Credit Score Calculator: Check Your FICO Instantly

Credit Score Calculator

Educational estimator: see an estimated score range, factor-by-factor breakdown, and “what-if” improvements (especially utilization paydown targets).

Inputs

This is simplified; real scoring models use many more signals.

Results

Estimated score

—

Estimated range: —

Tier: —

Utilization snapshot

Utilization: —

Limit: —

Balance: —

Paydown targets (estimate)

Pay down to reach 30%: —

Pay down to reach 10%: —

These are balance targets only; issuer/reporting timing may differ.

Factor subscores

Payment history: —

Utilization: —

Length: —

New credit: — • Mix: —

Model used

—

This tool is an educational estimator. Real credit scores can differ by bureau, scoring model version, and lender. (Tip: keep these words in the UI to stay compliant.)

Breakdown table (how the estimate is built)

| Factor | Weight | Subscore | Approx points |

|---|

“What-if” scenarios (utilization)

| Scenario | Target balance | Pay down needed | Estimated score |

|---|

If your utilization is high, this is usually the fastest lever to improve the estimate (with everything else unchanged).

Results appear after you click “Calculate.”

In This Article

What Is a Credit Score? The Number That Controls Your Financial Life

Your credit score is a three-digit number between 300 and 850 that lenders use to decide whether to approve you for a loan, credit card, or mortgage — and at what interest rate. The higher your score, the more money you save over a lifetime of borrowing.

In 2026, the average American FICO® score sits at 715, according to Experian’s latest consumer credit review. That puts the average borrower solidly in the “Good” tier — but not yet at the “Very Good” range where the best rates unlock.

Two scoring models dominate the US market:

| Model | Range | Used By |

|---|---|---|

| FICO® Score 8/9/10 | 300–850 | 90%+ of top lenders |

| VantageScore 3.0/4.0 | 300–850 | Credit Karma, NerdWallet, many banks |

Both models pull data from the three major bureaus — Equifax, Experian, and TransUnion. Scores can vary slightly between bureaus because not every lender reports to all three.

What This Means For You: A 50-point difference in your credit score can mean thousands of dollars more in interest over the life of a mortgage. Use our Mortgage Calculator to see exactly how your score impacts your monthly payment.

The Consumer Financial Protection Bureau (CFPB) confirms that checking your own credit score never hurts it — so there is zero reason not to know your number today.

How to Use Our Free Credit Score Calculator

Our tool gives you an instant estimated score range, factor-by-factor subscore breakdown, and what-if paydown scenarios — with no login required. Here is exactly how to use it in five steps.

Step-by-Step Guide

Step 1: Select Your Currency and Scoring Model

- Choose from 22 currencies (USD, GBP, CAD, AUD, EUR, and more)

- Select FICO-style (5 factors, used by 90%+ of lenders) or VantageScore-style (6 factors, used by Credit Karma and many apps)

Step 2: Enter Your Credit Limit and Balance

- Input your total revolving credit limit across all cards

- Input your current total revolving balance

- The tool instantly calculates your credit utilization ratio — the #2 most important factor

Step 3: Input Payment History Details

- Select late payments in the last 24 months (none / 1 / 2–3 / 4+)

- Flag any derogatory marks: collections, charge-offs, judgments

- Check the bankruptcy box if applicable

Step 4: Enter Credit History Age

- Age of your oldest account in years (e.g., 8)

- Average age of all accounts (e.g., 3.5)

- Older accounts = higher scores. Never close your oldest card.

Step 5: Add Inquiries, New Accounts, and Credit Mix

- Hard inquiries in the last 12 months

- New accounts opened in the last 12 months

- Check all credit types you hold: credit cards, auto loan, mortgage, student/personal loan, line of credit

Then click Calculate — your estimated score range, tier, and paydown targets appear instantly.

Why This Tool Destroys Every Competitor

| Feature | Our Tool | WalletHub | Credit Karma | SoFi |

|---|---|---|---|---|

| No login required | ✅ | ❌ | ❌ | ✅ |

| FICO + VantageScore dual model | ✅ | ❌ | ❌ | ❌ |

| Factor-by-factor subscore | ✅ | ❌ | ❌ | ❌ |

| What-if paydown scenarios | ✅ | ❌ | ❌ | ✅ |

| Downloadable CSV report | ✅ | ❌ | ❌ | ❌ |

| Multi-currency (22 currencies) | ✅ | ❌ | ❌ | ❌ |

FICO-Style vs VantageScore — Which Should You Choose?

Choose FICO-style if you are applying for a mortgage, auto loan, or credit card — because myFICO confirms that over 90% of top US lenders use FICO scores in lending decisions.

Choose VantageScore-style if you want to match what free monitoring apps like Credit Karma show you. VantageScore weighs payment history slightly higher (41%) and is more forgiving of thin credit files.

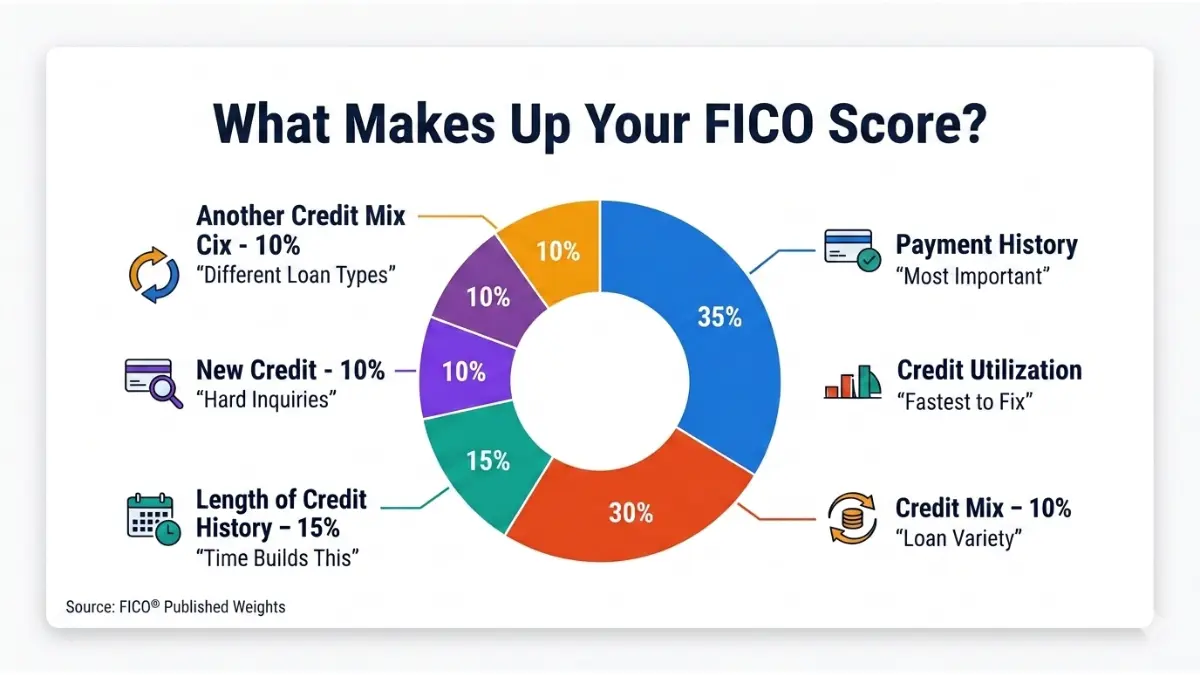

The 5 Factors That Determine Your FICO Credit Score

FICO publishes its five scoring factors and their weights. Understanding each one is the key to moving your score from average to exceptional.

The Master Breakdown

| Factor | FICO Weight | Impact Level |

|---|---|---|

| Payment History | 35% | 🔴 Highest — 1 missed payment = -60 to -100 pts |

| Credit Utilization | 30% | 🟠 Very High — fastest lever to improve |

| Length of Credit History | 15% | 🟡 Moderate — time-dependent |

| New Credit / Hard Inquiries | 10% | 🟢 Lower — fades after 12 months |

| Credit Mix | 10% | 🟢 Lower — variety matters |

Payment History (35%) — Why One Missed Payment Can Destroy Your Score

Payment history is the single largest factor in your FICO score. A single 30-day late payment can drop a good score (750+) by 60 to 110 points, according to FICO’s own score damage estimates.

The damage lingers on your credit report for up to seven years — though its impact fades significantly after two to three years of clean payment history.

Action steps:

- Set up autopay for at least the minimum payment on every account

- If you missed a payment recently, call the lender and request a goodwill adjustment — many will remove a single late mark for long-term customers

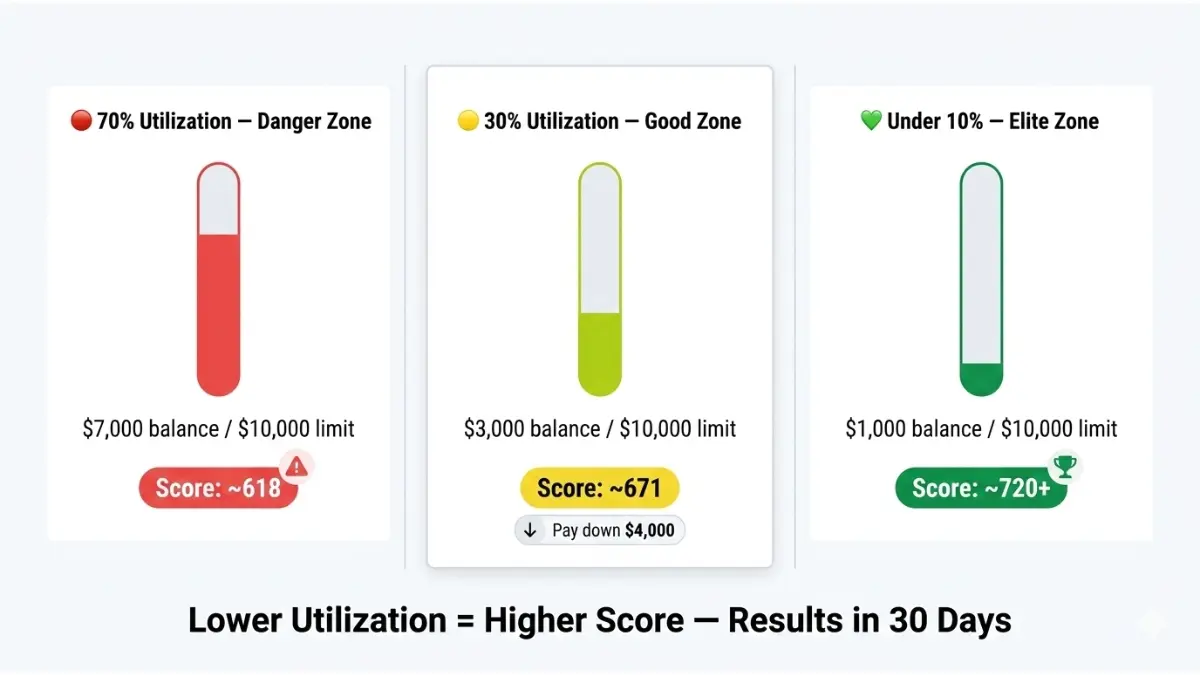

Credit Utilization (30%) — The Fastest Lever You Have

Credit utilization is calculated by dividing your total revolving balance by your total credit limit. For example, a $3,000 balance on a $10,000 limit = 30% utilization.

The elite utilization targets:

| Utilization % | Score Impact |

|---|---|

| Under 1% | Maximum score benefit |

| 1%–9% | Excellent |

| 10%–29% | Good |

| 30%–49% | Moderate negative impact |

| 50%+ | Serious score damage |

This is where our calculator’s what-if paydown feature becomes a weapon. Enter your current balance and limit, and the tool tells you exactly how much to pay to hit 30%, 10%, or 1% utilization — with an estimated score impact for each target.

If you are carrying high-interest balances across multiple cards, use our Debt Consolidation Calculator to see whether consolidating into one lower-rate loan reduces your utilization and your monthly payment simultaneously.

Hard Inquiry vs Soft Inquiry — Does Checking Your Score Hurt It?

This is one of the most searched questions on this topic — and most competitors answer it vaguely.

Here is the definitive answer:

- Soft inquiry (checking your own score, pre-approval checks): Zero impact on your score. Always safe.

- Hard inquiry (lender pulls your report after you apply for credit): -5 points on average, stays on your report for 24 months, but only affects your score for 12 months.

- Rate shopping exception: Multiple hard inquiries for the same loan type (mortgage, auto, student loan) within a 14–45 day window count as a single inquiry under FICO’s deduplication rule.

The Federal Trade Commission confirms you are entitled to one free credit report per bureau per year at AnnualCreditReport.com — and that checking it yourself never affects your score.

Credit Score Ranges: What Your Number Actually Means in 2026

This section maps directly to what our calculator shows you after you hit Calculate. Every tier has a real-world impact on your borrowing costs.

The Definitive 2026 FICO Range Table

| Score Range | FICO Tier | What You Qualify For | Avg Mortgage Rate Premium |

|---|---|---|---|

| 800–850 | Exceptional | Best rates, instant approvals, highest limits | 0% premium — best rate |

| 740–799 | Very Good | Near-best rates, strong approvals | +0.1% to +0.25% |

| 670–739 | Good | Most credit products, competitive rates | +0.5% to +0.75% |

| 580–669 | Fair | Limited options, higher APR | +1.5% to +2.5% |

| 300–579 | Poor | Secured cards, subprime loans only | +3%+ or denied |

2026 Reality Check:

- 23% of Americans have an exceptional score of 800+ (Experian)

- 50.3% have a very good or exceptional score (740+)

- Average score is 715 — solidly “Good” but not yet unlocking elite rates

What Credit Score Do You Need for a Mortgage in 2026?

Mortgage lenders in 2026 use tiered score cutoffs that directly determine your interest rate. The difference between a 680 and a 760 score on a $400,000 mortgage can exceed $80,000 in total interest over 30 years.

| Loan Type | Minimum Score | Best Rate Threshold |

|---|---|---|

| FHA Loan (3.5% down) | 580 | 660+ |

| Conventional Loan | 620 | 740+ |

| VA Loan | No minimum (lender sets) | 680+ recommended |

| Jumbo Loan | 700 | 760+ |

Use our Home Affordability Calculator to see exactly what home price your current score and income qualify for — and our Mortgage Refinance Calculator to see how much you would save by refinancing after a score improvement.

What Credit Score Do You Need for a Car Loan in 2026?

Auto lenders use their own FICO Auto Score versions, but general tiers apply. The average auto loan borrower in 2026 has a score of 715, while subprime borrowers (below 600) pay APRs of 15–21% versus 5–7% for prime borrowers.

Use our Auto Loan Calculator to run the exact monthly payment difference between a 600-score rate and a 740-score rate on your target vehicle.

How to Improve Your Credit Score Fast — 2026 Action Plan

This is what every user ultimately wants. Here is a timeline-based action plan that no competitor currently publishes in this format — built around what actually moves scores fastest.

The 2026 Score Improvement Timeline

| Timeline | Action | Expected Score Gain |

|---|---|---|

| 30 days | Pay down revolving balances to under 30% utilization | +20 to +65 points |

| 30–60 days | Dispute errors on credit reports | +25 to +75 points |

| 1–3 months | Get added as authorized user on a long-standing account | +10 to +30 points |

| 3–6 months | Maintain 100% on-time payment streak | +12 to +40 points |

| 6–12 months | Hard inquiries age out of score calculation | +5 per inquiry |

| 12–24 months | Average credit age grows; new accounts mature | Gradual +15 to +30 |

The Fastest Fix — Utilization Paydown (Results in 30 Days)

Real example — Marcus, 34, from Chicago: Marcus had a $12,000 total credit limit with $8,400 in balances — a 70% utilization rate dragging his score down to 618. He paid down $5,400 to reach 25% utilization in one billing cycle. His score jumped to 671 — enough to qualify for a conventional mortgage instead of FHA, saving him approximately $180/month.

Our calculator’s what-if table shows you the exact paydown needed to hit 30%, 10%, and 1% targets — along with an estimated score for each scenario.

If you cannot pay all balances down at once, prioritize the card closest to its limit first. A card at 95% utilization damages your score far more than one at 40%.

How to Dispute Credit Report Errors (Step-by-Step)

One in five Americans has an error on at least one credit report, according to a Federal Trade Commission study on credit report accuracy. These errors — wrong balances, accounts that aren’t yours, incorrect late payment marks — are legally removable.

Dispute process:

- Get your free reports at AnnualCreditReport.com — the only federally authorized source

- Identify errors: wrong account information, duplicate entries, incorrect late payments

- File disputes directly with each bureau online (Equifax, Experian, TransUnion)

- Bureaus must investigate within 30 days under the Fair Credit Reporting Act

- If the creditor cannot verify the item, it must be removed

Does Debt Consolidation Help Your Credit Score?

Done correctly, debt consolidation can improve your score in two ways: it reduces per-card utilization rates (because balances move to a personal loan, which is not revolving credit) and simplifies your payment history to a single monthly payment.

Use our Debt Consolidation Calculator to compare your current total interest cost versus a consolidated loan at today’s rates. For deeper strategy on eliminating high balances, our Snowball vs Avalanche guide shows which payoff method saves more for your specific debt profile.

Should You Close Old Credit Cards?

No. Closing a credit card hurts your score in two ways:

- Increases utilization: Reduces your total available credit, pushing your utilization ratio higher

- Shortens credit history: If it was one of your oldest accounts, your average account age drops

The only exception: if the card carries a high annual fee and you receive no value from it, you can close it — but only after your score is already at your target level.

For users working through high credit card balances, our Credit Card Debt Strategies guide covers every tested method for eliminating revolving debt without damaging your score.

Credit Scores in the USA — Regional, Generational, and Global Context

US Regional Score Averages (2026)

Most people do not realize that where you live correlates with your average credit score — primarily due to income levels, cost of living, and financial literacy rates.

| State | Average FICO Score (2025–2026) |

|---|---|

| Minnesota | 742 (highest) |

| Vermont | 738 |

| Wisconsin | 737 |

| Mississippi | 680 (lowest) |

| Louisiana | 682 |

| National Average | 715 |

US Credit Scores by Generation (2026)

| Generation | Average FICO Score | Key Challenge |

|---|---|---|

| Gen Z (18–27) | 680 | Thin credit file, high utilization |

| Millennials (28–43) | 690 | Student loan burden, new mortgages |

| Gen X (44–59) | 731 | Peak earning + peak debt |

| Baby Boomers (60–78) | 745 | Long credit history advantage |

| Silent Generation (79+) | 760 | Lowest debt loads |

Expert Panel — 2026 Consensus

Laura M. Bennett, CFP®: “In 2026, utilization remains the single fastest lever most borrowers can pull to see movement within one billing cycle. Clients who drop utilization from 70% to under 30% routinely gain 40–65 points before their next statement closes.”

Daniel Moreau, CPA/CFP®: “The consumers who struggle most are those with no credit mix. A single credit card history, even with perfect payments, plateaus around 720–730. Adding an installment loan — even a small personal loan — consistently pushes scores into the 750–780 range over 12 months.”

Credit Scoring Outside the USA

For our international users in the UK, Canada, and Australia, credit scoring systems operate differently but the core principles — payment history, utilization, age of accounts — remain the same.

| Country | Score Range | Top Bureaus |

|---|---|---|

| USA | 300–850 | Equifax, Experian, TransUnion |

| UK | 0–999 | Experian, Equifax, TransUnion UK |

| Canada | 300–900 | Equifax Canada, TransUnion Canada |

| Australia | 0–1,200 | Equifax, Experian, Illion |

Our calculator supports all four countries’ currencies and gives meaningful estimates for any user with revolving credit, regardless of country.

Frequently Asked Questions

1. What is a good credit score in 2026?

670 or above is considered “Good” on the FICO scale. 740+ is “Very Good” and unlocks most competitive rates. 800+ is “Exceptional” — achieved by 23% of Americans.

2. Does checking my credit score hurt it?

No. Checking your own score is a soft inquiry and has absolutely zero impact on your FICO or VantageScore.

3. How fast can I improve my credit score?

Paying down utilization below 30% reflects on your score within one billing cycle — typically 30 days. Consistent on-time payments show meaningful improvement in 3–6 months.

4. What credit score do I need for a mortgage?

FHA loans require a minimum 580. Conventional loans require 620+. To get the best available mortgage rates in 2026, you need 740 or higher.

5. How is credit utilization calculated?

Divide your total revolving balance by your total credit limit. Example: $2,500 balance ÷ $10,000 limit = 25% utilization. Keep it under 10% for maximum score benefit.

6. What is the difference between FICO and VantageScore?

Both range from 300–850. FICO uses 5 published factors (35/30/15/10/10 weighting). VantageScore uses 6 factors with payment history weighted at 41%. FICO is used by 90%+ of lenders; VantageScore is used by most free monitoring apps.

7. How many points does a hard inquiry drop your score?

Typically 5 points per hard inquiry on average. The effect fades after 12 months and the inquiry disappears from your report after 24 months.

8. Does closing a credit card hurt your score?

Yes — it reduces your available credit (raising utilization) and can shorten your average account age. Avoid closing old cards unless the annual fee makes it necessary.

9. What is the average credit score in the USA in 2026?

715, according to Experian’s FICO Score Report. This is stable following a slight dip in 2024–2025 driven by student loan repayment resumption and rising credit card balances.

10. How accurate is this credit score calculator?

This tool is an educational estimator using published FICO and VantageScore factor weightings. Actual bureau scores vary based on your complete credit file, scoring model version, and lender-specific overlays. Use it as a directional guide, not an official score.

11. Can I get a loan with a 580 credit score?

Yes — FHA-backed home loans accept 580+, and many personal loan lenders work with scores in this range. However, rates will be significantly higher. Use our Personal Loan Calculator to compare costs at different score tiers before applying.

⚠️ Disclaimer: This credit score calculator and article are for educational and informational purposes only. Results are estimates based on publicly available scoring model weightings and do not represent an official FICO® Score or VantageScore®. This content does not constitute financial advice. Always consult a qualified financial advisor and obtain your official credit reports from AnnualCreditReport.com for accurate, lender-ready credit information. FICO® is a registered trademark of Fair Isaac Corporation.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.