Best 0% APR Balance Transfer Cards April 2026: Eliminate $8,000 in 21 Months and Save $1,900 in Interest

Carrying $8,000 at 22% APR means $1,900 handed to your bank in interest. The top 0% APR balance transfer cards in April 2026 give you 21 months to eliminate that debt completely — with a 3%–5% transfer fee as the only real cost. Here’s what to compare before you apply.

In This Article

WHAT IS 0% APR

What Are 0% APR Cards and How Do They Eliminate Debt?

American households are drowning in credit card debt. According to the Federal Reserve’s latest consumer credit report, the average household now carries $8,347 in credit card balances as of January 2026, with interest rates averaging 22.63% APR. That means you’re paying over $1,800 per year just in interest charges alone.

0% APR balance transfer cards offer a lifeline. These specialized credit cards allow you to transfer your existing high-interest credit card debt and pay zero interest for an introductory period—typically 15 to 21 months. During this interest-free period, every dollar you pay goes directly toward eliminating your principal balance, not lining banks’ pockets with interest fees.

Here’s the math that matters: If you have $8,000 in credit card debt at 22% APR and make $500 monthly payments, you’ll pay $2,847 in interest over 19 months. Transfer that same balance to a 0% APR card, and you eliminate the entire debt in just 16 months while paying zero interest—saving you $2,847 and three months of payments.

How 0% APR cards work:

- You apply for a balance transfer card with an introductory APR offer of 0% for 15-21 months

- Once approved, you initiate a balance transfer from your high-interest cards

- You typically pay a one-time balance transfer fee of 3-5% of the transferred amount

- During the zero interest credit cards promotional period, you aggressively pay down the principal

- You eliminate debt faster without interest compounding against you

The key is having a solid debt payoff plan that ensures you’re debt-free before the 0% period expires.

How Much You’ll Save + Debt Timeline

How Much Money Can You Save with 0% APR Cards?

The savings from 0% APR cards aren’t theoretical—they’re substantial and calculable. Let’s break down exactly how much you’ll save based on your debt level.

Real Debt Elimination Timelines by Amount

$5,000 Debt Scenario: At 22% APR with $300 monthly payments, you’ll pay $791 in interest over 19 months. With a 0% APR card (assuming 3% transfer fee = $150), you save $641 and pay off the balance in 17 months instead.

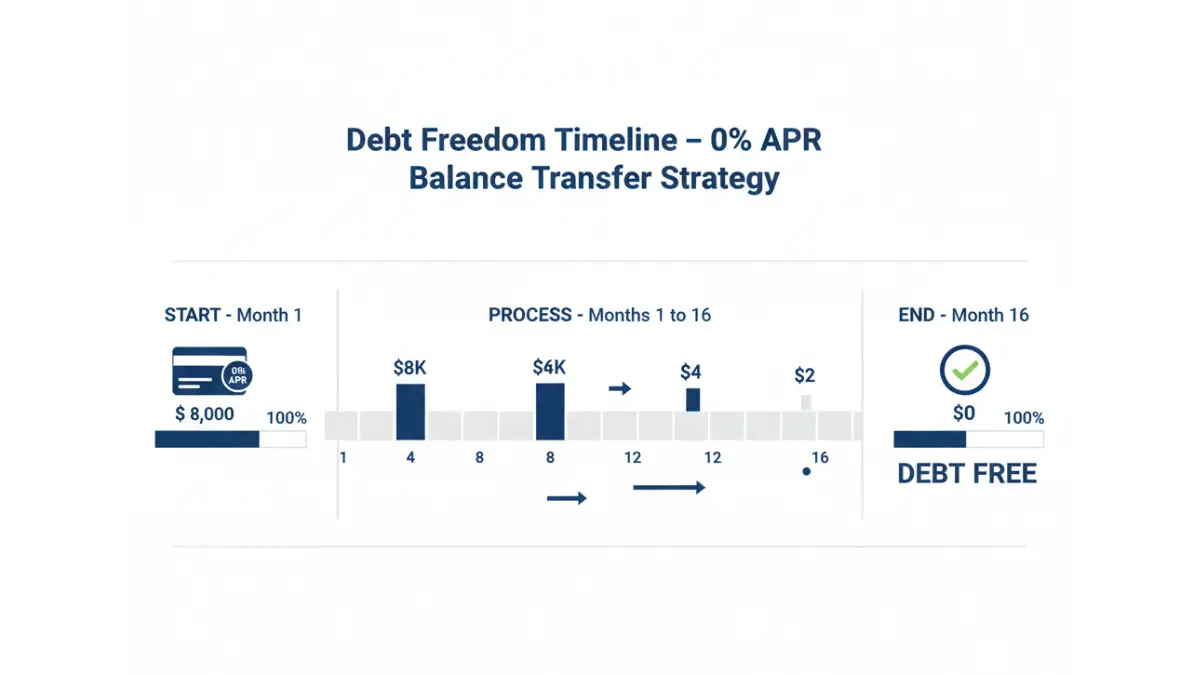

$8,000 Debt Scenario (Most Common): This is where 0% APR cards shine. At 22% APR with $500 monthly payments, you’re looking at $2,847 in interest over 19 months. Transfer to a 0% APR card, pay the $240 balance transfer fee (3% of $8,000), and you eliminate the debt in exactly 16 months while saving $2,607 in net savings.

$15,000 Debt Scenario: At 22% APR with $800 monthly payments, you’ll hemorrhage $5,438 in interest over 22 months. A 0% APR card with 21-month term (transfer fee: $450) lets you pay off credit card debt in 19 months, saving $4,988 net.

Your 16-Month Payoff Timeline for $8,000:

- Month 1: Transfer complete, balance: $8,000

- Months 1-15: Pay $500/month = $7,500 paid

- Month 16: Final payment of $500 = DEBT FREE

- Total paid: $8,240 ($8,000 + $240 fee)

- Total saved vs. 22% APR: $2,607

According to Consumer Financial Protection Bureau data, Americans paid over $130 billion in credit card interest and fees in 2022 alone. Understanding your balance transfer fee structure is critical—while the fee seems like a cost, it’s actually an investment that saves you thousands in interest charges.

Use our Credit Card Payoff Calculator to see your exact savings potential based on your current debt and interest rate.

Top 0% Apr Cards Comparison

Best 0% APR Balance Transfer Cards (January 2026)

Not all 0% APR cards are created equal. Here’s what actually matters: the length of your interest-free period, the balance transfer fee, and your approval probability based on credit score.

Top 5 Cards for Credit Card Consolidation:

| Card Name | 0% APR Period | Balance Transfer Fee | Regular APR | Credit Score Needed |

|---|---|---|---|---|

| Citi® Diamond Preferred® | 21 months | 3% or $5 min | 18.24%-28.99% | 670+ |

| Wells Fargo Reflect® | 21 months | 5% or $5 min | 17.99%-29.99% | 670+ |

| Chase Slate Edge℠ | 18 months | $0 | 19.99%-28.74% | 670+ |

| Discover it® Balance Transfer | 18 months | 3% or $5 min | 16.24%-27.24% | 670+ |

| BankAmericard® | 18 months | 3% or $5 min | 16.24%-26.24% | 670+ |

Our Top Pick: The Citi Diamond Preferred offers the longest introductory APR offer at 21 months, giving you maximum time to eliminate debt. Even with the 3% fee, the extended timeframe provides the most breathing room for larger balances.

Approval Requirements by Credit Score

Your credit score determines your approval odds. According to Experian’s 2026 credit score data, here’s the reality:

- 670-699 (Good): 60-70% approval rate for 0 APR cards

- 700-749 (Very Good): 80-85% approval rate

- 750+ (Excellent): 90-95% approval rate

If your score falls between 620-669, you’re in “Fair” territory. Focus on secured balance transfer options or consider improving your credit score before applying to maximize approval chances.

Bank-Specific Approval Patterns: Chase typically requires 700+ scores and looks for existing banking relationships. Citi is more flexible with 670+ scores. Discover approves fair credit applicants (640+) but may offer shorter 0% periods.

Before applying, check your credit utilization ratio. According to TransUnion research, keeping utilization under 30% significantly improves approval odds, even if your score is borderline.

Step-by-Step Action Plan

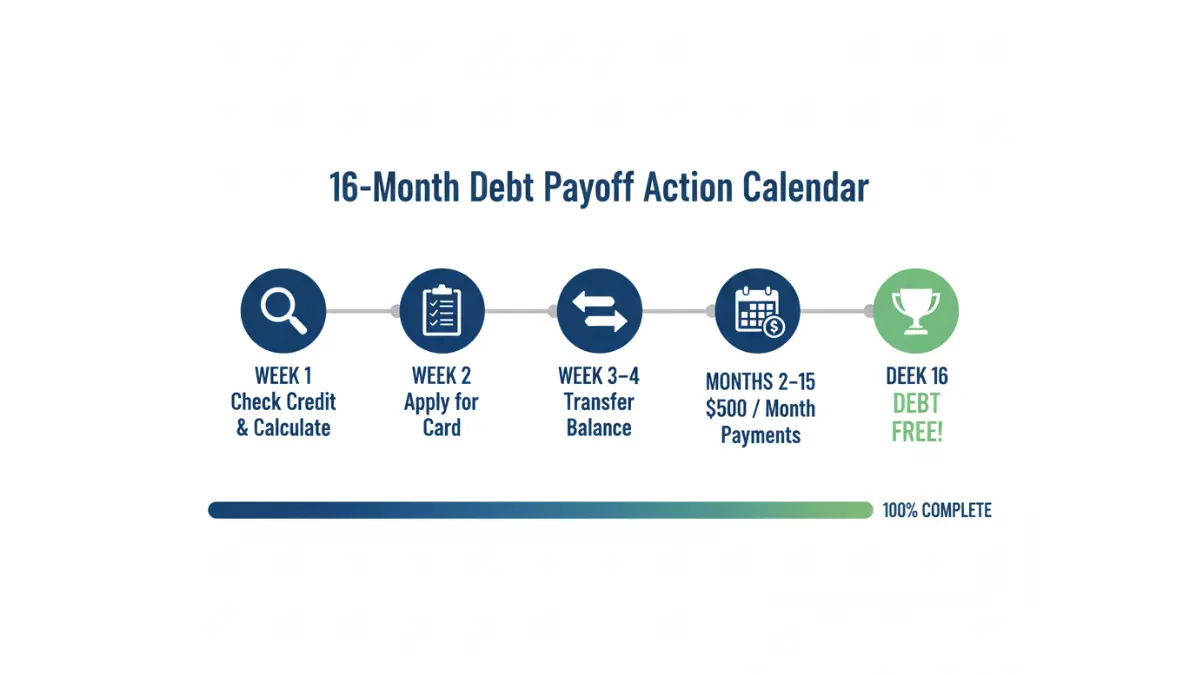

How to Transfer Your Balance and Eliminate Debt (16-Month Plan)

Theory doesn’t pay off debt—action does. Here’s your exact week-by-week protocol to become debt-free in 16 months.

Week-by-Week Action Timeline

Week 1: Calculate & Prepare Pull your credit report (free at AnnualCreditReport.com) and check your score. Calculate your total credit card debt across all accounts. Determine your realistic monthly payment: divide your total debt by 16 months ($8,000 ÷ 16 = $500/month).

Week 2: Compare & Apply Research zero interest credit cards using the comparison table above. Focus on cards offering 18-21 months at 0% APR. Apply for one card only—multiple applications tank your credit score. Monday or Tuesday applications typically process faster than weekend submissions.

Week 3-4: Transfer & Setup Once approved (typically 7-10 days), initiate your balance transfer immediately. Don’t wait. Most issuers require transfers within 60-120 days of account opening to qualify for the 0% rate. Set up automatic payments for $500/month (or your calculated amount) to ensure you never miss a due date.

Months 2-15: Execute & Monitor Make your $500 payment religiously. Avoid using the card for new purchases—most issuers apply payments to promotional balances first, meaning new purchases accrue interest immediately at the regular APR. Track your balance monthly. By month 15, you should have $500 or less remaining.

Month 16: Final Payment Make your last $500 payment and confirm zero balance. Keep the account open to maintain your available credit, which helps your credit utilization ratio and credit score—a strategy detailed in our debt consolidation guide.

Hidden Costs to Watch For

The balance transfer fee isn’t the only cost. Watch for these profit-killers:

- Annual fees: Some 0 APR cards charge $0-$95 yearly—avoid cards with annual fees for debt payoff purposes

- Cash advance fees: 3-5% per transaction plus immediate interest at 29.99% APR

- Late payment penalties: $30-$40 per occurrence, plus your 0% rate can be revoked

- Foreign transaction fees: 3% on international purchases (irrelevant if you’re not using the card for spending)

If you miss a single payment, most issuers can cancel your 0% promotional rate and spike your APR to the penalty rate—often 29.99%. According to the Federal Trade Commission’s credit card rules, this is legal if disclosed in your cardholder agreement.

Emergency fund consideration: While aggressively paying down your debt payoff plan, maintain a $1,000 minimum emergency fund. Without it, unexpected expenses force you back onto high-interest credit, sabotaging your progress.

Advanced Strategies + Common Mistakes

Advanced Debt Elimination Strategies

Basic strategies work for simple situations. These advanced tactics handle complex scenarios that competitors ignore.

The 75% Rule for 0% APR Cards

Never plan to use the full introductory period. Target paying off 100% of your debt in 75% of your available time. For an 18-month 0% period, finish in 13-14 months. For 21 months, finish in 16 months.

Why? Life happens. Job loss, medical emergencies, car repairs—unexpected expenses derail perfectly planned debt payoffs. Building in a 25% time buffer protects you from the catastrophic scenario where your 0% rate expires with a remaining balance, suddenly accruing 24.99% APR on the remainder.

Multiple Card Strategy (For Large Debts)

Have $20,000+ in credit card debt? One card probably won’t cover it. Most balance transfer cards cap transfers at $10,000-$15,000 or your approved credit limit, whichever is lower.

The strategic approach: Apply for your first 0 APR card and transfer your highest-interest debt first. Wait 3-4 months for your credit score to recover from the hard inquiry. Apply for a second card and transfer remaining balances. Stagger your payments to both cards, prioritizing the one with the shorter promotional period.

This technique appears in our snowball vs avalanche comparison, which analyzes optimal multi-debt payoff sequences.

What to Do If You’re Rejected

Rejection isn’t failure—it’s redirection. If denied for a balance transfer card:

- Personal loans: Banks and credit unions offer debt consolidation loans at 8-15% APR—not 0%, but far better than 22%

- Credit counseling: Non-profit agencies can negotiate reduced interest rates directly with creditors

- Secured loans: Home equity lines of credit (HELOCs) offer low rates if you own property

- Score improvement: Focus on the tactics in our credit score guide, then reapply in 6-12 months

Common Mistakes That Kill Success:

- Making only minimum payments during the 0% period (you’ll never pay off the balance)

- Using the card for new purchases (new charges accrue interest immediately)

- Missing a single payment (forfeits your 0% rate permanently)

- Closing your old credit card immediately after the transfer (damages your credit utilization ratio)

- Applying for multiple cards simultaneously (each hard inquiry drops your score 5-10 points)

COMPARISON + Frequently Asked Questions

0% APR Cards vs Other Debt Solutions

Balance transfer cards aren’t your only option for tackling credit card debt. Here’s how alternatives compare.

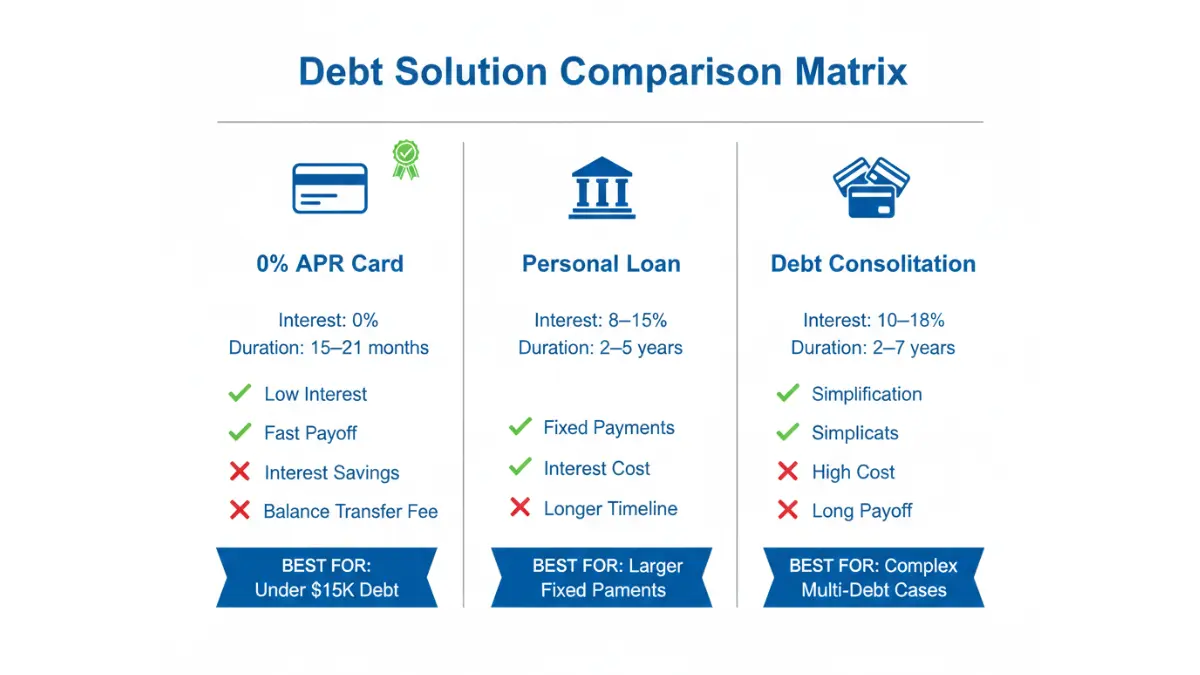

Balance Transfer vs Personal Loan vs Debt Consolidation

| Solution | APR | Term Length | Best For | Drawback |

|---|---|---|---|---|

| 0% APR Card | 0% (15-21 months) | 15-21 months | $3K-$15K debt, good credit | Transfer fee, limited timeframe |

| Personal Loan | 8-15% fixed | 2-5 years | $10K-$35K debt, fixed payments | Interest charges, origination fees |

| Debt Consolidation | 10-18% fixed | 2-7 years | $15K+ debt, multiple creditors | Long payoff, total interest paid |

When each makes sense: Choose balance transfer cards for debts under $15,000 that you can realistically pay off in 16-18 months. The interest-free period creates the fastest, cheapest path to zero balance.

Select personal loans for $10,000-$35,000 in debt when you need a longer, structured repayment plan with fixed monthly payments. The 8-15% rate beats credit cards but costs more than 0% cards.

Consider professional credit card consolidation when debt exceeds $35,000 across multiple creditors, or when you need help negotiating with creditors. Learn more about when this approach works in our debt escape strategies guide.

Frequently Asked Questions

1. How long do 0% APR offers last?

Most introductory APR offers run 15-21 months. Citi Diamond Preferred and Wells Fargo Reflect currently offer the longest terms at 21 months. After the promotional period ends, your rate jumps to the regular APR (typically 18-29%).

2. Will a balance transfer hurt my credit score?

Temporarily, yes. The hard inquiry drops your score 5-10 points, and opening a new account reduces your average account age. However, reducing your credit utilization (by adding available credit) typically offsets these negatives within 3-6 months.

3. Can I transfer a balance from one card to another with the same bank?

No. Banks don’t allow you to transfer balances between their own cards. Chase won’t let you transfer from one Chase card to another Chase card. You must transfer from a different bank’s card.

4. What happens if I don’t pay off the balance before 0% ends?

The remaining balance starts accruing interest at the regular APR (18-29%) from that point forward. The interest doesn’t retroactively apply to the original balance—only to what remains unpaid.

5. How much debt can I transfer?

Your transfer limit equals your approved credit limit or the card’s maximum transfer cap (often $10,000-$15,000), whichever is lower. Some issuers cap transfers at 75% of your credit limit to ensure you have available credit.

6. Can I use a 0% APR card for new purchases?

Technically yes, but you absolutely shouldn’t. Most cards apply payments to the 0% balance first, meaning new purchases immediately accrue interest at the regular APR (22%+). Treat your balance transfer card as debt payoff only.

7. How long does a balance transfer take?

Typically 5-21 days from when you initiate the transfer. During this period, continue making minimum payments on your old card to avoid late fees. The transfer isn’t instant.

8. Do I need excellent credit to get approved?

No, but it helps. Cards with the best terms (21 months, low fees) typically require 670+ scores. Some issuers approve 640+ scores but may offer shorter 0% periods (12-15 months instead of 18-21).

9. Can I transfer multiple credit card balances to one 0% APR card?

Yes, up to your approved credit limit. You can list multiple creditor accounts during the balance transfer request. However, you’ll pay the balance transfer fee (3-5%) on each transfer.

10. Are there any alternatives if I’m rejected for a 0% APR card?

Yes. Consider personal loans (8-15% APR), credit union debt consolidation programs, non-profit credit counseling, or secured loans like HELOCs. Our 30K debt payoff calculator compares multiple debt elimination approaches.

11. Should I close my old credit card after transferring the balance?

No. Keep it open with a zero balance. Closing accounts reduces your total available credit, which increases your credit utilization ratio and can drop your credit score by 20-50 points. Only close if there’s an annual fee you can’t eliminate.

Disclaimer

Important Financial Disclosure: The information provided in this article is for educational purposes only and does not constitute financial, legal, or professional advice. Finance Authority Hub is not a licensed financial advisor, credit counselor, or debt management service.

Credit approval is not guaranteed. Your approval for 0% APR balance transfer cards depends on your individual credit profile, income, existing debt obligations, and the issuing bank’s current lending criteria. Interest rates, promotional periods, and balance transfer fees are subject to change without notice and may vary based on creditworthiness.

Individual results will vary. The debt payoff timelines, savings calculations, and examples presented represent hypothetical scenarios based on the stated assumptions. Your actual savings and payoff timeline will depend on your specific debt amount, APR, monthly payment capacity, and adherence to the repayment plan.

Past performance does not guarantee future results. Historical credit card industry data and consumer debt statistics are provided for informational context and do not predict your personal financial outcomes.

No guaranteed returns or debt elimination. While 0% APR cards offer interest-free promotional periods, successful debt elimination requires consistent monthly payments, financial discipline, and avoiding new debt accumulation. Missing payments can result in loss of promotional rates and additional fees.

Data accuracy: All financial data, interest rates, and card terms are accurate as of January 2026 based on publicly available information from card issuers and government sources. Terms and conditions are subject to change. Always verify current rates and terms directly with card issuers before applying.

Consult a professional: Before making significant financial decisions, consult with a certified financial planner (CFP®), licensed credit counselor, or qualified financial advisor who can evaluate your complete financial situation and provide personalized recommendations.

Credit impact: Applying for credit cards results in hard inquiries that may temporarily lower your credit score. Opening new accounts affects your credit utilization ratio and average account age.

By using the strategies and information in this article, you acknowledge that you are solely responsible for your financial decisions and outcomes. Finance Authority Hub and its contributors assume no liability for financial losses, credit score impacts, or adverse outcomes resulting from the use of this information.

For questions about your specific financial situation, contact a licensed financial professional or certified credit counselor in your area.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.