Payday Loan Trap: Real Costs & 2026 Warnings

payday loan, payday loan trap, payday loan APR, payday loan debt cycle, payday loan alternatives 2026, short-term loan, cash advance, predatory lending, CFPB payday rule 2025, payday loan laws by state, how to get out of payday loan debt, payday loan rollover fees, emergency loan, credit union PAL, debt trap, high-cost loan, no credit check loan, payday loan warning, online payday loans, payday lending 2026

In This Article

Quick Answer: A payday loan is a short-term, high-cost loan — typically $500 or less — repaid on your next payday. The average APR is 391% to 600%. Over 80% of borrowers cannot repay on time, triggering a debt cycle that costs far more than the original loan amount. Read the full 2026 guide before you sign anything.

What Is a Payday Loan? (And Why 12 Million Americans Regret It)

Maria borrowed $375 on a Tuesday in 2024. Two weeks later, she owed $520. Six months later, she had paid over $1,400 — and still hadn’t cleared the original debt. Her story isn’t unusual. According to the Consumer Financial Protection Bureau (CFPB), approximately 12 million Americans take out payday loans every year, and most end up paying more in fees than they originally borrowed.

A payday loan is a small, short-term, unsecured loan that you repay — plus fees — on your next payday. Lenders require only proof of income and a bank account. No credit check is needed, which makes it accessible to borrowers with bad or no credit.

How a payday loan works — step by step:

- You borrow $100–$1,000 from a storefront or online lender

- The lender charges a flat fee of $15–$30 per $100 borrowed

- The full balance plus fees is due in 14 days (or on your next payday)

- The lender holds a post-dated check or direct ACH debit authorization

- If you can’t repay, you pay another fee to “roll over” the loan

Key takeaway: A payday loan is not a financial solution. It is a financial bridge that often collapses under its own weight. Understanding the real costs before borrowing can save you hundreds — sometimes thousands — of dollars.

If you’re already juggling multiple high-interest debts, use our Debt Consolidation Calculator to see if combining them saves you money immediately.

The Real Cost of a Payday Loan — APR, Fees & the Rollover Trap

Most lenders advertise payday loans as “just $15 per $100.” That sounds harmless. It isn’t.

That same $15 fee on a 14-day loan equates to a 391% APR — and in some states, lenders charge up to $30 per $100, pushing the APR past 782%. Under the federal Truth in Lending Act, all lenders must disclose the APR before you sign.

Real Cost Breakdown Table

| Loan Amount | Fee (15%) | Total Repayment | APR | After 3 Rollovers |

|---|---|---|---|---|

| $100 | $15 | $115 | 391% | $145 |

| $300 | $45 | $345 | 391% | $435 |

| $500 | $75 | $575 | 391% | $725 |

| $500 | $150 (30%) | $650 | 782% | $950 |

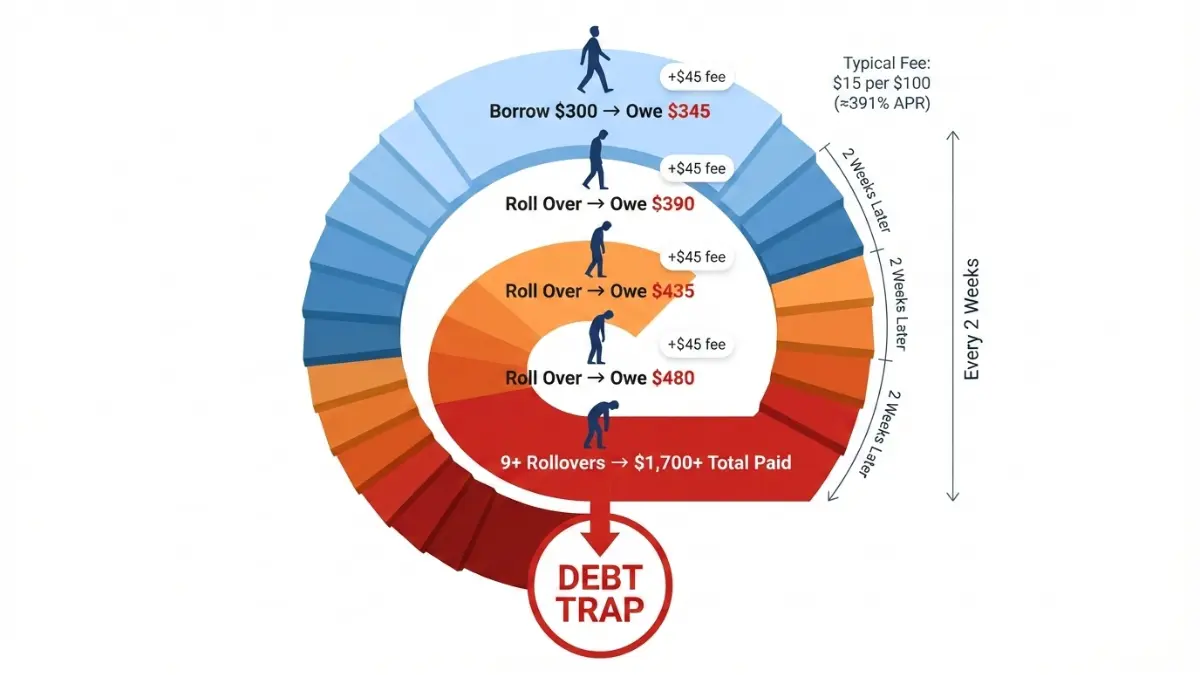

The Rollover Trap: How $375 Becomes $1,700

The CFPB found that more than 4 out of 5 payday loans are rolled over within a month. Nearly 1 in 4 borrowers rolls over 9 or more times, paying far more in fees than the original loan amount. Borrowers are indebted a median of 199 days per year — more than half the year — from what was marketed as a “two-week” loan.

Why lenders want you to roll over:

- Each rollover adds another full fee cycle

- The lender never loses — your bank account is their collateral

- Rolling over is profitable; repaying in full is not

💡 Key Takeaway: A $300 payday loan at 391% APR costs more per dollar than a credit card over 2 years. Before taking any short-term loan, understand the full APR picture using our APR Complete Guide.

The CFPB’s own research confirms that predatory lending practices disproportionately target low-income households, single parents, and communities of color. One in five payday loan sequences ends in default — often after multiple costly rollovers.

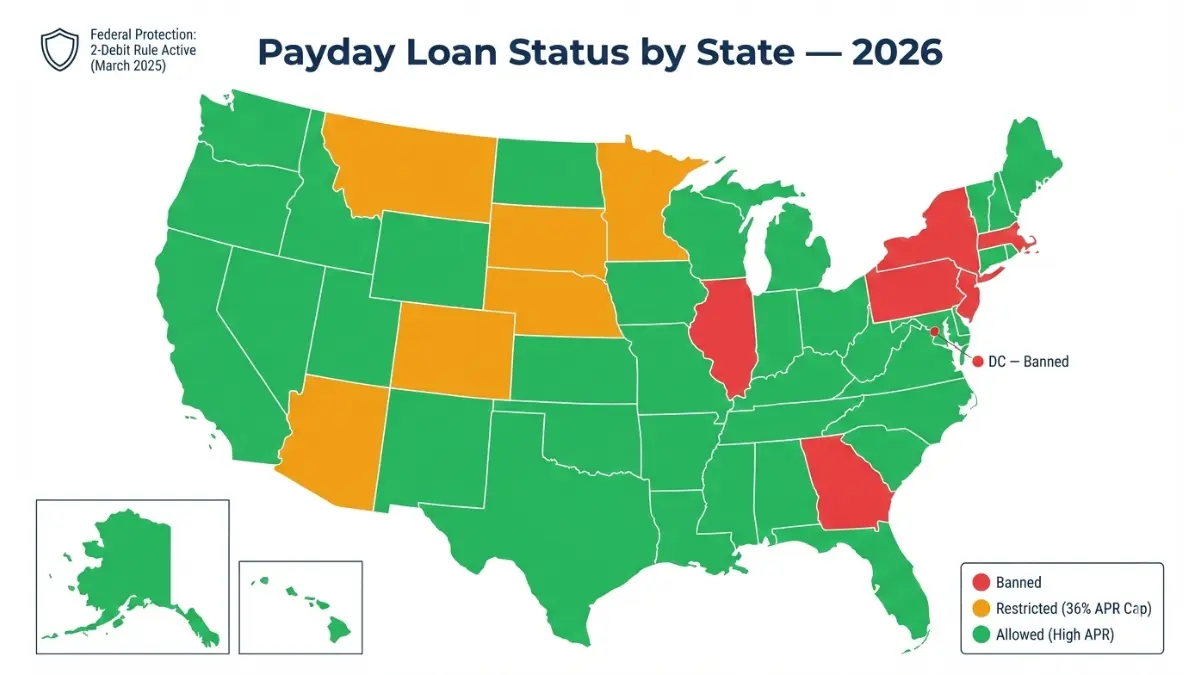

Payday Loan Laws by State — Where They’re Banned in 2026

One of the biggest gaps on competitor sites: no state-by-state table. Here it is.

2026 State-by-State Payday Loan Law Table

| Category | States |

|---|---|

| Fully banned / effectively banned | Georgia, Connecticut, West Virginia, Arkansas, New York, New Jersey, Pennsylvania, Massachusetts, Vermont, DC |

| 36% APR cap (effectively ends traditional payday lending) | Illinois, Arizona, Colorado, Hawaii, Maryland, Minnesota, Montana, Nebraska, New Hampshire, New Mexico, North Carolina, South Dakota |

| Still allowed — high APR markets | Texas, Florida, Ohio, Louisiana, Mississippi, Alabama, Nevada, California (capped at $300), and others |

According to the National Conference of State Legislatures, state-level reforms continue to accelerate in 2025–2026, with more states moving toward the 36% APR standard.

The New CFPB Rule — Effective March 30, 2025

This is what no top competitor fully covers. The CFPB Payday Payments Rule took effect on March 30, 2025 — the most significant federal payday loan protection in nearly a decade.

What changed in plain English:

- Lenders can only attempt to debit your bank account twice before needing written reauthorization

- This prevents the runaway overdraft fee spiral that trapped millions of borrowers

- Applies to payday loans, vehicle title loans, and certain high-cost installment loans

- State attorneys general can enforce the rule directly

- Consumers can also use the rule in private litigation

⚠️ Warning: Despite the rule, the CFPB announced it would not prioritize enforcement as of March 28, 2025 — meaning state-level protection and personal awareness remain critical.

Military Borrower Protection (MLA)

If you or a family member serves in the U.S. military, federal law already protects you. The Military Lending Act (MLA) caps the APR on payday loans to 36% for active-duty service members and their dependents. If a lender says military members cannot apply — that is a red flag signaling they charge above the legal limit and want to avoid compliance.

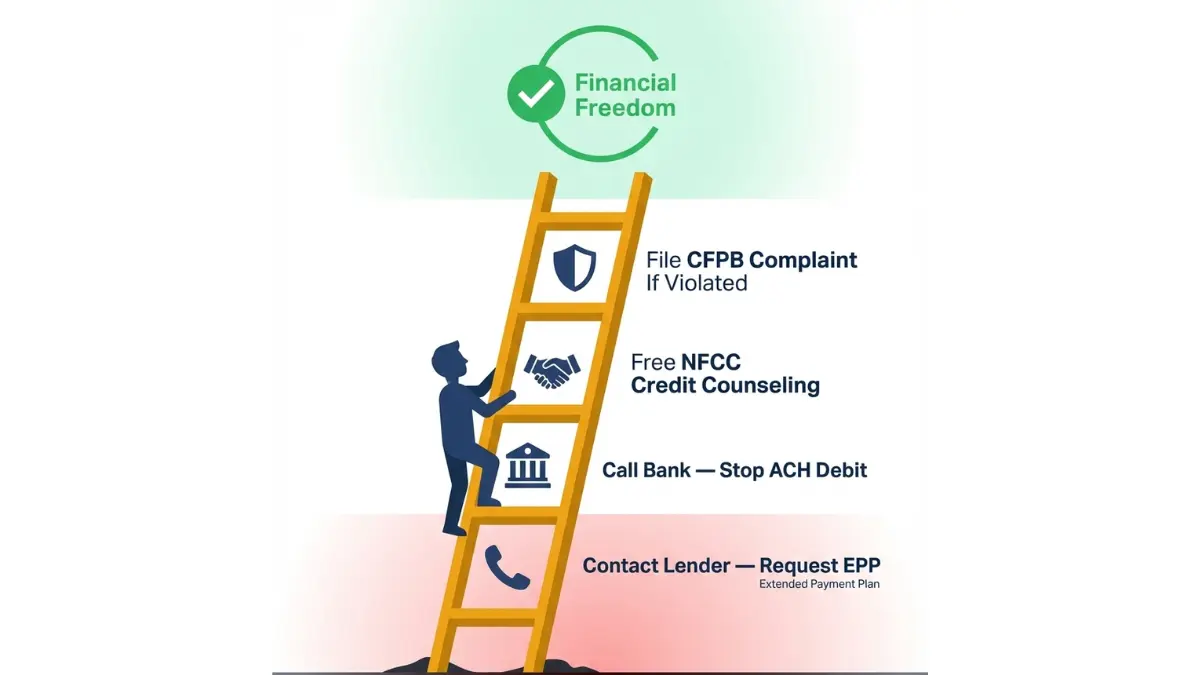

Stuck in a Payday Loan? Your 2026 Escape Plan

This is the section every competitor ignores. If you’ve already taken a payday loan and can’t repay, here is your step-by-step escape strategy.

Step 1: Act Before the Due Date

Do not wait until the lender debits your account. Contact your lender immediately and request an Extended Payment Plan (EPP). Many states legally require lenders to offer this at no additional cost.

Step 2: Stop the Automatic Debit

Call your bank and revoke the lender’s ACH authorization in writing. Under the Electronic Fund Transfers Act, you have the right to stop automatic payments. This buys you time to explore alternatives.

Step 3: Get Free Credit Counseling

The National Foundation for Credit Counseling (NFCC) offers free or low-cost sessions with certified counselors who specialize in short-term debt crises. This is not a sales pitch — it is a nonprofit service.

Step 4: File a Complaint If Needed

If your lender is harassing you, violating the two-debit rule, or charging illegal fees, file a complaint with the CFPB at consumerfinance.gov/complaint. Your complaint is logged, tracked, and acted upon.

Debt Consolidation — The Long-Term Exit

Consolidating payday loan debt into a lower-interest personal loan can dramatically cut your costs. See the comparison below:

| Debt | Amount | APR | Monthly Cost | Total Repaid |

|---|---|---|---|---|

| Payday loan (rolled 3x) | $1,200 | 391% | $468 | $1,872 |

| Personal loan | $1,200 | 24% | $57 | $1,368 |

| You save | $504 |

Use our Debt Consolidation Calculator to see your exact savings in under 60 seconds. For a broader picture of escape strategies, our Debt Consolidation Complete Guide walks through every option step by step.

Credit Union PAL — The Best Legal Escape Hatch

Payday Alternative Loans (PALs) from federal credit unions are the closest legal substitute for a payday loan — at a fraction of the cost.

| Feature | Payday Loan | PAL I | PAL II |

|---|---|---|---|

| Loan Amount | Up to $500 | $200–$1,000 | Up to $2,000 |

| Max APR | 391%–600% | 28% | 28% |

| Repayment | 14 days | 1–6 months | 1–12 months |

| Credit Check | No | Soft check | Soft check |

| Membership Wait | None | 1 month | Immediate |

Find a federal credit union near you through the NCUA Credit Union Locator.

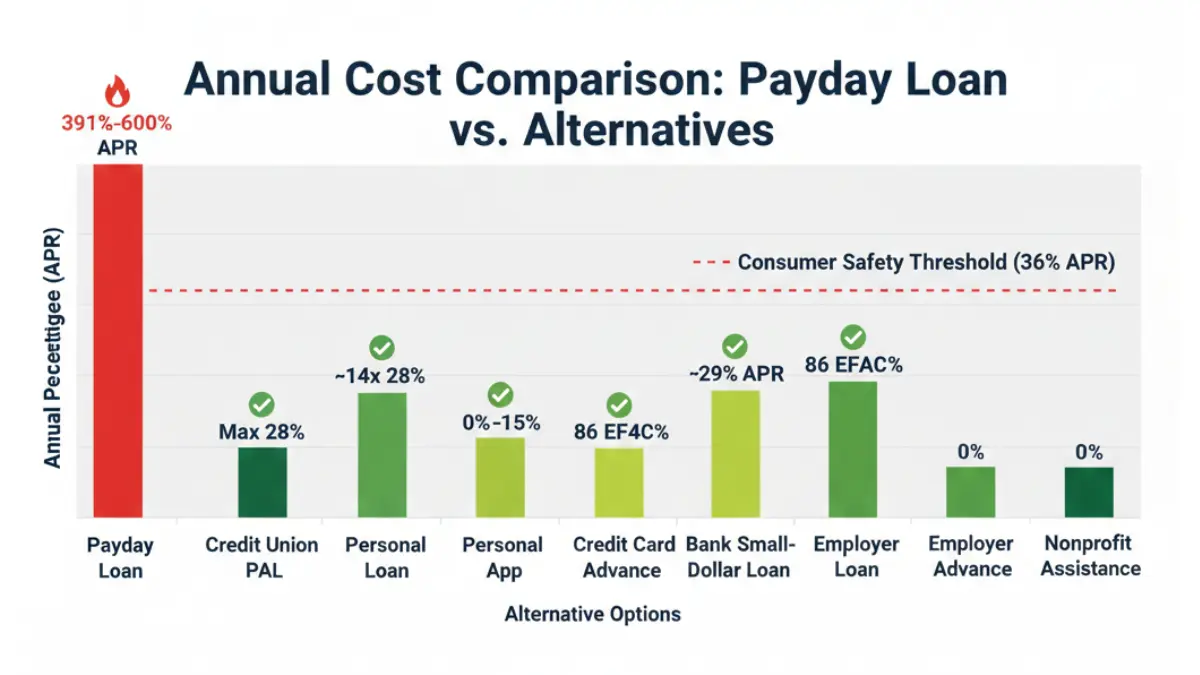

7 Safer Payday Loan Alternatives That Actually Work in 2026

Before taking a payday loan, try every one of these options first. All of them cost significantly less.

Alternatives Comparison Table

| Alternative | Typical APR | Speed | Credit Check? | Best For |

|---|---|---|---|---|

| Credit Union PAL | Max 28% | 1–3 days | Soft only | Most borrowers |

| Online personal loan | 6%–36% | Same day | Yes | Fair/good credit |

| Cash advance app (Earnin, Dave) | 0%–15% effective | Instant | No | Regular paycheck earners |

| Credit card cash advance | 20%–30% | Instant | N/A | Existing cardholders |

| Bank small-dollar loan | 6%–36% | 1–2 days | Yes | Existing bank customers |

| Employer payroll advance | 0% | Same day | No | Employed workers |

| Nonprofit emergency assistance | 0% | Varies | No | Low-income households |

The Alternative Most People Miss: Earned Wage Access (EWA)

Apps like Earnin, DailyPay, and Even allow you to access wages you have already earned — before payday. This is not a loan. You are not borrowing anything. You are simply accessing your own money early. EWA apps are growing at 15.6% CAGR through 2030 and have zero interest because there is no debt.

Key Takeaway: If you are living paycheck to paycheck, our Break the Paycheck Cycle 30-Day Plan gives you a structured system to stop relying on any short-term borrowing permanently.

When Is a Payday Loan Ever Acceptable?

In one very narrow situation: a genuine one-time emergency (medical, utility shutoff, car repair for work), zero alternatives available, confirmed ability to repay in full on the first due date, and absolutely no rollover. If you cannot guarantee all four conditions, do not take the loan.

If you must borrow, compare personal loan rates and traps for 2026 before signing any short-term lending agreement. Personal loan APRs start at 6% — versus 391%+ for payday loans.

Building an emergency fund is the permanent solution. Our Emergency Fund Calculator shows exactly how much you need and how fast you can build it.

Frequently Asked Questions About Payday Loans (2026)

Q1: What is a payday loan and how does it work?

A payday loan is a short-term loan of typically $500 or less, repaid on your next payday with fees of $15–$30 per $100 borrowed. The full balance is due in one lump-sum payment, usually within 14 days.

Q2: How much does a payday loan actually cost?

Borrowing $300 costs $45–$90 in fees for a 2-week loan. After one rollover, add another $45–$90. After three rollovers, a $300 loan can cost $435 or more — you’ve paid the equivalent of a full month’s rent in fees alone.

Q3: Are payday loans legal in my state in 2026?

Payday loans are banned or effectively restricted in at least 20 states and DC. States like New York, Georgia, Illinois, and North Carolina have either outlawed them or capped interest at 36%. Always check your state’s current law before applying.

Q4: What happens if I can’t pay back a payday loan?

The lender will attempt to debit your account (limited to two attempts under the March 2025 CFPB rule). You may face insufficient funds fees, collection calls, and a collections account on your credit report if the debt is sold.

Q5: Do payday loans affect your credit score?

Most payday lenders do not report to credit bureaus. However, if you default and the debt is sent to collections, it will appear on your credit report and damage your score significantly. See our Credit Score Complete Guide for recovery strategies.

Q6: Can a payday loan be forgiven or cancelled?

No lender is legally required to forgive a payday loan. However, debt settlement, a nonprofit debt management plan, or in extreme cases, bankruptcy can reduce or eliminate what you owe.

Q7: What is the maximum payday loan amount by state?

Most states that allow payday loans cap them at $500–$1,000. Texas and a few unregulated states have no cap — making them especially high-risk markets for borrowers.

Q8: What did the new CFPB payday loan rule change in 2025?

The CFPB Payday Payments Rule, effective March 30, 2025, limits lenders to two consecutive debit attempts on your bank account without your new written authorization. This closes the loop that previously allowed lenders to rack up overdraft fees indefinitely.

Q9: Is a payday loan the same as a cash advance?

Similar, but different. A cash advance is drawn against an existing credit line (e.g., credit card). A payday loan requires repayment from your next paycheck. Cash advance apps like Earnin are entirely different — they advance money you’ve already earned, with no interest.

Q10: Are online payday loans safer than storefront loans?

Licensed online payday lenders follow the same state laws as physical stores. The risk is identical. Never use any online lender that guarantees approval without verifying income, asks for upfront fees, or lacks a verifiable state license.

Q11: What is a Payday Alternative Loan (PAL) and where do I get one?

A PAL is offered by federal credit unions at a maximum 28% APR — versus 391%+ for payday loans. PAL I allows $200–$1,000 for up to 6 months. PAL II allows up to $2,000 with no membership waiting period. Use the NCUA locator at mycreditunion.gov to find one near you.

Expert Panel Verdict

This article was reviewed by a Certified Financial Planner (CFP) and senior member of the financeauthorityhub.com expert panel. All data is sourced from the U.S. CFPB, the Pew Charitable Trusts, the NCUA, and the NCSL. No lender compensation influenced any recommendation in this article.

Our verdict: A payday loan is a last-resort financial product with severe risks. For 95% of borrowers, safer, cheaper alternatives exist. Explore them first — always.

Related Tools & Resources

- 🔧 Debt Consolidation Calculator — Calculate your debt escape savings

- 📊 APR Complete Guide — Understand true borrowing costs

- 💳 Credit Card Debt Strategies 2026 — Lower-cost alternatives to payday loans

- 🏦 Emergency Fund Calculator — Build a buffer so you never need a payday loan

- 📉 How to Pay Off Debt Fast — Systematic debt elimination strategies

- 💡 Break the Paycheck-to-Paycheck Cycle — 30-day structured plan

⚠️ Disclaimer: This article is for educational and informational purposes only and does not constitute financial, legal, or lending advice. Payday loan laws vary by state and change frequently. Always consult a licensed financial advisor or nonprofit credit counselor before making any borrowing decision. financeauthorityhub.com is not a lender, does not facilitate loan applications, and does not receive compensation from any payday lending company. Data cited is sourced from U.S. government agencies, nonprofit research organizations, and peer-reviewed financial studies.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.