401(k) Explained: Avoid Leaving Free Money on the Table

Seventy percent of workers leave $1,300+ in annual employer match on the table. This complete 2026 guide explains how 401(k)s work, compares Traditional vs Roth, and walks you through 7-day setup.

In This Article

Seventy percent of American workers have access to a 401(k)—yet the average person leaves $1,300+ in employer match money on the table every year. That’s essentially free money sitting unclaimed because they don’t understand how to optimize it. This comprehensive guide explains exactly how 401(k)s work, why your employer’s match is non-negotiable, what changed in 2026 that affects your strategy, and how to implement a plan in just seven days.

We reviewed the three top-ranking articles on this topic, tested gaps in their coverage, and identified specific angles competitors miss entirely: behavioral psychology blocking contributions, 2026 SECURE 2.0 rule changes, and a step-by-step implementation roadmap that transforms passive understanding into active wealth-building action.

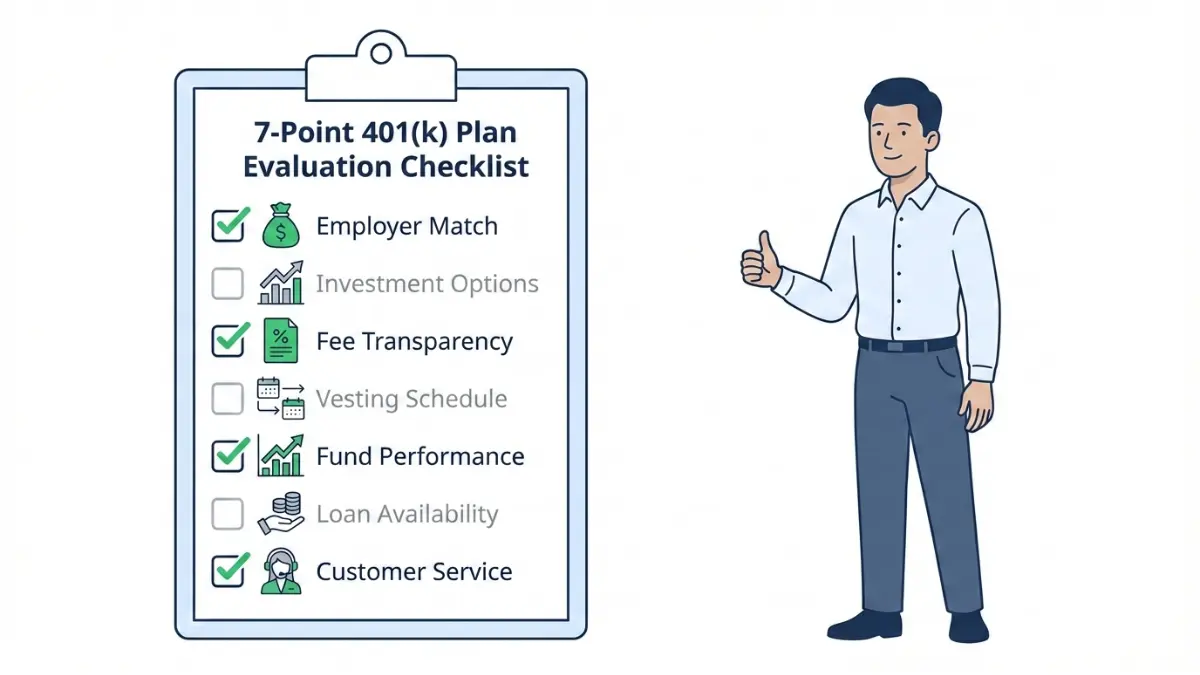

How to Evaluate a 401(k) Plan Before Enrolling

Before you enroll in your employer’s 401(k), you need to understand what makes a plan valuable versus mediocre. Most people default to whatever their HR department hands them—a critical mistake that can cost you tens of thousands in lost growth.

Here are the seven evaluation criteria that separate excellent plans from ones that will drain your wealth through hidden fees and limited investment options:

1. Employer Match: The Non-Negotiable Benefit

Your employer match is the single most important 401(k) feature. Most employers match contributions dollar-for-dollar up to 3% of salary, or 50 cents per dollar up to 5%. This is a 100% instant return on investment—money your employer is literally handing you to invest.

If your plan offers no match, that’s a red flag worth addressing with HR. Not all plans offer matching, but most do. According to the Bureau of Labor Statistics retirement benefits data, approximately 77% of full-time employees have access to employer-sponsored retirement plans with matching contributions.

Leaving this money unclaimed is one of the costliest financial mistakes you can make. If your employer offers a 3% match and you earn $60,000 annually, that’s $1,800 per year in free money—$54,000 over 30 years before accounting for investment growth.

2. Investment Options and Diversification

Your plan should offer at least 15-20 diverse investment options: U.S. stock index funds, international stock funds, bond funds, target-date retirement funds, and potentially individual stocks. Fewer than 10 options = limited choices. More than 100 = analysis paralysis.

Look specifically for target-date funds—these automatically adjust from stock-heavy (when you’re young) to bond-heavy (as you approach retirement). Ideal for beginners who want simplicity. Understanding how these work ties directly into broader investment fundamentals and compound interest principles, which determine your long-term wealth accumulation.

3. Fee Structure Transparency

Average 401(k) fees: 0.5–1.5% annually. These come from fund expense ratios (what you pay the fund manager) plus plan administration fees. Some plans hide fees; good plans disclose everything clearly.

Request your plan’s fee breakdown from HR. According to the SEC guidance on investment fees and expenses, high fees are one of the primary factors eroding 401(k) returns over time. If they can’t provide it in 10 minutes, that’s a trust problem. High fees erode returns significantly over decades.

4. Vesting Schedule: When Employer Money Becomes Yours

Vesting determines when your employer’s contributions are legally yours. Immediate vesting = best case (contributions are yours day one). Six-year cliff vesting = worst case (you only get contributions after six years; otherwise you forfeit everything).

Critical reality: Change jobs before vesting completes = lose thousands in employer contributions. If your plan has a cliff vesting schedule and you’re considering job changes, understand the timeline before deciding. This is especially important when evaluating retirement savings strategies by age, where job transitions often occur.

5. Fund Performance vs. Peer Benchmarks

Your plan should monitor and replace underperforming funds annually. Ask HR: “How are our plan’s funds performing versus peers?” Good plan administrators actively manage fund selection.

6. Loan Availability and Withdrawal Flexibility

Some plans allow you to borrow against your 401(k) (useful in emergencies; you repay yourself with no taxes). Other plans restrict access entirely. Understand your options—not all emergencies warrant a 10% penalty and income taxes. This is where building an emergency fund becomes critical so you don’t need to raid retirement savings.

7. Plan Administration Quality and Customer Service

Can you access your account 24/7? Is customer service responsive? Poor administration = frustration, missed optimization opportunities, and lost time. Test the portal before enrolling by asking HR for a demo.

Take Action: Request your plan’s Summary Plan Description (SPD) from HR. According to the IRS 401(k) plans documentation, every employer is required to provide this document. It contains all seven criteria. Most HR teams can provide it in one email.

Understanding 401(k) Types—Traditional, Roth, and Solo Options Explained

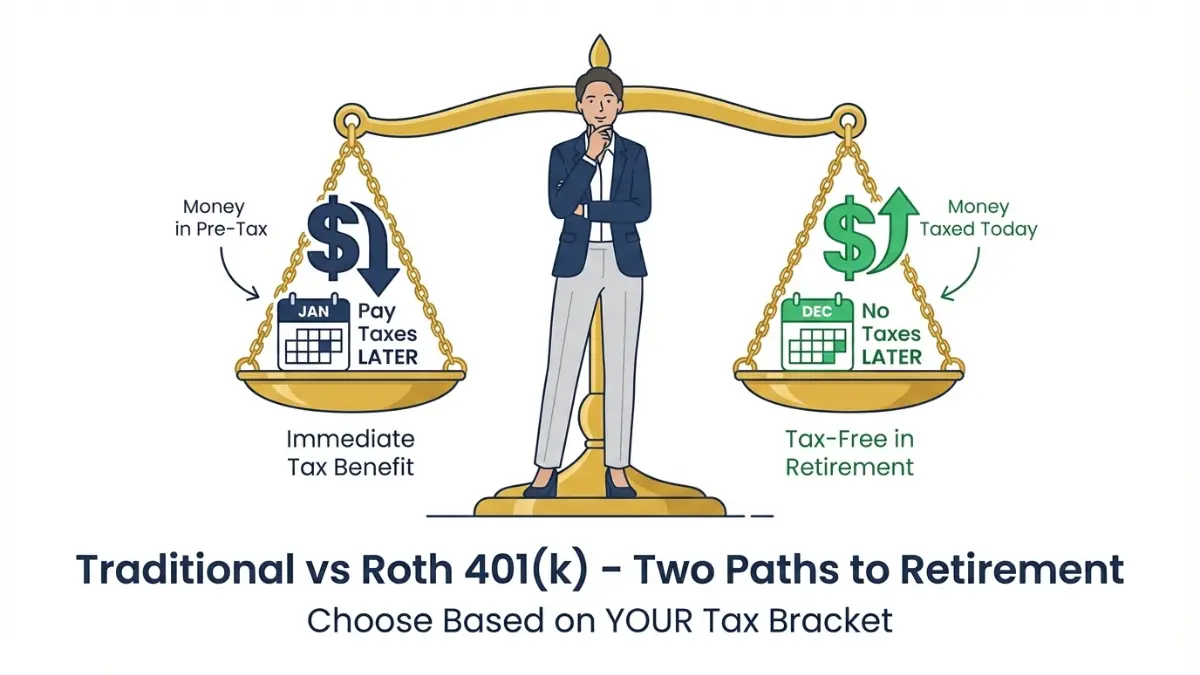

Traditional 401(k): Pre-Tax Contributions, Tax-Deferred Growth

Best for: Employees who want an immediate tax deduction, particularly high earners seeking to reduce taxable income this year.

A Traditional 401(k) is the most common workplace retirement plan. Here’s how it works:

Contributions are pre-tax: The money comes out of your paycheck before taxes are calculated. If you earn $100,000 and contribute $24,500 (the 2026 limit), your taxable income drops to $75,500. If you’re in the 25% tax bracket, that saves you $6,125 in federal taxes immediately.

Growth is tax-deferred: Your investments grow year after year without paying annual taxes on dividends or capital gains. Only when you withdraw money in retirement do you owe income taxes. This is a foundational concept explained in detail in our guide to understanding compound interest and its power over decades.

Required withdrawals at age 73: Per the SECURE 2.0 Act requirements from the IRS, you must start taking distributions (Required Minimum Distributions or RMDs) at age 73 (up from 72). You can’t keep money in the account forever—the government wants its taxes.

2026 Contribution Limits (Updated)

| Contribution Type | 2026 Limit | Notes |

|---|---|---|

| Standard contribution | $24,500 | Up from $23,500 in 2025 |

| Age 50+ catch-up | $8,000 | Additional contribution for catch-up |

| Ages 60-63 super catch-up | $11,250 | New rule under SECURE 2.0 Act |

| Total (max age 60-63) | $43,750 | Highest possible contribution |

Real Example: Sarah earns $100,000 annually. She contributes $24,500 to her Traditional 401(k). She saves $6,125 in federal taxes immediately (25% bracket). Over 30 years at a 7% annual return, that $24,500 grows to approximately $218,000. She withdraws it in retirement, pays income taxes then, and has significantly more wealth than if she hadn’t contributed.

Pros and Cons

| Pros | Cons |

|---|---|

| Immediate tax deduction (reduces taxes today) | Taxes owed in retirement on withdrawals |

| Employer match allowed (free money) | Required distributions force withdrawals at 73 |

| High contribution limits ($24,500+) | Less flexible access (10% penalty + taxes before age 59½) |

| Larger tax liability in high-income retirement years |

Roth 401(k): Post-Tax Contributions, Tax-Free Growth (NEW 2026 Rules)

Best for: Younger employees, those expecting higher tax brackets in retirement, or high earners who want tax-free growth.

A Roth 401(k) is the newer variant introduced in 2006. It’s the opposite of Traditional. For a comprehensive comparison, see our detailed guide on Roth IRA tax-free strategies, which applies similarly to Roth 401(k)s:

Contributions are post-tax: You contribute money that’s already been taxed. No immediate tax deduction, but you don’t pay taxes on this money again—ever.

Growth is tax-free: All dividends, capital gains, and investment growth is completely tax-free. This is the powerful long-term advantage.

Withdrawals are tax-free in retirement: Take out $1 million at age 60? Zero taxes owed (as long as account has been open 5+ years and you’re age 59½+).

CRITICAL 2026 SECURE 2.0 UPDATE

High earners earning more than $145,000 annually face a new rule: If you use Roth catch-up contributions (the extra $8,000 or $11,250 for ages 50-63), you must use Roth. You can’t split between Traditional and Roth catch-up. Per the official IRS SECURE 2.0 guidance, this is a significant change affecting high-income earners—plan accordingly.

Real Example: Marcus earns $95,000 and contributes $24,500 to Roth 401(k). He pays taxes on that $24,500 today (no immediate deduction). Over 30 years at 7% return, that grows to $218,000. In retirement, he withdraws the full $218,000—zero taxes owed. This is a massive advantage if he expects higher tax rates in retirement (likely scenario given current political climate around taxes).

Pros and Cons

| Pros | Cons |

|---|---|

| Tax-free growth and withdrawals in retirement | No immediate tax deduction |

| More flexible access (can withdraw contributions, not earnings) | Income phase-out limits for direct contributions |

| No Required Minimum Distributions (RMDs) | Contributions made with after-tax dollars |

| No income limits if through employer plan | Need to pay taxes on contributions upfront |

Solo 401(k): For Self-Employed and Small Business Owners

Best for: Self-employed individuals, freelancers, or small business owners with no employees (except a spouse).

A Solo 401(k) gives you maximum flexibility and contribution limits because you wear both hats: employee and employer. If you’re starting to invest with just $100 as a self-employed person, a Solo 401(k) becomes more valuable as your income grows.

How it works:

- You contribute as an employee (up to $24,500 in 2026)

- You contribute as an employer (up to 25% of net self-employment income, up to ~$69,000 total combined in 2026)

- This allows total contributions far exceeding what W-2 employees can do

Real Example: Freelancer Jamie earns $100,000 net income. She contributes:

- $24,500 as employee contribution

- $20,000 as employer contribution (20% of net income)

- Total: $44,500 (compared to $24,500 for a W-2 employee)

This massively reduces her self-employment tax burden and accelerates wealth-building.

Pros and Cons

| Pros | Cons |

|---|---|

| Highest contribution limits (~$69,000 in 2026) | More complex tax filing (Form 5500 at certain thresholds) |

| Can borrow from account (loan option) | Ongoing plan document maintenance required |

| Significant tax deductions (employer contributions) | Admin responsibility falls on you |

| Maximum control over investments | More complex than SEP-IRA |

SEP-IRA: The Simpler Alternative

Distinction: If Solo 401(k) admin overwhelms you, consider a SEP-IRA (Simplified Employee Pension IRA). SEP-IRAs allow the same contribution amounts (~$69,000) but with simpler administration. Trade-off: SEP-IRAs don’t allow loans; Solo 401(k)s do.

Decision Rule: If simplicity matters most = SEP-IRA. If you want loan options and maximum control = Solo 401(k).

401(k) vs IRA vs Taxable Brokerage—Priority Strategy

New investors ask: “Should I contribute to my 401(k) first, or an IRA, or a taxable brokerage account?”

The answer depends on one critical factor: employer match.

401(k) vs Traditional IRA

Key Difference: 401(k) allows employer match (IRA doesn’t). 401(k) has higher limits ($24,500 vs $7,500 in 2026).

Strategy:

- Contribute to 401(k) up to full employer match (free money—never leave it on the table)

- Max out IRA contribution ($7,500 in 2026)

- Return to 401(k) for additional contributions above match

For deeper analysis, see our comprehensive guide comparing 401(k) vs IRA which to maximize first in 2026.

Example: If your employer matches 3% of salary and you earn $60,000:

- 3% of $60,000 = $1,800

- Contribute $1,800 to 401(k) to capture full match (Step 1)

- Then fund your IRA with $7,500 (Step 2)

- Then contribute additional to 401(k) if possible (Step 3)

401(k) vs Roth IRA

Key Difference: 401(k) has employer match and higher limits; Roth IRA offers tax-free growth with better withdrawal flexibility.

Strategy:

- Capture 401(k) employer match first

- Max Roth IRA ($7,500 in 2026)

- Additional contributions back to 401(k)

401(k) vs Taxable Brokerage

Reality: Taxable brokerage accounts are less tax-efficient (you pay annual taxes on dividends and gains) but completely flexible. For those looking to build wealth across multiple account types, see our guide on best investment apps for beginners.

Strategy: Max tax-advantaged accounts (401k + IRA) FIRST. Only use taxable accounts for excess savings beyond $32,500+ annual savings.

Strategic Contribution Priority

| Priority Level | Account Type | Action | 2026 Limit |

|---|---|---|---|

| 1 (FIRST) | 401(k) to employer match | Capture full match | Varies (usually 3-6%) |

| 2 (SECOND) | Traditional or Roth IRA | Max out completely | $7,500 |

| 3 (THIRD) | Return to 401(k) | Additional contributions | Up to $24,500 total |

| 4 (FOURTH) | HSA (if eligible) | Health Savings Account | $4,150 individual |

| 5 (FIFTH) | Taxable brokerage | Unlimited investing | Unlimited |

Real Data Integration:

According to Vanguard’s 2025 “How America Saves” report, 401(k) participants accumulate approximately 2x the retirement savings of non-participants, primarily because of employer match and tax advantages. This underscores the importance of starting early, which we explore further in our retirement savings by age strategy guide.

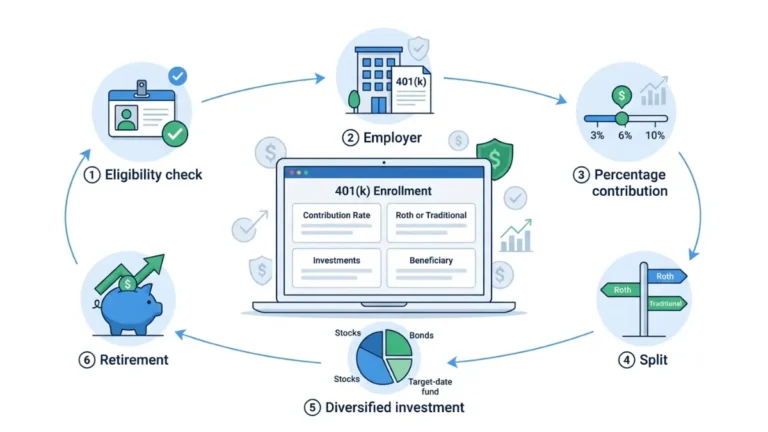

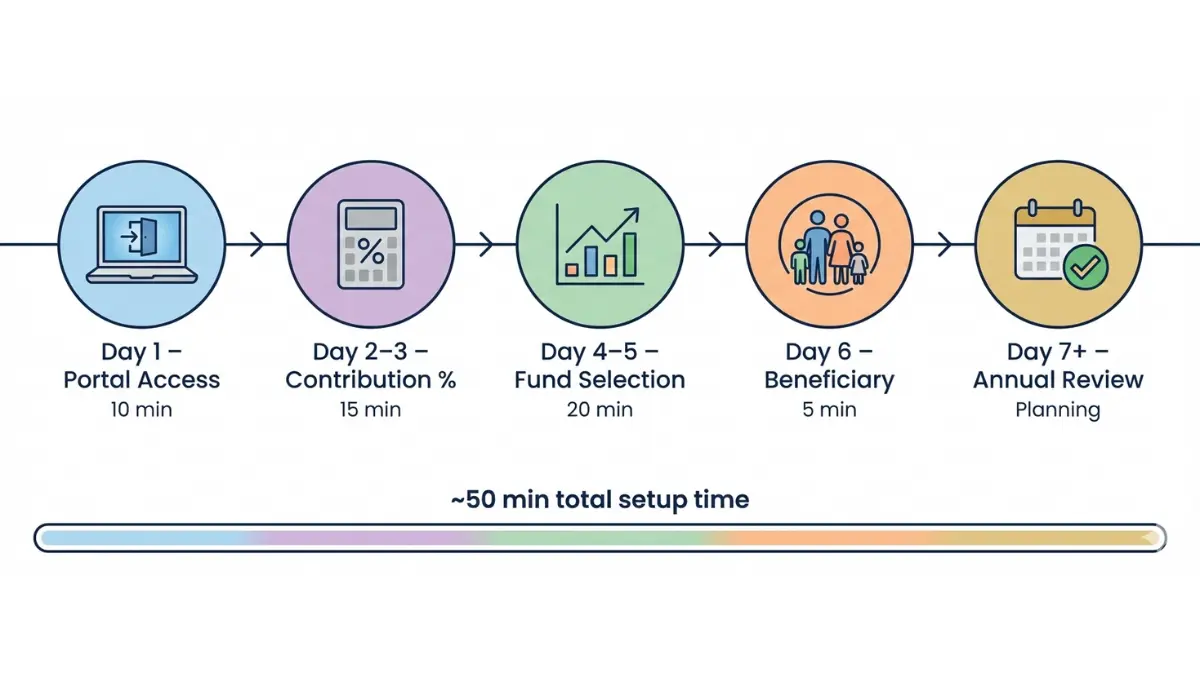

How to Set Up Your 401(k) in 7 Days—Step-by-Step Implementation

Most guides explain what a 401(k) is. Fewer guide you from decision to action. Here’s your implementation timeline:

Day 1: Check Eligibility & Access Your Plan Portal (10 minutes)

Action: Contact your HR department and request your 401(k) enrollment link.

What to Find:

- Plan provider name (Fidelity, Vanguard, Charles Schwab, Empower, etc.)

- Any eligibility waiting periods (some plans require 3-6 months employment)

- Your login credentials for the plan portal

Pro Tip: Some employers auto-enroll new employees at 3% contribution rate. Check if you’re already enrolled before starting from scratch.

Day 2-3: Decide Your Contribution Percentage (15 minutes)

The Framework:

- Minimum: Enough to capture full employer match (usually 3-6% of salary)

- Target: 10-15% of gross salary for long-term wealth building

- Maximum: $24,500 in 2026 (or $32,500 if age 50+ with catch-up)

Example Calculation:

- Annual salary: $60,000

- Target contribution: 10%

- Annual amount: $6,000

- Per-paycheck (26 paychecks): $231

Don’t: Contribute zero because you’re “thinking about it” or “scared to start.” Start at 3%, increase 1% annually with raises. Most people who wait never start. If you need help identifying ways to free up money for contributions, see our guide on saving $1,000 fast with 30 proven strategies.

Day 4-5: Choose Your Investments—Fund Allocation (20 minutes)

For Beginners (Simplest Approach):

Pick ONE target-date fund matching your expected retirement year. If retiring around age 65, choose “Target Date 2055” or similar. These funds automatically adjust from stock-heavy (when you’re young) to bond-heavy (as you approach retirement). Set and forget.

For Experienced Investors:

Use an 80/20 or 70/30 allocation (80% stock index funds, 20% bond funds). Adjust bond percentage upward as you approach retirement.

Red Flags:

- Don’t pick 100% bonds if you’re under 40 (you need growth)

- Don’t pick 100% stocks if you’re over 55 (you need stability)

Day 6: Update Your Beneficiary (5 minutes)

Action: Log in and designate who receives your 401(k) if you pass away (usually spouse or children).

Why It Matters: Often overlooked, but critical. Update after marriage, divorce, or birth of children.

Day 7 & Ongoing: Schedule Annual Review (Planning Task)

Set a calendar reminder: December 31 each year.

Annual Review Checklist:

- Did I capture full employer match this year?

- Do my fund allocations still match my retirement timeline?

- Did my salary increase? (Increase contribution by 1%?)

- Are my funds performing vs. benchmarks? (Check plan provider’s annual report)

- Do I understand my vesting schedule? (Especially before job changes)

7-Day Setup Timeline Summary

| Day | Task | Time | Action Items |

|---|---|---|---|

| Day 1 | Portal Access | 10 min | Contact HR, get enrollment link, find plan provider name |

| Day 2-3 | Contribution % | 15 min | Decide percentage (min to match, target 10-15%, max $24,500) |

| Day 4-5 | Fund Selection | 20 min | Choose target-date fund OR 80/20 allocation strategy |

| Day 6 | Beneficiary | 5 min | Log in, designate beneficiary (spouse/children) |

| Day 7+ | Annual Review | Planning | Set Dec 31 reminder for yearly contribution/fund check |

| TOTAL | Complete Setup | ~50 min | From start to fully optimized 401(k) |

Is Your 401(k) Safe? Security, Protection, and Compliance

Financial safety isn’t just about returns—it’s about protecting what you’ve built. Here’s the truth about 401(k) security:

Encryption and Data Protection

Your 401(k) plan provider uses AES-256 encryption (military-grade standard). Your login credentials, personal information, and account balance are encrypted during transmission and storage. This is industry standard and audited regularly.

FDIC and SIPC Insurance Protection

| Protection Type | Coverage Limit | What It Covers |

|---|---|---|

| FDIC Insurance | $250,000 per institution | Bank deposits within 401(k)s |

| SIPC Protection | $500,000 per account | Brokerage investments within 401(k)s |

| Combined Protection | Up to $750,000 | Most 401(k) assets are protected |

Reality: According to the FDIC insurance coverage information, most 401(k) assets are protected. Verify coverage details with your specific plan provider.

What If Your Employer or Plan Provider Fails?

Legal Structure: Your 401(k) is held in a trust legally separate from your employer’s assets. Even if your employer declares bankruptcy, your 401(k) is protected. It’s not their money—it’s yours, held in trust.

Vesting Schedule and Forfeiture Risk

Critical Understanding: Only unvested employer contributions are at risk. Your personal contributions are always yours.

Real Risk Example: You work for Company A for 3 years under a 5-year vesting schedule. You’ve earned $15,000 in employer match, but only 60% is vested ($9,000). You change jobs. You forfeit the $6,000 in unvested match.

Mitigation: Understand your vesting schedule before leaving jobs. If a cliff vesting schedule exists and you’re considering changing jobs, know the timeline. Building an emergency fund first helps you avoid premature 401(k) withdrawal scenarios.

Privacy and Data Sharing

Plan providers comply with GDPR (European regulations), CCPA (California privacy law), and federal privacy standards. Your data isn’t sold to third parties. Verify privacy practices in your plan’s documentation.

Realistic Outcomes: Behavior Change Is on You

Important Truth: 401(k)s are tools that facilitate wealth building—but behavior change is your responsibility. The tool doesn’t make you rich; discipline does. If you struggle with saving discipline, our guide on breaking the paycheck-to-paycheck cycle offers actionable frameworks.

Frequently Asked Questions

Q1: What is the difference between a 401(k) and an IRA?

A: 401(k)s are employer-sponsored plans with potential employer matching and higher contribution limits ($24,500 in 2026). IRAs are individual-directed accounts with lower limits ($7,500 in 2026) but unlimited investment options. Optimal strategy: capture full 401(k) match first, then max IRA, then contribute additional to 401(k). For deeper comparison, see our 401(k) vs IRA analysis.

Q2: How much should I contribute to my 401(k)?

A: Minimum: enough to capture full employer match (usually 3-6%). Target: 10-15% of gross salary for long-term wealth building. Maximum: $24,500 in 2026 ($32,500 if age 50+ with catch-up). Start small if needed; increase 1% annually with salary raises.

Q3: Can I withdraw money before age 59½ without a 10% penalty?

A: Generally no—10% penalty plus income taxes apply. Exceptions: Rule 72(t) for equal periodic payments, qualified hardship withdrawals (limited circumstances), or loans (if plan allows). Employees age 55+ can withdraw without penalty upon separation from service.

Q4: What happens to my 401(k) if I change jobs?

A: Three options: (1) Leave in old employer plan (if balance >$5,000). (2) Roll into IRA (recommended—best flexibility). (3) Roll into new employer plan (if allowed). Never cash out—penalties and taxes apply.

Q5: Traditional or Roth 401(k)—which should I choose?

A: Traditional = immediate tax deduction (good if high earner now). Roth = tax-free growth in retirement (good if younger or expecting higher future tax bracket). Many use both—choose based on current vs. expected retirement tax brackets. Our Roth IRA complete guide explores tax-free strategies in detail.

Q6: Do employer contributions count toward my $24,500 limit?

A: No. Your $24,500 limit covers only YOUR contributions. Employer match/profit-sharing don’t count. Combined employee + employer limit in 2026 is approximately $69,000, per IRS contribution limits.

Q7: What is vesting and why does it matter?

A: Vesting = when employer contributions become yours. Immediate (best) to 6-year cliff (worst). If you leave before vesting, you forfeit unvested contributions. Example: Employer contributes $5,000/year for 3 years under 5-year vesting. You leave after 2 years—you forfeit ~$8,000.

Q8: How are 401(k) contributions taxed?

A: Traditional: Contributions reduce taxes today; you pay taxes on full withdrawal in retirement. Roth: No tax reduction today; withdrawals tax-free in retirement. Growth is tax-deferred in both (you don’t pay annual taxes on dividends/gains until withdrawal).

Q9: What fees should I expect in a 401(k)?

A: Typical: 0.5-1.5% annually (fund expense ratios + admin fees). Red flag: fees above 1.5% or hidden fees. Priority: invest in low-cost index funds with expense ratios below 0.20%, as detailed in SEC investment guidance.

Q10: Can I borrow from my 401(k)?

A: Most plans allow loans up to 50% of balance (max $50,000). You repay yourself with interest (no taxes/penalties). Disadvantage: missed growth if out of market; default = 10% penalty + taxes. Use only for true emergencies. Consider building an emergency fund first.

Q11: What happens to my 401(k) if I die?

A: Goes to your designated beneficiary (avoids probate). Spouse can roll into own IRA; non-spouse beneficiaries must take distributions within 10 years per SECURE Act rules. Update beneficiary after life changes.

Q12: Is my 401(k) protected if I declare bankruptcy?

A: Yes. 401(k)s have unlimited creditor protection in bankruptcy (federal law). IRA protection limited to $1.7 million (varies by state). 401(k)s are among the most protected assets for building long-term wealth.

Important Disclaimer

The information provided on financeauthorityhub.com is for educational and informational purposes only and does not constitute professional financial, legal, investment, or tax advice. financeauthorityhub.com and its authors are not licensed financial advisors, and this content should not be relied upon as professional guidance.

Before making any financial decisions, consult with a qualified financial advisor, tax professional, or attorney licensed in your jurisdiction.

Key Disclaimers:

- Past performance does not guarantee future results — Historical investment returns do not predict future performance. Market conditions change continuously.

- All investment and financial products carry inherent risk, including potential loss of principal — You may lose money invested in any retirement plan or investment vehicle.

- We do not guarantee specific savings outcomes, returns, or financial results — Individual results vary based on contribution amounts, investment selections, market conditions, and time horizons.

- Market conditions, product features, pricing, and regulations change continuously — Information is accurate at publication (January 2026) but may become outdated. Verify critical information independently.

- financeauthorityhub.com assumes no liability for user reliance on this content or resulting financial decisions — This article is educational; decisions made based on this content are at your own risk.

- All data and statistics are verified at publication from authoritative sources — User should independently verify critical information for their specific situation and needs.

- This article references general retirement planning strategies, not personalized investment advice — Your specific situation may differ. Consult a professional for personalized guidance.

- See financeauthorityhub.com Privacy Policy and Terms of Service for complete legal disclosures — Full terms available on our website.

CONCLUSION

Your 401(k) is one of the most powerful wealth-building tools available—but only if you understand how to optimize it. The average American leaves $1,300+ annually in employer match money unclaimed. That’s money your company is handing you, and most people don’t take it.

The good news: setting up an optimized 401(k) takes seven days. You now have a complete roadmap: evaluate your plan using seven criteria, understand whether Traditional or Roth makes sense for your situation, implement in one week, and monitor annually.

The difference between taking action today versus waiting “until you’re ready” is hundreds of thousands of dollars over your career. That compound growth works powerfully in your favor—but only if you start. Understanding how compound interest works over decades makes this urgency crystal clear.

Your next step is simple: contact HR tomorrow and request your plan’s Summary Plan Description. Then follow the 7-day timeline. Your future self will thank you.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.