Financial Aid 2026: Get $40K+ Free (New Guide)

Discover how to secure $40,000+ in financial aid for college in 2026. Our expert guide covers Pell Grants, FAFSA deadlines, scholarships, state programs, and proven strategies to minimize costs.

In This Article

What Is Financial Aid? (Your Path to $40K+ Free Money)

Financial aid is money provided to students to cover college expenses without requiring immediate repayment in most cases. The typical undergraduate student receiving financial aid packages between $12,000 and $45,000 annually by combining federal grants, state programs, institutional scholarships, and work-study opportunities.

In the 2025-26 academic year, over 6.1 million students will receive Federal Pell Grants totaling more than $27 billion. When you add state grants, college scholarships, and other aid sources, the average package can exceed $40,000 for students who strategically apply to multiple programs.

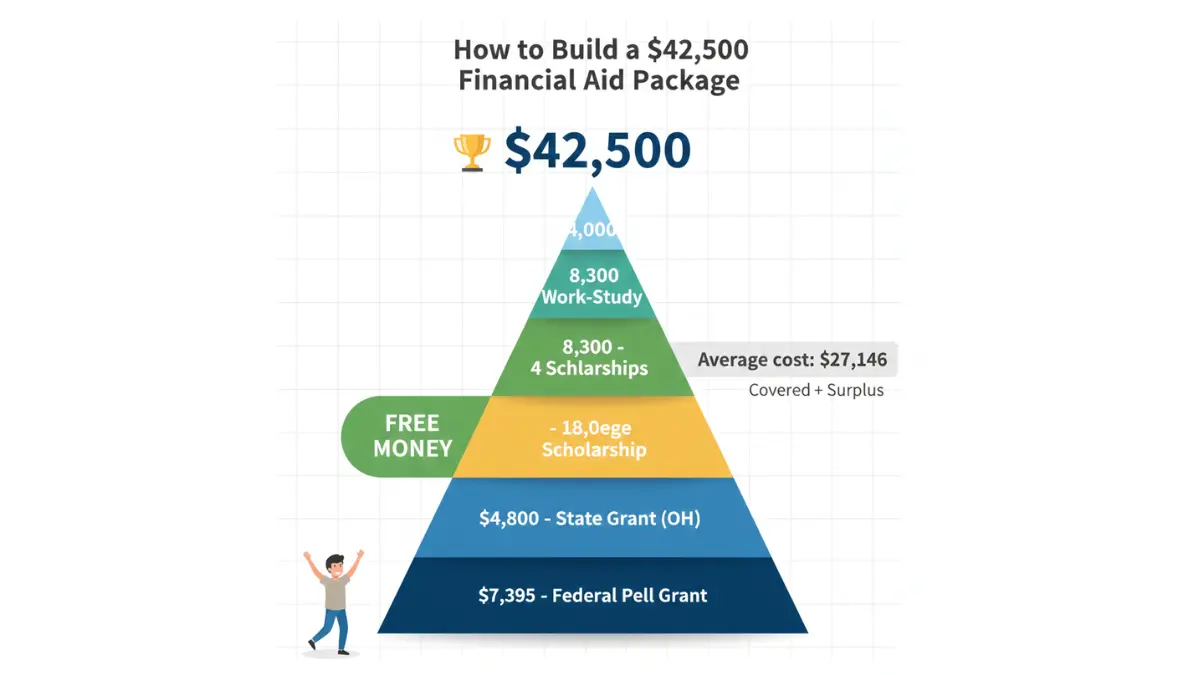

Sarah’s Real Success Story: A first-generation college student from Columbus, Ohio, secured $42,500 in financial aid for her freshman year at Ohio State University. Her package included a $7,395 Federal Pell Grant, $4,800 Ohio College Opportunity Grant, $18,000 institutional merit scholarship, $8,300 in private scholarships from four different organizations, and $4,000 in Federal Work-Study earnings. Sarah didn’t take out a single loan her first year.

Financial aid falls into four categories: grants (free money based on need), scholarships (free money based on merit or other criteria), work-study (part-time employment), and loans (borrowed money requiring repayment). The key to maximizing your aid package is understanding how to access all four types while prioritizing free money sources through the FAFSA 2026 new SAI Rules application process.

Critical 2026 Update: Starting July 1, 2026, new federal regulations will restrict Pell Grant eligibility for students enrolled less than half-time and those whose Student Aid Index exceeds twice the maximum grant amount. This makes timely application more urgent than ever for current high school juniors and college-bound students.

Financial Aid Types: Grants, Scholarships, Work-Study & Loans

Understanding each type of financial aid helps you build a strategic funding plan. Not all aid is created equal—prioritize free money before considering loans.

Federal Pell Grants: Up to $7,395 Free (2025-26)

The Federal Pell Grant represents the foundation of federal student aid and never requires repayment. For the 2025-26 award year (July 1, 2025 through June 30, 2026), the maximum award is $7,395 for eligible undergraduate students enrolled full-time.

Pell Grant eligibility is determined by your Student Aid Index (SAI), which ranges from -$1,500 to approximately $14,790 for calculated awards. Students qualify for maximum Pell Grants when family income falls below specific poverty guideline thresholds based on family size according to Federal Student Aid eligibility criteria.

Income Threshold Examples (2025-26):

| Family Size | Max Pell Income Limit (Single Parent) | Max Pell Income Limit (Two Parents) |

|---|---|---|

| 2 | ~$41,000 | ~$32,000 |

| 3 | ~$51,500 | ~$40,000 |

| 4 | ~$62,000 | ~$48,500 |

| 5 | ~$72,500 | ~$56,500 |

| 6 | ~$83,000 | ~$64,500 |

Important: You don’t repay Pell Grants. They’re gift aid that reduces your out-of-pocket college costs. Students can receive Pell Grants for up to six years (12 full-time semesters or 600% lifetime eligibility).

July 2026 Restriction Alert: Beginning with the 2026-27 award year, students enrolled less than half-time (fewer than 6 credit hours per semester) will lose Pell eligibility. Additionally, students whose SAI exceeds $14,790 (twice the maximum Pell amount) will be disqualified under new federal regulations.

Scholarships: $500 to $30,000+ Per Award

Scholarships represent free money awarded based on merit, talent, demographics, field of study, or other criteria. Unlike Pell Grants, scholarships don’t require demonstrated financial need in many cases.

Merit-Based vs. Need-Based Difference:

- Merit scholarships reward academic achievement (GPA 3.5+), test scores (SAT 1300+), athletic ability, or special talents

- Need-based scholarships consider family income alongside other factors

Where to Find Scholarships:

- Institutional: Offered directly by colleges (average $8,000-$25,000)

- Private: Corporations like Coca-Cola ($20,000), nonprofits, community foundations ($500-$5,000)

- Corporate: Company-sponsored programs like the Walmart Associate Scholarship ($2,500-$5,000)

Application Strategy: Submit applications to 15-20 scholarships to maximize your odds. The typical acceptance rate for competitive scholarships is 5-10%, meaning volume matters. Start your search junior year of high school and continue through college.

Pro Tip: Local scholarships from Rotary clubs, credit unions, and community organizations have less competition than national programs. A $1,000 local scholarship often requires just one essay versus 50 essays competing for a $10,000 national award.

Federal Work-Study: Earn $2,000-$5,000 Yearly

Federal Work-Study provides part-time jobs for undergraduate and graduate students with financial need through participating institutions. Students typically work 10-20 hours per week during the academic year earning federal minimum wage ($7.25/hour) or higher depending on the position and location.

Work-study earnings count toward your total financial aid package but are paid directly to you through regular paychecks—not applied to your tuition bill. This means you control how the money is spent on education-related expenses like books, supplies, transportation, or personal costs.

Key Advantages:

- Jobs often relate to your field of study (gaining resume experience)

- Flexible scheduling around class commitments

- On-campus convenience for most positions

- Earnings don’t count against your financial aid eligibility for the following year

Application Process: Indicate work-study interest on your FAFSA application. Schools with limited funding award on a first-come, first-served basis, making early FAFSA submission critical. Annual earnings typically range from $2,000-$5,000 based on hours worked.

Student Loans: Last Resort (Know the Difference)

Federal student loans should be your last option after exhausting all grant, scholarship, and work-study opportunities. Loans require repayment with interest after graduation or when you drop below half-time enrollment.

Federal Loan Comparison:

| Loan Type | Interest Rate (2025-26) | Annual Limit | Subsidy Benefit |

|---|---|---|---|

| Subsidized | 6.53% | $3,500-$5,500 | Government pays interest during school |

| Unsubsidized | 6.53% | $5,500-$12,500 | Interest accrues immediately |

| Parent PLUS | 9.08% | Up to cost of attendance | No subsidy; parents borrow |

Critical Warning: Only borrow what you cannot cover with grants, scholarships, and work-study. The average student loan debt is $28,000 at graduation, requiring $300+ monthly payments for 10 years. Before taking loans, use our Debt Consolidation Calculator to understand long-term repayment costs.

Subsidized Advantage: If you qualify based on financial need, subsidized loans don’t accrue interest while you’re enrolled at least half-time. Unsubsidized loans accumulate interest from the day of disbursement, meaning a $5,500 freshman year loan can grow to $6,800+ by graduation without payments.

For students needing to understand how loans impact long-term finances alongside other debt, our guide on how to pay off debt fast provides repayment strategies that can save thousands in interest.

How to Get Financial Aid: FAFSA Complete Walkthrough

The Free Application for Federal Student Aid (FAFSA) is your gateway to accessing over $120 billion in federal student aid annually, plus state and institutional funding.

FAFSA Basics: Your Gateway to $40K+

The FAFSA application opens October 1 each year for the following academic year. For example, the 2026-27 FAFSA opened October 1, 2025, for students attending college between July 2026 and June 2027.

Key Deadlines:

- Federal Deadline: June 30, 2027 (for 2026-27 aid)

- State Deadlines: Often much earlier (see state-specific table below)

- College Deadlines: Vary by institution; check each school’s financial aid website

The streamlined FAFSA contains just 36 questions and takes approximately 15 minutes to complete when you have required documents ready. The application is completely free—never pay anyone to help you file FAFSA according to the U.S. Department of Education.

What FAFSA Unlocks:

- Federal Pell Grants (up to $7,395)

- Federal Supplemental Educational Opportunity Grants (FSEOG) (up to $4,000)

- Federal Work-Study eligibility

- Direct Subsidized and Unsubsidized Loans

- State grant programs (varies by state)

- Institutional aid from your college

- Some private scholarship eligibility

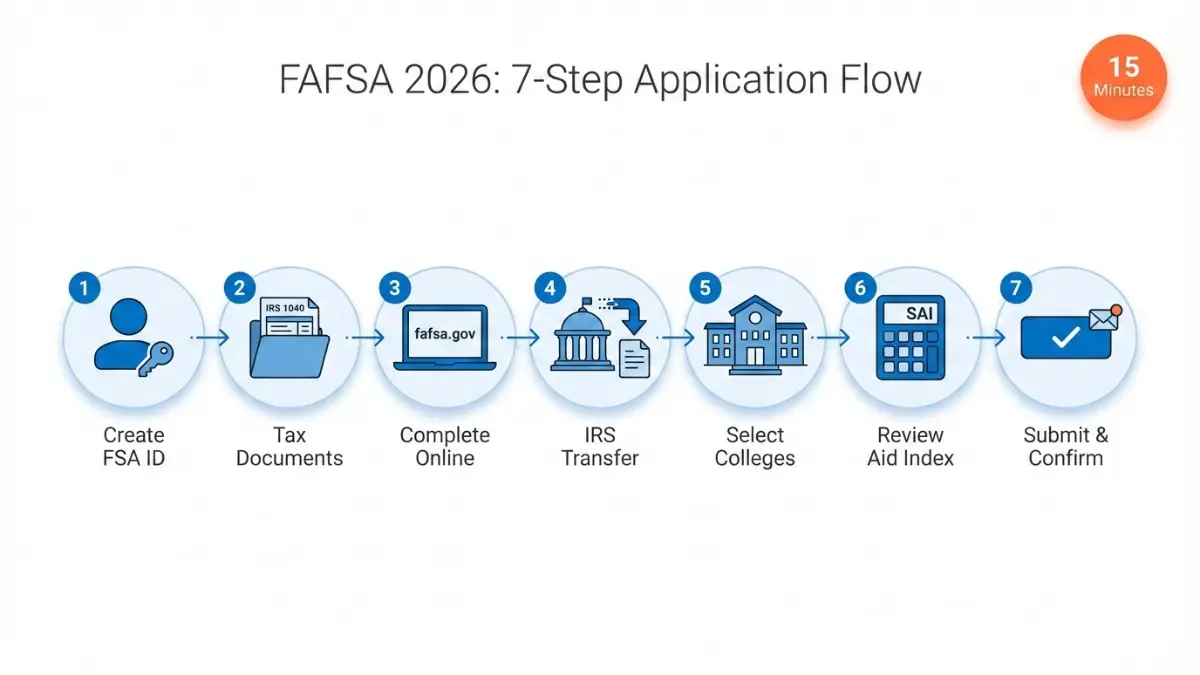

7 Steps to Complete FAFSA 2026-27

1. Create FSA ID (15 minutes):

Both student and parent (if dependent) need unique FSA IDs to electronically sign the FAFSA. Create yours at studentaid.gov using your Social Security Number, date of birth, and email address. Save your FSA ID username and password securely—you’ll use it for four years.

2. Gather Required Documents (1 hour):

- 2024 federal tax returns (for 2026-27 FAFSA)

- W-2 forms from all employers

- Records of untaxed income (Social Security, child support, veterans benefits)

- Current bank and investment account statements

- Business or farm records (if applicable)

3. Start Application at fafsa.gov:

Select “Start a New FAFSA” and choose the correct award year (2026-27). Answer questions about student demographics, citizenship status, and dependency status. Most students under 24 are considered dependent unless they’re married, have dependents, are veterans, or meet other independence criteria.

4. Import Tax Data Using IRS Data Retrieval Tool:

The FAFSA allows direct import of tax information from the IRS, reducing errors and speeding processing. Click “Link to IRS” when prompted and follow authentication steps. This feature imports adjusted gross income, tax paid, and other financial data automatically.

5. List Schools (Can Add Up to 10):

Add schools you’re applying to or considering. Schools receive your FAFSA data electronically and use it to build financial aid packages. You can change school selections after submission if your college plans change.

6. Review Student Aid Index (SAI):

After completing financial questions, FAFSA calculates your SAI—a number typically ranging from -$1,500 to $999,999 that measures your family’s ability to contribute. Lower SAI numbers indicate higher financial need and greater aid eligibility. Your SAI determines Pell Grant amounts and other need-based aid.

7. Submit & Track Confirmation:

Both student and parent electronically sign using FSA IDs. You’ll receive email confirmation within 3-5 days with your FAFSA Submission Summary showing your official SAI. Schools typically receive your data within 1-2 weeks and begin building aid packages.

For detailed SAI calculation methods and how it affects your specific situation, review our comprehensive FAFSA 2026 new SAI Rules guide that explains the recent formula changes.

State-Specific Deadlines (Don’t Miss These!)

Many states award grants on a first-come, first-served basis, meaning funds run out before the June 30 federal deadline. Missing your state deadline can cost you thousands in free money.

| State | Priority Deadline | Program | Maximum Award |

|---|---|---|---|

| California | March 2, 2026 | Cal Grant | $12,630 |

| Illinois | ASAP after Oct 1 | MAP Grant | $7,656 (funds limited) |

| Texas | January 15, 2026 | TEXAS Grant | $13,076 |

| New York | April 15, 2026 | TAP Grant | $5,665 |

| Ohio | October 1, 2025 | College Opportunity Grant | $3,360 |

| Pennsylvania | May 1, 2025 | State Grant | $5,750 |

| Georgia | June 30, 2026 | HOPE Scholarship | Varies by GPA |

| Florida | Rolling | Florida Student Assistance Grant | $1,690 |

State Deadline Strategy: File your FAFSA within two weeks of October 1 to ensure you meet all state deadlines. Even if you’re still deciding between colleges, file using your best current school list—you can update schools later without resubmitting the entire application.

Common FAFSA Mistakes (Cost Families $1,000s)

Using Wrong Tax Year:

The 2026-27 FAFSA requires 2024 tax information, not 2025 or 2026. Always use the “prior-prior year” taxes. Filing with the wrong year delays processing and may disqualify you from early state aid.

Listing 529 Plans as Student Assets:

Parent-owned 529 college savings plans are assessed at 5.64% in aid calculations, while student assets are assessed at 20%. Always report 529 plans as parent assets for dependent students to minimize impact on aid eligibility—this single mistake can reduce aid by thousands.

Not Filing Because “We Won’t Qualify”:

Families earning $90,000-$120,000 often qualify for partial Pell Grants, state aid, or federal loans. Many colleges require FAFSA for institutional merit scholarships regardless of need. Always file the FAFSA—it’s free and opens doors to more aid than most families expect.

Missing State Deadlines While Waiting:

Students sometimes delay FAFSA waiting for tax returns or college acceptance letters. File by your state’s priority deadline using estimated tax information if necessary. You can correct estimates later using the IRS Data Retrieval Tool without losing your place in line.

Not Updating FAFSA for Changed Circumstances:

Job loss, medical expenses, or divorce after filing can significantly reduce your SAI through Professional Judgment appeals to your college’s financial aid office. Don’t assume your initial FAFSA reflects your current situation—contact schools when major financial changes occur.

Optimizing your FAFSA also connects to broader financial planning—understanding your AGI 2026 Form 1040 helps you make strategic decisions that improve both tax outcomes and financial aid eligibility.

How to Get $40K+ in Financial Aid (Proven Tactics)

Securing maximum financial aid requires strategic planning across multiple funding sources. Here’s how students realistically achieve $40,000+ in annual aid.

Stack Multiple Aid Sources (The $40K Formula)

Sarah’s $42,500 Package Breakdown (Ohio State University, 2025-26):

- Federal Pell Grant: $7,395 (completed FAFSA in October)

- Ohio College Opportunity Grant: $4,800 (state grant for residents)

- Ohio State Institutional Merit Scholarship: $18,000 (3.8 GPA, 1340 SAT)

- Private Scholarships: $8,300 total

- Local Rotary Club Scholarship: $2,500

- Hispanic Scholarship Fund: $3,000

- Jack Kent Cooke Foundation: $1,500

- Community Foundation of Central Ohio: $1,300

- Federal Work-Study Earnings: $4,000 (15 hours/week at $13.33/hour)

Total FREE Money: $42,495

Out-of-Pocket Cost: $0 (after aid covered full cost of attendance)

This real example demonstrates that $40,000+ packages come from combining federal, state, institutional, and private sources—not from a single massive scholarship. Students who apply early, cast a wide net for scholarships, and attend schools offering generous institutional aid consistently exceed $40,000 in annual assistance.

8 Strategies to Maximize Financial Aid Eligibility

1. Apply Early for First-Come Aid:

Submit your FAFSA on October 1 or within the first week of opening. Federal Supplemental Educational Opportunity Grants (FSEOG), state grants like Illinois MAP, and college work-study funding are awarded first-come, first-served. Students filing in October receive 30-40% more in FSEOG funding than March filers at the same income levels.

2. Lower Your Student Aid Index (SAI):

Strategic financial moves before filing FAFSA can reduce your SAI and increase aid eligibility. Pay down consumer debt, maximize retirement contributions (401(k), IRA), and avoid holding assets in the student’s name. Grandparent-owned 529 plans distributed during college count as student income at 50%—wait until after filing final FAFSA (typically spring of junior year) to access these funds.

3. Apply to 100% Need-Met Schools:

Approximately 80 colleges guarantee to meet 100% of demonstrated financial need without loans. Elite schools like Harvard, Princeton, Yale, and MIT offer free tuition for families earning under $75,000-$100,000. The Princeton Promise covers full tuition and fees for families earning under $100,000 annually. Research schools’ financial aid policies before applying—this single decision impacts your total four-year costs by $100,000+.

4. Appeal Your Financial Aid Package:

About 70% of families who appeal financial aid awards receive additional funding averaging $3,000-$5,000 per year. Submit appeals in writing to your college’s financial aid office citing changed circumstances (job loss, medical bills, sibling college enrollment) or competitive offers from peer institutions. Use professional, factual language and include documentation supporting your request.

5. Search Lesser-Known Local Scholarships:

Local scholarships from community foundations, credit unions, civic clubs (Rotary, Kiwanis, Lions), and employer programs have acceptance rates 10-20x higher than national scholarships. A $1,000 local scholarship requiring one essay beats competing with 50,000 applicants for a $10,000 national award. Search your city name + “scholarships” or ask your high school counselor for local opportunities.

6. File FAFSA Every Year Without Exception:

Federal student aid isn’t automatic—you must file FAFSA annually to renew Pell Grants, work-study, and federal loans. Even if your financial situation hasn’t changed, colleges may adjust institutional aid based on updated family circumstances. Set an October calendar reminder each year to resubmit FAFSA using the previous year’s tax information.

7. Maintain Satisfactory Academic Progress (SAP):

Federal financial aid requires maintaining at least a 2.0 GPA and completing 67% of attempted courses. Falling below SAP standards results in immediate aid suspension. If you’re struggling academically, use tutoring resources, reduce your course load temporarily, and communicate with your financial aid office before problems become critical. Most schools allow one SAP appeal for extenuating circumstances.

8. Use Professional Judgment for Changed Circumstances:

Financial aid offices have authority to adjust your SAI when special circumstances occur after filing FAFSA. Qualifying situations include job loss, divorce, death of a parent, significant medical expenses, or natural disasters affecting your home. Document your situation with tax returns, termination letters, medical bills, or insurance claims and request a Professional Judgment review in writing.

Expert Quote Panel

Dr. Jennifer Martinez, CFP®, Finance Authority Hub Senior Financial Advisor:

“Most families leave $4,000-$8,000 on the table annually by not optimizing their FAFSA filing strategy. Simple moves like repositioning assets from student to parent accounts, paying down credit card debt before the FAFSA snapshot date, and maximizing retirement contributions can unlock thousands in additional grant money. I’ve seen families earning $95,000 qualify for $8,500 in Pell and state grants just by restructuring their finances two months before filing.”

Michael Chen, Director of Financial Aid, State University System:

“The biggest mistake I encounter? Families assuming they won’t qualify for aid based on income alone. I’ve awarded $25,000+ packages to families earning $120,000 when multiple siblings attend college simultaneously—the SAI formula accounts for family size and number in college. The second mistake is filing FAFSA in March instead of October. Early filers at our institution receive an average of $4,200 more in campus-based aid simply because funds haven’t been depleted yet.”

Students planning college finances alongside other major expenses should also review our Home Affordability Calculator to understand how education costs integrate with broader financial goals, especially for parents considering tuition payments while managing mortgage obligations.

15 Financial Aid Sources Competitors Won’t Tell You

Most financial aid guides focus exclusively on FAFSA and Pell Grants. Strategic students tap into multiple lesser-known sources that competitors overlook.

State-Specific Grant Programs (Free Money Hiding in Plain Sight)

Every state operates grant programs separate from federal aid, totaling over $10 billion annually. These programs require state residency and attendance at in-state institutions in most cases.

Top 10 States by Average Grant Award (2025-26):

- New York – TAP Grant: Up to $5,665 for residents attending public/private NY colleges

- California – Cal Grant: Up to $12,630 at private universities, $6,028 at UC/CSU

- Illinois – MAP Grant: Up to $7,656 (funds awarded first-come, first-served)

- New Jersey – TAG Grant: Up to $13,000 for full-time undergraduates

- Pennsylvania – State Grant: Up to $5,750 for PA residents at approved institutions

- Washington – State Need Grant: Up to $13,080 based on family income

- Texas – TEXAS Grant: Up to $13,076 at four-year public universities

- Minnesota – State Grant: Up to $11,648 for undergraduates with financial need

- Oregon – Opportunity Grant: Up to $3,270 for first-time degree seekers

- Vermont – Grant Program: Up to $13,050 for Vermont residents

Application Process: Most states use your FAFSA data automatically—no separate application required. However, some states like New York require additional state-specific forms. Check your state’s higher education agency website for requirements and deadlines, which often precede the federal June 30 deadline by 3-8 months.

Employer Tuition Assistance (Often Overlooked)

Approximately 56% of U.S. employers offer education benefits that most employees never use. Federal tax law allows companies to provide up to $5,250 annually in tax-free tuition assistance per employee.

Major Employers with Standout Programs:

- Starbucks: 100% tuition coverage for Arizona State University online bachelor’s degrees

- Amazon: Career Choice program pays $1,200 annually for job-relevant education

- UPS: $5,250 per year for part-time package handlers (immediately eligible)

- Walmart: $1 per day tuition for associates at partner universities

- Chipotle: $5,250 annually for degrees from 75+ universities (after 4 months employment)

- Target: $5,250 annually for undergraduate degrees, $10,000 for graduate programs

Strategy: Ask your HR department about tuition assistance before applying to colleges. Some programs require you to work in specific roles or locations, attend certain schools, or maintain minimum grades. Planning your college choice around employer benefits can eliminate $21,000-$42,000 in four-year costs.

Military & Veteran Benefits

Military service members, veterans, and their families access substantial education benefits outside traditional financial aid.

Post-9/11 GI Bill:

Covers full in-state tuition at public universities plus a monthly housing allowance (Basic Allowance for Housing – BAH) and annual $1,000 book stipend. Private university students receive up to $28,937.18 annually (2025-26 rate). Benefits extend for 36 months of full-time education (four academic years).

Reserve Officer Training Corps (ROTC) Scholarships:

Four-year Army, Navy, Air Force, and Marine ROTC scholarships cover full tuition, fees, books, and provide monthly stipends ($420-$500). Recipients commit to active duty service (typically 4 years) after graduation. High school seniors apply fall of senior year with selection in spring.

Yellow Ribbon Program:

Participating private colleges supplement GI Bill benefits to cover the gap between the annual cap and actual tuition costs. Over 1,900 schools participate, eliminating out-of-pocket costs for veterans attending expensive private universities.

Dependency Benefits:

Children of 100% disabled or deceased veterans qualify for Fry Scholarship or Dependents’ Educational Assistance (DEA) providing up to 36 months of education benefits.

For veterans and military families navigating multiple financial obligations including education, mortgage planning tools like our Mortgage Calculator help coordinate GI Bill housing allowances with home purchase decisions.

Income-Driven Repayment & Loan Forgiveness

While not grants, these federal programs significantly reduce loan repayment burdens for specific career paths and income levels.

Public Service Loan Forgiveness (PSLF):

Forgives remaining federal Direct Loan balance after 120 qualifying monthly payments (10 years) while working full-time for government or 501(c)(3) nonprofit employers. Teachers, social workers, public defenders, and nonprofit employees commonly use PSLF to eliminate $30,000-$100,000+ in student debt.

Teacher Loan Forgiveness:

Provides up to $17,500 in forgiveness for teachers working five consecutive years in low-income schools teaching math, science, or special education. Regular education teachers receive up to $5,000 after five years.

Income-Driven Repayment Plans:

Cap monthly payments at 10-15% of discretionary income regardless of loan balance. After 20-25 years of payments, remaining balances are forgiven (though forgiven amounts may be taxable). The new SAVE plan (Saving on a Valuable Education) offers the most generous terms with $0 payments for borrowers earning under 225% of poverty guidelines.

Understanding how student loan decisions affect your broader financial picture connects to managing all forms of debt—our guide on Credit Card Debt Escape Strategies provides complementary debt management tactics.

Niche Scholarship Databases

Free scholarship search platforms help you identify hundreds of opportunities matching your specific profile.

Top Free Scholarship Search Engines:

- Fastweb.com: Database of 1.5 million scholarships worth over $3.4 billion

- Bold.org: Features no-essay and quick-apply scholarships ($500-$10,000 awards)

- Scholarships.com: State-specific filters and deadline sorting (800,000+ scholarships)

- Community Foundations: Local organizations awarding $500-$5,000 with lower competition

- Professional Associations: Field-specific scholarships from nursing, engineering, teaching organizations

Search Strategy: Create comprehensive profiles on 3-4 platforms, set up scholarship match email alerts, and apply to 2-3 opportunities weekly starting junior year of high school. Treat scholarship applications as a part-time job—15 hours of applications monthly can yield $5,000-$15,000 in annual awards.

Financial Aid 2026: What’s New & Your Next Steps

Federal financial aid regulations undergo significant changes for the 2026-27 award year affecting millions of students. Understanding these changes ensures you maximize eligibility.

Critical July 2026 Changes (Big Beautiful Bill Impact)

Congress passed the Fiscal Responsibility Act (nicknamed “Big Beautiful Bill”) in July 2025, implementing major financial aid restrictions beginning July 1, 2026.

⚠️ Students Enrolled Less Than Half-Time:

Starting with the 2026-27 award year, undergraduate students taking fewer than 6 credit hours per semester lose Pell Grant eligibility entirely. Previously, part-time students received prorated Pell awards based on enrollment intensity. This change affects approximately 3 million part-time students who often work full-time while attending college.

⚠️ SAI Threshold Tightened:

Students whose calculated Student Aid Index exceeds $14,790 (twice the 2025-26 maximum Pell Grant of $7,395) will be completely ineligible for Pell Grants. Under previous rules, students with SAI up to $6,000-$7,000 could qualify for minimum Pell awards. This threshold change eliminates Pell eligibility for families in the $70,000-$90,000 income range with typical assets.

✅ Vocational & Trade School Expansion:

The same legislation expands Pell Grant eligibility to short-term workforce training programs lasting 8-15 weeks at qualified institutions. This opens federal grant funding to certificate programs in high-demand fields like healthcare, information technology, skilled trades, and manufacturing. An estimated 440,000 additional students will access Pell Grants through this pathway.

✅ Foreign Income Inclusion:

FAFSA now requires reporting of foreign income earned by students and parents, closing a previous loophole where families working overseas could claim artificially low U.S.-based income. This change promotes equity but may reduce aid for expatriate American families.

Your 5-Step Action Plan (Start Today)

Step 1: Create FSA ID at studentaid.gov (10 minutes)

Visit studentaid.gov and click “Create Account” for both student and parent. You’ll need Social Security Numbers, dates of birth, valid email addresses, and ability to answer knowledge-based verification questions. Save login credentials in a password manager—you’ll use your FSA ID for four years of FAFSA submissions, loan management, and aid tracking.

Step 2: Gather 2024 Tax Documents (1 hour)

Collect your 2024 federal tax return (Form 1040), all W-2 wage statements, 1099 forms for investment income, records of untaxed income (Social Security benefits, child support, veterans non-education benefits), and current checking/savings account balances. If you haven’t filed 2024 taxes yet, use estimated information and update later through FAFSA corrections.

For families optimizing tax returns to improve financial aid outcomes, our detailed guide on the 1040 Tax Form 2026 identifies seven common errors that impact both tax refunds and student aid calculations.

Step 3: Complete FAFSA 2026-27 (15 minutes active time)

Log into fafsa.gov using your FSA ID, select “2026-2027 FAFSA,” and begin answering questions. Use the IRS Data Retrieval Tool to automatically import tax information when prompted. List up to 10 colleges you’re considering—schools receive your information electronically and you can modify your school list anytime after submission. Review your answers carefully before clicking “Sign & Submit.”

Step 4: Research 15 Scholarships via Fastweb (2 hours)

Create a detailed profile on Fastweb.com including GPA, test scores, intended major, activities, demographics, and financial need. Browse matches and bookmark 15 scholarships with deadlines over the next 3-6 months. Prioritize local scholarships from community foundations, smaller national awards with specific eligibility criteria matching your profile, and renewable multi-year scholarships.

Step 5: Mark State Deadline on Calendar + Set Reminder

Find your state’s financial aid deadline using the table in Section 3 and create a smartphone reminder 30 days before the deadline. Many states award grants first-come, first-served, so setting an early reminder ensures you file with time to spare even if you experience delays gathering documents.

What This Means For You

Income <$60,000, Family of 4:

You likely qualify for the full $7,395 Pell Grant plus substantial state grants. Total federal and state aid could reach $12,000-$20,000 before including institutional scholarships. Apply to in-state public universities and private colleges offering generous need-based aid to minimize out-of-pocket costs. Focus on colleges meeting 100% of demonstrated need to maximize your aid package.

Income $60,000-$90,000, Family of 4:

Expect partial Pell Grant eligibility ($2,000-$5,000) depending on assets and exact SAI calculation. State grants may provide an additional $2,000-$7,000 depending on your state. Aggressively pursue merit scholarships and apply to colleges where your academic profile places you in the top 25% of admitted students—these schools offer the most competitive merit packages to attract strong students.

Income $90,000+, Multiple Kids in College:

Your SAI divides when multiple family members attend college simultaneously, potentially unlocking $10,000-$30,000 in need-based institutional aid per child. Many elite private colleges offer superior aid packages compared to public universities for families in this income bracket. Use net price calculators on college websites to compare actual costs—sticker price doesn’t reflect what you’ll pay after aid.

Students and families managing multiple financial goals including college costs, retirement savings, and home purchases benefit from integrated planning approaches covered in our Retirement Planning 30s 2026 guide showing how to balance education funding with long-term wealth building.

Final Action Call: Don’t leave free money on the table. Over $2.6 billion in Pell Grants goes unclaimed annually because eligible students don’t file FAFSA. Start your FAFSA today at studentaid.gov or schedule time this week to complete all five action steps. Your financial aid journey begins with a single free application that opens doors to tens of thousands of dollars in college funding.

FAQs

1. What is financial aid?

Financial aid is monetary assistance from federal/state governments, colleges, or organizations covering education costs. It includes grants, scholarships, work-study, and loans. Grants and scholarships don’t require repayment while loans must be repaid with interest.

2. How much financial aid can I get?

Aid amounts depend on income, family size, and enrollment status. Low-income students typically receive $7,395-$40,000+ annually combining Pell Grants, state grants, institutional scholarships, and work-study. Middle-income families ($60,000-$90,000) often qualify for $8,000-$25,000 in aid.

3. Do I have to pay back financial aid?

Grants and scholarships are FREE money requiring no repayment. Work-study earnings are paid wages you keep. Federal and private student loans must be repaid with interest after graduation or when enrollment drops below half-time.

4. When should I apply for FAFSA?

File FAFSA on October 1 annually for the next academic year. Earlier applications receive more campus-based aid (FSEOG, work-study) awarded first-come, first-served. State deadlines range from October through June—check your state’s priority date. Never wait past your state deadline.

5. Can I get financial aid with high income?

Yes. Families earning $90,000-$120,000 frequently qualify for partial federal aid, especially with multiple college-attending children. Many colleges require FAFSA for merit scholarships regardless of income. Elite private schools offer need-based aid to families earning up to $200,000.

6. What is a Pell Grant?

The Federal Pell Grant is need-based aid for undergraduates pursuing first bachelor’s degrees. Maximum award is $7,395 for 2025-26 based on Student Aid Index calculated from FAFSA. Pell Grants never require repayment and can be received for up to six years.

7. What is the Student Aid Index (SAI)?

SAI is a number from -$1,500 to $999,999 representing your family’s expected college contribution. FAFSA calculates SAI using income, assets, family size, and number in college. Lower SAI indicates higher financial need and greater aid eligibility.

8. How do I maximize financial aid?

File FAFSA by October 1, apply to 15+ scholarships, choose colleges meeting 100% need, appeal initial aid packages, maintain 67% course completion rate and 2.0+ GPA, and optimize finances before FAFSA (pay down debt, maximize retirement contributions).

9. What changed for financial aid in 2026?

Starting July 1, 2026: Students taking fewer than 6 credits lose Pell eligibility; SAI threshold tightened to $14,790 maximum; trade school certificates (8-15 weeks) gain Pell eligibility; foreign income must be reported. These changes affect the 2026-27 award year.

10. Can I get financial aid for online college?

Yes, if the institution is accredited and participates in federal Title IV programs. Complete FAFSA identically to traditional colleges. Over 3,000 online programs qualify for federal student aid including Pell Grants, loans, and work-study.

11. What happens if I miss the FAFSA deadline?

You can still file until June 30 federal deadline, but you may miss state/school aid with earlier deadlines. Some first-come aid exhausts by March-April. Late filers receive federal loans and Pell (if eligible) but lose thousands in state grants and campus-based aid.

Disclaimer

This article is for educational purposes only and does not constitute financial, legal, or tax advice. Financial aid eligibility, award amounts, federal regulations, and institutional policies change frequently and vary significantly by individual circumstances. Information presented represents general guidance current as of February 2026 and may not reflect the most recent updates to federal or state programs.

Always verify current information through official sources including studentaid.gov, your state’s higher education agency, individual college financial aid offices, and qualified financial advisors. Dollar amounts cited represent maximum potential awards when combining multiple aid sources and will vary based on your specific income, family size, assets, college choice, enrollment status, academic performance, and state of residence.

Consult a certified financial planner, tax professional, or licensed education consultant for personalized guidance regarding your unique financial situation and college funding strategy. Finance Authority Hub and its contributing experts provide general educational information only and cannot guarantee specific financial aid outcomes or eligibility for any particular student or family.

Federal student aid programs including Pell Grants, Direct Loans, and work-study are subject to annual Congressional appropriations and regulatory modifications. State grant programs depend on state budget allocations and may change or be eliminated without notice. Always confirm program availability and requirements directly with the administering agency before making enrollment or financial decisions.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.