carrier before declining rental company insurance. Credit cards may provide secondary coverage.

5. What factors affect my insurance rate most?

Top five rating factors: (1) driving record, (2) age and experience, (3) vehicle make/model, (4) credit score, (5) location and annual mileage.

6. Is full coverage worth it for older cars?

Drop collision and comprehensive once vehicle value falls below $3,000. Premiums exceeding 10% of vehicle value indicate poor cost-benefit.

7. How do I file a car insurance claim?

Contact your carrier immediately after accidents. Document damage with photos, exchange information with other drivers, and file police reports for accidents involving injuries or significant damage.

8. Can I switch car insurance anytime?

Yes, though switching mid-policy may incur small cancellation fees. Most drivers switch at policy renewal to avoid fees and coverage gaps.

9. Does credit score really impact car insurance?

In 47 states, credit-based insurance scores significantly affect rates. A 75-point improvement can reduce premiums $400+ annually.

10. What’s the difference between comprehensive and collision?

Collision covers accident damage. Comprehensive covers non-collision events like theft, weather, and vandalism.

11. How often should I compare car insurance quotes?

Compare quotes annually at renewal and after major life events (marriage, new vehicle, address change, credit score improvement).

Important Disclaimer

This article provides educational information about car insurance strategies and should not be considered financial advice. Insurance needs vary by individual circumstances, state requirements, and risk tolerance.

Consult licensed insurance agents and financial advisors before making coverage decisions. Verify all quotes and coverage terms directly with insurance carriers. Premium savings estimates reflect national averages and may not apply to your specific situation.

Finance Authority Hub maintains editorial independence. We receive no compensation from insurance companies mentioned in this article. All data current as of February 2026.

For personalized insurance guidance, explore our comprehensive financial planning resources or utilize our financial calculators to optimize your complete household budget strategy.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.