Affordable Car Insurance: Save $1,100 in 2026 — Expert-Verified Guide

Rates jumped 12% since 2024. But savvy drivers are still finding affordable car insurance from $41/mo. Here’s exactly how to save $1,100 before your next renewal.

In This Article

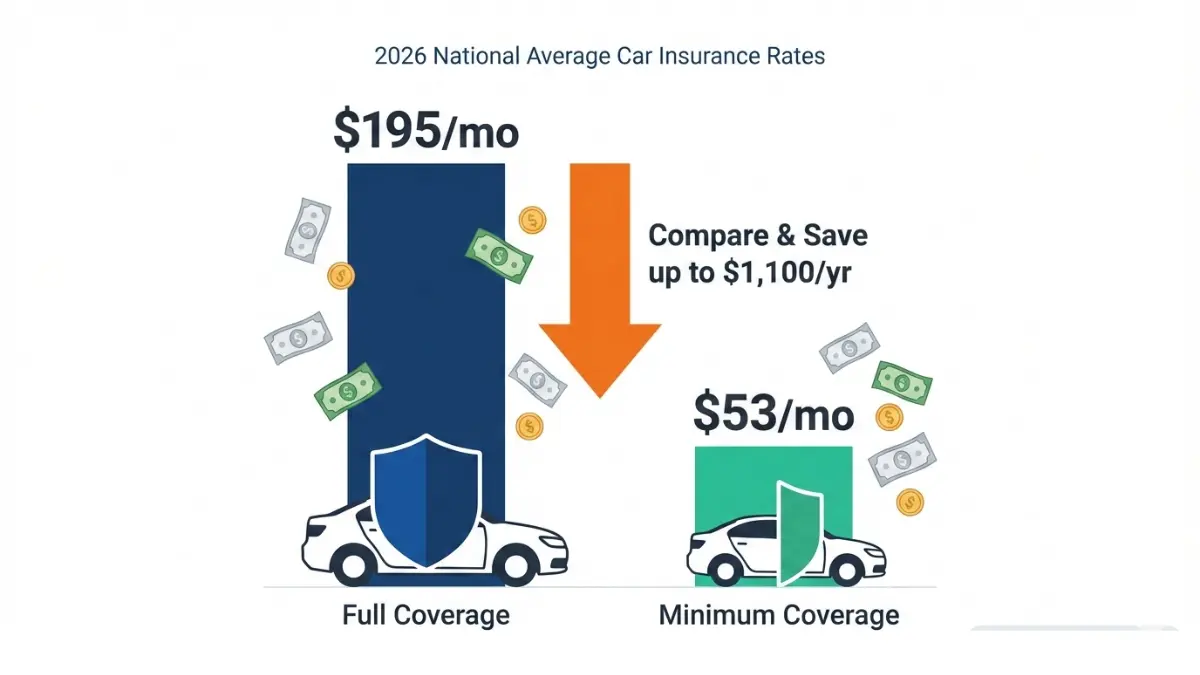

The national average for affordable car insurance in 2026 is $195/month ($2,340/year) for full coverage and $53/month ($633/year) for minimum coverage, according to NerdWallet’s February 2026 analysis. Travelers is the cheapest large insurer at $139/month. Drivers who compare at least 3–5 quotes save an average of $1,100 per year — yet most Americans never shop around.

What You’re Actually Paying — And What You Shouldn’t Be

Affordable car insurance is no longer a given. Rates have climbed more than 12% since 2024, and many drivers are silently overpaying hundreds of dollars every year without realizing it.

Here’s the 2026 national rate snapshot you need to bookmark:

| Coverage Type | National Average (2026) | Cheapest Available |

|---|---|---|

| Full Coverage | $195/mo · $2,340/yr | $139/mo — Travelers |

| Minimum Coverage | $53/mo · $633/yr | $41/mo — GEICO |

| Young Driver (Age 20) | $313/mo | Progressive |

| Senior Driver (Age 50) | $125/mo | Travelers |

| Military Family | — | $22/mo — USAA |

The problem? Most Americans renew without checking competitors. That’s the $1,100 mistake. According to LexisNexis Risk Solutions’ 2025 U.S. Auto Insurance Trends Report, record levels of policy switching in 2024 are saving drivers real money — but only those who act.

The good news: You don’t need to be an expert to cut your cheap car insurance bill. You just need a plan. Explore our insurance savings hub for a full overview of strategies across all policy types.

Why Car Insurance Rates Are Rising in 2026 — And What’s Pushing YOUR Bill Higher

The 2026 Rate Crisis: What Nobody Is Telling You

Car insurance rates didn’t just go up randomly. Three specific forces are driving your premium in 2026:

- Tariffs on auto parts — New import tariffs are pushing vehicle repair costs higher, which means insurers pay more per claim, which means you pay more per month.

- Rising labor costs — Collision repair labor is up significantly since 2022, adding directly to insurer loss ratios.

- Technology-heavy vehicles — Modern cars with sensors, cameras, and advanced driver assistance systems (ADAS) cost far more to repair after even minor accidents.

The Insurance Information Institute’s auto insurance data confirms: the average auto insurance expenditure rose 6.1% in a single year (2021–2022), and the pace has accelerated sharply since.

The 7 Factors That Determine YOUR Rate

Your car insurance quotes comparison depends on how insurers score these factors:

- Age — Drivers under 25 pay the most; rates peak at 16–19 and fall steadily through your 30s.

- ZIP Code — Urban ZIP codes face higher theft rates, denser traffic, and costlier claims.

- Credit Score — In most states, poor credit raises your rate by an average of 78% (Bankrate, 2026).

- Driving Record — One at-fault accident raises rates by an average of 42%. A DUI can double them.

- Vehicle Type — Sports cars, luxury models, and EVs carry higher premiums due to repair costs.

- Coverage Level — Full coverage costs ~3.7× more than minimum-only.

- Claims History — Even one claim stays on your record 3–5 years.

Cheapest vs. Most Expensive States (2026)

| Cheapest States | Avg. Full Coverage/Yr | Most Expensive States | Avg. Full Coverage/Yr |

|---|---|---|---|

| Wyoming | ~$1,300 | Louisiana | ~$3,600+ |

| Vermont | ~$1,350 | Florida | ~$3,300+ |

| New Hampshire | ~$1,400 | New Jersey | ~$2,991 |

| Idaho | ~$1,450 | New York | ~$2,900+ |

| Maine | ~$1,480 | Michigan | ~$2,800+ |

Key Insight: If you live in Florida or Louisiana, shopping around isn’t optional — it’s financial survival. North Carolina drivers, by contrast, pay 32% less than the national average.

What This Means For You: Your state matters almost as much as your driving record. If you’re managing other high-cost obligations alongside your premium, our debt consolidation calculator can help you see the full picture of where your money is going.

The 7 Most Affordable Car Insurance Companies of 2026 — Matched to YOUR Profile

No single company offers the lowest car insurance for every driver. Here’s who wins for each situation:

🥇 Best Overall: Travelers — $139/mo Full Coverage

Travelers is the cheapest large insurer in the nation for full coverage as of February 2026 (NerdWallet analysis). It offers accident forgiveness, strong coverage options, and is available in 42 states.

Best for: Good drivers aged 30–55 seeking the cheapest full coverage car insurance.

🥈 Best for Discounts: GEICO — $41/mo Minimum Coverage

GEICO offers 23 distinct discount categories — the most of any major insurer. Minimum coverage starts at $41/month nationally.

Best for: Drivers who want to stack multiple discounts to save on car insurance fast.

🥉 Best for Young Drivers: Progressive — from $313/mo

Progressive’s Snapshot telematics program rewards safe driving with savings up to 30%. It’s also the most competitive large insurer for drivers with violations on their record.

Best for: Young drivers (18–25) and high-risk drivers seeking affordable auto insurance.

🏅 Best for Military Families: USAA — $22/mo Minimum Coverage

USAA offers the nation’s single cheapest car insurance — $22/month for liability — but is exclusive to military members, veterans, and their families.

Best for: Active duty, veterans, and eligible family members. Non-negotiable if you qualify.

🏅 Best Rate Lock: Erie Insurance

Erie’s unique Rate Lock feature freezes your premium year over year — even after an accident or speeding ticket. Your rate only changes if you move, add a vehicle, or change drivers.

Best for: Drivers in Erie’s 12-state coverage area who want price stability over time.

🏅 Best for Seniors (50+): Travelers — $125/mo

Rates drop sharply in your 50s. Travelers’ average for 50-year-old drivers is $125/month — the cheapest among major national carriers.

Best for: Drivers aged 50–64 with clean records.

🏅 Best for Bad Credit Drivers: Shop by State First

Poor credit raises rates by up to 78% in most states. However, 6 states ban credit as a rating factor entirely: California, Hawaii, Massachusetts, Michigan, North Carolina, and Pennsylvania. If you live in one of these states, your credit score cannot legally raise your rate.

Best for: Drivers with credit challenges — especially in credit-ban states where affordable auto insurance for bad credit is legally protected.

| Company | Full Coverage/Mo | Min Coverage/Mo | Standout Feature |

|---|---|---|---|

| Travelers | $139 | $41 | Cheapest full coverage nationally |

| GEICO | ~$156 | $41 | Most discount options (23) |

| USAA | $84 | $22 | Military-only; lowest rates period |

| Progressive | Varies | — | Best for high-risk + telematics |

| Erie | Varies | — | Rate Lock; regional only |

| State Farm | ~$180 | $41 | Best customer satisfaction |

| Auto-Owners | Regional | Regional | Best regional option (26 states) |

For deeper analysis of what comprehensive protection actually covers, read our guide on comprehensive car insurance before choosing your coverage level.

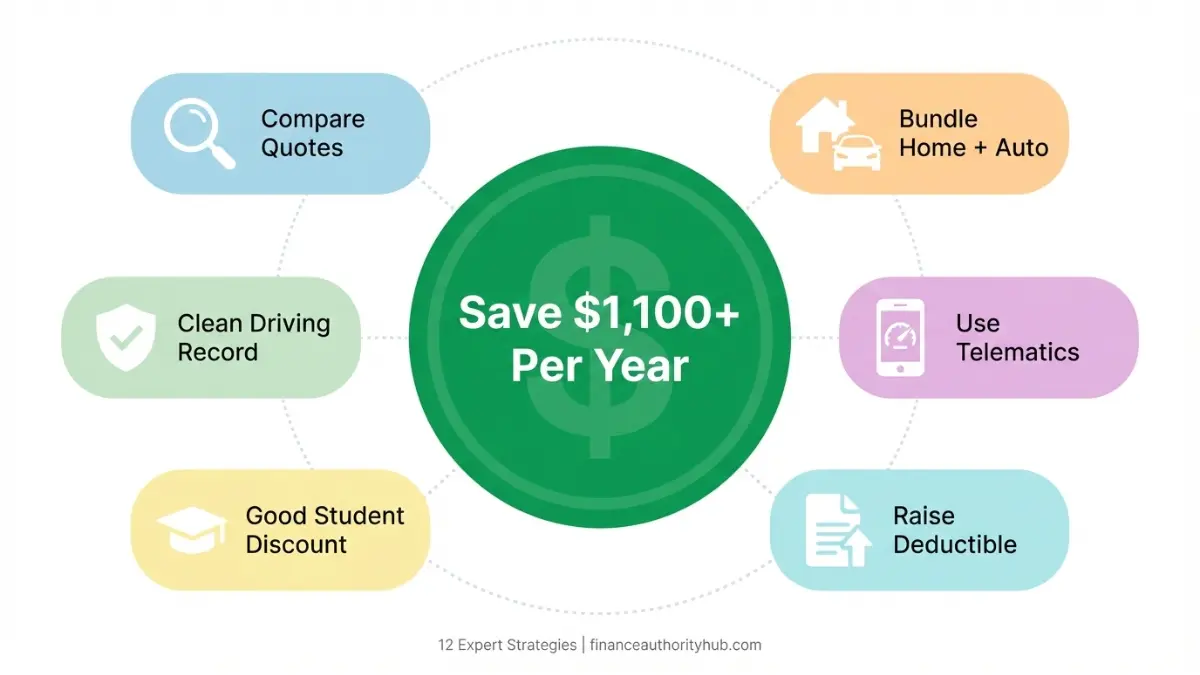

12 Proven Strategies to Save $1,100+ on Car Insurance in 2026

Real story: One driver reported by AARP saved $2,680 in a single afternoon by calling their broker and asking them to shop the market. Here’s the exact playbook.

The National Association of Insurance Commissioners (NAIC) confirms that drivers who regularly comparison shop consistently pay less than those who auto-renew. These strategies work.

The 12-Move Savings Playbook

1. Compare 3–5 Quotes With Identical Coverage

- Use the same limits, deductibles, and coverage type across every quote.

- Potential savings: $200–$800/year

- Critical detail: Get a verified quote (uses your real MVR), not an estimate.

2. Bundle Home + Auto Insurance

- State Farm’s bundle discount averages $847/year in savings (25% off).

- Farmers offers 17% off; Nationwide 15%.

- Potential savings: $330–$900/year

If you own a home or are considering buying, see how bundling fits your overall housing picture with our home affordability calculator.

3. Raise Your Deductible From $500 to $1,000

- This alone cuts your premium by 15–20%.

- Only do this if you have emergency savings to cover the higher out-of-pocket cost.

- Potential savings: $200–$400/year

4. Enroll in Telematics (Usage-Based Insurance)

- State Farm’s Drive Safe & Save: up to 30% off.

- Progressive’s Snapshot: up to 30% savings.

- GEICO’s DriveEasy: rewards safe braking, speed, and phone use.

- Potential savings: $150–$600/year

5. Pay Your Annual Premium in Full

- Monthly installment fees add up. Paying in full saves 5–10%.

- Potential savings: $50–$200/year

6. Use the Good Student Discount

- Full-time students with a B average (3.0 GPA) qualify for 10–25% off.

- GEICO offers up to 15% for good students + an additional discount for driver’s ed.

- Potential savings: $200–$400/year

7. Drive Less → Get a Low-Mileage Discount

- Drivers under 7,500 miles/year qualify for discounts up to 20%.

- Pay-per-mile insurance (e.g., Metromile via Lemonade) is ideal if you work from home.

- Potential savings: $100–$300/year

8. Complete a Defensive Driving Course

- State-approved courses cut your rate by 5–15%.

- Online options take 4–6 hours and cost $20–$50.

- Potential savings: $50–$150/year

9. Install Anti-Theft Devices

- Anti-theft systems, GPS trackers, and immobilizers can reduce comprehensive premiums by up to 30%.

- Confirm with your insurer that aftermarket devices qualify.

- Potential savings: $50–$200/year

10. Improve Your Credit Score

- Moving from “poor” to “good” credit can cut your rate by up to 78% in credit-rated states.

- Even a 50-point credit score improvement can make a measurable difference.

- Potential savings: $300–$1,000/year

For a roadmap to fix your credit and reduce insurance costs simultaneously, see our credit score complete guide.

11. Drop Collision Coverage on Older Cars

- If your car’s value is less than 10× your annual collision premium, drop it.

- Example: A car worth $4,000 doesn’t justify $600/year in collision coverage.

- Potential savings: Full collision premium (often $400–$800/year)

12. Shop at Every Renewal — Not Every 3 Years

- Rates change every 6 months. Your current insurer is almost never the cheapest after 2 years.

- Shopping annually takes 30–60 minutes and consistently saves $100–$400 vs. auto-renewing.

- Potential savings: $100–$400/year

💡 What This Means For You: Stack even 4 of these strategies and you can realistically reach $1,100+ in annual savings — the average among drivers who actively compare car insurance quotes comparison sites each year.

You can also explore our article on car insurance cut costs for a deeper breakdown of how drivers are cutting bills by up to 34% in 2026.

Affordable Car Insurance by Driver Situation — Your 2026 Quick-Reference Guide

High-Risk Driver Situations (What Competitors Don’t Cover)

After a DUI:

- Rates can double or more. Progressive, State Farm, and Dairyland are most competitive for SR-22 situations.

- Expect elevated rates for 3–10 years depending on your state.

After an At-Fault Accident:

- In 41% of cases, a different company is cheapest after an accident than before (NerdWallet, 2025 analysis).

- Never assume your current insurer will be most affordable post-claim.

EV Owners — The Emerging Blind Spot:

- Electric vehicles still cost more to insure due to expensive parts and specialized labor.

- The gap is closing: Travelers and State Farm are most competitive for EV coverage in 2026.

- If you’re financing an EV, check how it affects your overall budget with our mortgage calculator if you’re balancing a home loan simultaneously.

Young Drivers (18–25):

- Stay on a parent’s policy as long as possible — it’s the single biggest rate reducer.

- Alternatively, Progressive’s Snapshot program rewards new young drivers with above-average telematics discounts.

Seniors (65+):

- Rates begin rising again after 70. AARP-partnered programs and Hartford’s senior-specific offerings can offset this.

- Usage-based programs are particularly valuable for lower-mileage senior drivers.

Know Your State Rights

The NAIC’s consumer resources page outlines your rights in detail by state. Key facts:

- 6 states ban credit as a rating factor: CA, HI, MA, MI, NC, PA.

- New Hampshire does not require car insurance (but you must prove financial responsibility).

- Michigan recently reformed its no-fault system, reducing some of the nation’s highest rates.

If you’re also managing vehicle financing alongside affordable car insurance, our car tax 2026 guide can help you understand the full cost of vehicle ownership this year.

Frequently Asked Questions about Affordable Car Insurance

Q1: What is the cheapest car insurance company in 2026?

Travelers offers the cheapest full coverage at $139/month nationally. GEICO leads for minimum coverage at $41/month. USAA is the cheapest overall at $22/month but is only available to military families.

Q2: What is the average cost of car insurance per month in 2026?

The national average is $195/month for full coverage and $53/month for minimum coverage, based on NerdWallet’s February 2026 analysis. Your rate will vary based on age, ZIP code, vehicle, and driving record.

Q3: How can I get affordable car insurance with bad credit?

In CA, HI, MA, MI, NC, and PA, insurers cannot use credit as a rating factor. In other states, improving your credit score or using a state-assigned risk pool can help. Shopping multiple insurers is essential since each weighs credit differently.

Q4: How do I lower my car insurance premium fast?

The fastest moves: compare 3–5 quotes today, raise your deductible, enroll in telematics, and bundle your home and auto policies. Together, these can cut your premium by 20–40% within one renewal cycle.

Q5: Is minimum coverage car insurance enough?

Minimum coverage only covers damage to others — not your own vehicle. If you own a car worth more than $10,000 or carry a loan, full coverage is recommended. The NAIC advises most drivers carry at least $100,000/$300,000 in liability limits.

Q6: Can I get affordable full coverage car insurance?

Yes. Travelers offers full coverage from $139/month for good drivers. The key is comparing quotes across at least 5 insurers and stacking discounts like bundling, safe driver, and telematics programs.

Q7: Does my credit score affect car insurance rates?

In most states, yes — poor credit raises rates by an average of 78%. However, 6 states (CA, HI, MA, MI, NC, PA) prohibit credit-based pricing entirely.

Q8: What discounts give the biggest savings?

The top three are: bundle discount (up to 25% off), telematics programs (up to 40% off), and good driver / accident-free discount (up to 10–30% off). Stack all three for maximum impact.

Q9: How often should I shop for new car insurance?

Every 12 months at renewal — or any time your life changes (new car, new address, marriage, improved credit). Rates change every 6 months, and loyalty rarely pays.

Q10: Is affordable car insurance available for young drivers?

Yes, but it requires strategy. Stay on a parent’s policy, maintain a clean record, take a driver’s ed course, and use Progressive’s Snapshot or GEICO’s DriveEasy for telematics savings.

Q11: Will car insurance rates go down in 2026?

Rates are beginning to stabilize after steep increases in 2023–2025. Some insurers are filing for rate decreases as profitability improves. However, tariff effects on repair costs may offset some relief — especially for drivers in Florida, New York, and New Jersey.

Expert Verdict

“The single biggest mistake American drivers make is treating car insurance as a set-and-forget bill. In 2026, the difference between the most and least expensive insurer for identical coverage can exceed $2,000 per year. Comparison shopping is not optional — it is a financial discipline. Combine that with smart discount stacking and credit management, and saving $1,100 or more is entirely realistic for most households.”

— Finance Authority Hub Expert Panel | Reviewed February 2026

Related Guides You Should Read Next:

- 📄 Comprehensive Car Insurance: What’s Actually Covered in 2026

- 📄 Temporary Car Insurance: Cheapest Options

- 📄 Homeowners Insurance 2026: Stop Overpaying

- 📄 Cheap Insurance: Save in 2026

- 🧮 Debt Consolidation Calculator

⚠️ Disclaimer: This article is for educational and informational purposes only and does not constitute financial, legal, or insurance advice. Car insurance rates shown are national averages sourced from published 2026 analyses and may differ significantly based on your individual driver profile, state, vehicle, and insurer. Always consult a licensed insurance professional before making coverage decisions. Finance Authority Hub does not sell insurance products.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.