Rental Car Insurance: Skip It or Buy It? (2026)

Most US drivers waste $200–$400 on rental car insurance they already have. This 2026 expert guide reveals exactly when to skip it — and when skipping costs you thousands.

In This Article

Most drivers waste $200–$400 on rental car insurance they already have. Your personal auto policy, credit card, or both may cover you completely — making the counter’s $30–$50/day upsell entirely unnecessary. But for some drivers, skipping coverage is a costly mistake that leads to a surprise bill of $1,000 or more. This guide tells you exactly which situation you’re in — in under five minutes.

Quick Decision Snapshot: Your Coverage at a Glance

| Your Situation | Best Option |

|---|---|

| Full coverage personal auto policy | Use your policy + credit card (cost: $0) |

| Credit card only, no personal auto | Use card for CDW; buy SLI at counter |

| No car, no credit card | Buy third-party (Allianz ~$11/day) |

| Renting internationally | Buy local coverage — US policy rarely applies |

| Paying with a debit card | Buy CDW at counter — zero card protection |

Key facts before you reach the counter:

- Counter add-ons average $30–$60/day, or $210–$420 for a 7-day trip

- Third-party rental car insurance costs $11–$23/day

- Most full-coverage auto policies already extend to rental cars for personal use

- All four major credit card networks offer some form of rental car coverage — but with critical limits

What Does Rental Car Insurance Actually Cover?

The confusion at the rental counter is intentional. Agents present five different “coverages” in 90 seconds — most of which you probably don’t need. According to the Insurance Information Institute’s rental car insurance guide, rental car companies are legally required to include state-minimum liability in your base contract. Everything else is optional.

Here are the four main add-ons you’ll be offered — and what each one actually does:

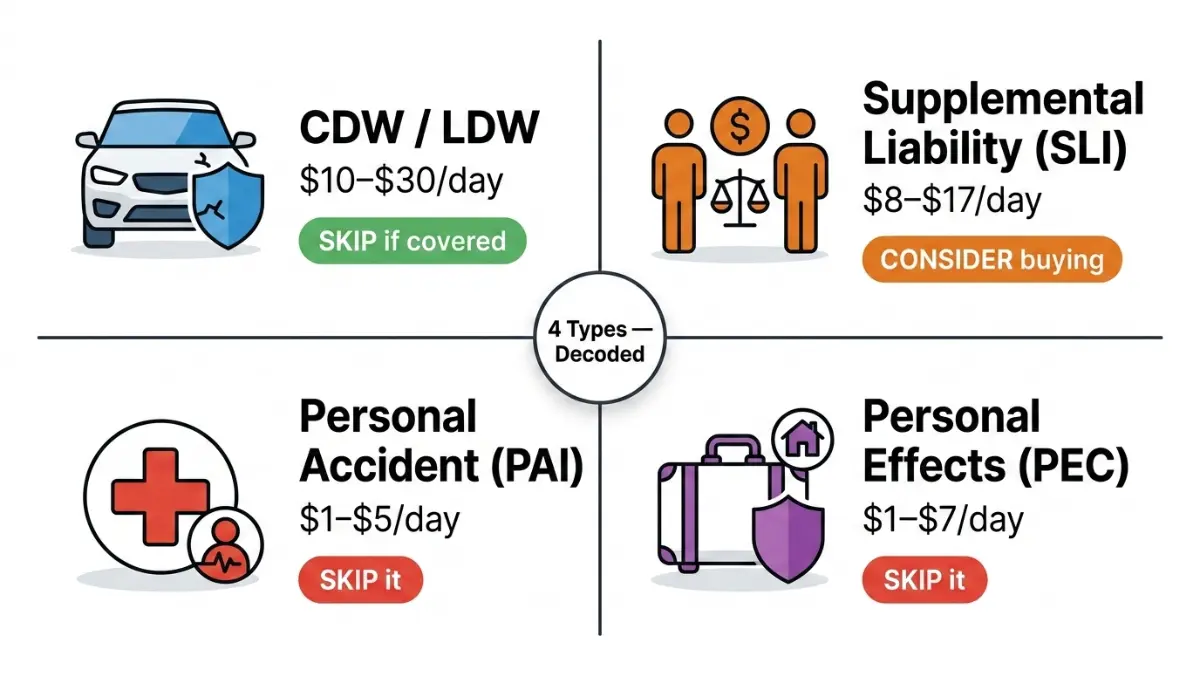

1. Collision Damage Waiver (CDW) / Loss Damage Waiver (LDW)

What it covers: Physical damage and theft of the rental car itself. Often includes loss-of-use fees and towing.

Cost: $10–$30/day

Important: CDW/LDW is not technically insurance — it’s a contractual waiver of liability.

Skip if: You have collision and comprehensive coverage on your personal auto policy, or an eligible credit card with primary rental coverage.

Buy if: You have no personal auto policy, or you’re paying with a debit card.

2. Supplemental Liability Insurance (SLI)

What it covers: Third-party bodily injury and property damage — beyond the rental company’s state-minimum liability. Coverage typically reaches $300,000–$1,000,000.

Cost: $8–$17/day

Skip if: Your personal auto liability limits are $100,000+ per person / $300,000 per accident.

Buy if: Your liability coverage is minimal or you’re driving in a high-traffic, high-risk location. This is the one add-on most worth considering.

3. Personal Accident Insurance (PAI)

What it covers: Medical bills and ambulance costs for the driver and passengers in a crash.

Cost: $1–$5/day

Skip it. If you have health insurance and your auto policy includes MedPay or PIP, PAI is pure duplication.

4. Personal Effects Coverage (PEC)

What it covers: Theft of personal items from the rental car — luggage, electronics, clothing.

Cost: $1–$7/day

Skip it. As noted by the NAIC’s auto insurance consumer resource, your existing homeowners or renters insurance typically covers belongings stolen from any vehicle. See our complete guide to renters insurance to confirm your off-premises theft protection.

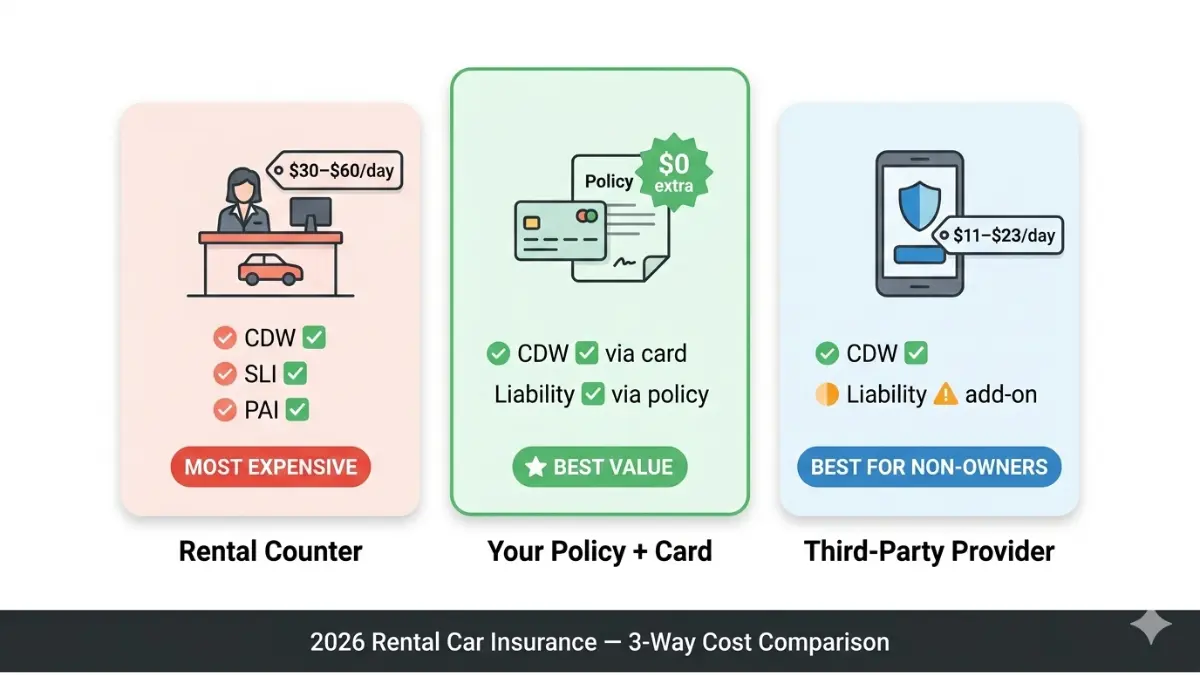

Counter Insurance vs. Credit Card vs. Third-Party — 2026 Cost Breakdown

This is the data table no competitor publishes. Use it to make your decision before you ever approach the counter.

| Coverage Source | CDW/LDW | Liability (SLI) | Medical | Daily Cost | Best For |

|---|---|---|---|---|---|

| Rental Counter | ✅ Full | ✅ Add-on ($8–17) | ✅ Add-on ($1–5) | $30–$60 | No other coverage |

| Personal Auto (Full Coverage) | ✅ Extends to rental | ✅ Your limits apply | ✅ Via PIP/MedPay | $0 extra | Most US drivers |

| Credit Card — Primary | ✅ CDW only | ❌ Not included | ❌ Not included | $0 extra | Travel-focused cards |

| Credit Card — Secondary | ⚠️ After personal policy | ❌ Not included | ❌ Not included | $0 extra | Supplement only |

| Allianz (Third-Party) | ✅ Up to $75K | ❌ | ❌ | ~$11–13/day | No personal auto |

| Bonzah (Third-Party) | ✅ | ✅ Liability add-on | ❌ | ~$11–23/day | Non-car owners |

The $400 Counter Trap — A Real Scenario

A traveler renting a mid-size car for 7 days accepts every add-on at the counter: LDW ($22/day), SLI ($14/day), PAI ($4/day), roadside ($6/day). Total extra cost: $322 for the week.

If that same traveler has a full-coverage personal auto policy and a Chase Sapphire Preferred card, their actual additional cost is $0. The counter insurance would have been completely redundant.

This is exactly why understanding rental car coverage before you travel is worth 10 minutes of your time. For comparison, see how this fits into the broader picture of affordable car insurance strategies.

Credit Card Rental Coverage: The Fine Print Traps Competitors Miss

Most articles stop at “your credit card covers you.” Here’s what they don’t tell you.

Credit card rental insurance typically does NOT cover:

- Damage to the roof, undercarriage, or tires

- Vehicles with more than 8 passenger capacity (vans, trucks, SUVs above a certain size)

- Exotic, antique, or high-value vehicles

- Rentals exceeding 15 days (domestic) or 31 days (international)

- Drivers not listed on the rental agreement

- Rentals paid with a debit card (coverage is void)

- International rentals in certain countries (varies by card)

- Accidents that violate the rental agreement (e.g., off-road driving, DUI)

Loss of Use — the hidden bill most travelers don’t expect: If the rental car is in the shop for repairs, the company charges you for every day it can’t be rented. At $40–$120/day, a 4-day repair = a $160–$480 surprise bill. Many credit cards do cover loss of use — but many do not. Check your card’s benefits guide before your trip.

Credit cards also never cover liability — meaning if you injure someone or damage their property, your card provides zero protection. That’s where your personal auto policy or SLI from the counter becomes critical. Learn more about how liability car insurance works and whether your limits are adequate.

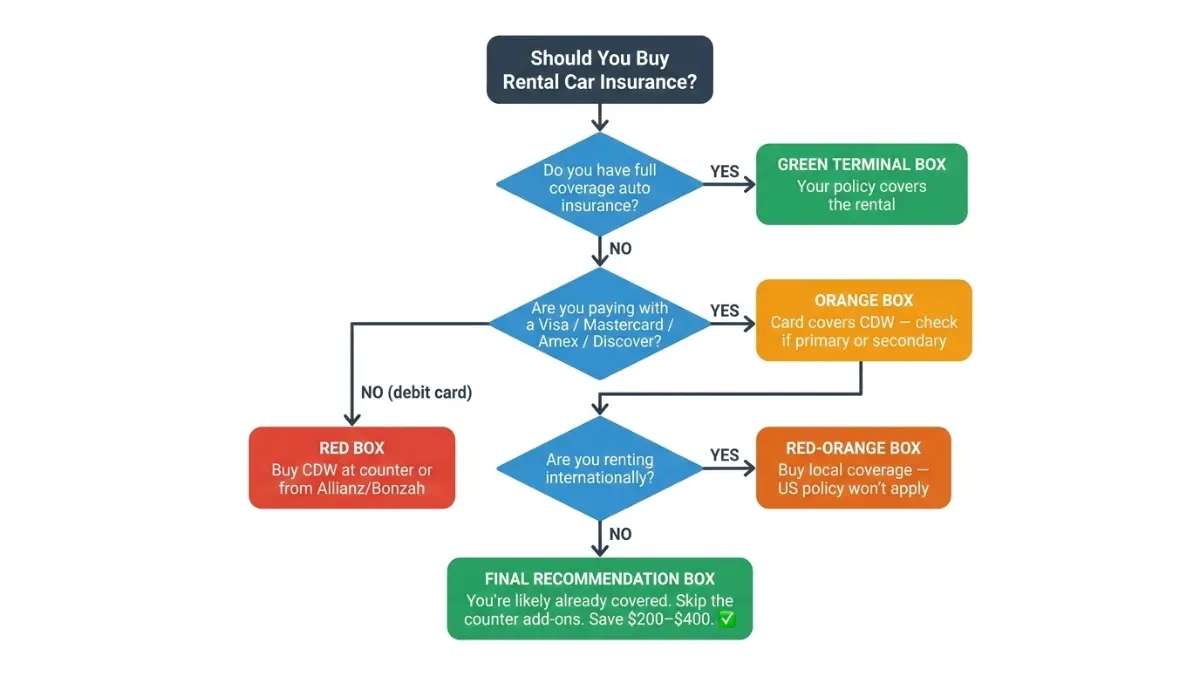

The 60-Second Decision Guide — Your Exact Situation

Answer these five questions. Your answers determine exactly what you need.

Q1: Do you have a personal auto policy with collision AND comprehensive?

→ Yes: Your rental car coverage is likely already active. Call your insurer before travel to confirm your deductible and rental terms.

→ No: You need to buy CDW from the counter or a third-party provider.

Q2: Did you pay for the rental with a Visa, Mastercard, Amex, or Discover card?

→ Yes: You likely have CDW coverage. Confirm whether it’s primary or secondary — and whether your rental type and country are covered.

→ No (debit card): You have no credit card protection. Buy CDW at the counter.

Q3: Are you renting outside the US or Canada?

→ Yes: Your US personal auto policy almost certainly does not apply. Your credit card may have country-specific exclusions. Buy local third-party coverage.

→ No: You’re likely covered by your existing policies.

Q4: Is your personal liability limit below $100,000 per person?

→ Yes: Strongly consider buying SLI at the counter ($8–$17/day). A serious accident with low limits could leave you personally exposed to six-figure claims.

Q5: Are you renting for business travel?

→ Yes: Personal auto policies often exclude business-use rentals. Check with your employer — many companies carry commercial auto coverage. Personal credit card coverage may also be void for business rentals.

Expert Takeaway: If you answered YES to Q1 and Q2, and NO to Q3–Q5, you almost certainly don’t need to buy anything at the counter. Save $210–$420 on your next 7-day trip.

Special Situations Every Competitor Ignores

Rideshare gap: If you’re driving a rental for Uber or Lyft, personal auto coverage and credit card coverage are both void. Rideshare commercial coverage is required.

Under-25 drivers: Some rental companies charge daily surcharges for drivers under 25. These fees are separate from insurance and are not covered by any policy.

EV and luxury rentals: Tesla, Rivian, and high-end SUVs often fall outside standard credit card coverage limits. Verify before renting.

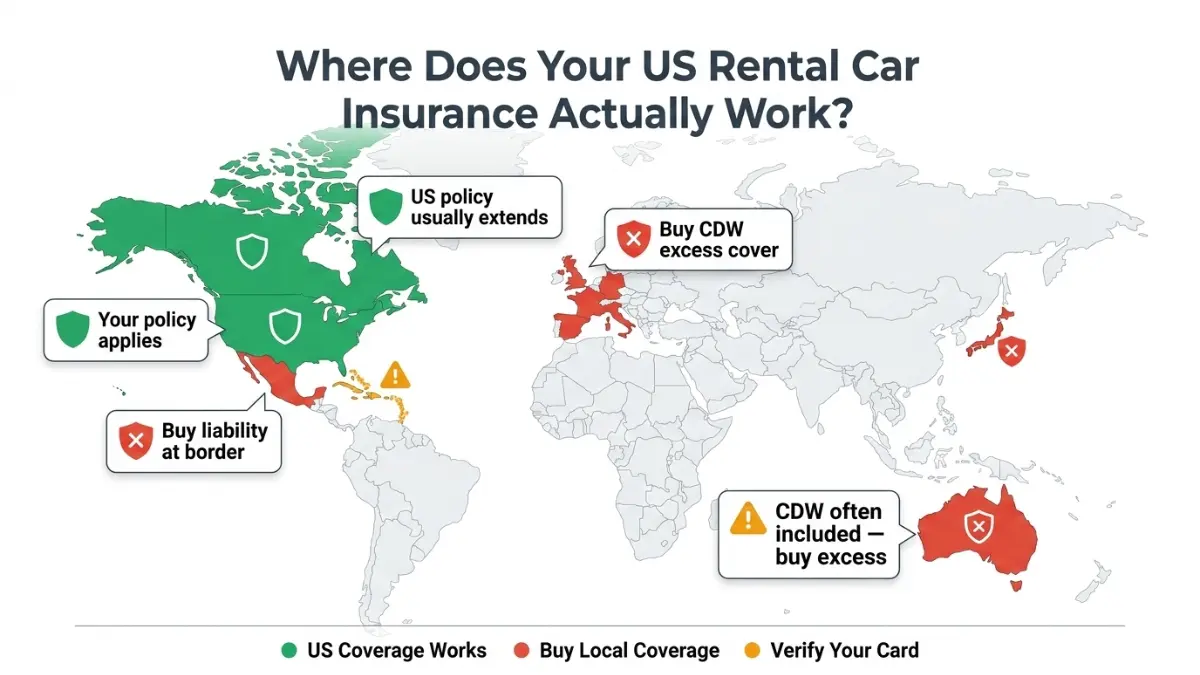

International Rental Car Insurance — The Coverage Cliff

Your US auto policy stops protecting you the moment you leave the country — in most cases. This is the most underserved topic in the rental car insurance space. Here’s exactly what applies, by country.

| Destination | US Auto Policy | Credit Card Coverage | Recommended Action |

|---|---|---|---|

| Canada | ✅ Usually | ✅ Usually | Verify before travel |

| Mexico | ❌ Almost never | ❌ Most cards exclude | Buy Mexican liability at border |

| UK / Europe | ❌ No | ⚠️ Some cards — verify | Buy CDW + excess insurance locally |

| Australia / NZ | ❌ No | ⚠️ Check your card | CDW often in base rate — buy excess cover |

| Caribbean | ❌ No | ⚠️ Very limited | Buy local SLI minimum |

Car Hire Excess Insurance — What American Travelers Don’t Know

In the UK and most of Europe, CDW (or Collision Damage Waiver) is included in the base rental rate. You’re not responsible for the full vehicle cost. But there is still an “excess” — the deductible you pay if the car is damaged — which can reach €1,500–€4,500.

Car hire excess insurance covers this gap. It costs approximately £3–£7/day and is sold by providers like RentalCover.com and AXA. It’s an entirely different product from standard US rental insurance, and no major US finance competitor covers it for an American audience.

This connects directly to the broader considerations in our travel insurance guide — international travel protection is a layered decision, and rental coverage is only one piece.

2026 Liability Minimum Updates

State minimum liability requirements are shifting. California increased its mandatory minimums to 30/60/15 on January 1, 2025 (up from 15/30/5). New Jersey has scheduled higher minimums effective in 2026.

This matters for rental car insurance because rental companies include state-minimum liability in every contract. If minimums are low in the state where you’re renting, your liability exposure gap is larger. Review your liability insurance coverage annually.

Best Third-Party Rental Car Insurance Options (2026)

If you don’t have personal auto insurance or need supplemental protection, third-party providers offer the best value. Avoid the counter markup.

| Provider | Daily Cost | CDW Limit | Liability Option | Best For |

|---|---|---|---|---|

| Allianz Travel | ~$11–13/day | Up to $75K | ❌ | Non-car owners, frequent travelers |

| Bonzah | ~$11–23/day | Up to $35K | ✅ (add-on) | Debit card users, no personal auto |

| RentalCover.com | ~$7–15/day | Varies | ❌ | International travelers |

When to use third-party:

- You don’t own a car and have no personal auto policy

- You’re paying with a debit card

- You’re renting internationally and your card has country exclusions

- You want to avoid filing a claim against your personal policy and risking a rate increase

For drivers who are uninsured or underinsured, third-party rental coverage pairs well with comprehensive car insurance — understanding both helps you identify your real coverage gaps.

Expert Verdict + 11 FAQs + Disclaimer

Expert Verdict — The Smartest Coverage Stack in 2026

For most US drivers with full coverage auto insurance and a Chase Sapphire, Capital One Venture X, or premium Amex card: Skip every counter add-on. Your real out-of-pocket cost is $0. Confirm your SLI exposure before declining.

For international travelers, debit card users, or drivers without personal auto insurance: Buy from a third-party provider before arrival. Allianz ($11–13/day) or Bonzah (with liability add-on) will cost 40–60% less than the rental counter.

The one add-on worth considering for almost everyone: SLI at $8–$17/day — especially if your personal liability limits are under $100,000.

— Expert panel reviewed, financeauthorityhub.com Finance Authority Hub

Frequently Asked Questions: Rental Car Insurance

Q1: Is rental car insurance required by law?

No. As confirmed by the NAIC’s consumer auto insurance guidance, rental companies must include state-minimum liability in the base rental contract. All additional coverage is optional.

Q2: Does my personal car insurance cover rental cars?

Usually yes, if you have full coverage (collision + comprehensive) and you’re renting for personal use — not business. Call your insurer before travel to confirm your deductible applies and to check international restrictions.

Q3: Does my credit card cover rental car damage?

Most major credit cards provide CDW coverage when you pay with that card and decline the counter’s damage waiver. But coverage is almost always secondary, and it excludes liability, medical, and many vehicle types. Check if your specific card offers primary or secondary coverage.

Q4: What is a collision damage waiver (CDW)?

A CDW is a contractual waiver — not an insurance product — that releases you from paying for damage to or theft of the rental vehicle. It’s typically the most expensive counter add-on, costing $10–$30/day. The terms can be voided by driving under the influence, using unauthorized drivers, or violating the rental agreement.

Q5: What is “loss of use” and will I owe it?

Loss of use is the fee the rental company charges for every day the damaged car cannot be rented while under repair. At $40–$120/day, a 4-day repair generates a $160–$480 bill. Many — but not all — credit cards cover this. Verify in your card’s benefits guide before your trip.

Q6: What if I don’t own a car — do I need to buy rental car insurance?

Yes. Without a personal auto policy, you have no base CDW or liability coverage. At a minimum, buy CDW + SLI from the counter, or purchase a third-party policy from Allianz or Bonzah before pickup. Also see our guide to temporary car insurance for non-owners.

Q7: Is rental car insurance worth it for international travel?

Almost always yes. Most US personal auto policies and many credit cards do not cover rentals in Mexico, Europe, Asia, or the Caribbean. Even cards with international coverage often have country-specific blacklists.

Q8: Can I buy rental car insurance without a credit card?

Yes. Third-party providers like Allianz and Bonzah sell standalone daily policies — no credit card required for eligibility. Allianz charges approximately $11–$13/day.

Q9: Does rental car insurance cover additional drivers?

Credit card coverage typically covers other drivers listed on the rental agreement. Counter insurance generally covers all authorized drivers. Always confirm before adding drivers — some policies void coverage for unlisted drivers.

Q10: What does rental car insurance NOT cover?

Regardless of source, rental car insurance almost never covers: third-party liability (credit cards), your personal medical expenses (most credit cards), personal belongings, off-road damage, DUI incidents, or unauthorized driver damage.

Q11: How much does rental car insurance cost per day in 2026?

Counter add-ons total $30–$60/day when fully stacked. Third-party providers cost $11–$23/day. Using your existing full-coverage policy and an eligible credit card costs $0 extra. Matching the right option to your situation is the core of this decision — and the difference between overpaying by $400 or paying nothing.

Related Reading From Finance Authority Hub

Building a complete picture of your insurance coverage means understanding how each policy fits together. Explore our guides to gap insurance, holiday insurance for 2026, and how to cut car insurance costs by up to 34% — all part of the same smart coverage strategy.

Disclaimer

This article is for educational and informational purposes only and does not constitute financial, insurance, or legal advice. Coverage terms, exclusions, and state requirements vary by insurer, credit card issuer, and jurisdiction. Always verify your specific coverage with your insurer, credit card provider, and state insurance department before renting a vehicle. financeauthorityhub.com is not affiliated with, endorsed by, or sponsored by any insurance company or rental car provider mentioned in this article.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.