Auto Loan Calculator 2026 – See Your Real Monthly Payment

Auto Loan Calculator

Estimate monthly payment and total cost using vehicle price, down payment, trade-in, sales tax, fees, APR, and term.

Inputs

This tool includes sales tax, fees, and trade-in to estimate the amount financed, which is how many auto loan calculators present “out-the-door” payment planning. [web:55][web:58]

Results

Estimated monthly payment

—

Payoff: — • Months: —

Amount financed (estimate)

—

Sales tax: —

Fees

—

—

Cash due (down + upfront fees): —

Trade-in summary

Net trade-in (approx.): —

Loan owed on trade: —

Lifetime totals (loan only)

Total interest: —

Total paid: —

Yearly amortization summary

| Year | Paid | Principal | Interest | Extra paid | Ending balance |

|---|

Monthly amortization schedule

| Month | Payment | Principal | Interest | Extra paid | Remaining balance |

|---|

Results appear after you click “Calculate.”

In This Article

Quick Answer: An auto loan calculator helps you estimate your exact monthly car payment based on vehicle price, down payment, interest rate (APR), and loan term. As of February 2026, the average auto loan interest rate dropped to 6.98% for a 60-month new car loan — the first time it has fallen below 7% since June 2023. Use the calculator above to see your real number in 30 seconds.

What Is an Auto Loan Calculator — and Why This One Is Different

Americans are carrying $1.66 trillion in auto loan debt, making car financing one of the most significant financial commitments most households make. Yet most people walk into a dealership without calculating their true monthly payment — and get burned.

A car loan calculator takes five inputs — vehicle price, down payment, trade-in value, APR, and loan term — and instantly shows your monthly payment, total interest paid, and payoff date. But here’s what most calculators skip.

What makes our auto loan calculator different from Bankrate, NerdWallet, and every other competitor:

- ✅ Sales tax included — most calculators ignore this $1,500–$4,000 cost

- ✅ Dealer fees included — title, registration, and doc fees are part of your real payment

- ✅ Trade-in + loan balance owed — calculates negative equity automatically

- ✅ Roll fees into loan option — shows you the true financed amount

- ✅ Extra monthly payment impact — see how $100/month extra saves you thousands

- ✅ Full amortization schedule — monthly and yearly breakdown

- ✅ CSV download — export your payment schedule instantly

- ✅ 22 currencies — works for US, UK, Canada, Australia, and more

The result? You see your real out-the-door payment — not a stripped-down estimate. Browse our full suite of financial tools to plan every aspect of your purchase.

How to Use This Auto Loan Calculator (5-Step Guide)

Most people miss two or three inputs and get a payment estimate that’s $80–$150 off. Here’s how to get an accurate result every time.

Step 1: Enter Your Vehicle Price

This is the sticker price or negotiated selling price — not the MSRP. Always negotiate this number down before calculating your loan. Your financed amount starts here.

Step 2: Add Down Payment + Trade-In Value

Enter your cash down payment. If you’re trading in a vehicle, enter its current market value (check Kelley Blue Book or Edmunds). Also enter your trade-in loan balance owed if you still have payments remaining — this is what causes negative equity and most calculators ignore it entirely.

Step 3: Enter Sales Tax Rate + Fees

Look up your state’s sales tax rate. Add dealer fees: title, registration, and documentation fees typically run $500–$1,200 depending on your state. Check “Roll fees into loan” if you want them financed — the calculator will show you exactly how this changes your monthly payment and total interest. Understanding the difference between APR vs. interest rate matters here — APR includes fees, interest rate does not.

Step 4: Enter Your APR and Loan Term

Your APR comes from your lender’s pre-approval offer, not the dealership. Enter the term in months: 36, 48, 60, 72, or 84 months are most common. We’ll cover exactly which term to choose in Section 5.

Step 5: Hit Calculate — Read Every Number

Don’t just look at the monthly payment. Check total interest paid — that’s your true cost of borrowing. Check payoff date. Then adjust inputs to compare scenarios side by side.

What Each Result Means:

| Result | What It Tells You |

|---|---|

| Monthly Payment | Your required payment each month |

| Amount Financed | Total borrowed (price – down + tax + fees) |

| Total Interest Paid | The real cost of the loan beyond principal |

| Payoff Date | When you own the car free and clear |

| Amortization Schedule | Month-by-month principal vs. interest breakdown |

Pro Tip: Apply to 3 lenders in the same 14-day window. Per the Consumer Financial Protection Bureau, multiple inquiries within this window count as a single credit pull — protecting your score while getting competing offers.

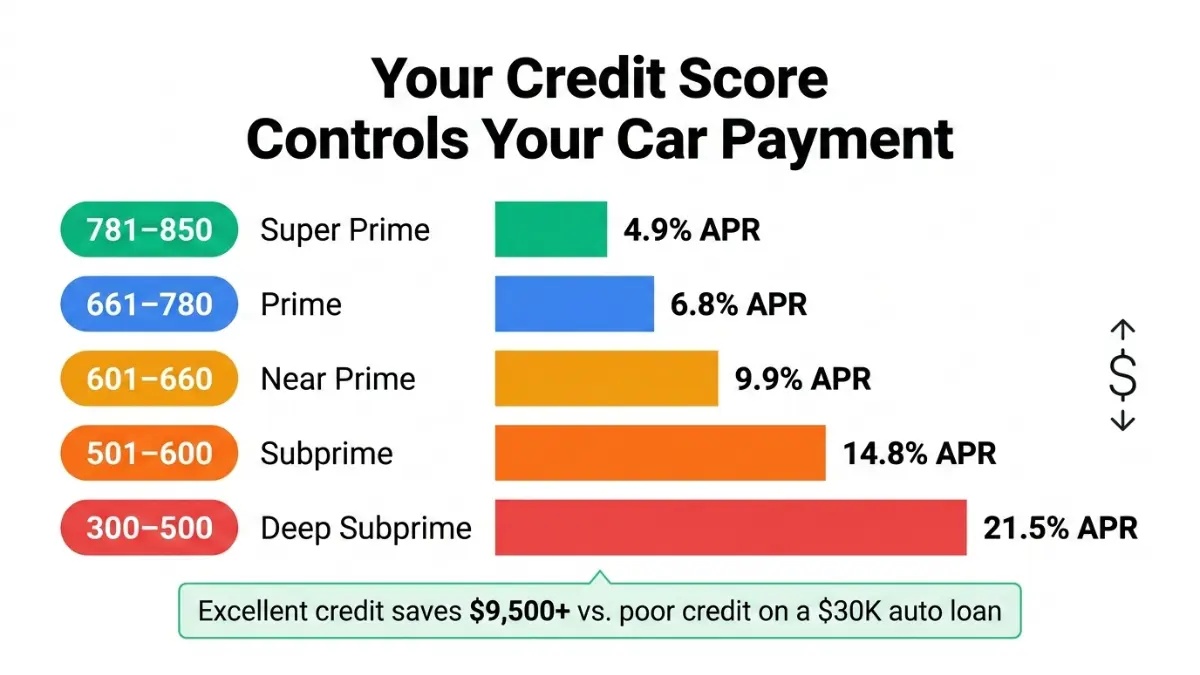

2026 Auto Loan Rates by Credit Score — The Table Competitors Won’t Show You

Your credit score is the single biggest factor controlling your monthly payment. A borrower with excellent credit pays around $160 less per month than a borrower with poor credit — and may end up saving over $9,500 in total interest over the life of the loan.

Here is what your credit score means for your car loan right now in 2026:

| Credit Score | Tier | New Car APR | Used Car APR | Monthly Payment ($30K / 60 mo.) | Total Interest ($30K) |

|---|---|---|---|---|---|

| 781–850 | Super Prime | ~5.2% | ~6.8% | ~$572 | ~$3,320 |

| 661–780 | Prime | ~6.9% | ~9.1% | ~$594 | ~$5,640 |

| 601–660 | Near Prime | ~9.7% | ~13.2% | ~$635 | ~$8,100 |

| 501–600 | Subprime | ~13.1% | ~18.4% | ~$685 | ~$11,100 |

| Below 500 | Deep Subprime | ~15.8%+ | ~21%+ | ~$720+ | ~$13,200+ |

Sources: Experian State of the Automotive Finance Market Q3 2025; Bankrate weekly rate survey, February 2026.

What This Means For You: Plug your credit tier’s APR into the auto loan calculator above right now. The difference between a 700 and 780 score on a $30,000 loan is not small — it’s over $5,000 in your pocket.

How to Get a Lower APR in 2026

- Get pre-approved before you visit the dealer. This is your single most powerful move.

- Shop credit unions — credit unions and online lenders are likely to offer lower rates than dealerships and their captive financing arms.

- Increase your down payment. More equity upfront signals lower lender risk.

- Add a creditworthy co-signer. This can drop your rate by 2–3 percentage points.

- Target a 36–60 month term rather than 72–84 — shorter terms get better APRs.

Rates are expected to remain relatively stable in early 2026. Borrowers with strong credit may see a modest decrease through the year, while those with poor credit are less likely to see meaningful relief. If you’re managing existing debt while planning this purchase, use our debt consolidation calculator to see if consolidating first could free up DTI and improve your loan eligibility.

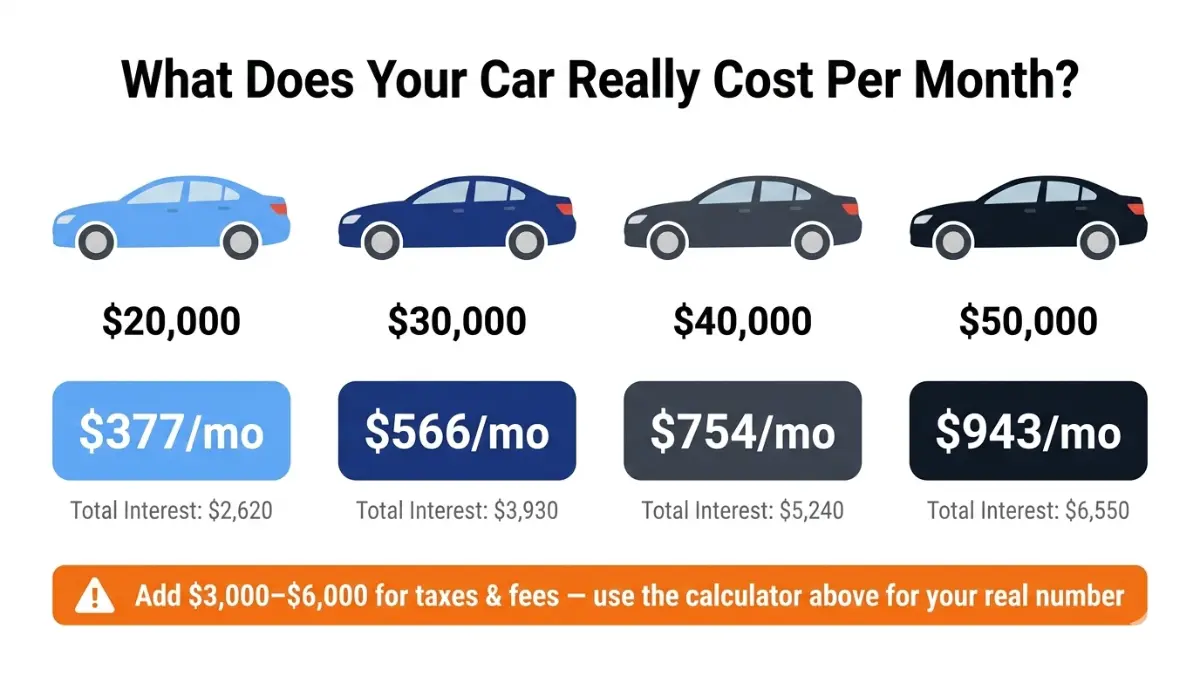

Real Auto Loan Payment Examples — $20K to $50K Cars

Wondering what a $30,000 car actually costs per month? These are real 2026 numbers, not estimates.

$20,000 Car — Monthly Payments at 6.98% APR

| Term | Monthly Payment | Total Interest |

|---|---|---|

| 48 months | $478 | $2,944 |

| 60 months | $396 | $3,760 |

| 72 months | $339 | $4,408 |

$30,000 Car — Monthly Payments at 6.98% APR

| Term | Monthly Payment | Total Interest |

|---|---|---|

| 48 months | $717 | $4,416 |

| 60 months | $594 | $5,640 |

| 72 months | $509 | $6,648 |

$40,000 Car — Monthly Payments at 6.98% APR

| Term | Monthly Payment | Total Interest |

|---|---|---|

| 48 months | $956 | $5,888 |

| 60 months | $792 | $7,520 |

| 72 months | $678 | $8,816 |

$50,000 Car — Monthly Payments at 6.98% APR

| Term | Monthly Payment | Total Interest |

|---|---|---|

| 48 months | $1,195 | $7,360 |

| 60 months | $990 | $9,400 |

| 72 months | $848 | $11,056 |

⚠️ Hidden Cost Warning: Dealer fees, sales tax, and add-ons can silently add $3,000–$6,000 to your loan amount. That’s why the calculator above includes all of them — most competing calculators do not. Run your full scenario using the tool at the top of this page.

The 20/4/10 Rule — Is Your Payment Actually Affordable?

This is the rule financial advisors use to keep car buyers out of trouble:

- 20% down payment minimum

- 4 years (48 months) maximum loan term

- 10% of your gross monthly income maximum on all car-related costs (payment + insurance + gas)

If your payment fails this test, you risk being upside-down on your loan — owing more than the car is worth — which creates a dangerous financial trap at trade-in time. After you calculate your car payment, use our home affordability calculator to ensure your total monthly obligations stay within budget.

The average new car payment reached $748 per month in Q3 2025 — a near-record high. Before committing to that number, make sure it fits your overall budget, not just your car budget.

How to Get the Lowest Auto Loan Rate in 2026 — and Avoid Costly Mistakes

6 Proven Strategies to Lower Your Monthly Car Payment

1. Get pre-approved before you step on the lot. This is non-negotiable. Pre-approval from a bank, credit union, or online lender gives you a baseline APR that dealers must beat to earn your business. The CFPB’s auto loan shopping guide confirms this as the single most effective strategy for borrowers.

2. Compare at least 3 lenders in a 14-day window. Per federal credit scoring rules, multiple auto loan inquiries within 14–45 days count as one inquiry. No credit damage for shopping smart.

3. Increase your down payment. Every $1,000 extra you put down reduces your financed amount and monthly payment. It also reduces your lender’s risk — which can unlock a slightly lower APR.

4. Choose the shortest term you can comfortably afford. We’ll explain exactly why in the next section. Shorter = lower APR + dramatically less interest paid.

5. Improve your credit score first. Improving your credit score from fair to very good could save you an average of $2,316 on your car loan alone — plus tens of thousands more across mortgages, credit cards, and personal loans over your lifetime. Read our complete credit score guide to find fast, actionable ways to move your score before you apply.

6. Time your purchase strategically. End of month, end of quarter, and holiday weekends are when dealers are most motivated to hit sales targets and offer better terms.

5 Auto Loan Mistakes That Cost Americans Thousands

Mistake #1: Focusing only on the monthly payment. Dealers love extending your term to 72 or 84 months because it drops your monthly payment — but dramatically increases total interest. Always look at the total cost of the loan.

Mistake #2: Skipping pre-approval. Walking in without pre-approval hands the interest rate negotiation entirely to the dealer. You’ll almost always pay more.

Mistake #3: Not factoring in sales tax and fees. Taxes and dealer fees can add 8–10% to the cost of your car depending on your state and dealership. A $35,000 car can easily become a $38,500+ financed amount.

Mistake #4: Rolling negative equity from your trade-in. If you owe $14,000 on a car worth $10,000, you’re $4,000 underwater. Rolling this into your new loan means you’re financing negative equity — and paying interest on it for years.

Mistake #5: Financing dealer add-ons. Extended warranties, paint protection, and GAP insurance rolled into your loan mean you’ll pay interest on floor mats for 60 months. Negotiate add-ons separately or decline them. Note: GAP insurance is worth having if your loan exceeds 80% of the car’s value — but buy it from your own insurer, not the dealership. Learn more in our guide to GAP insurance and automobile insurance rates 2026.

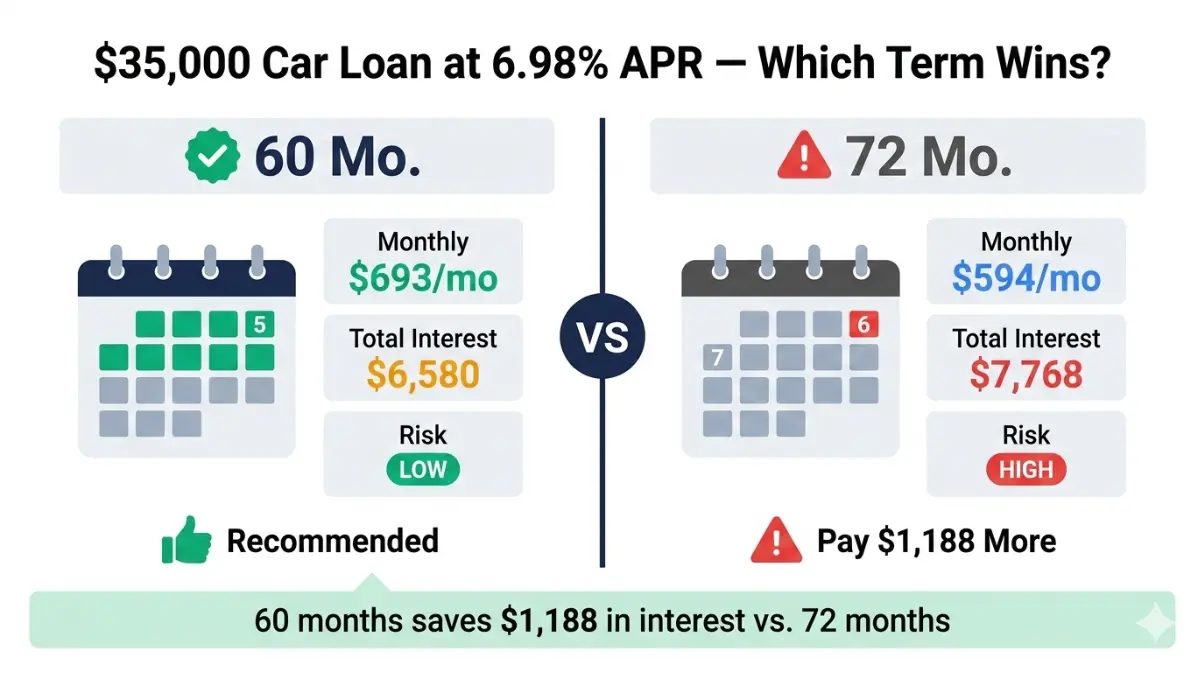

Should You Choose 60 or 72 Months? Real Numbers

This is the most common question buyers ask — and most sites give a vague answer. Here are the actual numbers on a $35,000 loan at 6.98% APR:

| Term | Monthly Payment | Total Interest | Total Cost |

|---|---|---|---|

| 48 months | $840 | $5,320 | $40,320 |

| 60 months | $693 | $6,580 | $41,580 |

| 72 months | $594 | $7,768 | $42,768 |

| 84 months | $522 | $9,848 | $44,848 |

Verdict: The jump from 60 to 72 months saves only $99/month but costs $1,188 more in interest. The jump from 60 to 84 months saves $171/month but costs $3,268 more — plus you’re at high risk of being upside-down for years. If you’re also managing mortgage payments alongside this decision, our mortgage refinance calculator can help you see your full debt picture before committing to a long car loan.

The Federal Reserve Bank of New York’s Household Debt Report confirms that auto loan delinquency rates are rising — a direct result of borrowers choosing unaffordable longer terms to get manageable-looking payments.

Frequently Asked Questions — Auto Loan Calculator 2026

1. What is a good auto loan interest rate in 2026?

The average rate for a 60-month new car loan now sits at 6.98% — the lowest since June 2023. A “good” rate is anything at or below this benchmark. Borrowers with excellent credit (781+) can expect 5%–5.5% on new vehicles.

2. How much car can I afford on a $60,000 salary?

Using the 10% rule, your total monthly car costs should stay under $500. That includes payment, insurance, gas, and maintenance. At 6.98% APR for 60 months, $500/month supports a loan of roughly $24,800. Add your down payment to that for your target vehicle price.

3. What credit score do I need for the best auto loan rate?

You need a score of 781 or higher (Super Prime) to qualify for the lowest advertised rates and manufacturer incentives. Scores between 661–780 (Prime) still get competitive rates. Below 660, rates rise sharply — improving your score before applying is worth the wait.

4. Is 72 months too long for a car loan?

For most buyers, yes. At 72 months, you’ll pay significantly more in total interest, and for the first 2–3 years, depreciation outpaces your payoff — leaving you upside-down. Choose 60 months or fewer unless 72 months is the only way to stay within a safe debt-to-income ratio.

5. How does a trade-in affect my auto loan?

Your trade-in value is subtracted from the vehicle price, reducing the amount financed. However, if you still owe money on your trade-in, that negative equity gets added back to your new loan. Our calculator handles this automatically — enter both fields for an accurate result.

6. Should I put 20% down on a car?

The 20% rule is a strong guideline. A larger down payment reduces your loan amount, monthly payment, total interest, and risk of negative equity. It also improves your odds of approval and your offered APR.

7. What is APR vs. interest rate on a car loan?

The interest rate is the base cost of borrowing. APR (Annual Percentage Rate) includes the interest rate plus any lender fees — making it the more accurate number to compare across loan offers. Always compare APRs, not interest rates. Our APR complete guide breaks down the math clearly.

8. Does getting pre-approved hurt my credit score?

A soft inquiry (pre-qualification) has zero impact. A hard inquiry (formal application) lowers your score slightly. But per federal credit scoring rules, multiple auto loan inquiries within a 14-to-45-day window count as a single inquiry — so shop freely within that window.

9. What is negative equity on a car loan?

Negative equity (also called being “upside-down”) means you owe more on your loan than the car is currently worth. This is common in the first 2–3 years of a loan due to depreciation. GAP insurance covers this gap if the vehicle is totaled or stolen.

10. Can I pay off my auto loan early?

Yes — and it saves you significant interest. Most auto loans have no prepayment penalty. Use the “Extra Monthly Payment” field in our calculator above to see exactly how much you’d save and how many months you’d eliminate by paying an extra $50, $100, or $200/month.

11. How is my monthly car payment calculated?

Your payment uses this formula: M = P × [r(1+r)^n] ÷ [(1+r)^n − 1], where P = loan principal, r = monthly interest rate (APR ÷ 12), and n = number of months. The calculator above handles all of this automatically — including taxes, fees, and trade-in adjustments that competitors omit.

📋 Disclaimer: This article and the auto loan calculator on this page are for educational and informational purposes only. They do not constitute financial, legal, or credit advice. Monthly payment estimates are approximations and may vary based on lender-specific terms, credit profile, state taxes, dealer fees, and other factors. Always verify your actual loan terms with a licensed lender before making any financial commitment. Auto loan rates change frequently — confirm current rates directly with your lender or financial institution.

🔗 Related Tools & Guides You May Find Helpful:

- Planning to buy a home too? Try our mortgage calculator

- Already have a car loan? See if refinancing makes sense with our mortgage refinance calculator

- Understand your full debt picture with our debt consolidation guide

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.