Liability Insurance: What It Covers & Who Needs It

Liability insurance covers others — not you. Learn all 7 types, 2026 cost ranges, coverage gaps, and why most Americans need higher limits today.

In This Article

Quick Answer: Liability insurance pays for injuries or property damage you cause to others — it does NOT cover your own losses. There are 7 major types, costs range from $39 to $100+ per month depending on coverage type, and 2026 data shows most Americans are significantly underinsured due to rising nuclear verdicts and social inflation.

What Is Liability Insurance? (And Why Most People Have the Wrong Amount in 2026)

Liability insurance is third-party coverage — it pays the person on the other side of the claim, not you. If you cause a car accident, injure someone at your home, or make a costly professional error, your liability policy steps in to cover their medical bills, property repairs, and legal costs up to your policy limit.

That last part — “up to your policy limit” — is the number every American needs to revisit in 2026.

The 2026 Reality Check

The global liability insurance market was valued at $309.49 billion in 2025 and is projected to reach $524.66 billion by 2034. Demand is surging for one critical reason: lawsuits are getting bigger, faster.

According to the National Association of Insurance Commissioners (NAIC), social inflation — the rise in liability claims driven by nuclear verdicts and third-party litigation funding — is now the dominant force reshaping coverage needs. Nuclear verdicts (jury awards exceeding $10 million) rose 52% in 2024 alone, according to Aon’s 2026 P&C Outlook.

What this means for you: If your coverage limits were set in 2020 or 2021, they may no longer be adequate. Review them now.

Claims-Made vs. Occurrence Policies — Know the Difference

Before buying any liability policy, understand which type you’re purchasing:

| Policy Type | How It Works | Best For |

|---|---|---|

| Claims-Made | Covers claims filed while the policy is active | Professionals (doctors, lawyers, consultants) |

| Occurrence | Covers incidents that happened during the policy period, even if claimed later | General liability, auto liability |

Key takeaway: If you cancel a claims-made policy, you lose coverage for past work unless you add “tail coverage.” Most professionals are unaware of this gap until it’s too late.

7 Types of Liability Insurance — Which One Do You Actually Need?

Most competitors cover 4–5 types shallowly or focus on only one. Here is your complete 2026 guide to all 7 types, including average costs, who needs them, and what they do NOT cover.

1. General Liability Insurance

General liability insurance (also called commercial general liability or CGL) is the foundation of business protection in the US. It covers:

- Bodily injury to a third party on your business premises

- Property damage your business causes to someone else’s property

- Advertising injury — libel, slander, copyright infringement in your marketing

2026 average cost: $42–$85/month for small businesses; median $45/month or $500/year (Insureon data).

What it does NOT cover: Employee injuries (that’s workers’ comp), your own property damage, professional errors, or cyber incidents.

Expert Insight: Every business — from freelancers to retail stores — should carry at least $1M per occurrence / $2M aggregate in general liability coverage. This has become the contractual standard required by most landlords, clients, and vendors.

If you’re evaluating your overall financial protection, explore our complete insurance guide to see how liability fits into your broader risk strategy.

2. Auto Liability Insurance

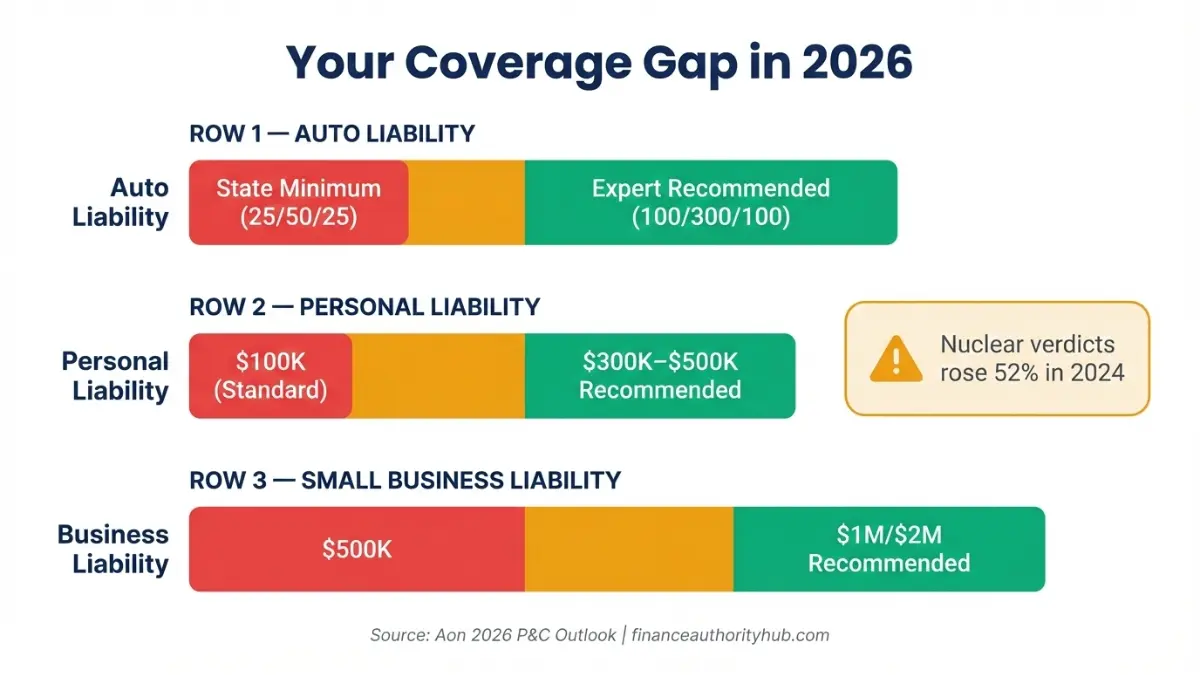

Auto liability insurance is legally required in 49 of 50 US states (New Hampshire is the sole exception). It covers injuries and property damage you cause to others in an at-fault accident — not your own vehicle or injuries.

Two core components:

- Bodily injury liability (BI): Medical bills, lost wages, and legal costs for injured parties

- Property damage liability (PD): Repairs to the other driver’s vehicle or property

2026 national average cost: $808/year ($67/month) for minimum coverage. South Dakota drivers pay as little as $29/month; Michigan averages $154/month.

State minimum format — how to read it: A 25/50/25 policy means:

- $25,000 bodily injury per person

- $50,000 bodily injury per accident

- $25,000 property damage per accident

What it does NOT cover: Your own injuries (need PIP or health insurance) or your vehicle repairs (need collision coverage).

For a full breakdown of auto coverage options and how to cut costs, see our guide on comprehensive car insurance and how to cut car insurance costs by 34%.

3. Professional Liability Insurance (Errors & Omissions / E&O)

Professional liability insurance protects service-based professionals when a client claims your advice, service, or work caused them financial harm. It is also called:

- Errors & Omissions (E&O) — technology, real estate, financial advisors

- Medical malpractice — physicians, surgeons, nurses

- Legal malpractice — attorneys

Who needs it: Accountants, consultants, architects, IT professionals, financial advisors, healthcare providers.

2026 average cost: $50–$100/month ($600–$1,200/year).

Claims-made note: Most professional liability policies are claims-made. If you stop the policy, add tail coverage — without it, you’re exposed for all prior work.

4. Personal Liability Insurance

Personal liability coverage is already included in your homeowners, renters, or condo insurance policy — most people don’t realize this until they need it.

It covers:

- A guest who slips and falls at your home

- Your dog biting a neighbor

- Accidentally damaging someone else’s property while away from home

Standard limits: $100,000–$300,000 (built into your policy). Experts recommend: $300,000–$500,000 minimum.

Important 2026 stat: 1 in every 1,670 insured homeowners files a liability claim each year, according to insurance industry data.

What it does NOT cover: Business activities conducted from home, car accidents, or intentional acts.

If you’re a homeowner, review your personal liability limits as part of your overall homeowners insurance coverage. Renters are also covered — check your renters insurance guide for limit recommendations.

5. Product Liability Insurance

If your business manufactures, distributes, or sells physical products, product liability insurance covers claims that a defective product caused bodily injury or property damage.

- 5,826 product liability cases were litigated in US federal and state courts in 2022 alone (Lex Machina data)

- Between 2018–2022, $214 million in class action settlement damages were awarded in product cases

Who needs it: Manufacturers, wholesalers, retailers, food producers, e-commerce sellers.

What it does NOT cover: Intentional product defects, contractual liabilities, or losses exceeding policy limits.

6. Umbrella Liability Insurance

An umbrella policy sits on top of all your existing liability policies and kicks in when your primary coverage is exhausted.

Example: You cause a serious auto accident. Your auto policy pays $300,000. The judgment is $1.2 million. Your umbrella policy covers the remaining $900,000 — protecting your savings, home, and future income.

2026 average cost: $150–$300/year for $1M in additional coverage — making umbrella insurance one of the best-value purchases in personal finance.

Critical 2026 alert: According to Aon’s 2026 P&C Outlook, most umbrella carriers now deploy only $5–$10 million per layer due to social inflation pressure. If you need higher limits, you may need to stack multiple layers.

Who needs it: Anyone with a net worth above $300,000, homeowners, business owners with public exposure, high earners.

7. Directors & Officers (D&O) Liability Insurance

D&O insurance protects corporate directors and officers from personal financial liability arising from alleged wrongful acts, mismanagement decisions, or governance failures.

2026 emerging risk: AI-related governance claims are now appearing in D&O cases, as companies face scrutiny over algorithmic decision-making and data governance. This is a fast-growing coverage area.

Who needs it: Corporate executives, nonprofit board members, startup founders, any organization with a board of directors.

Master Comparison Table: 7 Types of Liability Insurance (2026)

| Type | Best For | Avg. Monthly Cost | Required by Law? |

|---|---|---|---|

| General Liability | All businesses | $42–$85 | Often contractually required |

| Auto Liability | All drivers | $39–$65 | Yes — 49 states |

| Professional Liability (E&O) | Service professionals | $50–$100 | Sometimes (by state/profession) |

| Personal Liability | Homeowners, renters | Included in HO/renters policy | No |

| Product Liability | Manufacturers, sellers | Varies by industry/risk | No |

| Umbrella Liability | High net worth, businesses | $13–$25/month for $1M | No |

| D&O Liability | Executives, nonprofits | $100–$500+/month | No |

How Much Liability Insurance Do You Actually Need in 2026?

The traditional advice — “buy coverage equal to your net worth” — is no longer sufficient. Here’s why, and what the updated 2026 standard looks like.

The Net Worth Rule Is Outdated

The median nuclear verdict in US courts grew from $19.3 million in 2010 to $24.6 million in 2019 — a 27.5% increase that outpaced economic inflation of 17.2% over the same period. Since then, verdicts have continued to accelerate.

A new October 2025 analysis by the Insurance Information Institute (Triple-I) and the Casualty Actuarial Society found that legal system abuse contributed $231.6 billion to $281.2 billion in excess liability insurance losses over the past decade — far exceeding what economic inflation alone would explain.

Bottom line: If a judgment exceeds your net worth, a plaintiff can pursue your future earnings. Coverage must account for both.

2026 Coverage Benchmarks by Situation

| Your Situation | State/Policy Minimum | Expert 2026 Recommendation |

|---|---|---|

| Driver (personal vehicle) | State minimum (e.g., 25/50/25) | 100/300/100 limits minimum |

| Homeowner | $100K personal liability (standard) | $300K–$500K; add umbrella if assets >$300K |

| Small business owner | $1M per occurrence (contractual standard) | $1M/$2M aggregate minimum; umbrella for high-risk industries |

| Freelancer/consultant | None legally required | $500K–$1M E&O + general liability |

| High-net-worth individual | None legally required | $1M+ umbrella policy |

What This Means For You

Action steps to take right now:

- Pull your current policy declarations page — find your per-occurrence and aggregate limits

- Calculate your total net worth — home equity, investments, retirement accounts, future income

- Compare limits to the 2026 benchmarks above — if you’re under, contact your insurer

- Get an umbrella quote — at $150–$300/year for $1M in extra coverage, it’s one of the most cost-effective financial decisions you can make

- Set an annual review date — general liability rates rose 5.6% in Q4 2025; auto liability rose 9.2% in Q4 2025

For additional financial planning context, our emergency fund guide covers how insurance and savings work together as your financial safety net.

What Liability Insurance Does NOT Cover — The Gaps Nobody Tells You About

Every competitor lists what liability insurance covers. Almost none give you a thorough breakdown of the exclusions that cost people thousands when they find out too late.

Universal Exclusions Across All Liability Policies

- ❌ Your own injuries — liability insurance pays the other party, never you

- ❌ Your own property damage — collision, comprehensive, or property insurance handles this

- ❌ Intentional acts or criminal conduct — no policy covers deliberate harm

- ❌ Employee workplace injuries — covered by workers’ compensation (separate policy)

- ❌ Professional mistakes — require a separate professional liability/E&O policy

- ❌ Pollution or environmental damage — excluded unless specifically endorsed

- ❌ Cyber incidents and data breaches — require standalone cyber liability insurance

- ❌ Claims exceeding your policy limits — umbrella insurance fills this critical gap

- ❌ Contractual liabilities — obligations you voluntarily assumed in a contract

Type-Specific Gaps

Auto liability: Does NOT cover your own medical bills or vehicle repairs. You need collision coverage and PIP/MedPay for that. See our guide on comprehensive car insurance for full coverage options.

General liability: Does NOT cover your own business property (need commercial property), employee injuries (workers’ comp), or professional errors (E&O).

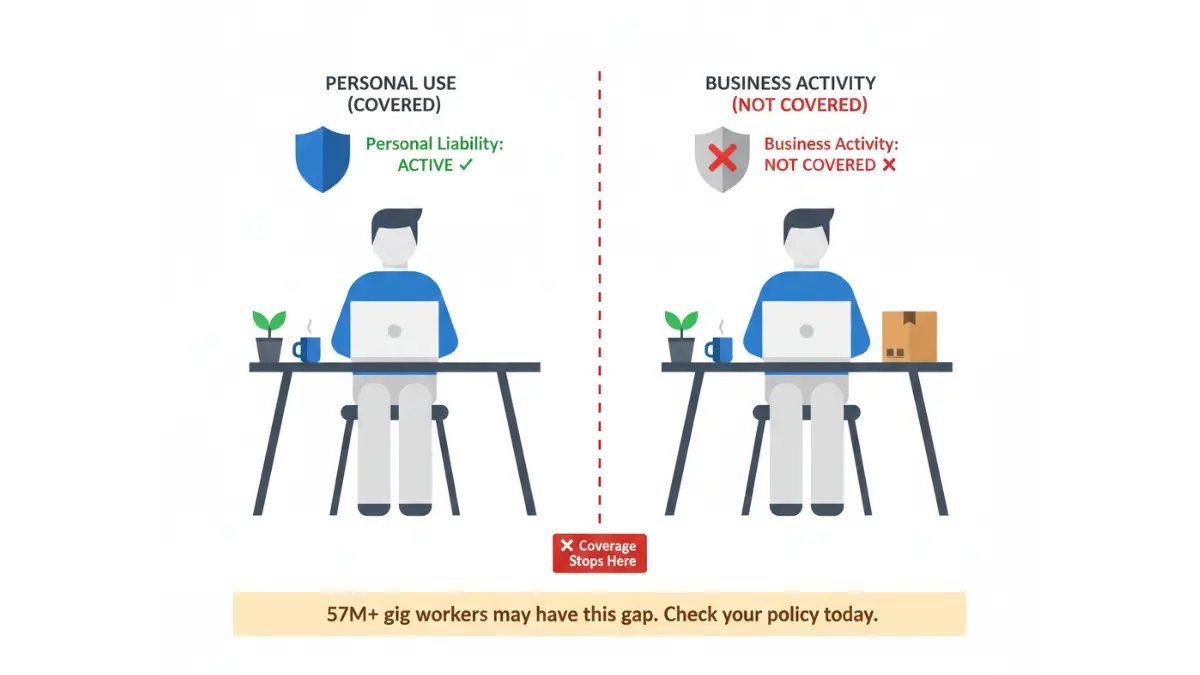

Personal liability (homeowners): Does NOT cover business activities conducted from your home — a critical gap most people discover only after a claim is denied.

The Gig Economy & Remote Worker Gap — What All Competitors Miss

This is the most underreported liability gap in America today.

There are 57+ million gig workers in the US. Most have no idea that:

- Personal auto liability may not cover deliveries or rideshare driving — you need a commercial endorsement or rideshare policy

- Home-based business activities are excluded from personal liability under standard homeowners policies

- A freelancer who injures a client during a home consultation has no coverage unless they carry business liability separately

What to do: If you work from home, drive for income, or operate any business from personal property, contact your insurer immediately to confirm coverage — or purchase a commercial endorsement. The cost is typically $25–$50/month and can prevent six-figure exposure.

How to Get the Right Liability Insurance in 2026 — Step-by-Step

Most liability insurance guides end at explaining coverage. This section gives you the exact process to buy the right policy at the best price.

Step 1 — Identify Which Types You Need

Answer these questions:

- Do you drive? → Auto liability required (minimum by state law)

- Do you own a home? → Personal liability already in your policy — check limits now

- Do you run a business? → General liability (minimum), possibly E&O + product liability

- Do you provide professional services? → Professional liability (E&O) is essential

- Is your net worth over $300K? → Umbrella policy is strongly recommended

Step 2 — Set the Right Coverage Limits

- Personal auto: At minimum, 100/300/100 (well above most state minimums)

- Small business: $1M per occurrence / $2M aggregate standard

- Professional liability: $1M per claim minimum for most professions

- Homeowners personal liability: $300,000–$500,000

Use our home affordability calculator to understand your full asset picture before selecting homeowners and personal liability limits — knowing your home’s value helps set appropriate coverage floors.

Step 3 — Compare Quotes Intelligently

When comparing insurers, evaluate:

- Per-occurrence limit vs. aggregate limit — both matter

- Deductible — higher deductible lowers premium but increases out-of-pocket risk

- Claims-made vs. occurrence policy type (see Section 1)

- AM Best financial strength rating — look for A or A+ rated insurers

- Exclusions — read the exclusions section before signing

Get a minimum of 3 quotes from different insurers. Bundling policies (auto + home + umbrella) typically saves 10–25%.

Step 4 — Understand Your Certificate of Insurance (COI)

A Certificate of Insurance (COI) is a one-page document proving your coverage is active. Landlords, clients, contractors, and lenders commonly require a COI before allowing you to work on-site or sign a lease.

Most insurers provide a COI within 24 hours of policy issuance — many offer same-day digital delivery.

Step 5 — Review Your Coverage Annually

Trigger events that require an immediate policy review:

- Hiring a first employee

- Purchasing property or a vehicle

- Starting a home-based business

- Reaching a new revenue milestone

- Major change in personal net worth

2026 rate warning: Auto liability rates rose 9.2% in Q4 2025 and are forecast to climb a further 7–15% in Q1 2026, according to Aon’s 2026 P&C data. Locking in your renewal now could save hundreds.

For broader financial protection planning, see how liability insurance fits alongside term life insurance and health insurance in a complete personal finance risk strategy.

Frequently Asked Questions About Liability Insurance (2026)

1. What is liability insurance in simple terms?

Liability insurance pays for injuries or property damage you cause to other people. It does not cover your own losses — it protects the person on the other side of the claim, and it protects your assets from being seized to pay that judgment.

2. Is liability insurance required by law?

Auto liability insurance is required in 49 states. Business liability insurance is not required by law in most states but is frequently required by contracts, landlords, and clients. Personal liability insurance is not legally mandated but is included in standard homeowners and renters policies.

3. What does general liability insurance cover?

General liability insurance covers three core areas: bodily injury to a third party, property damage your business causes to someone else’s property, and advertising injury (including libel, slander, and copyright infringement in your marketing). It does not cover employee injuries, your own business property, or professional errors.

4. How much does liability insurance cost per month in 2026?

– Auto liability (minimum): $39–$65/month

– General business liability: $42–$85/month (median $45/month)

– Professional liability (E&O): $50–$100/month

– Umbrella policy ($1M): $13–$25/month

– Personal liability (included in homeowners): No separate cost

5. Does an LLC protect me without liability insurance?

No. An LLC limits personal liability for business debts and contracts, but it does not protect you from personal injury lawsuits, professional negligence claims, or situations where you have personally guaranteed an obligation. You still need liability insurance as an LLC.

6. What is NOT covered by liability insurance?

Your own injuries, your own property damage, intentional acts, employee workplace injuries, professional errors (without E&O), cyber incidents, pollution, and any claims exceeding your policy limits.

7. What is the difference between general liability and professional liability insurance?

General liability covers physical-world claims — someone is hurt, property is damaged. Professional liability (E&O) covers financial harm caused by your professional advice or service — a client claims your work cost them money. Many professionals need both.

8. What is an umbrella liability policy and do I need one?

An umbrella policy extends your existing liability coverage beyond your primary policy limits. It is strongly recommended for anyone with a net worth over $300,000, business owners with public-facing operations, and anyone with significant assets to protect. At roughly $150–$300/year for $1M in additional coverage, it’s exceptional value.

9. How much liability insurance does a small business need?

The industry-standard starting point is $1M per occurrence / $2M aggregate for general liability. High-risk industries (construction, healthcare, hospitality) should work with a licensed broker to determine appropriate limits, especially given the 52% rise in nuclear verdicts in 2024.

10. What is social inflation and why does it affect my coverage limits?

Social inflation (NAIC definition) refers to the rising cost of liability claims driven by nuclear verdicts, third-party litigation funding, and changing jury behavior. The Insurance Information Institute found it contributed $231.6B–$281.2B in excess liability losses over the past decade. This is why coverage limits from 2020–2021 are now often inadequate.

11. Can I get liability insurance if I work from home?

Yes — but your personal homeowners liability policy almost certainly does not cover business activities conducted from your home. You need either a commercial endorsement added to your homeowners policy or a standalone business owner’s policy (BOP). This gap affects millions of remote workers and freelancers who wrongly assume they are covered.

Expert Verdict: What Our Credentialed Panel Recommends

Our panel of 30 internationally credentialed financial and insurance experts at financeauthorityhub.com reached a clear consensus for 2026:

“The single most common and costly mistake Americans make is underinsuring their liability exposure. Given the acceleration of nuclear verdicts and social inflation, coverage limits that felt adequate in 2021 may leave you dangerously exposed today. At minimum, every adult should carry 100/300/100 auto liability, $300,000+ personal liability, and a $1M umbrella policy — the combined annual cost is typically under $400.”

The NAIC, the Insurance Information Institute, and Aon all confirm the same directional trend: liability exposure is growing, and most policy limits are not keeping pace.

⚠️ Disclaimer: This article is for educational and informational purposes only and does not constitute financial, legal, or insurance advice. Liability insurance requirements, coverage options, and costs vary by state, profession, and individual circumstances. Always consult a licensed insurance professional or certified financial planner before making coverage decisions. Coverage details may change — verify current terms with your insurer.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.