Medicare Advantage Plans 2026: What’s Actually Changing

Over 2.6 million Americans lost their Medicare Advantage plan in 2026. Here’s what changed, which plans are best, and exactly what to do before your next enrollment window.

In This Article

Over 2.6 million Americans just lost their Medicare Advantage plan heading into 2026 — nearly double the terminations from the year before. At the same time, a landmark new rule caps your prescription drug costs at $2,100 for the entire year. If you haven’t checked your coverage status yet, you may be paying for a plan that no longer fits — or missing out on the biggest Medicare drug benefit in a decade.

This expert guide breaks down every major change to Medicare Advantage plans in 2026, ranks the best options by category, and tells you exactly what to do next.

⚡ Quick Facts — Medicare Advantage 2026 at a Glance

- 🏥 34M+ Americans enrolled in Medicare Advantage plans

- 💊 New $2,100 drug cap — you pay $0 after hitting this limit

- 💲 67% of plans charge no extra monthly premium

- 📉 3,373 plans available nationally — down 9% from 2025

- ⚠️ 2.6 million enrollees had their plan terminated for 2026

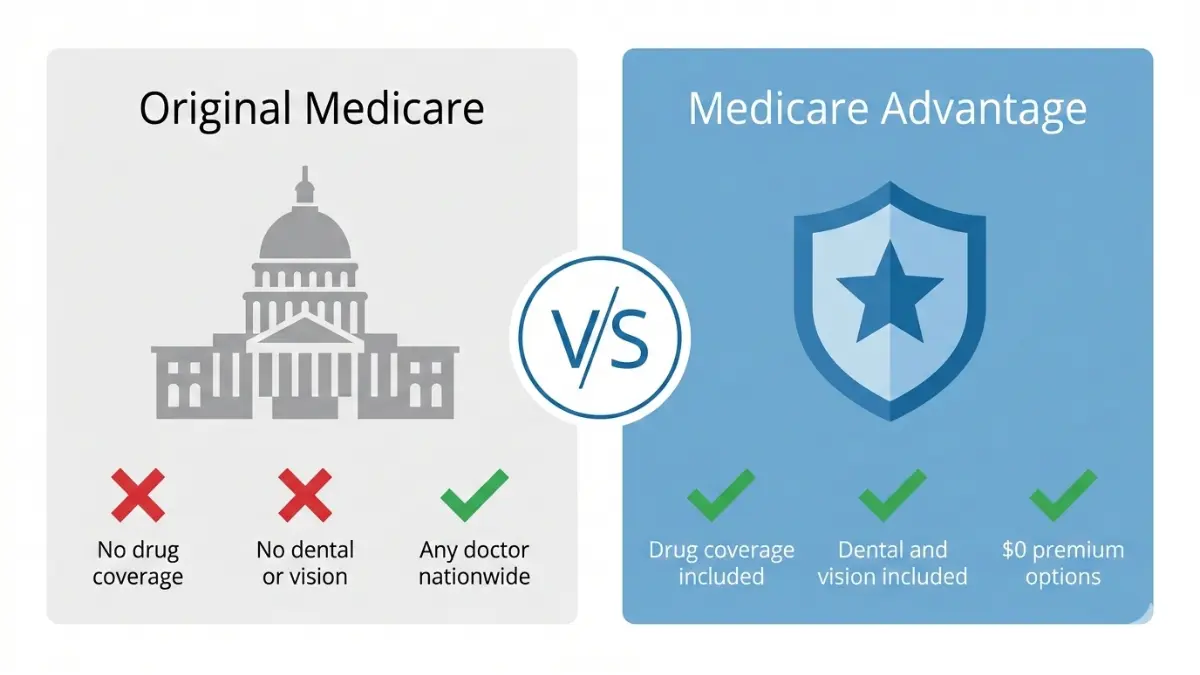

What Is a Medicare Advantage Plan and How Does It Work in 2026?

Medicare Advantage — also called Medicare Part C — is a private insurance alternative to Original Medicare. It bundles your Part A (hospital), Part B (medical), and usually Part D (prescription drugs) into a single plan offered by a private, government-approved insurer.

Important: Medicare Advantage replaces Original Medicare — it does not supplement it. You must still pay the mandatory Part B premium of $202.90/month in 2026 regardless of which plan you choose.

Medicare Advantage vs. Original Medicare — 2026 Comparison

| Factor | Original Medicare | Medicare Advantage |

|---|---|---|

| Monthly Premium | $202.90 (Part B only) | $202.90 + plan premium (often $0 extra) |

| Provider Network | Any Medicare-accepting doctor in the US | Limited to in-network providers |

| Drug Coverage (Part D) | Not included — must buy separately | Included in most plans (89%) |

| Extra Benefits | None | Dental, vision, hearing, fitness, OTC allowance |

| Out-of-Pocket Cap | No cap | Capped (varies by plan) |

| Drug Cost Cap | $2,100 (new 2026 rule) | $2,100 (new 2026 rule) |

Types of Medicare Advantage Plans

- HMO (Health Maintenance Organization) — Must use in-network doctors; requires primary care physician referrals; lowest cost

- PPO (Preferred Provider Organization) — More flexibility; can see out-of-network doctors at higher cost

- SNP (Special Needs Plan) — Designed for people with chronic conditions, low income, or institutional care needs

- PFFS (Private Fee-for-Service) — Set rates for any provider who accepts terms

Who Is Eligible?

- Enrolled in Medicare Part A and Part B

- Age 65+, or under 65 with qualifying disability

- Live in the plan’s service area

According to Medicare.gov’s official plan comparison tool, over 98% of Medicare beneficiaries have access to at least one $0-premium Medicare Advantage plan in 2026. If you’re also managing retirement finances, our retirement savings by age guide shows how healthcare costs fit into your long-term financial picture.

5 Major Changes to Medicare Advantage Plans in 2026

This is the section your competitors missed entirely. Here’s what’s actually different in 2026 — with real data, not fluff.

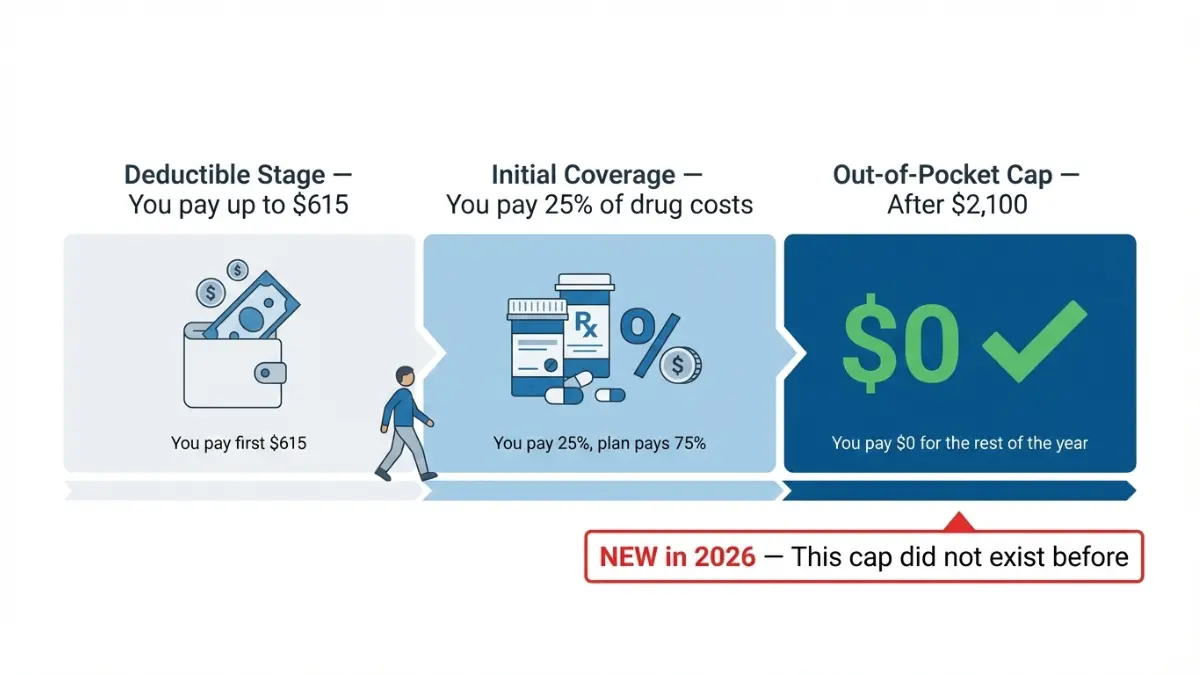

Change #1: The New $2,100 Prescription Drug Out-of-Pocket Cap

This is the biggest Medicare drug benefit change in over a decade — and almost no one is talking about it clearly.

How it works: Once your out-of-pocket spending on covered Part D drugs reaches $2,100 in 2026, you pay $0 for the rest of the year. This applies automatically to all Medicare Advantage plans that include Part D drug coverage.

Real example: You take a brand-name diabetes medication and a cholesterol drug. By June, you’ve spent $2,100 on prescriptions. From July through December — every refill costs you nothing.

According to Medicare.gov’s official Part D cost page, the maximum drug deductible in 2026 is also capped at $615, and some plans offer no deductible at all.

✅ What This Means For You: If you take multiple medications, this cap could save you thousands of dollars compared to 2025 rules. Check your plan’s formulary to confirm your drugs are covered.

Change #2: 2.6 Million Enrollees Lost Their Plan — Are You One of Them?

This is the crisis hidden in plain sight. According to KFF’s Medicare Advantage 2026 analysis, about 13% of individual Medicare Advantage enrollees are in a plan terminated for 2026 — nearly double the 1.3 million who faced terminations in 2025.

What happens if your plan was terminated:

- You received an Annual Notice of Change (ANOC) letter in September 2025 — check your mail

- You have a Special Enrollment Period to choose a new plan

- If you take no action, you’re automatically moved to Original Medicare — with no drug coverage

⚠️ Action Step: Go to Medicare’s Plan Finder right now, enter your ZIP code, and confirm your current coverage is still active for 2026.

Change #3: UnitedHealthcare and Humana Pulled Out of Hundreds of Counties

The two largest Medicare Advantage insurers made major market exits. According to KFF’s data:

- UnitedHealthcare exited 225 counties while entering only 14 new ones

- Humana exited 198 counties while entering just 5 new ones

- Both insurers now offer plans in roughly 80% of US counties, down from nearly 90% in 2025

This matters because Medicare Advantage plans are approved on a county-by-county basis. Your ZIP code determines everything — plan availability, cost, and network.

✅ What This Means For You: Even if your insurer is still operating nationally, your specific county may have lost plan options. Always verify by ZIP code, not by insurer name alone.

Change #4: Medicare-Negotiated Drug Prices Now in Effect

Starting January 1, 2026, Medicare’s negotiated prices for the first 10 high-cost brand-name drugs took effect. As confirmed by Medicare.gov’s drug plan guide, these negotiated prices apply to Part D coverage within Medicare Advantage plans.

The negotiated drugs include treatments for blood thinners, diabetes, and heart disease — conditions affecting tens of millions of Medicare beneficiaries.

✅ What This Means For You: If you take any of the 10 negotiated drugs, your out-of-pocket costs may be lower in 2026. Contact your plan directly for specifics on how pricing applies to you.

Change #5: New Provider Directory Rules + A New Special Enrollment Period

CMS introduced new rules requiring all Medicare Advantage Organizations to update their provider directories within 30 days of any network change and submit accurate data to Medicare’s Plan Finder.

Additionally, if you enrolled through Medicare Plan Finder and your doctor turns out to be out-of-network within three months, you qualify for a new Special Enrollment Period to switch plans. This protection is new for 2026 and applies only to enrollments made through Medicare Plan Finder.

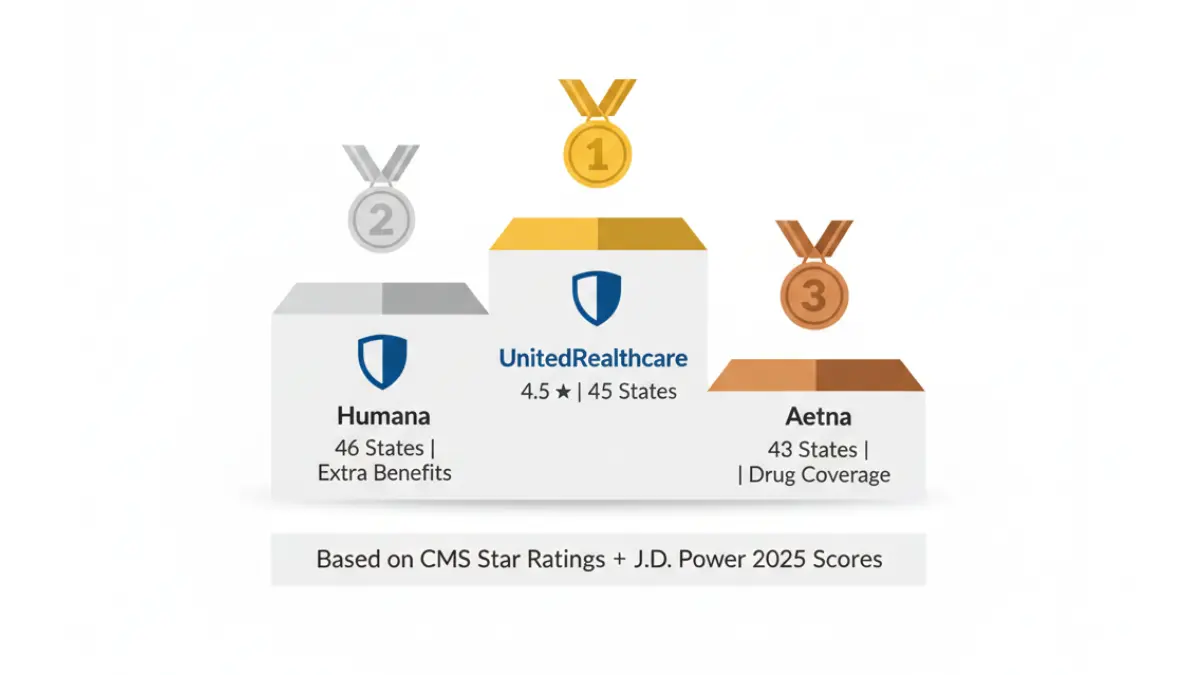

Best Medicare Advantage Plans 2026 — Expert Ranked by Category

Our expert panel evaluated plans based on CMS Star Ratings, J.D. Power customer satisfaction scores, $0 premium availability, network size, and drug coverage quality. Here are the top performers.

2026 Top Medicare Advantage Plans — Master Rankings Table

| Plan | Best For | CMS Stars | $0 Premium | States Available |

|---|---|---|---|---|

| UnitedHealthcare | Largest network | 4.0–4.5 ⭐ | ✅ 45 states | 94% of US counties |

| Aetna (CVS Health) | Drug coverage & low cost | 3.0–4.0 ⭐ | ✅ 43 states | 88% in 4+ star plans |

| Humana | Extra benefits & wellness | 3.5–5.0 ⭐ | ✅ 46 states | 85% of US counties |

| Kaiser Permanente | Highest quality ratings | ⭐⭐⭐⭐⭐ | Varies | Select states only |

| Devoted Health | Best emerging option | 4.0+ ⭐ | ✅ 29 states | Growing rapidly |

| BCBS (Anthem/Highmark) | Local trust & networks | 3.5–4.0 ⭐ | Varies by state | State-by-state |

Note on star ratings: According to KFF’s analysis of 2026 CMS data, 34 Medicare Advantage plans earned 5 stars for 2026 — up from just 7 plans in 2025.

Best Medicare Advantage Plan by Health Condition

No competitor ranks plans by health need. Here’s your personalized edge.

| Health Condition | Best Plan Type | Key Feature to Prioritize |

|---|---|---|

| Diabetes | MA-PD with strong Part D | Insulin $35/month cap, continuous glucose monitor coverage |

| Heart Disease | PPO with large cardiology network | Specialist access without referral |

| Cancer | C-SNP (Chronic Condition Special Needs Plan) | Extra hospital days, oncology network |

| Low Income / Dual Eligible | D-SNP (Dual Eligible Special Needs Plan) | Coordinates Medicare + Medicaid, $0 cost-sharing possible |

| Frequent Travelers | PPO or PFFS | Out-of-network emergency coverage across US |

If you’re also managing insurance costs broadly, our guide on health insurance expert math for 2026 shows how Medicare Advantage stacks up against other coverage options in retirement.

What About Dental, Vision, and Hearing?

Original Medicare covers none of these. Medicare Advantage plans cover all three.

According to KFF’s 2026 benefits spotlight, virtually all Medicare Advantage plans (98%+) offer dental, vision, and hearing benefits in 2026. If your dental costs are also a concern, see our dental insurance 2026 guide to understand what MA dental actually covers vs. standalone policies.

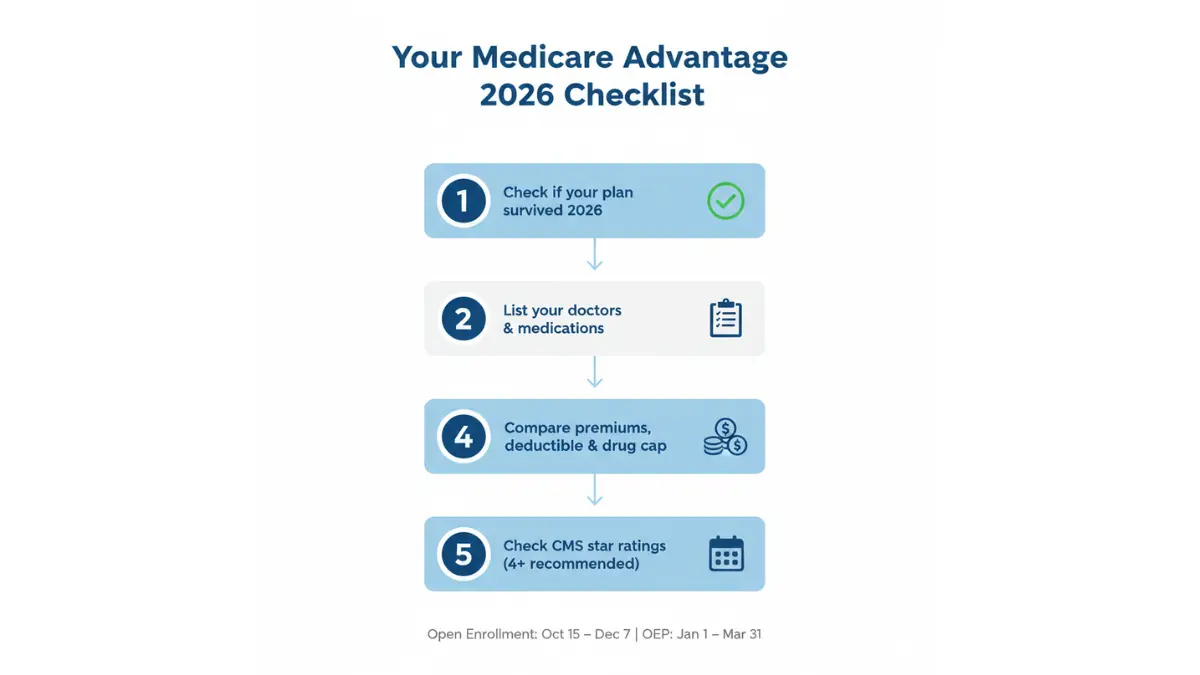

How to Choose the Right Medicare Advantage Plan in 2026

Don’t pick a plan based on brand name or TV ads. Here is the exact 5-step framework used by Medicare advisors.

Step 1: Verify Your Current Plan Is Still Active

Go to Medicare.gov Plan Compare, enter your ZIP code, and confirm your plan exists for 2026. If it doesn’t appear, you need to act immediately.

Step 2: List Your Doctors and Medications Before Comparing Plans

- Write down every doctor, specialist, and hospital you use

- List every prescription drug, including dosage

- Filter plans on Medicare Plan Finder by “my drugs” and “my doctors” to check coverage

Step 3: Compare These 5 Cost Factors — Table Format

| Cost Factor | 2026 Average | What to Watch For |

|---|---|---|

| Monthly Premium | ~$14.00 avg (CMS estimate) | Many plans = $0 extra beyond Part B |

| Part B Premium | $202.90/month | Required for ALL enrollees |

| Drug Deductible | Up to $615 max | Look for $0 deductible plans |

| Drug Out-of-Pocket Cap | $2,100 (NEW for 2026) | After this, you pay $0 for drugs |

| Plan Out-of-Pocket Max | Varies widely | Your most critical financial protection |

Step 4: Check CMS Star Ratings

- 5 stars — Exceptional; best quality and member experience

- 4–4.5 stars — Excellent; recommended for most enrollees

- 3–3.5 stars — Average; check specifics carefully

- 2 stars or below — Avoid; CMS flags these as underperforming

Step 5: Enroll During the Right Window

| Enrollment Period | Dates | What You Can Do |

|---|---|---|

| Annual Enrollment | Oct 15 – Dec 7 | Join, switch, or drop any plan |

| Medicare Advantage OEP | Jan 1 – Mar 31 | Switch MA plans or return to Original Medicare |

| Special Enrollment | Varies by qualifying event | If plan terminated, you moved, or you qualify for SEP |

As you plan retirement finances, it helps to see the full picture. Our retirement planning guide for your 30s and 401(k) explained guide help you integrate healthcare cost planning with long-term investment strategy.

Medicare Advantage vs. Original Medicare — Is It Worth It in 2026?

This is the question every new enrollee asks. Here’s a direct, honest answer.

When Medicare Advantage Makes More Sense

- You want $0 or low monthly premium beyond Part B

- You want dental, vision, and hearing coverage included

- You use a limited set of doctors who are in-network

- You take regular prescriptions and benefit from the $2,100 drug cap

- You want one single card for all coverage

When Original Medicare Makes More Sense

- You travel frequently and need nationwide provider freedom

- You have complex health needs requiring frequent specialist access

- You prefer no referral requirements for specialists

- You’re willing to buy a separate Medigap supplement for cost protection

Bottom Line: For most American seniors on a fixed income, Medicare Advantage plans offer better value in 2026 — especially with the new drug cap. The trade-off is a narrower provider network. Always verify your specific doctors and prescriptions are covered before enrolling.

Managing overall costs in retirement is a multi-part equation. If you’re balancing housing costs alongside healthcare, our home affordability calculator and reverse mortgage 2026 guide are useful resources for seniors evaluating housing and healthcare simultaneously.

Frequently Asked Questions — Medicare Advantage Plans 2026

Q1: What is the best Medicare Advantage plan in 2026?

UnitedHealthcare offers the largest national network covering 94% of US counties, while Kaiser Permanente leads in 5-star quality ratings. The best plan depends entirely on your location, doctors, and medications — there is no single universal “best.”

Q2: What are the biggest changes to Medicare Advantage in 2026?

Three changes stand out: the new $2,100 prescription drug out-of-pocket cap, a dramatic increase in plan terminations affecting 2.6 million enrollees, and Medicare-negotiated drug prices taking effect January 1, 2026.

Q3: Is Medicare Advantage worth it in 2026?

For most seniors, yes. 67% of plans charge no extra monthly premium, and the new drug cap provides significant financial protection. The main trade-off is a restricted provider network.

Q4: What happens if my Medicare Advantage plan was terminated for 2026?

You receive a Special Enrollment Period to choose a new plan. If you take no action, you’re automatically enrolled in Original Medicare without drug coverage. Act immediately by visiting Medicare.gov’s plan compare tool.

Q5: How many Medicare Advantage plans are available in 2026?

Nationally, 3,373 plans are available — a 9% decrease from 2025. The average beneficiary can choose from 32 plans with drug coverage, according to KFF’s 2026 plan offerings analysis.

Q6: What is the $2,100 drug cap exactly?

Once your out-of-pocket spending on covered Part D prescription drugs reaches $2,100 in 2026, you pay $0 for all covered drugs for the rest of the calendar year. This applies to all Medicare Advantage plans with Part D coverage. Medicare.gov confirms this cap applies universally regardless of which plan you’re enrolled in.

Q7: Can I switch Medicare Advantage plans in 2026?

Yes — during the Open Enrollment Period (January 1–March 31) you can switch plans or return to Original Medicare. Annual Enrollment (October 15–December 7) allows the broadest changes. Special Enrollment Periods apply if your plan was terminated.

Q8: What is the Medicare Advantage out-of-pocket maximum in 2026?

It varies by plan. CMS sets a legal maximum limit, but each plan sets its own cap below that. Always compare the out-of-pocket maximum — it’s the most important financial protection in any plan.

Q9: Which Medicare Advantage plans have 5-star ratings in 2026?

34 plans earned 5-star CMS ratings for 2026, up dramatically from just 7 in 2025. Kaiser Permanente accounts for 5 of those five-star designations. View the full CMS star ratings list at cms.gov for complete details.

Q10: Does Medicare Advantage cover dental, vision, and hearing?

Yes — 98%+ of Medicare Advantage plans in 2026 include dental, vision, and hearing benefits. Original Medicare covers none of these. For standalone dental coverage comparison, see our dental insurance 2026 guide.

Q11: What’s the Part B premium for Medicare Advantage enrollees in 2026?

All Medicare Advantage enrollees must still pay the Medicare Part B premium of $202.90 per month in 2026, regardless of whether their plan charges an additional premium. Some plans offer a “Part B Giveback” benefit that reduces this cost — Humana and UnitedHealthcare both offer this in select markets.

⚠️ Disclaimer: This article is for educational and informational purposes only and does not constitute financial, medical, or insurance advice. Medicare plan availability, premiums, benefits, and networks vary by location and individual circumstances. Always consult a licensed Medicare advisor or visit Medicare.gov before making any enrollment decisions. financeauthorityhub.com is not affiliated with Medicare, CMS, or any private insurance provider.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.