Comprehensive Car Insurance: Is It Worth It in 2026?

Is comprehensive car insurance worth it in 2026? See real costs, the 10% Rule, what’s covered vs. not, and exactly when to keep or drop your coverage.

In This Article

Comprehensive car insurance covers non-collision damage to your vehicle — including theft, hail, floods, fire, vandalism, and animal strikes. It costs an average of $134–$421 per year as a standalone add-on. In 2026, with full coverage averaging $2,496/year nationally, comprehensive coverage is worth it if your car’s value exceeds 10x your annual premium. Here’s exactly how to decide — faster and clearer than any other guide online.

What Is Comprehensive Car Insurance?

The 2026 Definition — Plain English

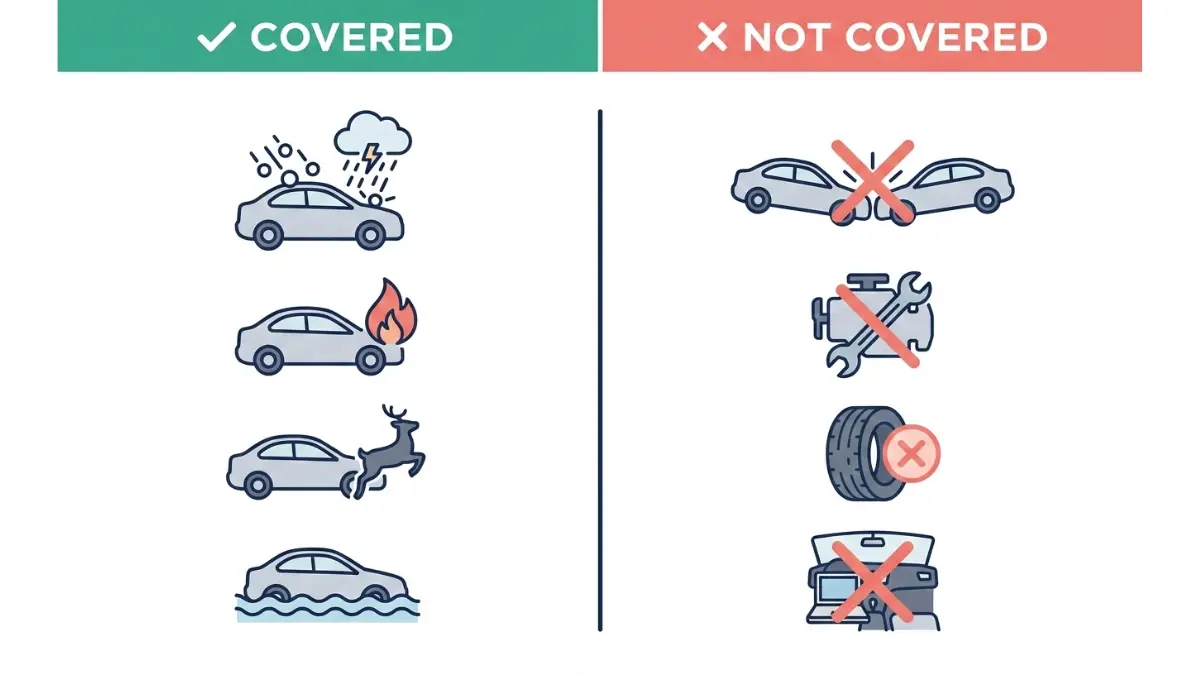

Comprehensive car insurance is the coverage that protects your vehicle from damage that has nothing to do with hitting another car. Think of it as your shield against the things you can’t control — hailstorms, floods, deer, thieves, and fires.

According to the NAIC Consumer’s Guide to Auto Insurance, comprehensive coverage pays for damage to your vehicle from “fire, severe weather, vandalism, floods and theft” — as well as broken glass and windshield damage. It does not cover mechanical breakdowns or normal wear and tear.

What Comprehensive Car Insurance Covers vs. What It Doesn’t

| ✅ Covered | ❌ Not Covered |

|---|---|

| Theft of your vehicle | Collision with another car |

| Hail and storm damage | Mechanical breakdown |

| Flood and water damage | Normal wear and tear |

| Fire and explosion | Personal belongings inside the car |

| Vandalism and graffiti | Intentional damage by you |

| Deer or animal strikes | Rideshare accidents (without add-on) |

| Falling objects (tree limbs) | Engine failure |

| Earthquake damage | Tire blowouts (no road hazard) |

| Civil unrest / riots | Custom parts (unless separately insured) |

Key takeaway: Comprehensive only pays up to your vehicle’s Actual Cash Value (ACV) — not its replacement cost. If your car is worth $12,000 and hail causes $9,000 in damage, your insurer pays $9,000 minus your deductible.

Comprehensive vs. Collision vs. Full Coverage

This is the most misunderstood area — and where competitors fall short.

| Coverage | What It Pays For | Required By Law? | Required by Lender? |

|---|---|---|---|

| Comprehensive | Non-collision damage | No | Yes (if financed/leased) |

| Collision | Crash damage to your car | No | Yes (if financed/leased) |

| Liability | Damage you cause to others | Yes (most states) | Yes |

| “Full Coverage” | All three combined | No | Yes (if financed/leased) |

Important: “Full coverage” is not a legal term. As the NAIC Shopping Tool confirms — “there is no such thing as full coverage.” It simply refers to combining liability, collision, and comprehensive together.

Is Comprehensive Car Insurance Required?

No state requires comprehensive coverage by law. However, if you finance or lease your car, your lender will require both comprehensive and collision. This is their way of protecting their financial interest in your vehicle.

Once you pay off your car, the choice is entirely yours — and that’s exactly when the 10% Rule (covered in Section 3) becomes critical.

How Much Does Comprehensive Car Insurance Cost in 2026?

Real 2026 National Cost Data

Auto insurance rates skyrocketed 50%+ between 2020 and 2025. The good news: ValuePenguin’s 2026 State of Auto Insurance report confirms that 2026 increases are slowing dramatically — just 0.67% nationally.

Here’s what you’re actually paying in 2026:

| Coverage Type | Average Annual Cost (2026) |

|---|---|

| Comprehensive only (standalone add-on) | $134–$421/year |

| Collision only | ~$473/year |

| Full coverage (comprehensive + collision + liability) | $2,496–$2,513/year |

| Minimum liability only | $618–$912/year |

Sources: ValuePenguin, Insurance.com, III.org, 2026 data

At just $134–$421/year for comprehensive alone, it’s one of the most cost-effective add-ons available in personal auto insurance.

Comprehensive Car Insurance Cost by Age (2026)

Your age significantly impacts your premium. Here are the general ranges for full coverage including comprehensive:

| Age | Avg. Monthly Full Coverage |

|---|---|

| 20 | $397/month |

| 30 | ~$189/month |

| 40 | ~$178/month |

| 55 | ~$177/month |

| 70 | ~$190/month |

Source: NerdWallet February 2026 rates analysis

Teen drivers pay the steepest premiums — with rates as high as $6,094/year for full coverage at age 16. Rates generally bottom out in your 50s and then creep back up.

Most Expensive vs. Cheapest States for Full Coverage (2026)

Where you live matters enormously. Flood plains, hail corridors, and high-theft metro areas directly raise your comprehensive premium.

| Most Expensive States | Avg. Annual Full Coverage | Cheapest States | Avg. Annual Full Coverage |

|---|---|---|---|

| Nevada | $300+/month | Vermont | $1,299/year |

| Louisiana | $300+/month | Maine | $1,500/year |

| Florida | $4,210/year | Wyoming | ~$1,332/year |

| Connecticut | $314/month | Idaho | $1,473/year |

| Maryland | $4,224/year | New Hampshire | $1,368/year |

Florida’s average of $4,210/year is 57% above the national average — driven heavily by hurricane and flood claims that fall squarely under comprehensive coverage.

What Raises Your Comprehensive Premium?

- ZIP code — flood zones, wildfire areas, high-theft cities

- Vehicle value — higher ACV = higher payout potential = higher premium

- Deductible level — lower deductible = higher premium

- Claims history — prior comprehensive claims can raise future rates

- Credit score — insurers in most states use credit-based insurance scores

- Car model — vehicles frequently stolen (Honda Civic, Kia, Hyundai) cost more to insure comprehensively

What This Means For You: If you drive a high-theft vehicle like a Kia or Hyundai — which have made national headlines for theft vulnerabilities — your comprehensive premium may be above average regardless of where you live. This makes the coverage more valuable, not less.

For more ways to cut your car insurance costs by up to 34%, see our dedicated cost-reduction guide.

Is Comprehensive Car Insurance Worth It? The Expert Decision Framework

The Answer Most Guides Won’t Give You Upfront

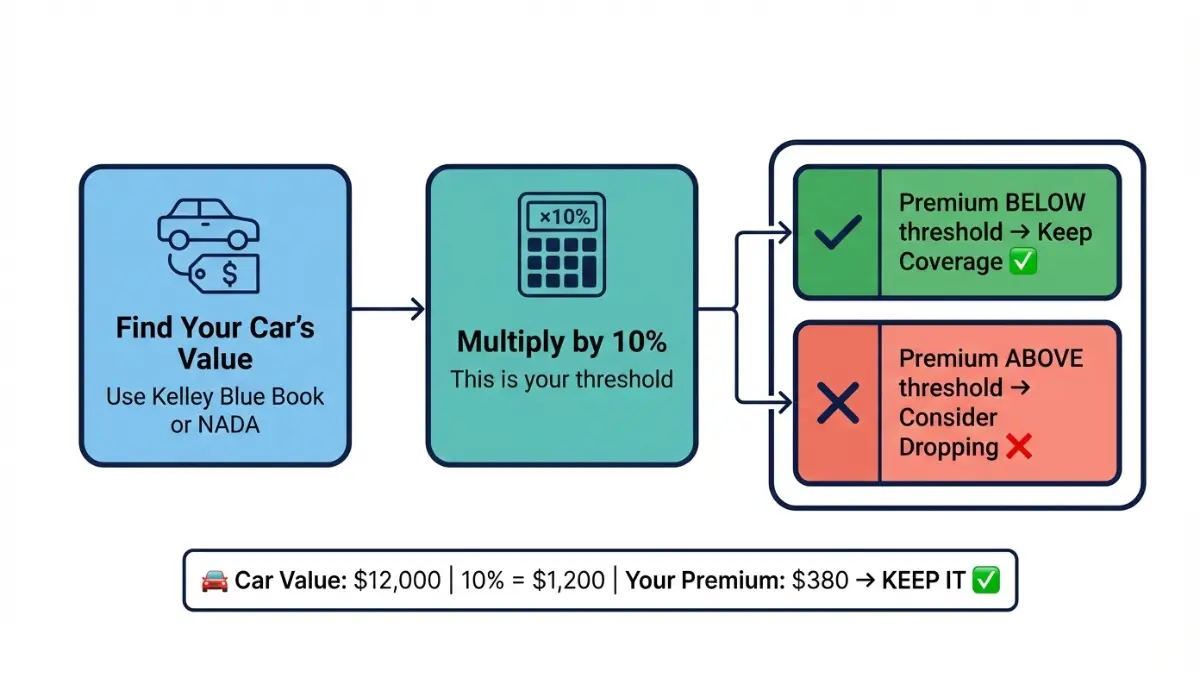

Comprehensive car insurance is worth it if your annual premium is less than 10% of your vehicle’s current market value. This is called the 10% Rule — and it’s the only framework you need.

Most competitors bury this. We’re putting it front and center.

The 10% Rule — With Real Math

Step 1: Find your car’s current Actual Cash Value (use Kelley Blue Book or NADA). Step 2: Multiply that value by 10%. Step 3: Compare to your annual comprehensive premium.

| Scenario | Car Value | Annual Comprehensive Cost | 10% Threshold | Decision |

|---|---|---|---|---|

| New car owner | $28,000 | $421 | $2,800 | ✅ Keep it |

| Mid-age car | $12,000 | $380 | $1,200 | ✅ Keep it |

| Older paid-off car | $3,500 | $350 | $350 | ⚠️ Borderline |

| High-mileage clunker | $2,000 | $300 | $200 | ❌ Consider dropping |

Source: MoneyGeek 10% Rule framework, verified 2026

Real example: Sarah drives a 2013 Honda Civic worth $7,000. Her comprehensive premium is $290/year. Since $290 < $700 (10% of $7,000), she should keep the coverage.

When You’re REQUIRED to Keep Comprehensive Coverage

You have no choice in these situations:

- Financed vehicle — your lender requires it until the loan is paid off

- Leased vehicle — your leasing company mandates it for the full lease term

- GAP insurance policies — most require active comprehensive coverage to function

If you have a car loan and drop comprehensive, your lender can force-place their own insurance on your vehicle — typically at 2–3x the normal cost.

When You Should Drop Comprehensive Coverage

Consider dropping it if all of these apply:

- ✅ Your car is fully paid off

- ✅ Your car’s ACV is under $4,000

- ✅ Your comprehensive premium exceeds 10% of your car’s value

- ✅ You have enough savings to replace or repair your car without hardship

- ✅ You live in a low-risk area (low theft, low flood/hail risk)

The 2026 Climate Risk Factor — Why Dropping Coverage Is Riskier Than Ever

This is the angle none of the top competitors are covering in 2026.

Severe weather events — hailstorms, flooding, wildfires — are directly covered by comprehensive insurance. And they’re becoming more frequent:

- Hail damage claims in the Midwest and Great Plains are rising annually

- Florida, Texas, Louisiana, and coastal states face escalating hurricane and flood risk

- California wildfire zones continue to expand each year

If you live in a FEMA-designated high-risk flood zone or a state prone to hail (Texas, Kansas, Nebraska, Oklahoma, Colorado), the value of comprehensive coverage increases substantially — even for older vehicles.

For a broader look at how insurance decisions connect to your overall financial picture, explore our complete insurance cost-cutting guide or review our detailed homeowners insurance guide to see how bundling can cut comprehensive premiums further.

How to Choose the Right Comprehensive Deductible

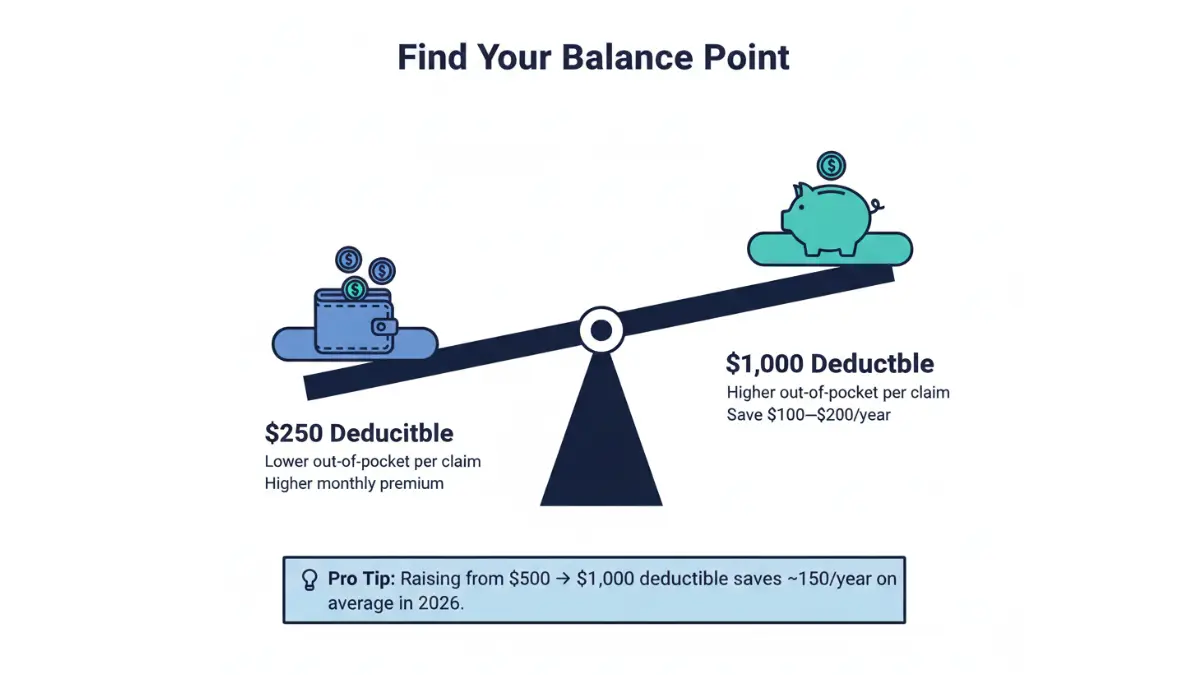

What Is a Deductible in Comprehensive Insurance?

Your deductible is the amount you pay out-of-pocket before your insurer covers the rest of a claim. If a hailstorm causes $2,000 in damage and your deductible is $500, you pay $500 and your insurer pays $1,500.

Comprehensive deductibles are separate from collision deductibles — you can choose different amounts for each.

The Deductible Breakeven Analysis

Most drivers choose between $500 and $1,000. Here’s how the math breaks down:

| Deductible | Annual Premium Impact | Break-Even Claims Frequency |

|---|---|---|

| $250 | Highest premium | 1 claim every 5–7 years |

| $500 | Mid-range | 1 claim every 7–10 years |

| $1,000 | Lowest premium | 1 claim every 10–15 years |

Bottom line: Raising your deductible from $500 to $1,000 typically saves $100–$200/year on your comprehensive premium. If you go more than 5–7 years without a comprehensive claim (statistically likely), you come out ahead.

Pro Tip: Stacking Deductible Savings With Discounts

Raising your deductible while simultaneously bundling your auto and homeowners insurance can reduce your total comprehensive premium by 15–25%. For example:

- Raise deductible: saves ~$150/year

- Bundle home + auto: saves ~$200–$400/year

- Good driver discount: saves ~$50–$150/year

Total potential savings: $400–$700/year — without changing your actual coverage.

If you’re managing significant monthly expenses, our debt consolidation calculator can help you see how insurance savings fit into your broader budget strategy.

Best Companies for Comprehensive Coverage in 2026

Not All Comprehensive Coverage Is Equal

The cheapest comprehensive premium isn’t always the best comprehensive coverage. What separates top carriers is what they include automatically — and what they make you pay extra for.

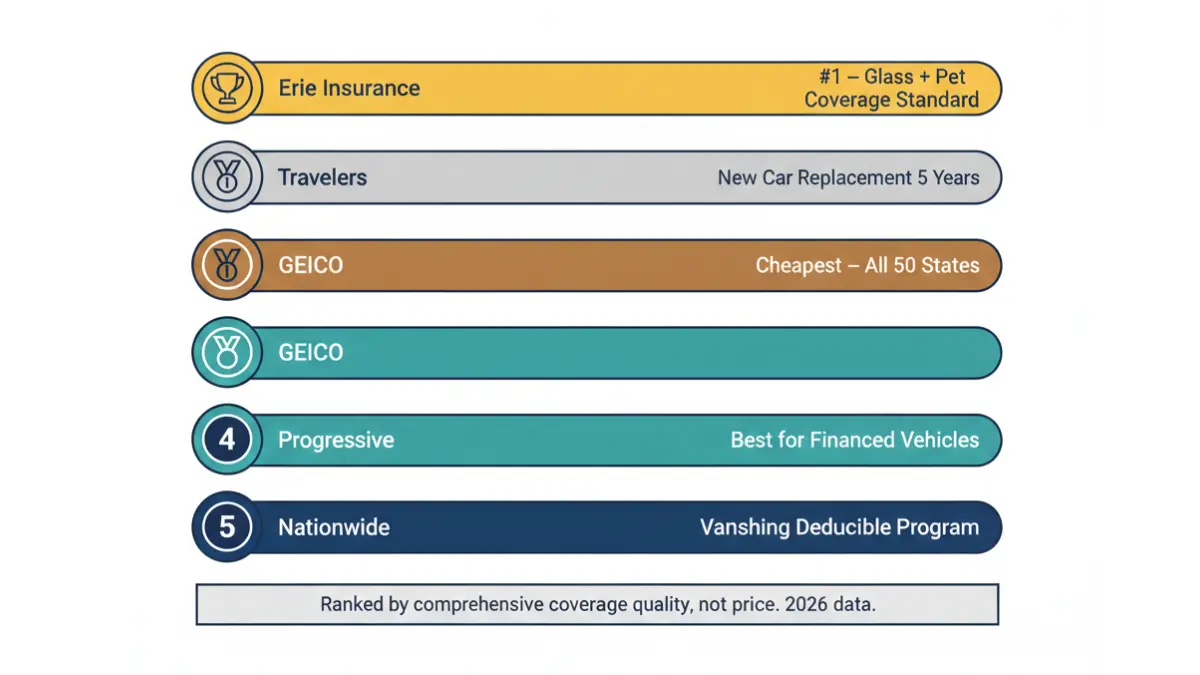

Top 5 Companies for Comprehensive Coverage (2026)

| Company | Comprehensive Standout Feature | Avg. Annual Full Coverage | Best For |

|---|---|---|---|

| Erie | Pet injury + glass repair standard; Rate Lock | Below avg (~$1,800) | Midwest/East Coast drivers |

| Travelers | New car replacement for 5 years; accident forgiveness | $2,103/year | New car owners |

| GEICO | Cheapest rates in 50 states; mechanical breakdown option | $1,867/year | Budget-focused drivers |

| Progressive | GAP coverage available; animal strikes + rental reimbursement | Above avg | Drivers with loans |

| Nationwide | Vanishing deductible program reduces out-of-pocket costs | Below avg | Long-term policyholders |

What to Specifically Look for in Comprehensive Coverage

Beyond price, ask these questions before choosing a carrier:

- Windshield repair: Does the carrier offer zero-deductible glass repair? Erie and many regional carriers do.

- Rental reimbursement: If your car is being repaired after a covered claim, will you have a rental car paid for?

- Pet coverage: Progressive includes coverage for pet injuries in an accident. Erie includes it in comprehensive policies.

- New car replacement: Travelers replaces your totaled new car with a new model — not a depreciated payout — for the first 5 years.

- J.D. Power Claims Satisfaction: Erie ranked #1 in J.D. Power’s 2025 U.S. Auto Claims Satisfaction Study in multiple regions.

How to Get the Best Comprehensive Quote in 3 Steps

Step 1: Get your car’s current ACV from Kelley Blue Book or NADA. Step 2: Apply the 10% Rule (Section 3) to confirm comprehensive is worth keeping. Step 3: Compare at least 3 quotes at the same deductible level — $500 is the standard benchmark.

Important: Always compare quotes with identical deductible amounts. Mixing a $250 deductible quote from one company against a $1,000 deductible quote from another will give you a false picture of savings.

If you’re considering a temporary policy — for example, while between cars — our guide to temporary car insurance and its cheapest options is worth reading before you commit to a full annual policy.

FAQs — Comprehensive Car Insurance (2026)

Q1. Does comprehensive car insurance cover hitting a deer?

Yes. Animal strikes are specifically covered under comprehensive — not collision. Whether it’s a deer, elk, or dog, the claim falls under your comprehensive deductible, not collision.

Q2. Does comprehensive cover a cracked windshield?

Yes. Windshield and glass damage are covered under comprehensive. Some carriers — including Erie and Safelite-partnered insurers — offer zero-deductible glass repair on windshield-only claims.

Q3. Is comprehensive the same as full coverage?

No. Full coverage is a combination of comprehensive + collision + liability. Comprehensive alone only covers non-collision events. You can purchase comprehensive without collision, though lenders rarely allow it.

Q4. Does comprehensive car insurance cover flood damage?

Yes. Flood, hurricane water damage, and storm surge are all covered under comprehensive. This makes it especially critical for drivers in Florida, Texas, Louisiana, and other coastal or flood-prone states.

Q5. Will filing a comprehensive claim raise my rates?

Usually not significantly. Comprehensive claims are generally non-fault events (weather, theft, vandalism), so most insurers don’t penalize you the same way they would for a collision claim. Always confirm with your specific carrier.

Q6. Can I get comprehensive without collision?

Yes — if your car is paid off and you own it outright. However, lenders and leasing companies require both. Buying comprehensive without collision is sometimes useful for older vehicles that have high theft risk but low market value.

Q7. Does comprehensive car insurance cover vandalism?

Yes. Keyed paint, broken windows, slashed tires (from malicious acts), and graffiti are all covered. File a police report before making a claim — most insurers require one for vandalism.

Q8. What is the average comprehensive car insurance cost per month?

Comprehensive as a standalone add-on costs approximately $11–$35/month ($134–$421/year) in 2026. It’s one of the most affordable forms of vehicle protection relative to the risk it covers. For general insurance savings strategies, explore our cheap insurance guide.

Q9. Does comprehensive cover my belongings inside the car?

No. Personal property inside your vehicle — laptop, phone, luggage — is not covered by comprehensive auto insurance. Those items may be covered under your renters insurance or homeowners insurance policy instead.

Q10. Does comprehensive car insurance apply to natural disasters?

Yes. Hail, tornadoes, hurricanes, floods, fires, and earthquakes all qualify as comprehensive claims. This is particularly important in 2026 given increasing climate volatility across the US.

Q11. When exactly should I drop comprehensive insurance?

Drop it when your annual premium exceeds 10% of your car’s current market value AND you have sufficient emergency savings to replace or repair the vehicle. Run the 10% Rule calculation from Section 3 before making this decision. For the full picture on managing your insurance costs alongside broader financial goals, see our complete insurance overview.

Expert Consensus

The NAIC — the primary US insurance regulatory body — advises consumers to always “weigh the value of the car and the cost to replace or repair it against what you would save in premium costs” before dropping comprehensive coverage. That principle, combined with the 10% Rule and the 2026 climate risk factors outlined above, gives you a complete decision framework no other guide online currently offers in one place.

📌 Disclaimer: This article is for educational and informational purposes only. It does not constitute financial, legal, or insurance advice. Auto insurance coverage, costs, and requirements vary by state, insurer, vehicle type, and individual circumstances. Always consult a licensed insurance professional before making coverage decisions. Data cited reflects publicly available 2026 insurance industry rates and may not reflect individual quotes.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.