Truck Insurance: Real 2026 Rates Most Drivers Overpay

Most truck owners overpay by 20–40% on insurance. This 2026 guide reveals real rates from $77–$2,500/month, legal requirements, and 8 proven ways to cut your premium fast.

In This Article

What Is Truck Insurance and How Much Does It Cost in 2026?

Truck insurance costs $77–$195/month for personal pickup trucks and $900–$2,500+/month for commercial owner-operators in 2026. Most American truck owners are still on their original default policy — and quietly overpaying by 20–40% every year without realizing it.

Auto insurance premiums rose 17.8% in 2024 according to the U.S. Bureau of Labor Statistics Consumer Price Index. Truck owners felt this harder than most. If you haven’t reviewed your truck insurance policy in the last 12 months, there is a strong chance you’re leaving real money on the table.

This guide covers every truck insurance type, real 2026 rate data, legal requirements, and eight proven ways to cut your premium — everything your current insurer doesn’t want you to know.

2026 Truck Insurance Quick Rate Reference:

| Truck Type | Coverage Level | Monthly Rate |

|---|---|---|

| Personal pickup (minimum liability) | State minimum | $77–$99 |

| Personal pickup (full coverage) | 100/300/100 limits | $140–$195 |

| Delivery/gig driver | Commercial add-on | $150–$400 |

| Commercial truck (leased-on) | Primary liability | $250–$500 |

| Owner-operator (own authority) | Full commercial | $900–$1,600 |

| New authority operator | Full commercial | $1,800–$2,500+ |

Which truck insurance type do you need?

- Own a pickup truck for personal use only → Personal auto policy

- Use your truck for DoorDash, Amazon Flex, or any delivery → Commercial endorsement required

- Drive commercially under someone else’s authority → Owner-operator leased-on policy

- Own your own MC number → Own-authority commercial truck insurance

To plan your full vehicle cost picture — including insurance, payments, and maintenance — explore our suite of financial planning tools at financeauthorityhub.com/tools.

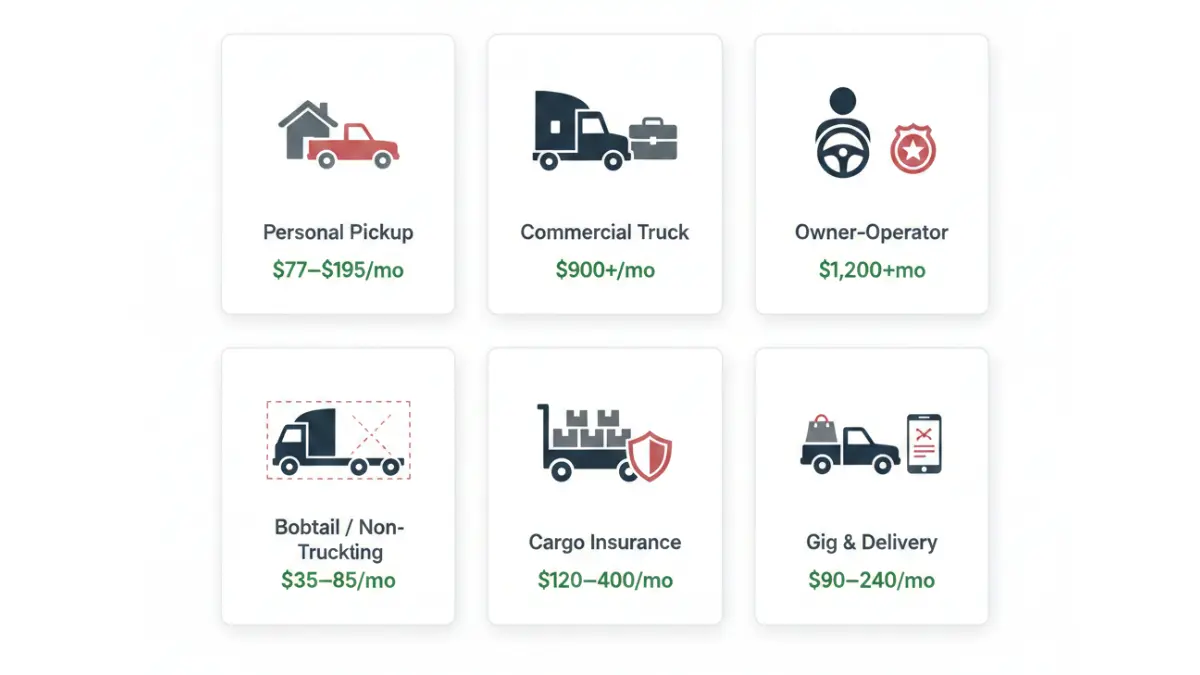

6 Types of Truck Insurance — Which One Actually Covers You?

This is where most drivers make their costliest mistake. Buying the wrong truck insurance type doesn’t just waste money — it can leave you with zero coverage at claim time.

Personal Pickup Truck Insurance

Covers your F-150, Ram 1500, Tacoma, or any other personal-use pickup. Includes liability, collision, comprehensive, and uninsured motorist coverage. Average cost: $77–$195/month depending on model, state, and driving record.

This policy explicitly excludes any commercial use. If you’re hauling materials for a job or driving for hire — even occasionally — a personal policy will deny your claim.

Commercial Truck Insurance

Required when a truck is used to transport goods, haul cargo, or support a business. Covers tractor-trailers, box trucks, flatbeds, dump trucks, and fleet vehicles. Average cost: $200–$600/month for smaller commercial vehicles, significantly higher for heavy-duty rigs.

The Insurance Information Institute confirms that personal auto policies provide no coverage for vehicles owned by a business or used primarily for business purposes.

Owner-Operator Truck Insurance

For independent truckers who own their truck and haul under their own MC (motor carrier) authority. This is the most complex and expensive category. Leased-on drivers (operating under a carrier’s authority) pay $250–$500/month. Own-authority operators pay $900–$2,500+/month.

Bobtail Insurance (Non-Trucking Liability)

Covers a semi-truck driver when operating without a trailer — between loads, after delivery, or driving home. Your primary commercial policy only covers you while under dispatch. Cost: $30–$50/month added to your base policy.

This coverage is frequently skipped and frequently denied at claim time. It’s one of the most overlooked gaps in trucking insurance. For a deeper look at how liability coverage works across vehicle types, see our guide on liability car insurance.

Motor Truck Cargo Insurance

Protects the freight you’re hauling in case of theft, damage, or loss. Required by most brokers and shippers. Coverage typically ranges from $50,000 to $250,000 in cargo limits. Cost: $100–$300/month as a standalone add-on.

Gig & Delivery Driver Coverage (The Gap No Competitor Covers)

This is the fastest-growing uninsured category in the US right now. If you use your personal truck for DoorDash, Instacart, Amazon Flex, or any other gig platform — your personal auto policy is almost certainly void during deliveries.

Most major carriers offer a commercial use endorsement for $50–$150/month extra. Some gig platforms provide limited third-party liability while you’re on an active delivery — but this coverage ends the moment you mark the delivery complete. You are responsible for obtaining your own coverage for the rest of your driving time.

Coverage Type Comparison Table:

| Coverage Type | Who Needs It | Avg. Monthly Cost | Legally Required? |

|---|---|---|---|

| Personal auto | Pickup truck owners | $77–$195 | Yes (state minimum) |

| Commercial liability | Business fleet owners | $200–$600 | Yes (federal + state) |

| Owner-operator (own authority) | Independent truckers | $900–$2,500 | Yes (FMCSA) |

| Bobtail/non-trucking liability | Semi drivers between loads | +$30–$50 | Recommended |

| Motor truck cargo | Freight carriers | +$100–$300 | Required by brokers |

| Gig/delivery endorsement | DoorDash, Amazon Flex drivers | +$50–$150 | Yes (contract terms) |

Truck Insurance Rates in 2026: Real Numbers by State and Company

Truck insurance isn’t just expensive — it’s been getting more expensive faster than almost any other insurance category. Understanding what’s driving costs in 2026 helps you push back effectively when shopping for quotes.

Why Truck Insurance Rates Are Higher in 2026

The Insurance Information Institute reports that commercial auto defense and containment expenses have nearly tripled over the past decade, driven by litigation costs, higher vehicle repair bills, and more frequent severe weather events. According to the Triple-I’s Commercial Auto Trends and Insights report, social inflation — excessive litigation driving up settlements — remains the primary cause of commercial truck insurance premium increases.

For personal pickup trucks, the CPI for motor vehicle insurance rose 17.8% in 2024 alone. This is why renewal quotes are shocking drivers nationwide.

Cheapest vs. Most Expensive States for Truck Insurance (2026)

| State | Personal Pickup (Monthly) | Commercial Truck (Monthly) |

|---|---|---|

| Vermont | ~$90 | ~$284 |

| Iowa | ~$95 | ~$295 |

| Pennsylvania | ~$102 | ~$310 |

| Ohio | ~$108 | ~$320 |

| Florida | ~$198 | ~$450+ |

| Michigan | ~$210 | ~$470+ |

| Louisiana | ~$205 | ~$460+ |

High-premium states share common traits: high population density, aggressive litigation environments, and higher-than-average severe weather claims. If you’re in Florida or Michigan, comparing multiple quotes is non-negotiable.

Best Truck Insurance Companies in 2026 — Rate vs. Quality

| Company | Best For | Avg. Monthly (Pickup Full Coverage) | AM Best Rating |

|---|---|---|---|

| Auto-Owners | Cheapest full coverage | ~$84 | A++ |

| GEICO | Budget-conscious personal trucks | ~$91 | A++ |

| Erie | Claims satisfaction | ~$110 | A+ |

| Progressive | Commercial + fleet coverage | ~$140 | A+ |

| The Hartford | Small fleet operators | ~$200 | A+ |

| OOIDA | Owner-operators specifically | ~$250+ | B++ |

| Nationwide | Multi-vehicle and fleet | ~$204 | A+ |

According to Progressive’s IIHS-HLDI analysis of cheapest trucks to insure, midsize pickup trucks average $1,527 annually — making them among the most affordable vehicle categories to insure overall.

Cheapest Pickup Trucks to Insure in 2026

- Ford Maverick — ~$177/month (cheapest on the market)

- Ford Ranger — ~$180/month

- Nissan Frontier — ~$184/month

- Honda Ridgeline — ~$193/month

- Chevrolet Colorado — ~$194/month

Most expensive: Ram 1500 TRX (~$3,255/year), GMC Hummer EV (~$343/month), Ford Super Duty (~$300/month).

💡 What This Means For You: If you’re driving a Ram TRX or Ford Super Duty for personal use, switching to a less expensive-to-insure model at renewal could save $1,000–$1,500/year in premiums alone. Also, if your truck insurance premium is squeezing your monthly budget, our automobile insurance rates guide breaks down all vehicle types side-by-side.

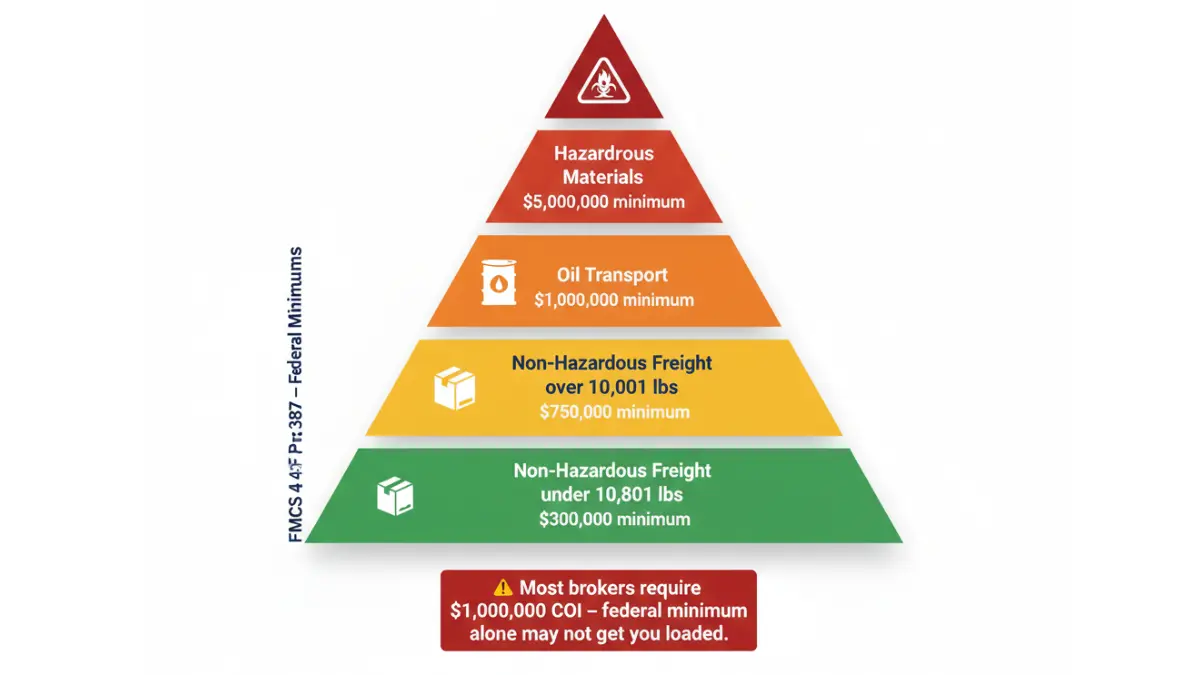

FMCSA Requirements: What the Law Actually Demands in 2026

Buying the wrong commercial truck policy — or the right one with the wrong limits — doesn’t just waste money. It can cost you your operating authority and your livelihood.

Per FMCSA’s insurance filing requirements under 49 CFR Part 387, operating authority will not be granted until minimum financial responsibility is on file. This is non-negotiable federal law.

Minimum Federal Liability Coverage by Cargo Type

| Cargo / Operation Type | Minimum Liability Required |

|---|---|

| Non-hazardous property (over 10,001 lbs) | $750,000 |

| Non-hazardous property (under 10,001 lbs) | $300,000 |

| Oil transport | $1,000,000 |

| Hazardous materials (certain categories) | $5,000,000 |

What Is a COI — and Why Brokers Reject Loads Without It

A Certificate of Insurance (COI) is the document your insurer files proving your coverage is in force. Brokers check it before every load. If your COI limits don’t match the rate confirmation — typically $1M auto liability and $100K cargo — you don’t get loaded. Period.

Many new operators discover this the hard way: their coverage technically meets federal minimums but fails broker COI requirements. Always ask your agent: “Will this policy get me a COI that meets standard broker requirements?”

2026 FMCSA Rule Update

Effective January 16, 2026, new financial responsibility rules for brokers and freight forwarders came into force. These changes tightened requirements for proof of insurance filings and COI turnaround timelines. If you renewed your policy before this date, verify your filings are current with your insurance provider immediately.

💡 Key Takeaway: Federal minimums are a floor, not a target. Most brokers require $1M liability. If your policy shows $750K, you may meet legal requirements and still lose loads. Understanding comprehensive car insurance coverage structures can help you understand what “full coverage” actually means across different vehicle types.

How to Lower Your Truck Insurance Premium: 8 Tactics That Work in 2026

The average truck owner overpays by $400–$900 per year. Not because they can’t get better rates — but because they never ask, never compare, and never take the five steps that move the needle.

Here are eight tactics that actually work in 2026, ranked by average savings impact:

1. Compare at least 3 quotes before renewal Rates for the identical driver profile vary 30% or more between carriers. One quote is not a market price — it’s one company’s guess. Get Progressive, GEICO, and at least one regional carrier on the same coverage before deciding.

2. Install a dash cam or telematics device Programs like Progressive’s Snapshot or Nationwide’s SmartRide offer up to 20–40% savings based on documented safe driving behavior. For commercial operators, GPS and ELD data can reduce premiums significantly when presented to underwriters.

3. Pay annually, not monthly Monthly payment plans include financing fees that add $150–$400/year to your total cost. Paying in full at renewal eliminates this entirely. If cash flow is a concern, our affordable car insurance guide outlines strategies for making annual payments manageable.

4. Raise your deductible strategically Moving your deductible from $500 to $1,000 typically reduces your premium by 10–15%. Only do this if you have accessible emergency savings to cover the deductible if needed.

5. Bundle your policies Combining your truck insurance with home, life, or other coverage with one carrier typically saves $200–$400/year. This is one of the most underused discounts in the market.

6. Clean your Motor Vehicle Record (MVR) six months before renewal Insurers pull your MVR at renewal. Minor violations typically fall off after three years. Timing your renewal or policy start date after a violation ages off the three-year window can meaningfully reduce your rate.

7. Shop 60 days before renewal, not at the last minute Last-minute renewals force you into expensive or non-standard markets. Starting your quote process 60 days out gives you leverage, time to compare, and access to better pricing tiers.

8. Maintain continuous coverage — never let it lapse Even a 30-day gap in coverage is flagged by underwriters and can spike your next premium by 15–25%. This applies to both personal and commercial truck insurance.

💡 What This Means For You: Applying just three of these tactics — comparing quotes, installing telematics, and paying annually — can realistically save $600–$1,200/year on a full-coverage commercial policy. For strategies to redirect those savings, see our guide on how to save $1,000 fast.

Truck Insurance FAQs: 11 Questions Answered

1. How much is truck insurance per month?

Personal pickup truck insurance averages $77–$195/month for full coverage in 2026. Commercial truck insurance for owner-operators runs $900–$2,500+/month depending on authority type, cargo, and operating radius.

2. Is truck insurance more expensive than regular car insurance?

For personal pickup trucks, the difference is small — about 6% more than average car insurance nationally ($2,669 vs. $2,513 annually). Commercial truck insurance is in a completely different cost tier than personal auto.

3. What does truck insurance cover?

A standard full-coverage truck insurance policy covers liability (bodily injury + property damage), collision, comprehensive, and uninsured/underinsured motorist. Commercial policies add cargo, bobtail, and motor carrier liability options.

4. Do I need commercial truck insurance for my personal truck?

Only if you use it for business. Delivering goods, hauling materials for pay, or driving for any gig platform triggers a commercial coverage requirement. Personal auto policies explicitly exclude business use.

5. What is the cheapest pickup truck to insure in 2026?

The Ford Maverick is the cheapest pickup truck to insure in 2026, averaging approximately $177/month for full coverage. The Ford Ranger and Nissan Frontier follow closely.

6. What is bobtail insurance?

Bobtail insurance (also called non-trucking liability) covers a semi-truck operator when driving without a trailer — for example, after dropping a load or commuting home. Most primary commercial policies do not cover this period.

7. How do I get cheaper commercial truck insurance?

The most effective tactics are: comparing multiple quotes 60 days before renewal, installing dash cams or GPS telematics, paying annually, and maintaining a clean loss run (no claims history). Clean safety records are the single biggest discount lever.

8. What is the FMCSA minimum insurance for owner-operators?

The FMCSA requires a minimum of $750,000 in primary liability for non-hazardous freight over 10,001 lbs under 49 CFR Part 387. Hazardous materials require up to $5,000,000. Most brokers require $1,000,000 as a COI minimum regardless.

9. Does truck insurance cover cargo?

Not automatically. Motor truck cargo insurance is a separate coverage that must be added to your policy. Most brokers require cargo limits of at least $100,000. Without it, any freight damage or theft is your personal financial liability.

10. Why did truck insurance rates go up in 2026?

Three converging factors: rising vehicle repair costs, social inflation (litigation driving larger jury awards), and increased severe weather events. The Insurance Information Institute documented commercial auto defense costs nearly tripling over the past decade. Rates are expected to remain elevated through 2026–2027.

11. Can I insure my truck for business and personal use on the same policy?

Yes — with the right policy structure. A commercial auto policy can include personal use provisions. Some carriers also offer a “business use” endorsement on a personal auto policy for lighter commercial activity. Always disclose your actual usage when getting quotes — misrepresentation is grounds for claim denial.

⚠️ Disclaimer: This article is for educational and informational purposes only and does not constitute financial, legal, or insurance advice. Truck insurance rates vary based on individual circumstances, driving record, location, vehicle type, and coverage selections. Rate figures cited are 2025–2026 industry averages and benchmarks — your actual quote will differ. Always consult a licensed insurance professional before making coverage decisions. External links to government and industry sources are provided for reference only.

Related Guides You May Find Helpful:

- Automobile Insurance Rates 2026: Complete Guide

- Gap Insurance: Do You Really Need It?

- Car Insurance: Cut Costs 34% in 2026

- Comprehensive Car Insurance Explained

- Insurance: Stop Overpaying in 2026

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.