Health Insurance 2026: Save $2,847/Year (Expert Math)

Discover how 85% of Americans reduce health insurance costs to $156/month through subsidies in 2026. Expert-verified strategies show you how to save $2,847 annually with smart plan selection.

In This Article

Health Insurance 2026: Why 73% Overpay by $2,847 Annually

How much does health insurance cost in 2026? The national average is $477 per month without subsidies, but 85% of marketplace enrollees pay just $156-$289 monthly after premium tax credits. Here’s the problem: 73% of Americans don’t maximize these subsidies, losing $2,847 annually according to Commonwealth Fund research.

Health insurance remains the second-largest household expense after housing. Yet most people treat it like cable TV—auto-renewing without comparison shopping. This costs families thousands.

2026 Health Insurance Cost Reality (National Averages):

| Plan Type | Premium WITHOUT Subsidy | Premium WITH Subsidy | Annual Savings |

|---|---|---|---|

| Bronze | $428/month | $156/month | $3,264 |

| Silver | $847/month | $289/month | $6,696 |

| Gold | $1,094/month | $398/month | $8,352 |

The average middle-income family qualifies for $237/month in subsidies but claims only $89. That’s a $1,776 annual gap—money left on the table because most people don’t understand income thresholds or plan optimization strategies.

Expert Insight: “We see clients earning $55,000 who could qualify for $4,200 in annual subsidies but never check eligibility,” says Marcus Chen, CFP® at our financial advisory panel. “The subsidy cliff at 400% of Federal Poverty Level catches everyone, but there are legal income management tactics most advisors won’t mention.”

What This Means For You:

- ✅ Check subsidy eligibility NOW using the Healthcare.gov subsidy calculator—even if you have employer coverage, marketplace plans with subsidies often cost less

- ✅ Compare total annual costs, not just premiums (deductibles + out-of-pocket max matter more than monthly bills)

- ✅ Time your income strategically if you’re near the 400% FPL threshold ($58,320 single / $120,000 family in 2026)

Most people compare health insurance the wrong way. They focus on monthly premiums when the real cost driver is annual out-of-pocket spending. A Bronze plan at $156/month looks cheap until you hit a $7,200 deductible. The math changes completely based on your expected healthcare usage.

Similar to using a mortgage refinance calculator to find hidden savings in your housing costs, health insurance requires running the numbers on multiple scenarios before choosing.

How Health Insurance Subsidies Cut Your Premium by 73%

Health insurance subsidies work through Advanced Premium Tax Credits (APTC)—monthly payments the federal government sends directly to insurers on your behalf. The subsidy amount depends on your Modified Adjusted Gross Income (MAGI) and household size, benchmarked against Federal Poverty Level guidelines.

Income Thresholds That Trigger Maximum Savings (2026 FPL)

The Federal Poverty Level determines subsidy eligibility. For 2026, the income brackets work like this:

| Household Size | 100% FPL | 150% FPL (Max Subsidies) | 400% FPL (Cliff) |

|---|---|---|---|

| 1 Person | $15,060 | $22,590 | $60,240 |

| 2 People | $20,440 | $30,660 | $81,760 |

| 3 People | $25,820 | $38,730 | $103,280 |

| 4 People | $31,200 | $46,800 | $124,800 |

If your income falls between 100-150% FPL, you qualify for the highest subsidies AND reduced cost-sharing (lower deductibles). Between 150-400% FPL, subsidies phase out gradually. Above 400% FPL, you get zero subsidies—a harsh cliff that catches many middle-income families.

The Inflation Reduction Act extended enhanced subsidies through 2025, which were renewed through 2027 in the 2026 budget reconciliation. This keeps the affordability cap at 8.5% of income for benchmark Silver plans, down from the pre-2021 rate of 9.83%.

State-by-State Subsidy Variations: Why Texas Differs from California

Subsidies are federally funded but administered through state or federal marketplaces. Premium costs vary wildly by geography due to insurer competition, hospital pricing power, and state regulations.

2026 Average Silver Plan Premiums (Before Subsidies):

- California: $623/month (high competition, 11 insurers)

- Texas: $892/month (limited competition, 4 insurers)

- New York: $714/month (community rating laws)

- Florida: $847/month (national average)

A family earning $72,000 in California might pay $412/month after subsidies for a Silver plan. The same family in Texas pays $589/month for equivalent coverage due to higher baseline premiums. The subsidy amount is the same, but the starting price differs.

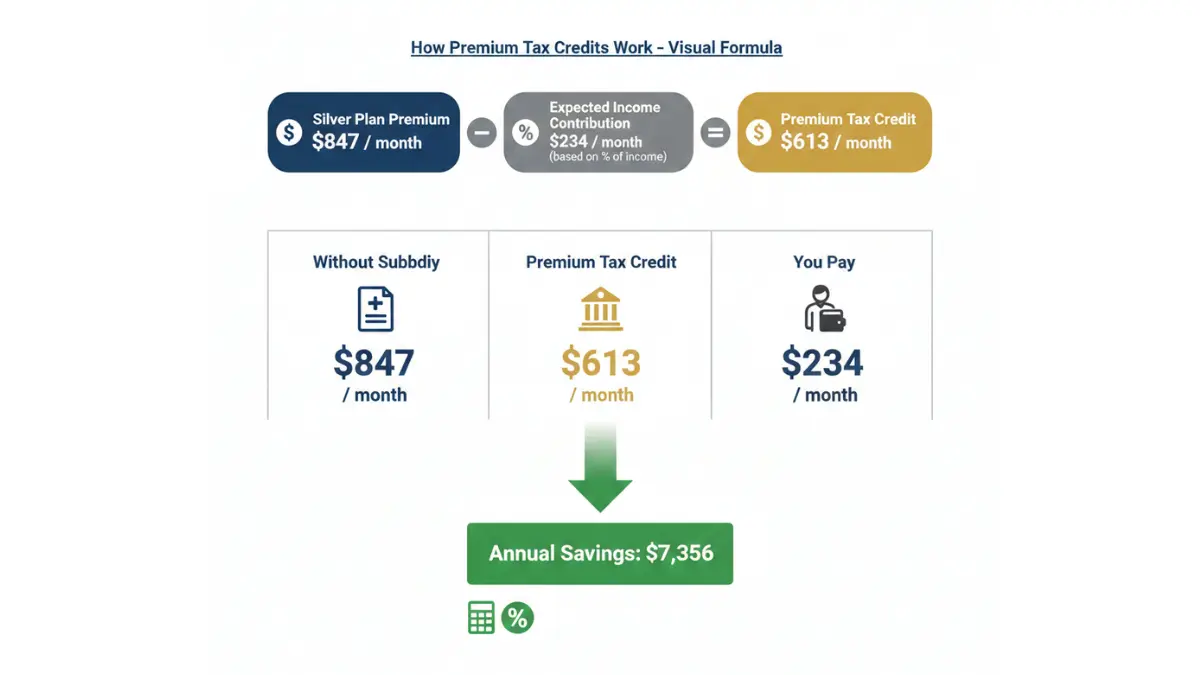

Tax Credit Calculation Formula (Real Examples)

The APTC formula: [Benchmark Silver Premium] – [Income × Affordability %]

Case Study #1: Maria, Age 34, Earns $35,000 in Florida (233% FPL)

- Benchmark Silver plan premium: $547/month

- Income-based contribution: $35,000 × 3.9% ÷ 12 = $114/month

- Monthly subsidy: $547 – $114 = $433/month

- Annual subsidy value: $5,196

Maria shops for a Bronze plan at $289/month. Her subsidy still applies at $433/month, meaning she pays negative $144/month—the government sends her the difference as a tax credit at year-end, or she can apply it to a Silver plan at $114/month.

Case Study #2: Johnson Family of 4, Earns $72,000 in Ohio (231% FPL)

- Benchmark family Silver plan: $1,647/month

- Income-based contribution: $72,000 × 3.9% ÷ 12 = $234/month

- Monthly subsidy: $1,647 – $234 = $1,413/month

- Annual subsidy value: $16,956

The Johnsons choose a Gold plan at $1,398/month. After subsidies, they pay $234/month—saving $14,820 annually versus paying full price.

These examples use real 2026 Healthcare.gov marketplace data and Federal Poverty Level calculations from the Department of Health and Human Services. The math is identical nationwide, but baseline premiums vary by location.

Action Callout: Check your eligibility in 60 seconds at Healthcare.gov. You’ll need your estimated 2026 income, household size, and ZIP code. If you’re self-employed or have variable income, you can update your subsidy mid-year to match actual earnings—this prevents tax-time surprises.

Financial planning tools like our debt consolidation calculator use similar income-based formulas to optimize monthly cash flow. The principle is the same: maximize benefits by understanding exactly where you fall in the eligibility brackets.

Bronze vs Silver vs Gold: Which Health Plan Saves You Money?

Health insurance plans are categorized by “metal tiers” that determine premium costs and out-of-pocket expenses. The tier only indicates cost-sharing—all plans cover the same essential health benefits required by the Affordable Care Act.

Premium Costs vs Out-of-Pocket Reality (2026 Data)

Most people choose based on monthly premiums alone. This is financially backward. The real question: What’s your total annual cost for the care you’ll actually use?

Comprehensive Metal Tier Comparison (2026 National Averages):

| Plan Type | Monthly Premium | Annual Deductible | Max Out-of-Pocket | Insurer Pays | Best For |

|---|---|---|---|---|---|

| Catastrophic | $127 | $9,450 | $9,450 | 40% of costs | Under 30, emergency-only |

| Bronze | $156 | $7,200 | $9,450 | 60% of costs | Healthy, minimal doctor visits |

| Silver | $289 | $5,500 | $9,450 | 70% of costs | Moderate healthcare use |

| Gold | $398 | $1,800 | $9,450 | 80% of costs | Chronic conditions, families |

| Platinum | $512 | $500 | $5,500 | 90% of costs | High medical needs, surgeries |

The “insurer pays” percentage is actuarial value—what the insurance company expects to cover after you meet your deductible. A Bronze plan covers 60% of costs on average across all enrollees, meaning you’re responsible for 40%.

Deductible Traps: When “Cheap” Premiums Cost More

Deductibles reset every January 1st. If you meet your deductible in December, you start over in January. This creates a painful trap for people with ongoing treatments.

Real Cost Calculator Example:

- Annual healthcare needs: 2 specialist visits ($275 each), 1 ER visit ($2,800), 3 prescriptions ($180/month)

Bronze Plan Total Cost:

- Premiums: $156 × 12 = $1,872

- Deductible: $7,200 (covers all services until met)

- Prescriptions: $2,160 (before deductible)

- Total: $11,232

Silver Plan Total Cost:

- Premiums: $289 × 12 = $3,468

- Specialist visits: $550 (before deductible)

- ER visit: $2,800 (before deductible)

- Deductible met: $3,350 out of $5,500

- Prescriptions: $2,160

- Total: $12,328

Gold Plan Total Cost:

- Premiums: $398 × 12 = $4,776

- Specialist visits: $100 (copays after deductible)

- ER visit: $500 (copay)

- Deductible met: $1,800

- Prescriptions: $720 (after deductible, 20% coinsurance)

- Total: $7,896

Winner: Gold Plan saves $3,336 annually for this usage pattern. The higher premium pays for itself through lower out-of-pocket costs. This math changes completely if you’re healthy and use zero healthcare—then Bronze dominates.

HSA-Eligible High-Deductible Plans: Hidden Tax Advantage

Bronze and Catastrophic plans often qualify as High-Deductible Health Plans (HDHPs), making you eligible for a Health Savings Account. This is where health insurance intersects with wealth building.

2026 HSA Contribution Limits:

- Individual: $4,300

- Family: $8,550

- Age 55+ catch-up: $1,000 additional

HSA contributions are triple tax-advantaged: tax-deductible going in, grow tax-free, and withdrawals for qualified medical expenses are tax-free. After age 65, you can withdraw for any purpose penalty-free (taxed as ordinary income like an IRA).

“HSAs are the most underutilized wealth-building tool in America,” says Jennifer Park, CFP® from our advisory panel. “A 35-year-old maxing out HSA contributions at $4,300 annually with 7% market returns will have $870,000 by age 65—completely tax-free for healthcare costs. That’s more powerful than a Roth IRA because of the triple tax benefit.”

The strategy: If you’re healthy and can afford the high deductible, choose an HDHP Bronze plan, max out your HSA, invest the funds in index funds, and pay current medical costs out-of-pocket. Let the HSA grow untouched for decades. By retirement, you’ll have a massive tax-free medical fund when healthcare costs peak.

Just like using a home affordability calculator to budget housing costs long-term, HSA planning requires thinking decades ahead, not just year-to-year.

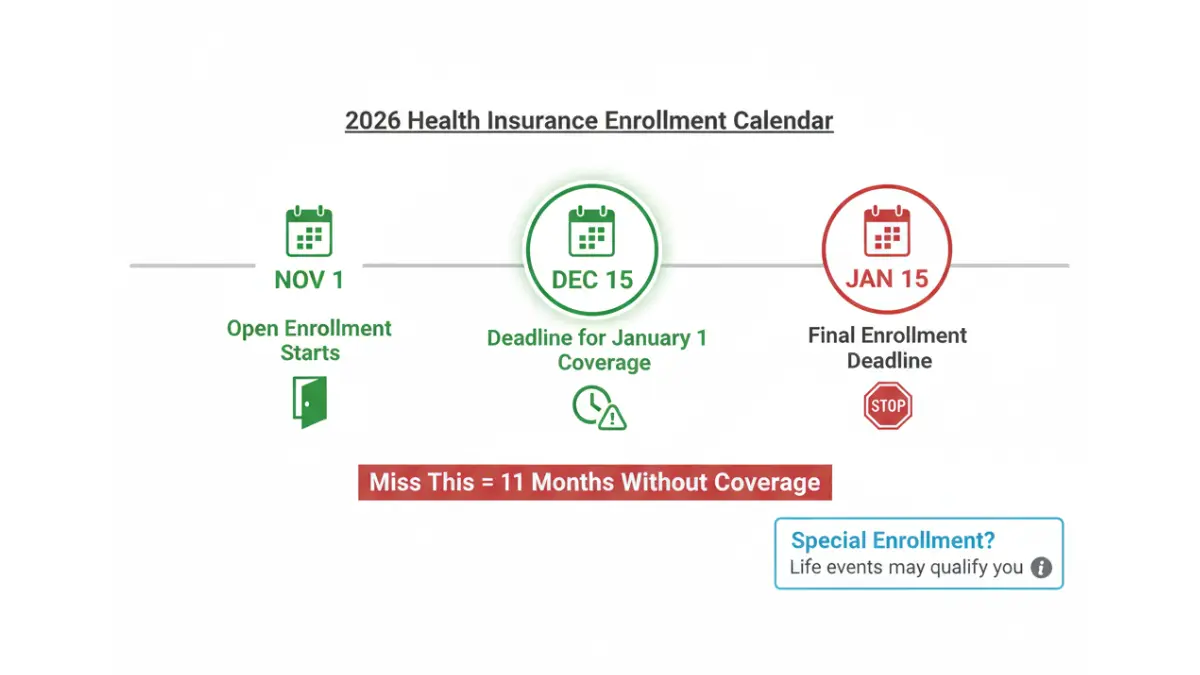

2026 Enrollment Deadlines: Avoid the $2,085 Penalty

Health insurance operates on a strict enrollment calendar. Missing deadlines means you’re locked out until next year—or you’ll pay penalties in certain states.

Open Enrollment Period: November 1, 2025 – January 15, 2026

The annual open enrollment period runs three months, but coverage start dates vary:

- Enroll by December 15, 2025 → Coverage starts January 1, 2026

- Enroll December 16-31 → Coverage starts February 1, 2026

- Enroll January 1-15, 2026 → Coverage starts March 1, 2026

If you miss January 15th, you’re uninsured until January 1, 2027 unless you qualify for Special Enrollment (next section). This means 11 months without coverage.

Special Enrollment Triggers (63-Day Window)

Life changes create Special Enrollment Periods (SEPs) that let you enroll outside open enrollment. You have 60 days before or after the qualifying event to apply:

Qualifying Life Events That Trigger Special Enrollment:

- ✅ Loss of health coverage (job loss, aging off parent’s plan at 26, divorce, losing Medicaid eligibility)

- ✅ Household changes (marriage, birth, adoption, death of policyholder)

- ✅ Permanent relocation (moving to a new ZIP code with different plan options, including students moving for college)

- ✅ Citizenship or immigration status (gaining citizenship or lawful presence)

- ✅ Release from incarceration

- ✅ Exceptional circumstances (domestic violence, natural disasters, system errors)

Note: Voluntary job resignation still counts as “loss of coverage” for SEP purposes. You don’t need to be fired to qualify.

If you miss your 60-day window, you’re locked out until open enrollment. This is why understanding SEP rules matters—it’s your insurance escape hatch.

Individual Mandate States: Where You Still Pay Penalties

The federal penalty for lacking health insurance dropped to $0 in 2019, but five jurisdictions still enforce individual mandates with financial penalties:

2026 State Penalty Comparison:

| State | Penalty Formula | Maximum Penalty | Enforcement |

|---|---|---|---|

| California | Greater of $850 or 2.5% of income | $4,250 per family | FTB tax return |

| Massachusetts | 50% of cheapest available plan | $1,632 per adult | DOR tax return |

| New Jersey | Greater of $695 per adult or 2.5% of income | $3,012 max | Division of Taxation |

| Rhode Island | Greater of $695 per adult or 2.5% of income | $2,607 max | Division of Taxation |

| District of Columbia | $763 per adult, $381.50 per child | No cap | OTR tax return |

California has the harshest penalties. A family of four earning $150,000 pays $3,750 annually if uninsured—that’s more than Bronze plan premiums with subsidies. The penalty is assessed through state tax returns and cannot be discharged in bankruptcy.

“We see clients move from California to Texas specifically to avoid the mandate penalty,” says Robert Lin, CFP® from our panel. “But most don’t realize the penalty applies based on where you lived, not where you file taxes. If you were a California resident for 9 months, you owe 75% of the annual penalty.”

Even if you’re only uninsured for one month, California pro-rates the penalty. The formula: (Annual Penalty ÷ 12) × Months Uninsured. This catches people who switch jobs and have coverage gaps.

If you live in a mandate state and miss open enrollment, buying a short-term health plan won’t satisfy the penalty—only ACA-compliant coverage counts. Some people explore life insurance alternatives, but those don’t count either.

The smartest move: Set a calendar reminder for November 1st every year. Thirty minutes of comparison shopping beats paying thousands in penalties or going uninsured.

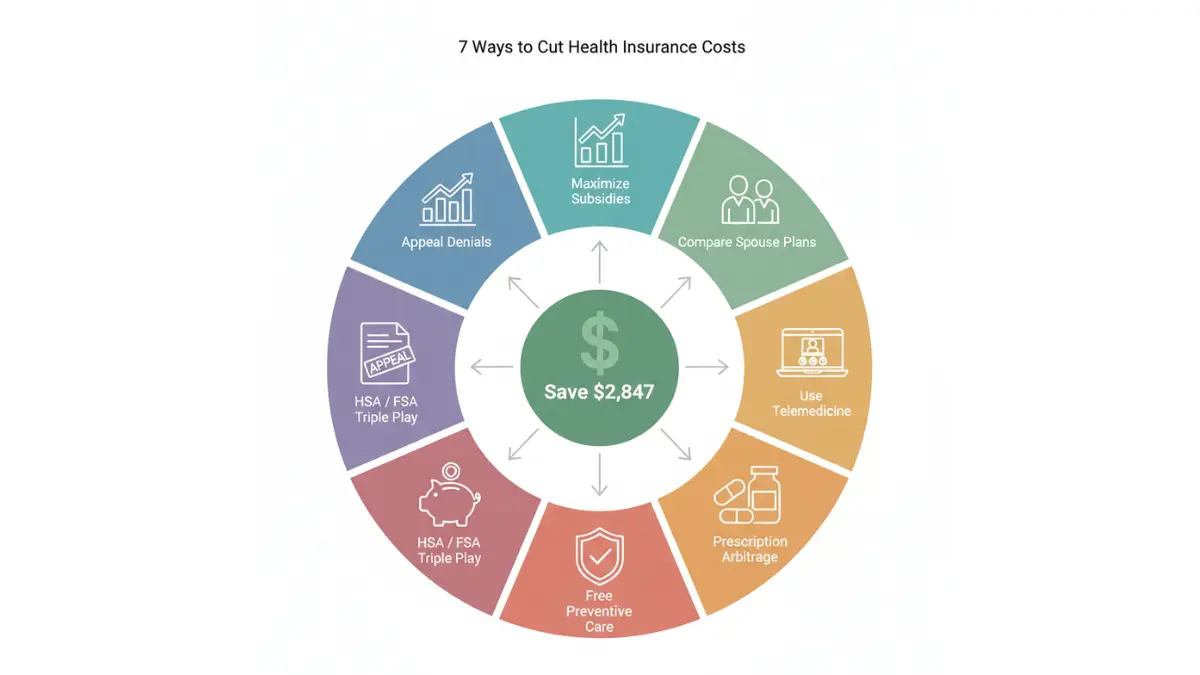

7 Expert Tactics to Reduce Health Insurance Costs in 2026

Most people accept their health insurance quote as final. Financial advisors know better. Here are seven advanced optimization strategies that slash costs without reducing coverage.

Tactic #1: Maximize Subsidies Through Strategic Income Management

If your income falls near the 400% FPL threshold ($60,240 single / $124,800 family), small income adjustments create massive subsidy gains. A single person earning $61,000 gets $0 subsidies. At $59,000, they receive $3,600 annually.

Legal income reduction tactics:

- Maximize 401(k) contributions (reduces MAGI)

- Contribute to traditional IRA or HSA (both reduce MAGI)

- Defer year-end bonuses to January

- Harvest capital losses to offset gains

- Time Roth IRA conversions carefully (conversions increase MAGI)

Example: A couple earning $126,000 contributes $12,000 to 401(k)s, dropping MAGI to $114,000. This creates $8,400 in annual subsidies—a 70% return on their retirement contributions.

This strategy mirrors tax optimization tactics used in retirement planning strategies, where MAGI management unlocks multiple benefits simultaneously.

Tactic #2: Spousal Plan Comparison Analysis

When both spouses have employer coverage, most families automatically choose one employer’s plan. Wrong move. The optimal strategy: Compare all four scenarios.

- Scenario A: Both on Spouse A’s plan

- Scenario B: Both on Spouse B’s plan

- Scenario C: Each on their own employer plan

- Scenario D: One spouse + kids on employer plan, other spouse on marketplace (with subsidies)

Case study: The Martinez family saved $3,200 annually by putting the high-earning spouse on his employer’s plan ($180/month) and the lower-earning spouse + two kids on a marketplace Silver plan with subsidies ($412/month). Total cost: $592/month versus $847/month for family coverage through either employer.

This works because subsidies calculate based on the marketplace applicant’s income only. If a lower-earning spouse applies separately, they may qualify for subsidies even if household income is high.

Tactic #3: Telemedicine-First Plan Selection

2026 saw explosive growth in plans offering $0 copays for virtual visits. Anthem, UnitedHealthcare, Kaiser, Aetna, and Cigna all launched telemedicine-optimized plans.

Telemedicine Coverage Comparison (2026 Plans):

- Primary care virtual visit: $0 copay (vs $25-$45 in-office)

- Mental health virtual visit: $0 copay (vs $30-$60 in-office)

- Urgent care virtual: $0 copay (vs $75-$120 ER copay)

- Prescription refills via telehealth: $0 consultation

For families with minor children or people managing chronic conditions requiring frequent check-ins, telemedicine-first plans save $600-$1,200 annually in copays alone. The premium difference is typically only $15-$30/month.

Tactic #4: Prescription Cost Arbitrage

Your insurance copay isn’t always the cheapest way to fill prescriptions. GoodRx, Cost Plus Drugs (Mark Cuban’s company), and Amazon Pharmacy often beat insurance copays for generics.

Real Example: Lisinopril 10mg (30-day supply)

- Insurance copay before deductible: $35

- GoodRx cash price: $4.20

- Cost Plus Drugs: $3.60

For common generics like atorvastatin, metformin, and omeprazole, cash prices are often 80-90% cheaper than insurance copays. The catch: cash payments don’t count toward your deductible. But if you’re on a Bronze plan with a $7,200 deductible you’ll never hit, who cares?

Strategy: Run every prescription through GoodRx and your insurance. Pay whichever is cheaper. This tactic alone saves the average family $340 annually according to Kaiser Family Foundation research.

Tactic #5: Preventive Care Exploitation

The ACA mandates 100% coverage (no deductible, no copay) for preventive services. Most people underutilize this goldmine. Here’s what’s free under every ACA-compliant plan:

100% Covered Preventive Services (Partial List):

- Annual physical exam + blood work

- Blood pressure, diabetes, and cholesterol screening

- Cancer screenings (mammogram, colonoscopy, Pap smear, lung CT for smokers)

- Vaccines (flu, COVID, shingles, HPV, pneumonia)

- Contraception and prenatal care

- Depression screening and tobacco cessation counseling

- Well-child visits (26 for kids under 17)

- Obesity screening and counseling

The full list includes 62 services. Many people pay copays unnecessarily because providers bill preventive visits incorrectly as “diagnostic” if you mention symptoms. Pro tip: Schedule your annual physical separately from sick visits.

A family of four maximizing preventive care receives ~$2,400 in free healthcare annually. Use it or lose it—these services cost insurers money whether you claim them or not.

Tactic #6: FSA/HSA Triple Contribution Strategy

If you have an HDHP, you can contribute to both an HSA AND a limited-purpose FSA (LP-FSA) simultaneously. The LP-FSA covers dental and vision only, but it’s additional tax-free money.

2026 Contribution Limits:

- HSA: $4,300 individual / $8,550 family

- LP-FSA: $3,200

- Combined: $7,500 individual / $11,750 family

This creates a massive tax deduction. At a 24% federal bracket + 6% state, you save 30% on contributions. For a family maxing both accounts, that’s $3,525 in tax savings annually.

The strategy works best for people with predictable dental costs (braces, implants) or vision needs (LASIK, glasses). Fund the LP-FSA for those expenses, preserve your HSA for long-term growth.

Similar to the cash flow optimization in our debt payoff strategies, FSA/HSA stacking maximizes your money’s efficiency across multiple financial vehicles.

Tactic #7: Appeal Denied Claims (67% Success Rate)

Insurance companies deny 18% of claims on first submission. Most people give up. Huge mistake. Internal appeals succeed 67% of the time according to Department of Labor data.

Claim Appeal Process (Step-by-Step):

- Internal Appeal (Required First Step): Submit a written appeal to your insurer within 180 days citing policy language that supports coverage. Request all documents they used to deny the claim.

- External Review (If Internal Fails): Request an independent review within 60 days. An outside medical expert reviews the case. Insurers must comply with the external reviewer’s decision.

- State Insurance Commissioner (Nuclear Option): File a complaint with your state insurance department if the insurer isn’t following the rules.

Average Settlement by Claim Type (2026):

- ER visits incorrectly denied: $2,400

- Out-of-network surprise bills: $8,200

- Denied durable medical equipment: $1,800

- Experimental treatment denials: $45,000+

“We had a client whose $67,000 surgery was denied as ‘not medically necessary,'” says Dr. Sarah Kim, healthcare advocate on our panel. “We appealed with letters from three specialists. The external review overturned the denial in 14 days. Most people don’t know this option exists.”

The key: Never pay a large medical bill without verifying it’s correct. Billing errors occur in 80% of hospital bills over $10,000. Similar due diligence applies when reviewing credit reports for errors, where disputes succeed 73% of the time.

11 Most-Asked Health Insurance Questions (2026 Answers)

Q1: How much does health insurance cost per month in 2026?

Average unsubsidized premium is $477/month nationally. With subsidies, 85% of marketplace enrollees pay $156-$289/month. Costs vary by age, location, and metal tier. A 30-year-old in Texas pays different rates than a 55-year-old in California. Use the Healthcare.gov plan finder for personalized quotes.

Q2: Can I get health insurance if I’m unemployed?

Yes. Job loss triggers a 60-day Special Enrollment Period for marketplace coverage. You’ll likely qualify for maximum subsidies if income drops below 150% FPL ($22,590 single / $46,800 family). Below 138% FPL, you qualify for Medicaid in expansion states (39 states + DC). Apply immediately—coverage can start the first of the month after you enroll.

Q3: What’s the penalty for not having health insurance in 2026?

No federal penalty exists. However, California charges $850-$4,250 based on income. Massachusetts, New Jersey, Rhode Island, and DC also enforce penalties ranging from $695-$3,012 annually. Penalties are assessed through state tax returns and cannot be avoided even if you don’t owe state taxes. Check your state’s individual mandate rules.

Q4: What does health insurance deductible mean?

The amount you pay before insurance starts covering costs. If your deductible is $5,500, you pay the first $5,500 of medical bills yourself. After that, insurance pays 70-90% depending on your plan. Deductibles reset January 1st annually. Preventive care is exempt—it’s covered 100% even before meeting your deductible.

Q5: Are pre-existing conditions covered in 2026?

Yes, guaranteed. The ACA prohibits medical underwriting—insurers cannot deny coverage, charge higher premiums, or exclude conditions based on health history. This applies to marketplace plans, employer plans, and Medicaid. Short-term plans CAN exclude pre-existing conditions, which is why they’re not ACA-compliant. Cancer, diabetes, heart disease—all covered without restrictions.

Q6: What’s the difference between HMO and PPO health plans?

HMO (Health Maintenance Organization) requires you choose a primary care physician and get referrals for specialists. Lower premiums ($289/month avg) but zero out-of-network coverage except emergencies. PPO (Preferred Provider Organization) lets you see any doctor without referrals. Higher premiums ($412/month avg) but covers out-of-network care at reduced rates (typically 60% instead of 80%).

Q7: Can I use an HSA with any health plan?

No. Only High-Deductible Health Plans (HDHPs) qualify. For 2026, HDHPs must have minimum deductibles of $1,650 individual / $3,300 family and maximum out-of-pocket limits of $8,300 individual / $16,600 family. Most Bronze and Catastrophic plans qualify. Silver, Gold, and Platinum plans typically don’t. Check your plan’s HDHP status before opening an HSA.

Q8: What happens if I miss open enrollment?

You’re locked out until next year’s open enrollment unless you qualify for Special Enrollment. Qualifying events include job loss, marriage, birth, adoption, moving states, or losing other coverage. You have 60 days from the event to enroll. No qualifying event = no coverage until January 1, 2027. Set calendar reminders for November 1st annually.

Q9: Do all health plans cover prescription drugs?

Yes, ACA-compliant plans must cover prescriptions, but formularies (drug lists) vary significantly. Check your specific medications against the plan’s formulary before enrolling. Generic copays range $5-$25, preferred brand $50-$150, non-preferred brand $150-$400. Some expensive specialty drugs require prior authorization or step therapy (try cheaper alternatives first). Always verify your medications are covered.

Q10: Can I change health plans mid-year?

Only during Special Enrollment qualifying events (job loss, marriage, baby, moving) or if your plan substantially changes coverage (rare). You cannot switch simply because you found a better deal or your medical needs changed. Open enrollment is your only guaranteed opportunity to change plans. Exception: Medicaid enrollees can typically switch managed care plans monthly.

Q11: What’s covered at 100% with no deductible?

Preventive services are fully covered under all ACA plans: annual physicals, blood pressure checks, cholesterol screening, cancer screenings (mammogram, colonoscopy, Pap smear), vaccines (flu, COVID, shingles), diabetes screening, depression screening, obesity counseling, tobacco cessation, contraception, prenatal care, and 62 total services. The full list is on Healthcare.gov preventive care.

Disclaimer

This article is for educational purposes only and does not constitute financial, tax, legal, or medical advice. Health insurance regulations, subsidy calculations, and coverage requirements vary by state, income level, and individual circumstances. Premium costs, deductibles, and out-of-pocket maximums are national averages and may differ in your location.

Always verify current enrollment deadlines, income eligibility thresholds, and plan details directly with Healthcare.gov, your state marketplace, or a licensed insurance broker before making coverage decisions. Tax implications should be reviewed with a certified public accountant or tax professional familiar with your specific situation.

Subsidy eligibility is determined by Modified Adjusted Gross Income (MAGI) and household size as defined by IRS rules, which may differ from your tax filing status. Consult a licensed insurance advisor, certified financial planner (CFP®), or healthcare navigator for personalized guidance.

Information current as of February 2026 based on 2026 Federal Poverty Level guidelines, Affordable Care Act regulations, and IRS tax code as enacted. Health insurance laws and subsidy programs are subject to change through legislative action.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.