APR vs Interest Rate: Stop Overpaying in 2026

APR and interest rate aren’t the same — and lenders count on your confusion. Discover the hidden fee gap, 2026 real rates by loan type, and how to fight back.

In This Article

APR (annual percentage rate) is the true cost of borrowing — it includes your interest rate PLUS all lender fees. Your interest rate is just one piece. The gap between the two can cost you thousands of dollars on a single loan. Most borrowers never check the difference. By the end of this guide, you will.

APR vs Interest Rate — The Core Difference Explained

What Is an Interest Rate?

Your interest rate is the basic cost a lender charges to borrow money. It is expressed as a percentage of your loan principal. It does not include any fees, closing costs, or origination charges.

Think of it as the sticker price — what the lender advertises. It looks appealing. But it is not the full story.

What Is APR? The Full 2026 Definition

APR (annual percentage rate) is the complete annual cost of borrowing. It wraps your interest rate together with all mandatory fees charged by the lender, then expresses the total as a yearly percentage.

The Consumer Financial Protection Bureau (CFPB) defines APR as “a broader measure of the cost of borrowing money than the interest rate.” It was mandated by the Truth in Lending Act (TILA) specifically so borrowers could compare lenders on a level playing field.

APR vs Interest Rate: Side-by-Side Comparison

| Feature | Interest Rate | APR |

|---|---|---|

| What it measures | Cost of borrowed principal | Total cost of borrowing |

| Includes lender fees? | ❌ No | ✅ Yes |

| Includes origination fees? | ❌ No | ✅ Yes |

| Includes mortgage points? | ❌ No | ✅ Yes |

| Which is higher? | Always lower | Always higher |

| Best used for | Understanding monthly payments | Comparing loan offers |

Why Is APR Always Higher Than the Interest Rate?

APR folds in fees that your interest rate ignores entirely. Common fees bundled into APR include:

- Origination fees (typically 1%–10% of the loan amount)

- Mortgage broker fees

- Discount points paid at closing

- Private mortgage insurance (PMI)

- Certain closing costs

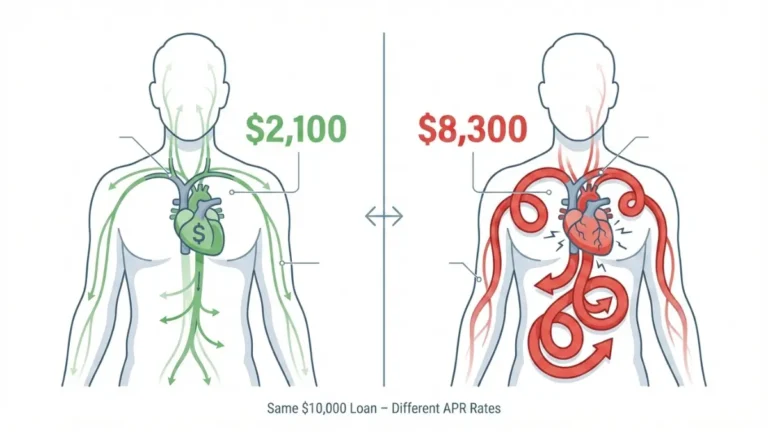

What This Means For You: When a lender advertises a 6.0% mortgage rate and your Loan Estimate shows 6.38% APR — that 0.38% gap represents thousands in real fees. Always compare APR, not just the interest rate. Use our Mortgage Calculator to see exactly how much your lender’s fees add to your total cost.

Current APR Rates in 2026 — What You Should Actually Be Paying

The Federal Reserve held the federal funds rate steady at 3.50–3.75% in January 2026 after three cuts in 2025. This directly shapes what APRs look like across all loan types right now. You can track official benchmark rate data on the Federal Reserve’s H.15 Selected Interest Rates release.

2026 APR Rates by Loan Type

| Loan Type | Avg Interest Rate | Avg APR | Fee Gap | Good APR Target |

|---|---|---|---|---|

| 30-yr Fixed Mortgage | 6.10–6.16% | 6.38–6.55% | 0.2–0.4% | Below 6.5% |

| 15-yr Fixed Mortgage | ~5.46–5.50% | ~5.65–5.85% | ~0.2% | Below 5.9% |

| Personal Loan | 7%–12.16% avg | 7%–35.99% | 0–10% | Below 12% |

| Credit Card | ~19.7% avg | ~19.7% avg | $0 | Below 20% |

| Auto Loan | ~7–9% | ~8–11% | ~1–2% | Below 9% |

| Federal Student Loan | 5.5–7% | ~5.5–7% | Minimal | Federal rate |

Mortgage APR in 2026

The 30-year fixed mortgage is averaging 6.10–6.16% in interest rate terms but 6.38–6.55% APR once fees are counted. Before you sign, check how your APR affects your buying power with our Home Affordability Calculator.

If you are comparing lenders across states, our guide on lowest mortgage rates by state in 2026 shows you where rates run lowest — and why APR differences across states can exceed 0.5%.

Personal Loan APR in 2026

Personal loan APRs span a brutal 7% to 35.99% range. The average across all lenders is 12.16%, but credit unions average just 10.72%. Online lenders start lower (6.49%) but can go as high as 35.99%.

Key Warning: If a personal lender’s APR equals their interest rate, ask why. Either they charge zero fees (rare) or they are hiding costs elsewhere. Our dedicated guide on personal loan rates and traps in 2026 exposes the most common tricks.

Credit Card APR in 2026

Credit card APR averages ~19.7–22.83% as of February 2026. Unlike mortgages and personal loans, credit card APR typically equals the interest rate — because issuers cannot predict per-customer fees upfront.

2026 Fact: Americans are carrying $1.23 trillion in credit card debt. At 22% APR, a $5,000 balance with minimum payments costs $7,723 in interest over 23 years.

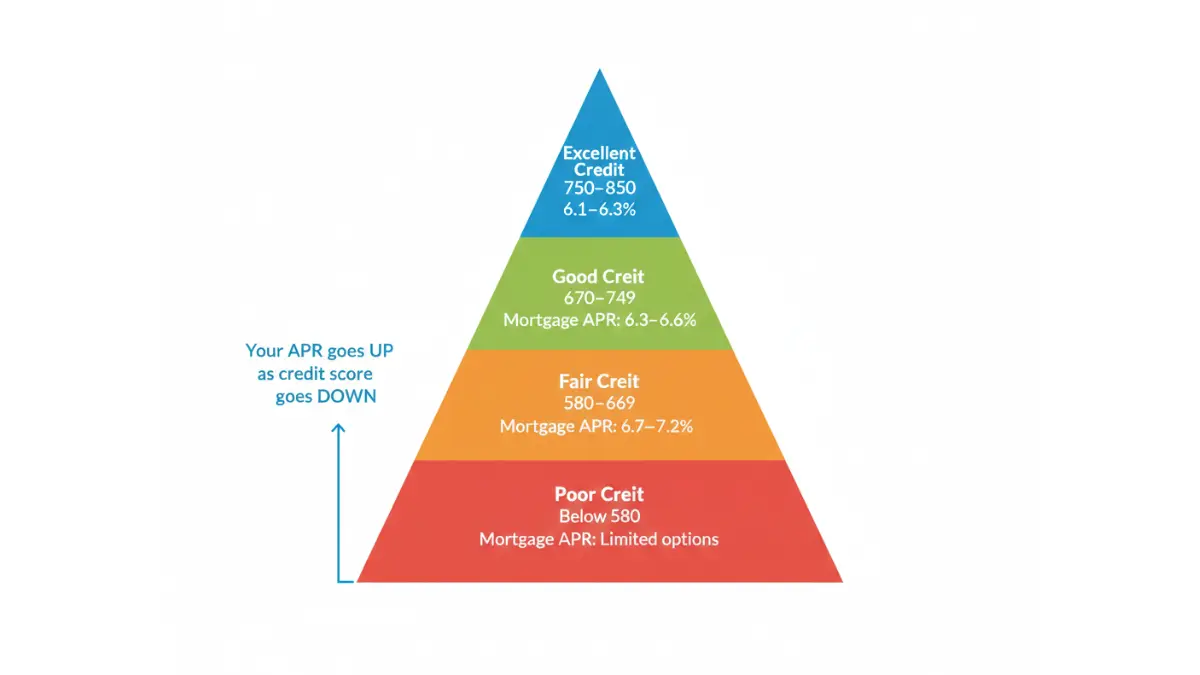

APR by Credit Score — 2026 Benchmark Table

This is what no competitor shows you. Your credit score is the single biggest factor controlling your APR:

| Credit Score Tier | FICO Range | Personal Loan APR | Mortgage APR | Credit Card APR |

|---|---|---|---|---|

| Excellent | 750–850 | 7%–11% | 6.1%–6.3% | 17%–20% |

| Good | 670–749 | 11%–17% | 6.3%–6.6% | 20%–24% |

| Fair | 580–669 | 17%–25% | 6.7%–7.2% | 24%–28% |

| Poor | Below 580 | 25%–35.99% | Limited options | 28%–36% |

What This Means For You: Moving from “Fair” to “Good” credit can cut your mortgage APR by 0.5–1%, saving $20,000–$40,000 over a 30-year loan. Improving your credit score before you borrow is the highest-ROI financial move available. Read our Credit Score Complete Guide to learn exactly how.

Fixed APR vs Variable APR + How APR Is Calculated

Fixed APR: Stability in a Volatile Market

A fixed APR stays the same for the life of the loan. Your monthly payment never changes. In a 2026 environment where the Fed is still navigating inflation and rate uncertainty, fixed APR gives you predictability.

Best for: 30-year mortgages, personal loans, auto loans where you want payment stability.

Variable APR: The 2026 Risk You Need to Understand

A variable APR fluctuates with a benchmark index — typically the Prime Rate or SOFR. When the Fed raises rates, your APR rises. When they cut, it falls.

Right now, with the Fed holding steady at 3.50–3.75% and further cuts uncertain, variable APRs carry meaningful risk for long-term borrowers. Before refinancing a variable-rate product, run the numbers with our Mortgage Refinance Calculator first.

Fixed vs Variable APR: Quick Comparison

| Feature | Fixed APR | Variable APR |

|---|---|---|

| Rate changes? | ❌ Never | ✅ Yes, with Fed/index |

| Better when rates rise? | ✅ Yes | ❌ No |

| Better when rates fall? | ❌ Miss the drop | ✅ Yes |

| Predictability | High | Low |

| Best for | Long-term loans | Short-term borrowing |

How Is APR Calculated? (Step-by-Step)

APR is not magic — it follows a formula. Here is how lenders calculate it:

- Start with your interest rate (e.g., 6.10%)

- Add all mandatory fees charged by the lender (origination, broker, points, PMI)

- Spread those fees across the loan term as an annualized cost

- Combine both into a single yearly percentage = your APR

Real Example:

- Loan amount: $300,000

- Interest rate: 6.10%

- Lender fees: $4,200 (origination + points)

- Loan term: 30 years

- Resulting APR: ~6.38%

That 0.28% APR gap equals $4,200 paid upfront — money that would have stayed in your pocket at a zero-fee lender. Use our Debt Consolidation Calculator to model how switching to a lower-APR product reshapes your total debt cost.

What This Means For You: Two lenders can quote the same 6.10% rate and charge wildly different APRs depending on their fee structure. Always request the APR — not just the interest rate — in writing before proceeding.

How to Use APR to Stop Overpaying — Your 2026 Action Playbook

Step-by-Step: Compare Two Loan Offers Using APR

Here is a real example that exposes the trap most borrowers fall into:

| Lender A | Lender B | |

|---|---|---|

| Interest Rate | 5.90% | 6.10% |

| Lender Fees | $6,500 | $0 |

| APR | 6.38% | 6.10% |

| Total Cost Over 5 Years | Higher ❌ | Lower ✅ |

Lender A looks cheaper because of the lower advertised rate. But Lender B’s zero-fee structure makes its APR — and total cost — significantly lower. Over a 5-year period, Lender B saves you roughly $3,800–$5,200 depending on loan size.

This is exactly what the CFPB’s loan comparison guidance instructs borrowers to do: compare APRs, not interest rates.

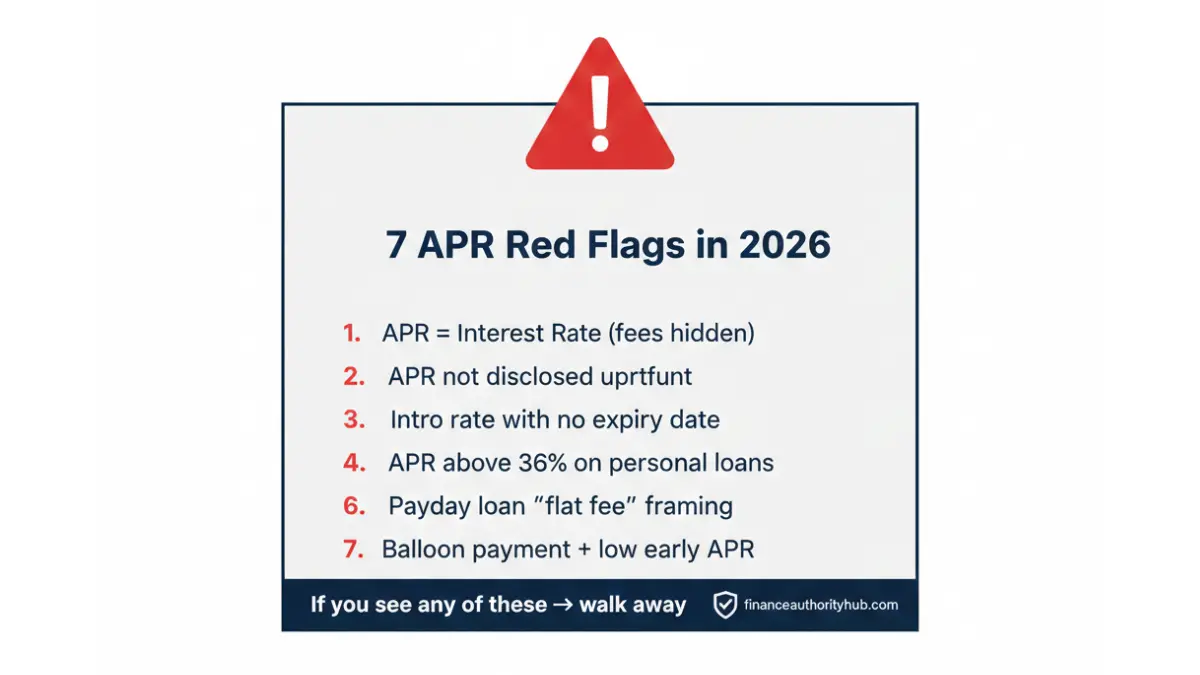

Red Flag APRs: 7 Warning Signs of a Predatory Lender

No competitor covers this. Know these before you sign anything:

- APR equals the interest rate — but fees exist in the fine print under different names

- APR not disclosed until signing — TILA requires upfront disclosure; refusal is illegal

- “Special introductory” APR with no clear expiry date or reversion rate

- APR above 36% on a personal or installment loan — the threshold consumer advocates call unaffordable

- Payday loan APR — these routinely run 300%–400% APR when annualized; see the full breakdown in our Payday Loan Trap guide

- Dealer-inflated auto APRs — dealers can mark up your rate and pocket the difference

- Balloon payment structures hiding a low early APR that spikes on the final payment

How to Negotiate a Lower APR (What Lenders Don’t Tell You)

Lenders do not advertise this — but APR is negotiable more often than borrowers realize:

- Get pre-qualified with at least 3 lenders before committing. Competition forces lower offers.

- Use competing offers as leverage. Show Lender A that Lender B quoted you 0.5% lower APR.

- Ask for a fee waiver on origination fees — many lenders will remove or reduce them for strong borrowers.

- Improve your credit score first. Even 20–30 FICO points can drop your APR by 0.5–1.5%.

- Pay discount points strategically — only if you plan to hold the loan long enough to break even.

What This Means For You: On a $350,000 mortgage, negotiating just 0.5% off your APR saves $1,750 per year — and $52,500 over 30 years. It takes one phone call to get a competing quote. Make it.

APR Traps to Avoid in 2026

| Trap | How It Works | How to Avoid It |

|---|---|---|

| 0% Intro APR expiry | Rate jumps to 20%+ after 12–21 months | Pay off full balance before period ends |

| Dealer auto loan markup | Dealer inflates your rate; pockets difference | Get pre-approved at your bank/credit union first |

| Payday “fee” framing | Flat fee looks small; annualizes to 400%+ APR | Always ask for the annualized APR |

| ARM resets | Low intro APR resets higher after 5–7 years | Model worst-case with refinance calculator |

If you are carrying high-interest debt at a punishing APR, consolidating may significantly cut your total cost. Calculate your potential savings now using our Debt Consolidation Calculator.

Credit Card APR in 2026 — The Rules Are Different

Why Credit Card APR Equals the Interest Rate

Unlike mortgages and personal loans, credit card APR and interest rate are the same number. Credit card issuers cannot bundle upfront fees into APR because they cannot predict which fees each customer will trigger.

This means comparing credit card APRs is straightforward — no hidden fee gap to decode.

The Three Credit Card APRs You Must Know

Most cardholders only know their purchase APR. There are actually three:

| APR Type | Average in 2026 | When It Applies |

|---|---|---|

| Purchase APR | 19.7%–22.83% | Balances not paid in full monthly |

| Balance Transfer APR | 0% intro → then 18–29% | On transferred balances from other cards |

| Cash Advance APR | 25%–30% | Immediate; no grace period |

Critical 2026 Warning: The cash advance APR starts accruing interest immediately — there is no grace period. At 28% APR, a $1,000 cash advance costs you $280 in interest within 12 months even if you make payments.

Intro 0% APR Cards: Use Them Right or Pay the Price

A 0% intro APR card can be a powerful debt payoff tool — but only when used correctly. If you carry a balance past the promotional period, your remaining balance often retroactively accrues interest at the full APR.

The rule: Only use a 0% intro APR offer if you have a concrete plan to pay the full balance before the promotional period ends. Our guide on 0% APR credit cards for eliminating up to $8,000 in debt shows you exactly which cards offer the longest windows and how to maximize them.

If you’re struggling with credit card debt at a high APR, the Credit Card Debt Escape Strategies guide walks through the fastest proven paths to zero.

APR vs Interest Rate — 11 Most-Asked Questions Answered

Q1: What is the difference between APR and interest rate?

The interest rate is the basic cost of borrowing the principal. APR is the interest rate plus all mandatory lender fees, expressed as an annual percentage. APR is always higher — and always the more accurate cost comparison tool.

Q2: Why is APR higher than the interest rate?

Because APR includes fees the interest rate ignores — origination charges, broker fees, discount points, and mortgage insurance. The more fees a lender charges, the bigger the gap between rate and APR.

Q3: Does APR affect my monthly payment?

No. Your monthly payment is calculated using the interest rate, not the APR. APR reflects total loan cost over time — it is a comparison tool, not a payment driver.

Q4: What is a good APR for a mortgage in 2026?

With 30-year mortgage rates averaging 6.10–6.16% in February 2026, a good APR is anything below 6.5%. Borrowers with 750+ credit scores should target below 6.3% APR. See our 15 vs 30-Year Mortgage Comparison to find which term gives you the best total APR outcome.

Q5: What is a good APR for a personal loan in 2026?

The average personal loan APR is 12.16% across all lenders. A good APR is anything below 12% for borrowers with good credit. If you are quoted above 20%, consider improving your credit score or applying at a credit union, which caps APRs at 18% for federal members.

Q6: What is a good APR for a credit card in 2026?

The national average is approximately 19.7–22.83% APR. Excellent credit borrowers (750+) can qualify for 17–20% APR. Anything below 20% is considered strong in today’s market.

Q7: Is a lower APR always better?

Usually — but not always. A loan with a lower APR but high upfront fees may cost more than a slightly higher-APR loan with zero fees, especially if you plan to pay the loan off early or refinance within a few years. Always model both scenarios.

Q8: How do I lower my APR?

– Improve your credit score before applying (biggest single factor)

– Shop and compare at least 3 lenders for competing APR quotes

– Negotiate origination fees directly with the lender

– Apply with a co-signer with stronger credit

– Consider a shorter loan term (lenders often offer lower APRs)

Q9: What is the difference between APR and APY?

APR (annual percentage rate) is the rate you pay to borrow money. APY (annual percentage yield) is the rate you earn on savings, accounting for compound interest. APR is relevant for loans; APY is relevant for savings accounts and CDs. Our guide on banks offering 5% APY with zero fees shows where you can maximize your savings yield in 2026.

Q10: Does the Federal Reserve directly control APR?

Not directly. The Fed controls the federal funds rate, which influences — but does not set — consumer APRs. Mortgage APRs are more tied to 10-year Treasury yields. Credit card APRs follow the Prime Rate, which moves with the Fed. Personal loan APRs are driven heavily by lender credit risk models.

Q11: What is a 0% intro APR and is it worth it?

A 0% intro APR offer means you pay zero interest on purchases or balance transfers for a set period — typically 12 to 21 months. It is worth it if and only if you pay off the full balance before the promotional period expires. After expiry, rates typically jump to 19%–29% APR.

📌 Disclaimer: This article is for educational and informational purposes only and does not constitute financial, legal, or investment advice. APR rates and financial data cited reflect conditions as of February 2026 and are subject to change. Always consult a licensed financial advisor before making borrowing or lending decisions.

Sources: Consumer Financial Protection Bureau — APR vs Mortgage Rate | Federal Reserve H.15 Interest Rate Data | CFPB — APR vs Loan Rate

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.