Gap Insurance: Don’t Pay Until You Read This (2026)

Most drivers overpay for gap insurance by $600+ at the dealership. Our credentialed experts reveal exact 2026 costs, who truly needs it, and when to cancel.

In This Article

Gap insurance — also called Guaranteed Asset Protection (GAP) — covers the difference between what you still owe on your car loan and what your insurer pays if your vehicle is totaled or stolen. If you finance or lease a car in 2026, this one coverage could save you thousands of dollars you’d otherwise pay out of pocket.

What you’ll learn in this guide:

- Exactly how gap insurance works (with real numbers)

- Who genuinely needs it — and who can safely skip it

- Why dealer-sold gap insurance costs up to 10x more than your insurer charges

- The 2026 EV depreciation risk most drivers don’t know about

- When to cancel gap insurance and how to do it

- Step-by-step guide to buying it the smart way

How Gap Insurance Works — And Why Your Loan Creates a Dangerous Shortfall

The Depreciation Math That Catches Drivers Off Guard

A new car loses roughly 20% of its value within the first year of ownership, according to the Insurance Information Institute. That depreciation hits hardest in the first 12–18 months — exactly when your loan balance is still near its peak.

Standard auto insurance pays only the Actual Cash Value (ACV) of your vehicle at the time of a claim. That is the current market value, not what you paid — and not what you owe.

What “Actual Cash Value” Actually Means for You

ACV is calculated by taking the original purchase price and subtracting depreciation based on your car’s age, mileage, and condition. If your vehicle is totaled, your insurer pays ACV, not your loan payoff balance.

The dangerous gap that forms:

| Month | Car Value (ACV) | Loan Balance | Gap Owed Out-of-Pocket |

|---|---|---|---|

| Month 1 | $38,000 | $40,000 | $2,000 |

| Month 6 | $33,500 | $38,200 | $4,700 |

| Month 12 | $31,900 | $36,400 | $4,500 |

| Month 18 | $29,800 | $34,200 | $4,400 |

| Month 30 | $25,000 | $26,000 | $1,000 |

Based on a $42,000 vehicle with a 60-month loan at 7.5% APR — reflecting 2026 average auto loan rates.

Step-by-Step: What Happens When You File a Gap Claim

- Your car is totaled or stolen in a covered incident

- Your comprehensive or collision insurance pays out — capped at ACV, minus your deductible

- A shortfall remains between that payout and your remaining loan balance

- Gap insurance covers that shortfall, paying your lender directly

- You walk away with no remaining loan balance — and can move forward

What This Means For You: Without gap insurance, you could spend months making payments on a car you no longer own. The Consumer Financial Protection Bureau (CFPB) confirms that gap coverage is optional — but for financed vehicles in years one through three, it is one of the most financially protective decisions you can make.

Do You Need Gap Insurance? Answer These 5 Questions First

Not every driver needs gap insurance. Use this framework to decide quickly.

The 5-Question Decision Checklist

| Question | If YES → |

|---|---|

| Did you put less than 20% down on your vehicle? | You likely need gap insurance |

| Is your loan term 60 months or longer? | You likely need gap insurance |

| Did you roll negative equity from a previous loan into this one? | You almost certainly need it |

| Did you buy a high-depreciation vehicle (luxury, EV, sports car)? | You need it urgently |

| Are you in the first 24 months of your loan? | Gap insurance is highly recommended |

If you answered YES to 3 or more questions, gap insurance is worth carrying.

When You Can Safely Skip Gap Insurance

- You own your vehicle outright (no loan)

- Your loan balance is already below the car’s ACV

- You made a down payment of 25% or more

- You are past month 36 on a standard 60-month loan

- Your vehicle holds value unusually well (certain trucks, SUVs)

🚨 2026 Alert: The EV Depreciation Risk Nobody Is Talking About

Electric vehicles depreciate 25–40% faster than comparable gas-powered cars, largely due to rapid battery technology improvements making older EV models less desirable. A $55,000 EV can lose $18,000–$22,000 in value within 18 months.

- Tesla Model 3 depreciated ~27% in Year 1 (2024–2025 data)

- Rivian R1T lost approximately 31% in Year 1

- Hyundai Ioniq 6 dropped ~22% in its first 12 months

What This Means For EV Owners: If you financed a new electric vehicle with less than 20% down in 2024 or 2025, your loan balance almost certainly exceeds your car’s current ACV. Gap insurance for EVs is not optional — it is essential. For broader vehicle financing guidance, explore our affordable car insurance guide and comprehensive car insurance overview.

Gap Insurance Cost in 2026 — Why Most Drivers Overpay by $600

This is the section dealers hope you never read.

What Gap Insurance Actually Costs Through Your Insurer

Adding gap insurance to your existing auto policy is inexpensive. Most major insurers charge $20–$60 per year — typically just 5–7% added to your existing collision and comprehensive premium.

2026 Provider Cost Comparison:

| Insurer | Estimated Monthly Cost | Annual Cost | Notes |

|---|---|---|---|

| Erie Insurance | $3–$5/month | ~$36–$60 | Includes new/better car replacement in some states |

| Nationwide | $2–$4/month | ~$24–$48 | Gap Plus: covers up to 120% of ACV |

| Progressive | $3–$5/month | ~$36–$60 | Capped at 25% above ACV |

| State Farm | $3–$5/month | ~$36–$60 | Payoff Protector via State Farm Bank loans |

| Allstate | $3–$6/month | ~$36–$72 | Waives covered losses up to $50,000 |

| USAA | $2–$4/month | ~$24–$48 | Best option for military and veterans |

Rates vary by state, vehicle type, and loan amount. Always verify with your insurer directly.

What Dealerships Charge — The Markup You Must Know

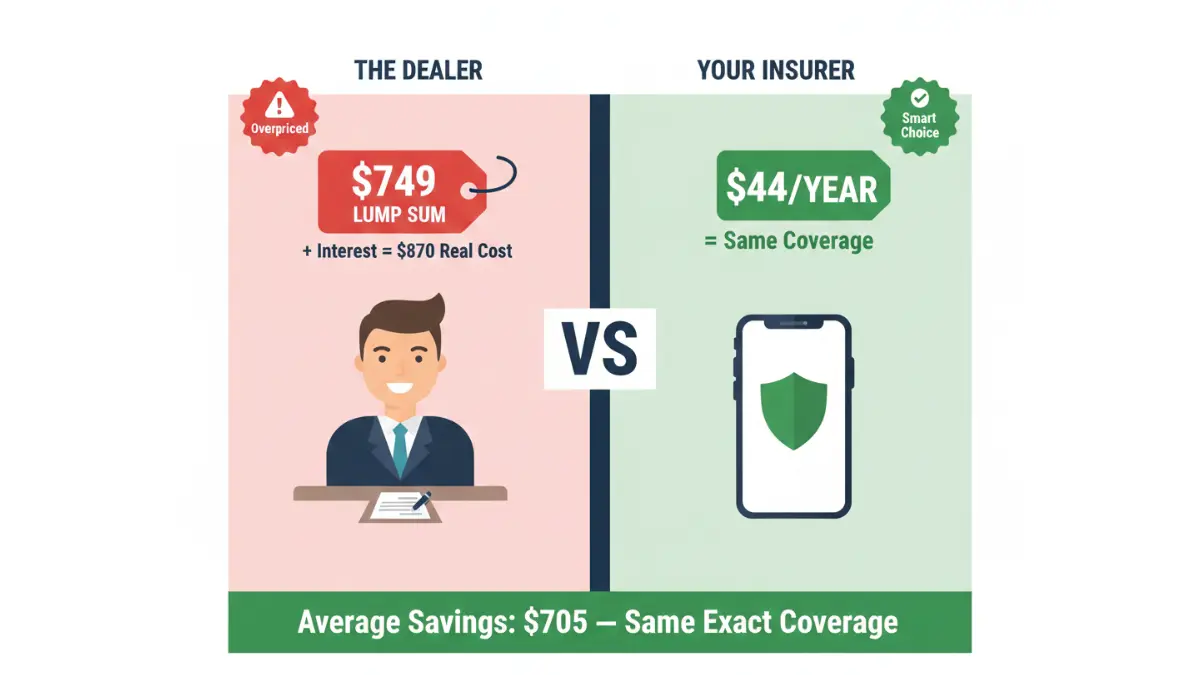

Dealers routinely sell gap insurance as a lump-sum add-on rolled into your financing. The typical dealer charge: $400–$900 upfront, which then accrues interest over your loan term.

At a 7.5% APR over 60 months, a $700 dealer gap product actually costs you closer to $870 in real dollars — for the exact same coverage your insurer provides for $25/year.

Real-World Case Study — Marcus, 34, Nashville, TN: Marcus financed a 2024 Toyota Camry for $34,000. At the dealer’s F&I office, he was quoted $749 for gap insurance rolled into his loan. After reading this guide, he called his insurer instead. He added gap coverage for $44/year — saving $705. Over his 5-year loan, that $705 saved him an additional $78 in interest. Total savings: $783.

The CFPB explicitly warns that you are never required to purchase gap insurance from a dealer to qualify for a car loan. Always shop your insurer first.

How to Get the Best Gap Insurance Rate in 3 Steps

- Call or log in to your current insurer first — ask specifically for “gap coverage” or “loan/lease payoff coverage”

- Compare at least two other insurers — rates vary significantly by company and state

- Confirm coverage terms — check maximum payout caps, whether your deductible is covered, and eligibility age of vehicle

For managing your total debt picture across auto loans and other obligations, our debt consolidation guide and APR vs. interest rate explainer are essential reads before signing any financing contract.

When to Cancel Gap Insurance — The Exact Tipping Point

Keeping gap insurance past its useful period is money wasted. Here is precisely when to cancel.

The Break-Even Rule

Cancel gap insurance when your loan balance drops to or below your car’s ACV.

You can check your car’s approximate ACV using free tools like Kelley Blue Book or Edmunds. Check your remaining loan balance on your lender’s portal or most recent statement.

Practical Milestones for a 60-Month Loan:

| Loan Progress | Typical ACV vs. Balance | Action |

|---|---|---|

| Months 1–18 | Loan exceeds ACV by $3,000–$6,000+ | Keep gap insurance |

| Months 19–30 | Loan exceeds ACV by $1,000–$3,000 | Keep gap insurance — still exposed |

| Months 31–42 | ACV approaches loan balance | Review monthly |

| Months 43–60 | ACV equals or exceeds loan balance | Cancel gap insurance |

Timeline varies significantly based on make, model, depreciation rate, and loan terms.

How to Cancel Gap Insurance

- Through your insurer: Call or log into your account and remove the endorsement — effective at your next billing cycle

- Dealer-sold gap: Contact the gap provider directly (not the dealer). You are entitled to a pro-rated refund under most state laws for unused coverage

- Financed into your loan: Request a refund from the gap provider, then apply the refund toward your principal balance

What This Means For You: Canceling at the right time and applying your refund to your principal is a double win — you eliminate a premium you no longer need AND reduce the balance on which you pay interest.

Gap Insurance vs. Alternative Coverages

| Coverage Type | What It Covers | Best For |

|---|---|---|

| Gap Insurance | Loan/lease balance minus ACV | Financed or leased vehicles, first 3 years |

| New Car Replacement | Full replacement with same make/model | Buyers who want a brand-new replacement, not loan payoff |

| Loan/Lease Payoff | Similar to gap, often capped at 25% of ACV | Lower-risk situations with smaller gaps |

| Better Car Replacement | Replaces with a newer/lower-mileage model | Drivers who want an upgrade after a total loss |

For broader insurance cost strategies across multiple policy types, see our insurance cost reduction guide and our detailed breakdown of liability car insurance.

How to Buy Gap Insurance in 2026 — The Smartest Path

Step-by-Step: Adding Gap Coverage to Your Existing Policy

- Log in to your insurer’s app or website, or call their customer service line

- Request to add “gap coverage” or “loan/lease payoff coverage” to your existing auto policy — you must already have comprehensive and collision coverage

- Confirm your vehicle is eligible — most insurers require the car to be fewer than 3 years old with you as the original owner

- Review the coverage cap — some insurers cap gap payouts at 25% of ACV; others (like Nationwide) cover up to 120% of ACV

- Ask about the deductible — some policies cover your collision deductible as part of the gap payout; others do not

Questions to Ask Your Insurer Before Buying

- What is the maximum gap payout limit on this policy?

- Does this cover my comprehensive/collision deductible?

- What vehicles and loan types qualify?

- Is there a maximum vehicle age or mileage restriction?

- How do I file a gap claim if my car is totaled?

- What is the cancellation and refund policy?

What to Watch Out For at the Dealership

Dealers often present gap insurance quickly during the F&I (Finance and Insurance) signing process. Key red flags:

- Being told gap insurance is required to get financing (it is not — the CFPB confirms this)

- Gap rolled into your loan without your explicit agreement

- No disclosure of the total cost including interest over the loan term

- No mention that your own insurer likely offers it for far less

The Insurance Information Institute’s guide to gap insurance reinforces that shopping around before committing to dealer-offered products is always in your financial interest.

For related cost-saving strategies across your vehicle and broader financial profile, explore our car insurance cost reduction guide and liability insurance overview.

FAQs — 11 Most-Asked Questions About Gap Insurance

1. What does gap insurance cover?

Gap insurance covers the difference between your vehicle’s Actual Cash Value and your remaining loan or lease balance if the car is totaled or stolen. It does not cover repairs, mechanical issues, or missed payments.

2. How much does gap insurance cost per month?

Through your insurer, gap insurance typically costs $2–$6 per month ($20–$60/year). Through a dealer, you may pay $400–$900 upfront — often rolled into your loan with added interest.

3. Is gap insurance worth it?

Yes — if you financed with less than 20% down, have a loan term of 60+ months, or are driving a high-depreciation vehicle (especially an EV). The cost is minimal versus the potential thousands you could owe after a total loss.

4. Does gap insurance cover a totaled car?

Yes. A totaled vehicle is the primary use case for gap insurance. It pays the difference between your insurer’s ACV payout and your remaining loan balance.

5. Can I get gap insurance on a used car?

It depends on the insurer. Many require the vehicle to be fewer than 3 model years old and have you as the original owner. Some providers do offer it for used vehicles — confirm with your insurer directly.

6. Does gap insurance cover theft?

Yes. If your vehicle is stolen and not recovered, gap insurance pays the difference between the ACV payout from your comprehensive coverage and your outstanding loan balance.

7. How long do I need gap insurance?

Typically for the first 2–3 years of a loan, or until your loan balance falls below your vehicle’s ACV — whichever comes first. Use the table in Section 4 as your reference.

8. Can I cancel gap insurance at any time?

Yes. If purchased through your insurer, you can cancel at any renewal or mid-policy. If dealer-sold, you are entitled to a pro-rated refund for unused coverage under most state laws.

9. Does gap insurance cover my deductible?

It varies by insurer and policy. Some gap products (such as Nationwide’s Gap Plus) include deductible reimbursement. Others do not. Always confirm this before purchasing.

10. Is dealer gap insurance the same as insurer gap insurance?

Functionally similar — but not the same price. Dealer gap typically costs 10–15x more when accounting for the lump sum and added loan interest. Your insurer’s version provides equivalent protection at a fraction of the cost.

11. Do electric vehicles need gap insurance? Absolutely.

EVs depreciate 25–40% faster than gas vehicles in 2026, creating larger gaps between loan balance and ACV sooner. If you financed an EV, gap insurance is strongly recommended for the first 3–4 years.

⚠️ Disclaimer: This article is for educational and informational purposes only and does not constitute financial, legal, or insurance advice. Gap insurance costs, coverage terms, provider availability, and eligibility requirements vary by state, insurer, and individual circumstances. Always consult a licensed insurance professional before making coverage decisions. Refund eligibility for cancellation varies by state law and policy terms.

Reviewed and fact-checked by the editorial team at financeauthorityhub.com — your trusted source for verified, expert-backed financial guidance.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.