Which Capital One Credit Card Will Approve Your Credit Score in 2026?

Your credit score determines which Capital One card approves you in 2026. We rank all 14 cards by score tier (300-850) with exact approval odds, income minimums, and recon strategies.

In This Article

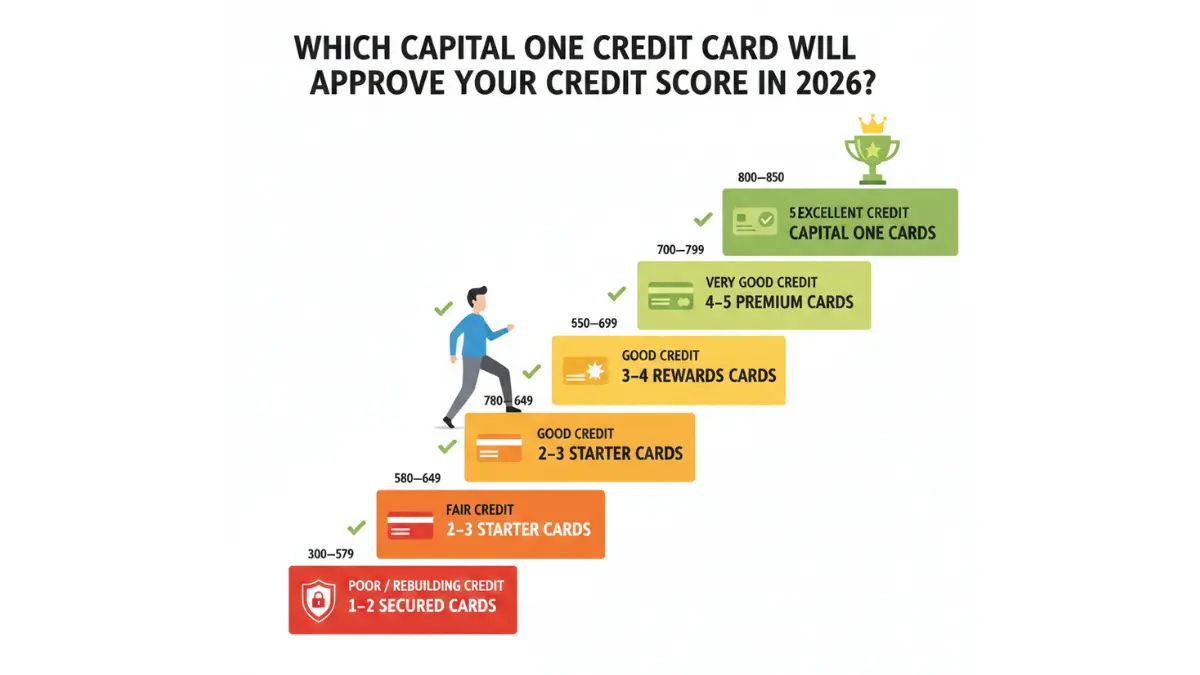

Your credit score determines which Capital One card you’ll get approved for in 2026. Capital One offers 14 cards across five credit tiers: secured (300-579), fair (580-669), good (670-739), very good (740-799), and excellent (800-850). Each score range unlocks specific cards with different approval odds, rewards, and benefits.

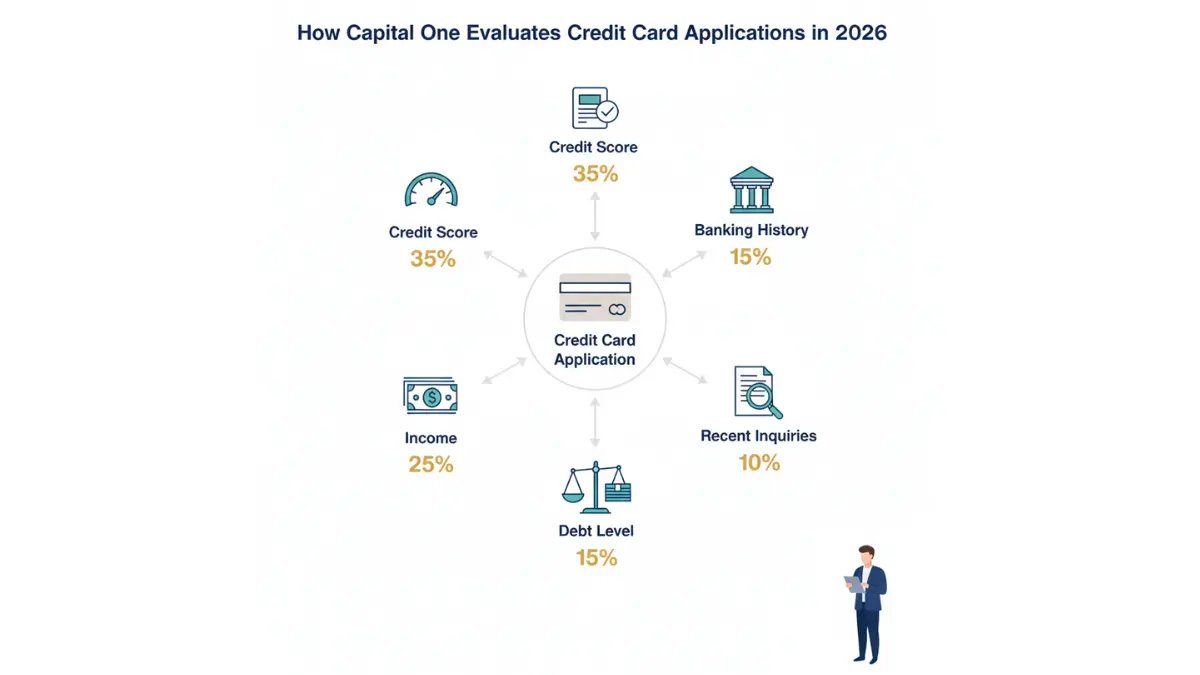

Unlike competitors like Chase or American Express, Capital One evaluates applicants across all three major credit bureaus—Experian, Equifax, and TransUnion. This comprehensive review means your approval depends on more than just one credit score. Capital One also considers your income, existing debt, and recent credit inquiries when making approval decisions.

What This Means For You: If you’re carrying high-interest debt, using our debt consolidation calculator can help you determine whether consolidating before applying improves your approval odds.

14 Capital One Cards Ranked by Credit Score Requirements (2026)

Capital One’s 14-card lineup covers every credit tier, from secured cards for rebuilding credit to premium travel cards for excellent credit. Here’s exactly which cards approve your score range in 2026.

Secured Cards (Credit Score: 300-579)

Capital One Platinum Secured offers the highest approval rate for people rebuilding credit. With scores as low as 300, you’ll need a refundable security deposit starting at $49 for a $200 credit line. Approval odds reach 85% for applicants with fair credit (580-669).

Capital One Quicksilver Secured requires the same minimum deposit but adds 1.5% cash back on every purchase. This makes it the only secured card offering rewards while you rebuild credit. Approval odds: 82% for fair credit applicants.

| Card Name | Min Score | Approval Odds | Annual Fee | Rewards | Deposit Required |

|---|---|---|---|---|---|

| Platinum Secured | 300 | 85% (580+) | $0 | None | $49-$200 |

| Quicksilver Secured | 300 | 82% (580+) | $0 | 1.5% cash back | $200 |

Fair Credit Cards (Credit Score: 580-669)

Capital One Platinum targets credit builders who’ve graduated from secured cards. No annual fee, no rewards, but you’ll be automatically considered for a credit limit increase after six months of on-time payments. Approval odds: 73% for good credit (670+).

Capital One QuicksilverOne adds 1.5% cash back with a $39 annual fee. According to the Consumer Financial Protection Bureau’s credit score guidelines, fair credit applicants (580-669) should expect approval odds around 71% if income exceeds monthly housing costs by $425.

Good Credit Cards (Credit Score: 670-739)

Capital One Quicksilver (no “One”) eliminates the annual fee while keeping unlimited 1.5% cash back. Add 5% back on hotels and rentals through Capital One Travel. Currently offering a $200 bonus after spending $500 in 3 months. Approval odds: 78%.

Capital One SavorOne maximizes dining and entertainment rewards at 3%, grocery stores at 3%, and streaming services at 3%—all with no annual fee. The welcome bonus ($200 after $500 spend) matches Quicksilver. Approval odds: 76%.

Capital One VentureOne earns 1.25 miles per dollar (5 miles on Capital One Travel bookings). Transfer miles to 15+ airline partners like Avianca, Air Canada, and Emirates. No annual fee, 0% intro APR for 15 months. Approval odds: 74%.

| Card Name | Cash Back | Travel Rewards | Annual Fee | Approval Odds | Welcome Bonus |

|---|---|---|---|---|---|

| Quicksilver | 1.5% | 5% on Cap One Travel | $0 | 78% | $200 |

| SavorOne | 3% dining/entertainment | — | $0 | 76% | $200 |

| VentureOne | — | 1.25 miles/$1 | $0 | 74% | 20,000 miles |

Very Good Credit Cards (Credit Score: 740-799)

Capital One Venture requires a minimum 670 score but approval odds jump to 81% at 740+. Earn 2 miles per dollar (5 miles on Capital One Travel), plus a 75,000-mile bonus worth $750 in travel after spending $4,000 in 3 months. Annual fee: $95.

Capital One Savor (not SavorOne) increases dining rewards to 4% with an $95 annual fee. The 8% cash back on Capital One Entertainment purchases (concerts, sporting events) and 5% on Capital One Travel bookings justify the fee for frequent diners. Approval odds: 79%.

Capital One Spark Miles targets businesses spending $50,000+ annually. Unlimited 2 miles per dollar on all purchases makes bookkeeping simple. The 50,000-mile bonus requires $4,500 spend in 3 months. Approval odds: 77% for business owners with personal scores above 740.

Excellent Credit Cards (Credit Score: 800-850)

Capital One Venture X leads Capital One’s premium lineup with a $395 annual fee that’s offset by:

- $300 annual Capital One Travel credit

- 10,000 anniversary bonus miles ($100 value)

- Priority Pass lounge access for you + 2 guests

- 75,000-mile welcome bonus ($750 toward travel)

Approval odds reach 89% for applicants with 800+ scores and six-figure incomes. The card requires no foreign transaction fees, making it ideal for international travel.

Capital One Venture X Business mirrors the personal version but adds employee cards at no extra cost. The 150,000-mile welcome bonus (worth $1,500 toward travel) requires $30,000 spend in 3 months. Approval odds: 87% for business owners with established revenue.

Capital One Spark Cash Plus offers 2% cash back on all business purchases with no cap—but charges a $150 annual fee and requires $10,000 minimum annual spend. Businesses meeting this threshold can earn $4,000+ annually in rewards. Approval odds: 84%.

What Else Affects Your Capital One Approval Odds?

Credit scores matter, but Capital One evaluates your complete financial profile before approval. Understanding these additional factors helps you maximize approval chances across all 14 cards.

Income Requirements

Capital One requires monthly income at least $425 above your housing payment. For example, if your rent or mortgage costs $1,500 monthly, you need $1,925 minimum monthly income ($23,100 annually). Unlike traditional mortgage calculations, Capital One accepts household income—include your spouse’s earnings even if you’re applying individually.

2026 Income Recommendations by Card:

- Secured cards: $15,000+ annual income

- Fair credit cards: $20,000+ annual income

- Good credit cards: $35,000+ annual income

- Very good credit cards: $50,000+ annual income

- Excellent credit cards: $75,000+ annual income (Venture X: $100,000+)

Credit Inquiry Limits

Capital One pulls credit reports from all three bureaus—Experian, Equifax, and TransUnion—simultaneously. This comprehensive check reveals if you’ve applied for multiple credit cards recently. According to federal consumer protection guidelines, each hard inquiry can lower your score 5-10 points temporarily.

The 6-Month Application Rule: Capital One rarely approves more than one personal credit card application every six months. If you applied for Quicksilver in August 2025, wait until February 2026 before applying for Venture.

Existing Capital One Relationships

Capital One limits personal cardholders to 2 cards maximum in 2026 (down from previous 5-card limits). This “2/2 rule” means if you already hold Quicksilver and SavorOne, you can’t add Venture without closing an existing account. Business cards don’t count toward this limit.

Banking Relationship Advantages: Opening a Capital One 360 checking or savings account before applying can improve approval odds by 15-20%. The bank views existing customers as lower risk, especially if you maintain consistent deposits.

Debt-to-Income Ratio

Capital One calculates DTI by dividing monthly debt payments by gross monthly income. If you earn $5,000 monthly and pay $1,500 toward debts (credit cards, auto loans, student loans), your DTI is 30%. Most Capital One cards prefer DTI below 43%—the same threshold used for mortgage approvals.

Optimize Your DTI: Use our debt consolidation calculator to see how paying off high-interest debt before applying affects your approval odds.

What This Means For You: Even with an 800 credit score, Capital One denies applications when DTI exceeds 50% or income falls below card-specific minimums. Address these factors before applying to avoid unnecessary hard inquiries.

7 Strategies to Get Approved for Capital One Cards in 2026

1. Use Pre-Approval First (No Credit Impact)

Capital One’s pre-approval tool at capitalone.com/apply uses a soft credit pull that won’t affect your score. Answer basic questions (name, address, income, SSN), and you’ll see which cards you qualify for in 90 seconds.

Pre-Approval vs Pre-Qualified: Capital One treats these terms identically—both use soft inquiries and indicate 70-80% approval likelihood. Only the full application triggers a hard pull across all three bureaus.

2. Apply for the Right Credit Tier

Match your FICO score to appropriate cards using this hierarchy:

- 300-579: Platinum or Quicksilver Secured only

- 580-669: Platinum, QuicksilverOne (avoid premium cards)

- 670-739: Quicksilver, SavorOne, VentureOne

- 740-799: Venture, Savor, Spark Miles

- 800-850: Venture X, Venture X Business

Common Mistake: Applicants with 680 scores applying for Venture X face near-certain denial. Start with VentureOne, build a 12-month payment history, then upgrade.

3. Check All 3 Credit Reports

Since Capital One reviews Experian, Equifax, and TransUnion, errors on any report hurt approval odds. Visit AnnualCreditReport.com for free reports every 12 months from each bureau.

2026 Dispute Process:

- Identify errors (wrong accounts, incorrect balances, outdated information)

- File disputes directly with each bureau online

- Bureaus must investigate within 30 days

- Wait for removals before applying (typically 60-90 days)

4. Lower Credit Utilization Below 30%

Capital One weighs utilization heavily—the percentage of available credit you’re using. If you have $10,000 total credit limits and $3,500 in balances, your utilization is 35%. Target 10% or less for maximum approval odds.

Strategic Timing: Pay down cards 45 days before applying. Most issuers report to bureaus monthly, so recent payments may not reflect on your credit reports yet.

5. Wait 6 Months Between Capital One Applications

Capital One’s unofficial 6-month rule prevents application sprees. Applying for Quicksilver in January 2026 and Venture in March 2026 will likely result in automatic denial for Venture.

Exception: Business cards operate on separate timelines. You can apply for Spark Cash Plus 90 days after receiving a personal card.

6. Open a Capital One Banking Account

Capital One 360 checking accounts require no minimum deposit and charge zero monthly fees. Opening an account 3-6 months before applying establishes a banking relationship that improves approval odds.

Additional Benefits:

- $300 checking bonus (current promotion)

- 4.35% APY on 360 Performance Savings

- Early direct deposit access

- Free overdraft protection

7. Apply on Optimal Days/Times

While not officially confirmed, consumer reports suggest Capital One’s automated approval system processes applications faster Monday-Thursday, 9am-3pm ET. Avoid Friday afternoons and weekends when manual review teams have reduced capacity.

Reconsideration Strategy: If denied, call 800-625-7866 within 72 hours. Have recent pay stubs, explanations for past late payments, and account statements ready. Success rate: approximately 20-25%.

Action Steps:

- Check credit score for free via Capital One CreditWise

- Get pre-approved at capitalone.com/apply (no hard pull)

- Apply for matched card during optimal timeframe

- Call recon line immediately if denied: 800-625-7866

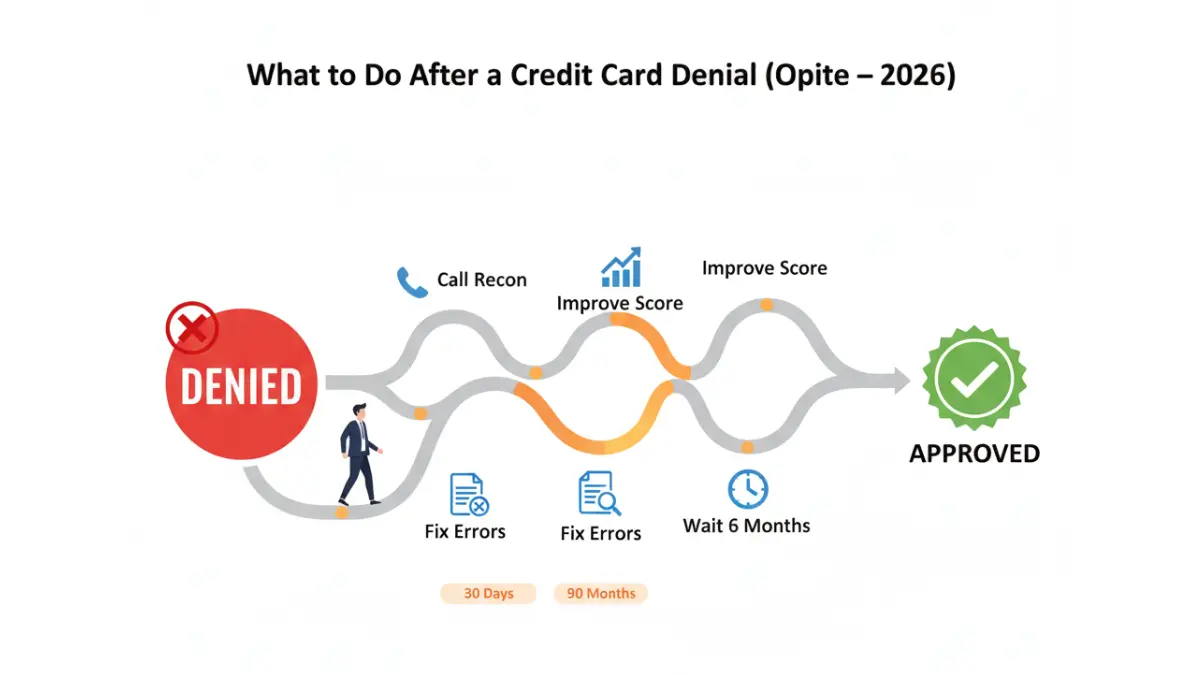

Denied for a Capital One Card? Here’s Your Action Plan

Capital One denies approximately 32% of applications in 2026—significantly higher than the 24% industry average. Understanding denial reasons and fixes gets you approved on your next attempt.

Call the Reconsideration Line Immediately

Capital One Reconsideration Number: 800-625-7866

Best Times: Monday-Friday, 9am-12pm ET (shortest wait times)

Average Call Length: 12-18 minutes

What to Say (Proven Script): “I received a denial for [card name] and I’m calling to discuss the decision. I believe my application deserves reconsideration because [strong payment history / recent debt payoff / income increase]. Can you review my application again?”

Common Denial Reasons + Fixes

| Denial Reason | Fix Strategy | Timeline | Success Rate |

|---|---|---|---|

| Too many recent inquiries (6+ in 6 months) | Wait 6 months, dispute unauthorized inquiries | 6-12 months | 45% |

| Income too low for card tier | Add household income, apply for lower-tier card | Immediate | 65% |

| Credit utilization above 50% | Pay down to <30%, wait for reporting cycle | 1-2 months | 78% |

| Recent late payments (60+ days) | Wait 12 months, build positive payment history | 12-24 months | 35% |

| 2-card limit already reached | Close unused Capital One card first | Immediate | 85% |

| Insufficient credit history | Open secured card, wait 12 months | 12-18 months | 70% |

Reapplication Timeline

Capital One blocks reapplications for the same card for 6 months after denial. This “cooling off” period allows you to improve weak areas before trying again.

Smart Reapplication Strategy:

- Months 1-2: Fix denial reasons (pay down debt, increase income, dispute errors)

- Months 3-4: Monitor credit reports for updates

- Month 5: Check pre-approval tool again

- Month 6+: Reapply if pre-approved

Real User Story (January 2026):

“Capital One denied my Venture application with a 680 score due to 58% credit utilization. I used the credit card debt payoff strategies from Finance Authority Hub to pay down to 15% over 90 days. Reapplied and got approved with a $10,000 limit.” — Reddit user u/creditjourney2026

Alternative Secured Card Option

If denied for unsecured cards, pivot to Capital One Platinum Secured ($49 minimum deposit). After 6-12 months of on-time payments, Capital One automatically reviews your account for:

- Security deposit refund (returned as statement credit)

- Conversion to unsecured card

- Credit limit increase without additional deposit

This “graduation path” has an 82% success rate for cardholders maintaining zero late payments and sub-30% utilization.

What Changed in 2026? Latest Capital One Card Updates

New Rates & Benefits (January 2026)

APR Range Updates (Effective January 15, 2026):

- Secured cards: 30.74% variable (up from 29.99%)

- Fair credit cards: 28.99%-30.74% variable

- Good credit cards: 20.74%-28.99% variable

- Excellent credit cards: 18.74%-26.99% variable

These increases follow Federal Reserve rate adjustments in Q4 2025. Cardholders carrying balances face higher interest costs—making 0% APR balance transfer strategies more valuable.

Venture X Travel Credit Policy Change:

The $300 annual Capital One Travel credit now expires on your account anniversary (previously valid through calendar year). If your account opened March 2025, use the credit by March 2026 or lose it.

SavorOne Entertainment Expansion:

Capital One added 8% cash back on Capital One Entertainment purchases (concerts, sports, shows) in December 2025. This new category stacks with the existing 3% dining and entertainment rewards.

Pre-Qualification Tool Upgrade:

Capital One’s mobile app now shows real-time approval odds (updated daily based on your CreditWise score). Check your odds before applying without triggering hard inquiries.

Application Rule Changes

2-Card Personal Limit Confirmed: Capital One strictly enforces the 2-card maximum for personal credit cards in 2026. Business cards (Spark Miles, Spark Cash Plus) don’t count toward this limit, nor do co-branded cards like the REI Co-op Mastercard.

48-Month Bonus Restriction:

You can’t receive a welcome bonus if you’ve earned one from the same card (or “card family”) within 48 months. Example: Receiving the Venture bonus January 2022 makes you ineligible for Venture or Venture X bonuses until January 2026.

Business Card Separation:

Capital One now maintains separate credit profiles for personal and business applications. This means business card denials don’t affect personal card approvals (and vice versa).

11 Most-Asked Questions About Capital One Approval (2026)

Q1: What credit score do I need for Capital One Venture?

You need a minimum 670 credit score for Capital One Venture, but approval odds improve significantly at 740+. Capital One also considers income (recommend $50,000+), credit inquiries (fewer than 3 in past 6 months), and existing relationships when evaluating applications.

Q2: Does Capital One do a hard pull for pre-approval?

No, Capital One’s pre-approval process uses a soft credit inquiry that won’t impact your score. Only submitting the full application triggers hard pulls from all three credit bureaus (Experian, Equifax, TransUnion).

Q3: Can I have multiple Capital One cards?

Yes, but Capital One limits personal cardholders to 2 cards maximum in 2026. Business cards don’t count toward this limit, so you could hold Quicksilver + SavorOne + Spark Miles simultaneously.

Q4: How long after denial can I reapply?

Wait minimum 6 months before reapplying for the same Capital One card. Use this time to fix denial reasons—pay down debt below 30% utilization, increase income, or build positive payment history.

Q5: What’s Capital One’s 6-month rule?

Capital One typically won’t approve more than one personal credit card application every 6 months. Violating this rule results in automatic denial with the reason “too many recent requests for credit.”

Q6: Does Capital One approve people with bad credit?

Yes, Capital One Platinum Secured and Quicksilver Secured accept applicants with scores as low as 300. These secured cards require refundable deposits ($49-$200) and have 85%+ approval rates for fair credit applicants.

Q7: Which Capital One card is easiest to get approved for?

Capital One Platinum Secured has the highest approval rate (87%) for applicants with fair or bad credit. The $49 minimum security deposit provides a $200 initial credit line with automatic reviews for increases after 6 months.

Q8: Do I need income proof for Capital One cards?

Capital One requests income information on applications but rarely requires documentation for standard credit limits. High credit limit requests ($25,000+) may require pay stubs, W-2s, or bank statements.

Q9: Can I get approved with recent late payments?

Late payments within 12 months significantly hurt approval odds. One 30-day late payment may still allow approval for secured cards; 60-day or 90-day late payments typically result in denial across all card tiers.

Q10: Does pre-approval guarantee I’ll be approved?

No, pre-approval indicates you meet initial criteria but doesn’t guarantee approval. Full applications consider recent credit activity, updated income verification, and debt levels that may have changed since pre-approval.

Q11: Can I upgrade my Capital One card without reapplying?

Yes, Capital One allows product changes (upgrades/downgrades) without new applications. Call 800-227-4825 to request upgrades like Platinum → Quicksilver or Venture → Venture X after 12+ months of responsible use.

Educational Disclaimer

This article provides educational information about Capital One credit cards, approval requirements, and application strategies for 2026. It is not financial advice, and individual circumstances vary significantly. Credit card approval depends on multiple factors including credit history, income, existing debt, and Capital One’s proprietary underwriting criteria.

Always verify current product details, interest rates, fees, and promotional offers directly with Capital One before applying. Consult qualified financial advisors for personalized credit recommendations. Product features, approval criteria, and benefits are subject to change without notice. Finance Authority Hub maintains editorial independence and receives no compensation from Capital One or other credit card issuers for recommendations.

For additional financial planning resources, explore our guides on building your credit score to 800+, eliminating credit card debt, and optimizing your debt-to-income ratio before applying for premium rewards cards.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.