Personal Loans: Rates, Traps & Top Picks 2026

Average personal loan rate is 12.27% in 2026 — but hidden fees & traps cost borrowers thousands. Expert-vetted picks, real rate tiers by credit score & 5 traps to avoid before you sign.

In This Article

⚡ Quick Answer (60 seconds): A personal loan is an unsecured installment loan repaid in fixed monthly payments over 2–7 years. The average personal loan rate is 12.27% APR as of February 2026. Best available: 6.49% APR for excellent-credit borrowers. But the rate is only half the story — hidden origination fees, term traps, and APR confusion cost American borrowers thousands every year. Here’s everything you need to know before you apply.

What Is a Personal Loan? (The 60-Second Answer)

A personal loan is a lump-sum installment loan from a bank, credit union, or online lender. You receive a fixed amount, then repay it — principal plus interest — in equal monthly payments over a set loan term. Most personal loans are unsecured, meaning no collateral is required. Lenders use your credit score, income, and debt load to approve you and set your rate.

Personal loans are one of the most versatile financial products available. Unlike a car loan or mortgage, you can use the funds for almost any lawful purpose. As of Q3 2025, according to LendingTree’s 2026 personal loan statistics, 25.9 million Americans carry an active personal loan — with total outstanding debt hitting $269 billion, the highest level ever recorded.

Secured vs. Unsecured Personal Loans

- Unsecured personal loans — No collateral. Approval based purely on creditworthiness. The most common type for debt consolidation and large purchases.

- Secured personal loans — Backed by an asset (savings account, car). Lower rates, but you risk losing the asset if you default.

- Fixed-rate loans — Same monthly payment for the entire loan term. Over 95% of personal loans are fixed-rate — predictable, budget-friendly.

- Variable-rate loans — Rate moves with the market. Rare for personal loans. Avoid unless terms clearly favor you.

Personal Loan Fast Facts Table

| Feature | Typical Range |

|---|---|

| Loan Amounts | $1,000 – $250,000 |

| Loan Terms | 2 – 7 years |

| APR Range (Feb 2026) | 6.49% – 35.99% |

| Funding Speed | Same day – 5 business days |

| Minimum Credit Score | 560–680 (varies by lender) |

Top Reasons Americans Take Personal Loans (Q3 2025)

- 51% — Debt consolidation or credit card refinancing (#1 use case by far)

- 9.5% — Everyday bills and living expenses

- 6.9% — Home improvement projects

- Remainder — Weddings, medical expenses, major purchases, emergencies

💡 Expert Tip: If you’re consolidating high-interest credit card debt, a personal loan is one of the smartest financial moves in 2026. Use our Debt Consolidation Calculator to see your exact interest savings — most borrowers discover $3,000–$8,000 in total savings.

Personal Loan Interest Rates in 2026 — Real Numbers

Understanding current personal loan interest rates is the most critical step before applying. The APR range is enormous — from 6.49% to 35.99% — and the difference between those two ends can mean paying thousands of dollars more on the exact same loan amount.

Current Average Rates — February 2026

According to Credible marketplace data for the week ending February 8, 2026:

- 3-year personal loan average: 13.44% APR (down from 15.29% one year ago)

- 5-year personal loan average: 18.11% APR (down from 19.93% one year ago)

- Best available rate: 6.49% APR (LightStream, excellent-credit borrowers only)

- National average: 12.27% APR (Bankrate Monitor, Feb 4, 2026 — for 700 FICO, $5,000 loan, 3-year term)

Personal Loan Rates by Credit Score Tier

| Credit Score | Tier | Expected APR Range | Best Strategy |

|---|---|---|---|

| 800+ | Excellent | 6.49% – 11% | Target LightStream, SoFi, Discover |

| 740–799 | Very Good | 10% – 16% | Prequalify with 3+ lenders, compare APR |

| 670–739 | Good | 14% – 22% | Credit unions often beat online lenders |

| 580–669 | Fair | 20% – 30% | Add a co-borrower to lower rate |

| Below 580 | Poor | 28% – 36%+ | Improve score first; try Upgrade or Universal Credit |

What the Fed Rate Hold Means for Borrowers Right Now

The Federal Reserve held the funds rate steady at 3.50–3.75% at its January 2026 meeting, following three consecutive quarter-point cuts in late 2025. Historical data from the Federal Reserve FRED database shows personal loan rates typically lag Fed decisions by several months.

What this means for you: Don’t wait for dramatic rate drops — rates are already 1–2 percentage points lower than one year ago. The smartest move is to improve your credit score now to qualify for a lower rate tier, rather than waiting for the market.

Bank vs. Fintech vs. Credit Union — Who Wins on Rate?

| Lender Type | Avg. Rate Range | Best For | Watch Out For |

|---|---|---|---|

| Online Fintech | 8% – 36% | Speed (same-day funding) | Origination fees 1–10% |

| Banks | 9% – 25% | Existing customers (relationship discounts) | Slower approval (3–5 days) |

| Credit Unions | 7.99% – 18% | Lowest rates; legally capped at 18% | Membership requirement |

Credit unions lead on rate. NCUA Q3 2025 data shows the national 3-year credit union average was 10.72% APR — over 2 full percentage points below the bank average. Online lenders now serve 48.6% of all personal loan borrowers, according to TransUnion.

For a deeper look at how debt load affects your overall financial picture, see our guide on Debt Consolidation: Save $3,500.

5 Personal Loan Traps That Cost Borrowers Thousands

Every top competitor tells you which personal loans to get. None of them warn you what happens after you click apply. These five traps are responsible for most of the money American borrowers unnecessarily lose on personal loans every year.

Trap 1: The Origination Fee Silent Killer

Origination fees range from 1% to 10% of your loan amount — charged before you receive a single dollar. On a $20,000 loan with a 5% origination fee:

- You receive $19,000

- You pay interest on the full $20,000

- Your effective APR jumps immediately — but the advertised headline rate won’t show this

🚨 Real Math: $20,000 loan | 5% origination fee → You receive $19,000 | Interest still calculated on $20,000 | Effective APR rises from 9% to ~9.5% before you make a single payment.

Action step: Always compare APR — not the interest rate. APR includes all fees. The CFPB’s guide to credit reports and scores explains exactly how APR disclosure works and what lenders are legally required to show you.

Trap 2: Comparing Interest Rate Instead of APR

A lender advertising 6.5% interest rate + 5% origination fee can cost more in total than a lender advertising 8% interest rate + zero fees. These two loans look completely different at first glance — but only APR tells you the real total cost.

- Action step: Request APR quotes from at least 3 lenders before choosing. Our APR Complete Guide 2026 breaks down exactly what APR means in real dollar terms.

Trap 3: The Long-Term Monthly Payment Illusion

Lenders push longer loan terms because lower monthly payments feel more affordable. But the total interest cost explodes.

| Loan Term | Monthly Payment | Total Interest Paid | Total Cost |

|---|---|---|---|

| 3 years (36 months) | $513/month | $1,472 | $16,472 ✅ |

| 5 years (60 months) | $349/month | $5,933 | $20,933 ❌ (+$4,461 more) |

| 7 years (84 months) | $271/month | $7,741 | $22,741 ❌ (+$6,269 more) |

Example: $15,000 loan at 14% APR. FinanceAuthorityHub calculations.

Action step: Before signing anything, use our Debt Consolidation Calculator to calculate your actual total cost across different loan terms.

Trap 4: Prepayment Penalties — Paying Extra to Pay Less

Some lenders charge a prepayment penalty if you pay off your loan early. A 2% early payoff fee on a $30,000 loan costs $600 — wiping out a significant portion of your interest savings. Look for the terms “prepayment fee,” “early payoff fee,” or “early termination charge” buried in your loan agreement.

- Action step: Only choose lenders that explicitly state “no prepayment penalty” in writing. LightStream, SoFi, and Discover all offer prepayment-penalty-free loans.

Trap 5: The Variable Rate Disguised as a Low Rate

Some fintech lenders advertise an attractive introductory rate that is actually variable and tied to market benchmarks. Unlike a fixed-rate personal loan, your monthly payment can rise if rates increase — destroying your budget planning.

- Action step: Confirm “fixed rate” in writing before signing. Fixed-rate personal loans make up 95%+ of the market for good reason: predictability protects your monthly budget.

🛡️ Expert Panel Warning: “Borrowers who focus only on the monthly payment — rather than total cost and all fees — consistently overpay by $2,000–$6,000 on standard personal loans. APR is your single most important comparison tool.” — FinanceAuthorityHub Expert Panel

Best Personal Loans of 2026 — Expert-Vetted Picks

Our expert panel reviewed lenders across 60+ data points including APR range, fee structure, credit requirements, funding speed, and borrower protections. Here are the top personal loans for 2026, organized by borrower need.

Quick Comparison: Top Personal Loans 2026

| Lender | Best For | APR Range | Min. Credit Score | Origination Fee |

|---|---|---|---|---|

| LightStream | Excellent credit / large amounts | 6.49% – 25.99% | Good/Excellent | None |

| SoFi | No fees + job loss protection | 8.99% – 29.99% | 680 | Optional |

| Discover | No-fee loans, good credit | 7.99% – 24.99% | 660 | None |

| Upgrade | Fair credit / debt consolidation | 9.99% – 35.99% | 580 | 1.85% – 9.99% |

| PenFed CU | Lowest maximum rate (credit union) | 7.99% – 17.99% | 650 | None |

Best Personal Loans for Debt Consolidation

If your primary goal is debt consolidation, prioritize lenders that pay your creditors directly — removing the temptation to spend the funds elsewhere. SoFi and Upgrade both offer direct creditor payment. With 51% of borrowers using personal loans for debt consolidation, this is the highest-impact feature most comparison sites ignore.

See our complete strategy guide: How to Crush $30k of Debt in 12 Months.

Best Personal Loans for Bad Credit

Borrowers with scores below 620 should start with Upgrade (min. 580) and Universal Credit (min. 560). Expect APRs of 25%–35%. Prequalify first — it uses a soft credit check with zero score impact. Always check your free official credit report at AnnualCreditReport.com before applying.

Also see our Credit Score Complete Guide: How to Reach 800 to understand exactly how to move into a better rate tier.

Best for Same-Day Funding

LightStream and SoFi offer same-day funding if you apply and accept loan terms before 2:30 PM ET on a business day. Upgrade and Best Egg fund within 1 business day for most applicants. Always verify your bank account information upfront to avoid delays.

If you’re comparing personal loans against 0% APR credit cards, our guide to 0% APR Cards That Eliminate $8k of Debt in 16 Months explains exactly when a balance transfer beats a personal loan.

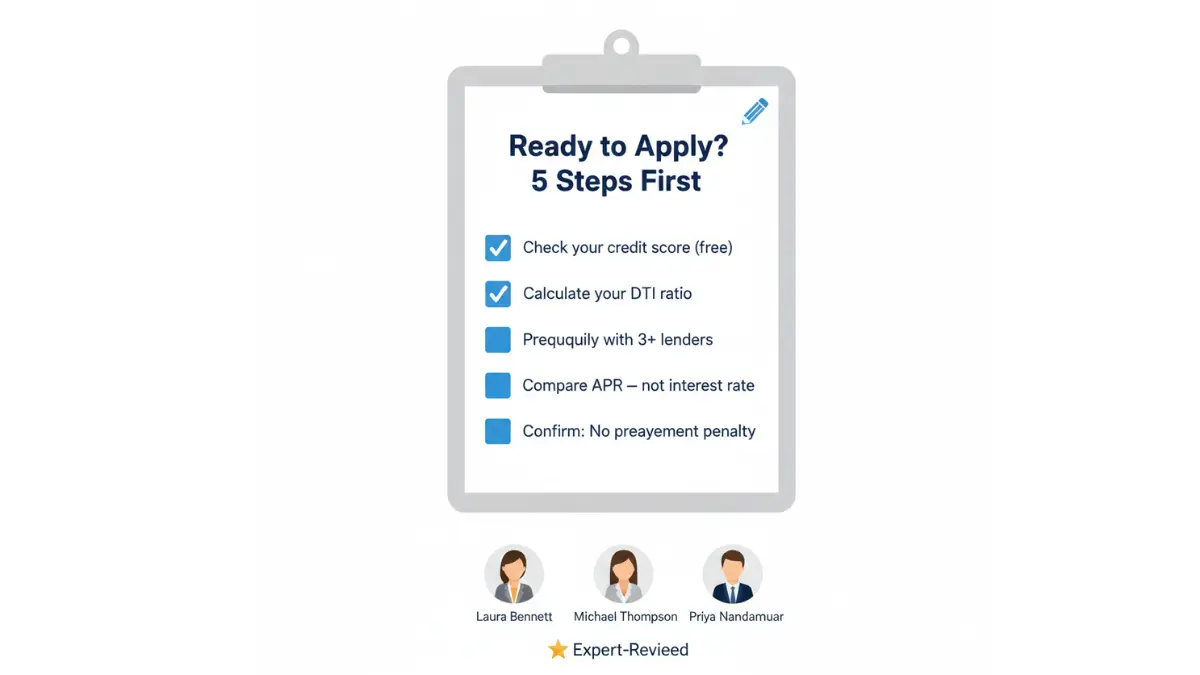

How to Get Approved for a Personal Loan at the Lowest Rate

Getting approved is only half the battle. Getting the lowest personal loan interest rate you actually qualify for requires preparation. Follow these five steps before submitting any application.

Step 1: Check Your Credit Score First (Free) Visit AnnualCreditReport.com — the only federally authorized source for free credit reports. Check all three bureaus (Equifax, Experian, TransUnion). Dispute any errors before applying. One inaccurate negative mark can cost you 2–5 percentage points on your rate.

Step 2: Calculate Your Debt-to-Income Ratio (DTI) Divide your total monthly debt payments by your gross monthly income. Most lenders want DTI below 40%. If yours is higher, pay down existing balances before applying. Our Home Affordability Calculator helps you model your full financial picture.

Step 3: Prequalify With 3+ Lenders (Soft Check Only) Prequalification triggers a soft inquiry — zero credit score impact. Compare APR (not interest rate), origination fee, total repayment cost, and whether a prepayment penalty applies. Never apply to just one lender.

Step 4: Choose the Shortest Term Your Budget Handles Shorter loan term = lower APR + dramatically less total interest. As the table in Section 3 shows, choosing 3 years over 5 years on a $15,000 loan saves over $4,400 in interest.

Step 5: Set Up Autopay Before Funding Most major lenders — SoFi, LightStream, Upgrade — offer 0.25%–0.50% APR discounts for enrolling in autopay. On a $20,000 loan, that single step saves $150–$300 over the loan life. Essentially free money.

Application Documents Checklist

| Document | Why It’s Required |

|---|---|

| Government-issued ID (passport / driver’s license) | Identity verification — legally required |

| Recent pay stubs (2–3 months) | Income verification |

| Federal tax returns (last 2 years) | Income consistency — especially for self-employed |

| Bank statements (2–3 months) | Asset and cash flow verification |

| Social Security Number | Credit check authorization |

| Employer name and contact info | Employment verification |

💡 Pro Move — Improve Your Score Before Applying: Moving from the “Good” tier (670–739) to “Very Good” (740+) can reduce your personal loan APR by 4–8 percentage points. On a $15,000 loan over 3 years, that saves $1,800–$3,600 in total interest. Even 30–60 days of focused credit improvement — paying down card balances below 30% utilization and disputing errors — can push your score over a threshold.

For the full credit improvement roadmap, see our Credit Score Guide: How to Reach 800.

When You Should NOT Get a Personal Loan in 2026

This is the section no competitor writes — because it doesn’t earn affiliate revenue. But it’s the section that builds genuine trust and delivers real value. A personal loan is a powerful tool, but it is not always the right one.

| Your Situation | Better Alternative | Why It Wins |

|---|---|---|

| Excellent credit, paying off credit cards | 0% APR balance transfer card | 0% interest for 12–21 months — unbeatable if you clear the balance in time |

| Home improvement project, you own your home | Home Equity Loan / HELOC | Rates of 6–9% secured against equity — significantly lower than unsecured personal loans |

| Medical bills from a hospital | Hospital payment plan | Most hospitals offer 0% internal financing — always ask before you borrow |

| Small short-term need under $1,500 | Paycheck advance app | No interest; free short-term bridge if used responsibly |

Personal Loan vs. Credit Card — The Real 2026 Comparison

The average credit card APR is 23.96% as of December 2025 — nearly double the average personal loan rate of 12.27%. For most borrowers carrying revolving credit card debt, a personal loan for debt consolidation is the smartest financial move available right now.

The one exception: if you qualify for a 0% APR credit card and can realistically pay off the full balance within the promotional period, the 0% card wins every single time.

To explore home equity as a higher-value alternative for large borrowing needs, see our Home Equity: 4 Ways to Use It in 2026 guide.

Personal Loans FAQ: 11 Expert Answers (2026)

Q1. What is a good personal loan interest rate in 2026?

Anything below the national average of 12.27% APR is competitive. Borrowers with a credit score of 750+ should target 10% or below. Excellent-credit borrowers can qualify for rates as low as 6.49% from LightStream.

Q2. How fast can I get a personal loan?

LightStream and SoFi offer same-day funding if you apply and accept terms before 2:30 PM ET. Most online lenders disburse within 24–48 hours. Banks typically take 3–5 business days.

Q3. What credit score do I need for a personal loan?

Most lenders require a minimum FICO score of 580–640. For the best personal loan rates, target 720 or above. Some credit unions approve members with scores as low as 560.

Q4. Does applying for a personal loan hurt my credit score?

Prequalifying uses a soft inquiry — no score impact at all. A formal application triggers a hard inquiry, typically reducing your score by 2–5 points temporarily. Multiple applications within 14–45 days are usually counted as a single inquiry by FICO scoring models.

Q5. What is an origination fee on a personal loan?

An upfront charge of 1%–10% deducted from your loan amount before disbursement. On a $10,000 loan with a 5% origination fee, you receive $9,500 but pay interest on $10,000. Always compare APR — it includes origination fees in the cost calculation.

Q6. Can I get a personal loan with bad credit?

Yes. Upgrade and Universal Credit approve borrowers with scores as low as 560–580. Expect APRs of 25%–35%. A co-borrower with good credit significantly reduces your rate. Also review our Credit Card Debt Escape Strategies 2026 for parallel debt management steps.

Q7. What’s the difference between APR and interest rate?

The interest rate is the base borrowing cost. APR (Annual Percentage Rate) includes the interest rate plus all fees — origination, processing, and any other lender charges. APR is the only true apples-to-apples comparison metric. Always compare APR — never just the interest rate.

Q8. How much can I borrow with a personal loan?

Loan amounts range from $1,000 to $100,000 with most mainstream lenders. Some lenders like BHG Money offer up to $250,000 for well-qualified borrowers. The approved amount depends on your income, credit score, and DTI ratio.

Q9. Are personal loan interest rates fixed or variable?

The vast majority are fixed-rate — your monthly payment stays identical for the entire loan term. Variable-rate personal loans exist but are rare. Always confirm “fixed rate” in writing before signing any loan agreement.

Q10. Is a personal loan better than a credit card for debt consolidation?

For most borrowers, yes. The average personal loan rate (12.27%) is nearly half the average credit card APR (23.96%). The only exception is a 0% APR balance transfer card — which beats any personal loan rate if you can pay off the full balance before the promotional period expires.

Q11. What happens if I miss a personal loan payment?

You’ll typically face a late fee of $15–$40 or 5% of the payment amount. Payments more than 30 days late are reported to credit bureaus and can significantly damage your FICO score. Contact your lender immediately if you anticipate missing a payment — most major lenders have hardship programs that can defer or restructure payments without credit damage.

⚖️ Disclaimer: This article is for educational and informational purposes only and does not constitute financial, legal, or investment advice. Personal loan rates, lender offerings, and regulations change frequently. Always verify current rates directly with lenders and consult a qualified financial advisor before making any borrowing decisions. FinanceAuthorityHub.com does not guarantee the accuracy of third-party data cited herein.

Article by the FinanceAuthorityHub Expert Panel — 30 credentialed financial advisors. Sources: Federal Reserve, CFPB, Credible, Bankrate Monitor, LendingTree, NCUA, TransUnion.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.