Whole Life Insurance Truth: Worth It in 2026?

Whole life insurance costs 10x more than term — but in 2026, top insurers are paying $14B+ in record dividends. Is it worth it for you? Expert verdict inside.

In This Article

Whole life insurance provides permanent, lifelong coverage with fixed premiums and a guaranteed cash value that grows tax-deferred — but it costs 10–15x more than term life. In 2026, top mutual insurers are distributing a record $14+ billion in dividends combined. Whether whole life insurance is worth it depends entirely on your financial goals, income level, and time horizon.

What Is Whole Life Insurance? (2026 Plain-English Breakdown)

Whole life insurance is a type of permanent life insurance that never expires as long as you pay your premiums. Unlike term life, it does not have an end date. It also builds a savings component called cash value that grows at a guaranteed rate inside your policy.

According to the National Association of Insurance Commissioners (NAIC), whole life is classified as a “cash-value policy” — meaning part of every premium goes toward coverage, and the rest grows as an asset you can access while alive.

The 3 Guaranteed Promises of Every Whole Life Policy

Every whole life insurance policy legally guarantees these three things:

- Fixed premiums — your monthly cost never increases, even as you age or if your health changes

- Guaranteed death benefit — paid income-tax-free to your beneficiaries per the IRS life insurance tax rules

- Cash value growth — a guaranteed rate of 3%–4.65% annually (2026 industry average)

How Cash Value Actually Builds — Year by Year

This is the part agents rarely explain upfront. Cash value does not accumulate evenly.

| Policy Year | Cash Value Status | What’s Happening |

|---|---|---|

| Year 1–3 | Near zero | Setup costs + admin fees consume most premium |

| Year 4–7 | Slow build begins | Guaranteed interest starts compounding |

| Year 8–14 | Steady growth | Dividends (if mutual insurer) accelerate growth |

| Year 15–20+ | Compounding accelerates | Cash value becomes a meaningful financial asset |

Key Takeaway: Whole life insurance is a long-game financial tool. If you cancel within the first 5 years, you will likely receive very little cash value back.

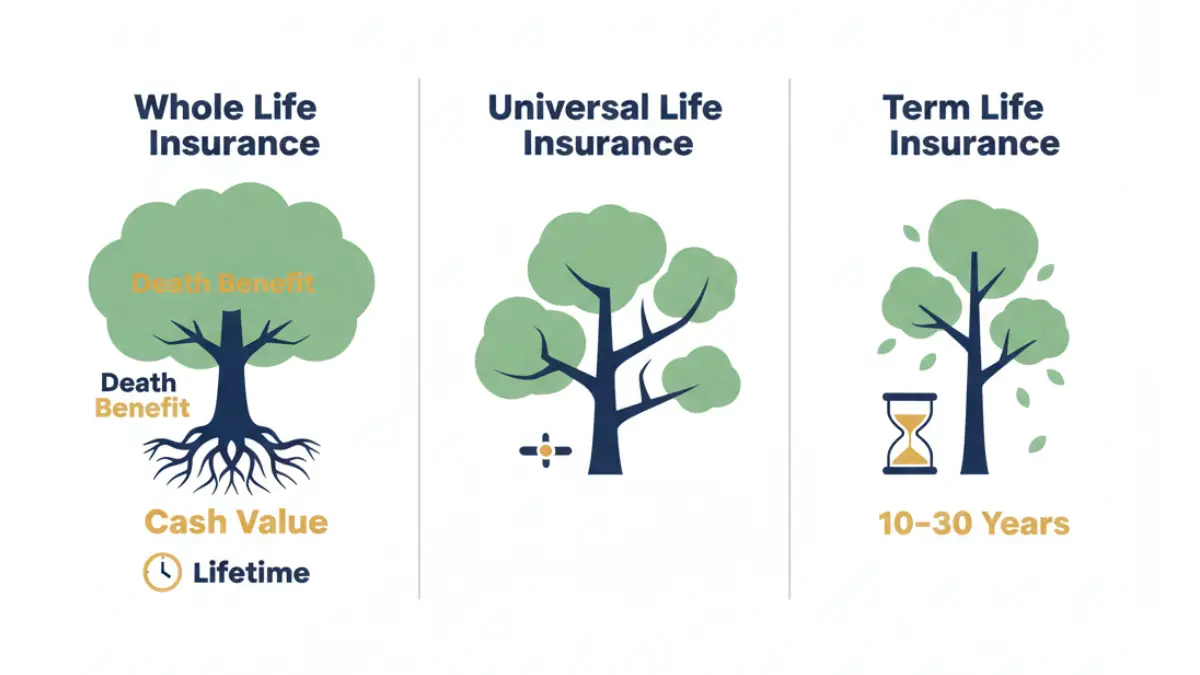

60-Second Comparison: Whole Life vs. Universal Life vs. Term

| Feature | Whole Life | Universal Life | Term Life |

|---|---|---|---|

| Coverage Duration | Lifetime | Lifetime (flexible) | 10–30 years |

| Premium | Fixed | Flexible | Fixed during term |

| Cash Value | Yes — guaranteed | Yes — variable | None |

| Dividends | Possible (mutual insurer) | No | No |

| Avg Monthly Cost ($500K) | ~$667 | ~$294 | ~$55 |

| Best For | Estate planning, HNW | Flexible long-term | Young families, income replacement |

If you are weighing permanent coverage costs against your total financial picture, explore the financial tools at financeauthorityhub.com to model your budget across different scenarios.

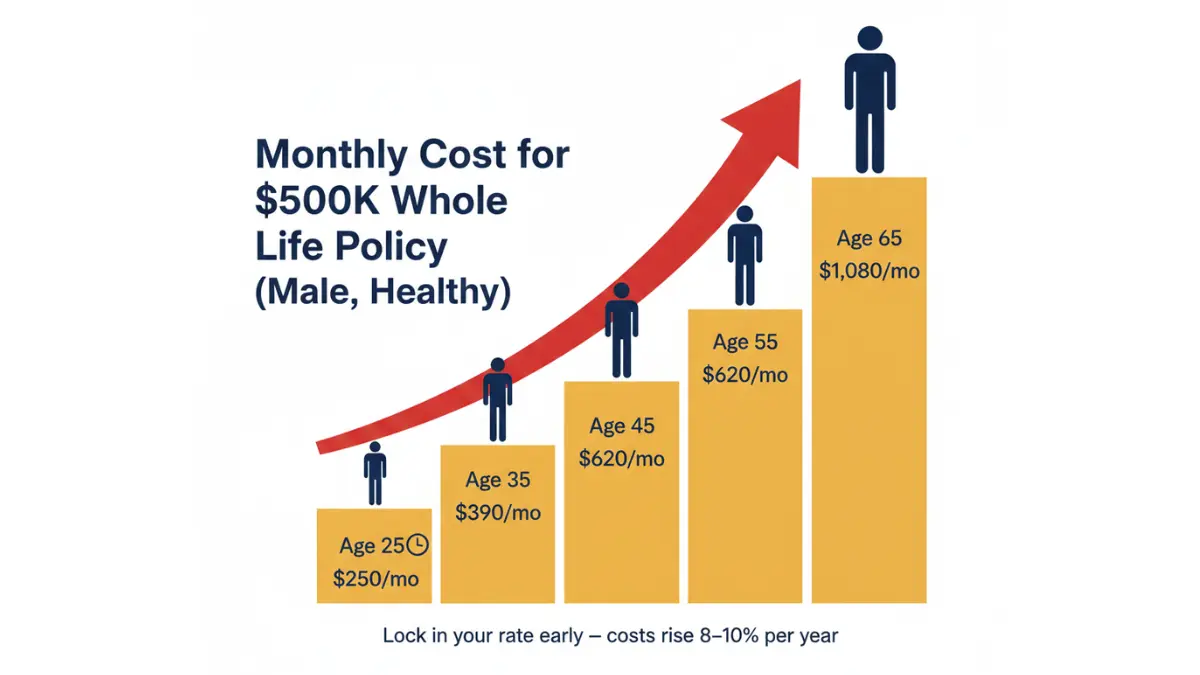

Real Whole Life Insurance Costs in 2026 — By Age, Gender & Health

Here’s what most guides won’t show you: the actual monthly dollar gap between whole life and term life. For a $500,000 policy, whole life averages $667/month vs. $55/month for term — a 1,113% premium difference. That gap is real, and it matters.

Monthly Cost Table: $500,000 Whole Life Policy (2026 Data)

| Age | Male (Healthy) | Female (Healthy) | Male (Smoker) |

|---|---|---|---|

| 25 | ~$250/mo | ~$210/mo | ~$540/mo |

| 35 | ~$390/mo | ~$330/mo | ~$820/mo |

| 45 | ~$620/mo | ~$510/mo | ~$1,290/mo |

| 55 | ~$1,080/mo | ~$890/mo | ~$2,100/mo |

| 65 | ~$1,950/mo | ~$1,590/mo | Often ineligible |

Sources: MoneyGeek 2026 rate aggregates, Aflac 2026 rate tables, PinnacleQuote 2026 data.

Women pay approximately 24% less than men for the same policy because of longer average life expectancy — 81.1 years for women vs. 75.8 years for men, per the CDC Mortality in the United States 2023 report.

5 Factors That Control Your Premium

Understanding these helps you shop smarter:

- Age — the single biggest factor; premiums rise 8%–10% per year of delay

- Gender — women consistently pay less due to actuarial life expectancy data

- Health classification — Preferred Plus vs. Standard rating = 20%–30% cost difference

- Coverage amount — larger policies offer slight per-dollar efficiency

- Payment structure — 10-Pay and 20-Pay cost more monthly but end sooner

Limited-Pay vs. Pay-to-100: Which Costs Less Long-Term?

| Structure | Monthly Premium | Total Paid by Age 80 |

|---|---|---|

| Pay-to-100 (35-year-old male) | ~$390/mo | ~$222,300 |

| 20-Pay (ends at 55) | ~$910/mo | ~$218,400 |

| 10-Pay (ends at 45) | ~$1,650/mo | ~$198,000 |

If you can afford higher payments upfront, 10-Pay and 20-Pay policies often cost less in total over a lifetime. Consult a licensed advisor and compare this against your overall debt load — use our Debt Consolidation Calculator to assess how life insurance premiums fit alongside your existing obligations.

The Real Benefits — Including What Competitors Don’t Tell You

Most guides list the same three benefits. Here’s the complete picture that NerdWallet, Bankrate, and Investopedia all miss in 2026.

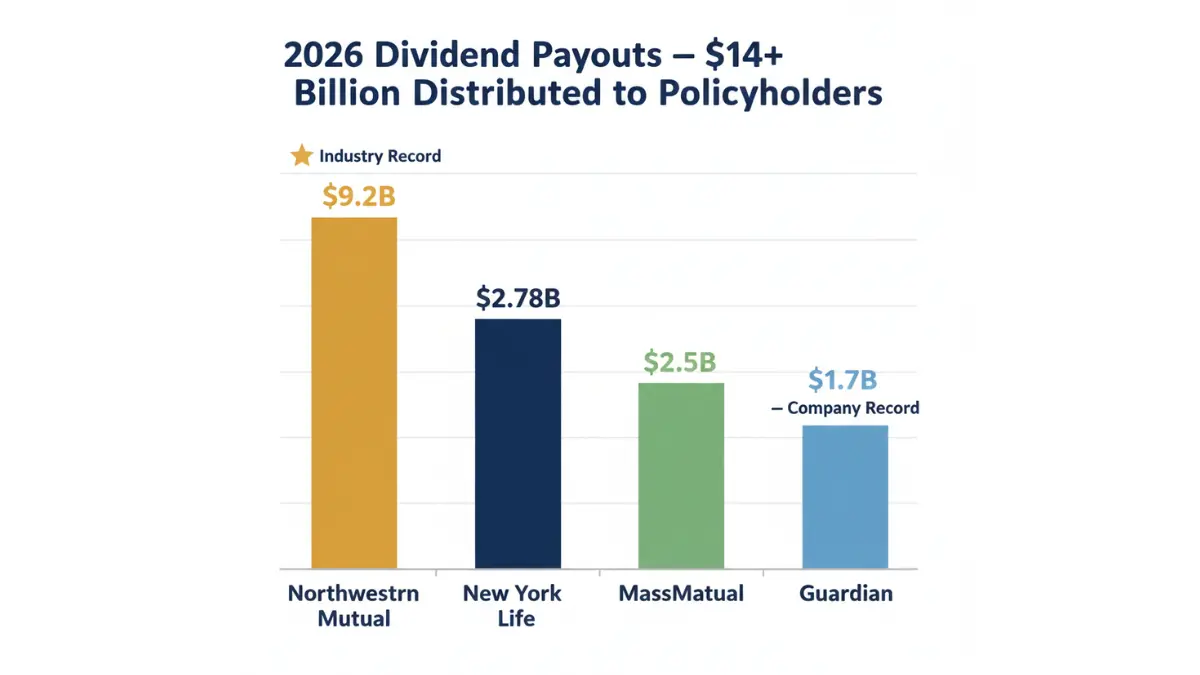

The $14+ Billion Dividend Story: 2026’s Biggest Insurance News

In 2026, the top mutual life insurers are distributing record-breaking dividends. This is the most significant story in the whole life insurance market right now — and almost no major guide is covering it.

| Company | 2026 Dividend Payout | COMDEX Score | AM Best |

|---|---|---|---|

| Northwestern Mutual | $9.2 billion (industry record) | 100 | A++ |

| New York Life | $2.78 billion | 100 | A++ |

| MassMutual | $2.5 billion | 100 | A++ |

| Guardian | $1.7 billion (company record) | 99 | A++ |

What is a COMDEX score? It is a composite ranking from 1–100 that combines ratings from all four major agencies: AM Best, S&P, Moody’s, and Fitch. Only three U.S. insurers currently hold a perfect score of 100: Northwestern Mutual, New York Life, and MassMutual.

Important: Dividends are not contractually guaranteed. However, these companies have paid dividends to eligible policyholders for over 150 consecutive years without interruption.

Tax Advantages Most Americans Don’t Know About

Whole life insurance carries three significant tax benefits under the U.S. tax code. These are confirmed by IRS Publication 525 on Taxable and Nontaxable Income:

- Cash value grows tax-deferred — you pay no annual tax on internal growth

- Policy loans are not taxable income — you borrow against your own cash value without triggering a tax event

- Death benefit is paid income-tax-free — beneficiaries receive the full face value, no federal income tax owed

For high-income earners who have maxed out their 401(k) and Roth IRA, a whole life policy becomes a legitimate third tax-advantaged vehicle.

The Infinite Banking Concept — Legitimate or Overhyped?

Infinite Banking (IBC) uses your whole life policy’s cash value as a personal financing tool. Instead of borrowing from a bank, you borrow against your own policy — the cash value continues earning interest while the loan is outstanding.

It works best when:

- You hold the policy for 15+ years before heavy borrowing

- You are a high-income earner who has exhausted other tax-advantaged accounts

- You have the discipline to repay policy loans consistently

It does not work well when:

- You need short-term coverage on a tight budget

- You expect to cancel the policy within 10 years

- Your primary goal is pure income replacement

Benefits Summary Table

| Benefit | Detail |

|---|---|

| Death Benefit | Guaranteed, income-tax-free to beneficiaries |

| Cash Value Growth | 3%–4.65% guaranteed annually (2026 avg.) |

| Dividends | Not guaranteed, but 150+ year track records at top mutual insurers |

| Tax-Free Loans | No credit check, no income tax triggered |

| Estate Planning | Covers estate taxes, equalizes inheritance, creates generational wealth |

| Premium Stability | Locked in at purchase — never increases regardless of age or health |

Whole Life vs. Term Life — The Honest 2026 Verdict

The debate is simple on the surface: pay less now (term) or build an asset (whole life). But the real answer is more nuanced.

Side-by-Side Comparison

| Category | Whole Life Insurance | Term Life Insurance |

|---|---|---|

| Coverage duration | Lifetime | 10–30 years only |

| Monthly cost ($500K, age 35) | ~$390/mo | ~$35/mo |

| Cash value | Yes — guaranteed | None |

| Dividends | Possible (mutual insurer) | None |

| Market share 2024 | 36% ($5.8B new premiums) | 19% ($3.0B) |

| Best for | Estate planning, HNW, long-term | Young families, income replacement |

| 99% of term policies… | — | Never pay a death claim (Mutual of Omaha data) |

Real Scenario: Same $500K Coverage, Two Strategies (Age 35)

Strategy A — Whole Life at $390/month:

- By age 65: ~$148,200 paid in premiums

- Cash value at 65: estimated $180,000–$220,000 (plus dividends)

- Death benefit: $500,000 guaranteed for life

- Estate/legacy outcome: Strong

Strategy B — Term Life at $35/month + Invest $355/month in S&P 500 Index Fund:

- By age 65: ~$12,600 paid in term premiums

- Investment portfolio at historical 7% return: estimated $430,000–$500,000

- Coverage ends at 65 — no death benefit unless renewed at much higher cost

- Wealth-building outcome: Stronger — but zero guaranteed legacy

The honest verdict: Neither strategy is universally better. Whole life wins for estate planning and guaranteed legacy. Term plus investing wins for pure wealth accumulation. The right answer depends on your specific goals.

For a deeper comparison of your investment options alongside insurance costs, read our Index Funds vs. Mutual Funds guide.

Expert Panel Verdict

According to the NAIC Life Insurance Consumer Guide, permanent life insurance “can be a good choice when coverage is needed permanently and when you want a savings component.” Our international expert panel at financeauthorityhub.com agrees — with an important condition:

“Whole life insurance delivers maximum value when held for 20+ years by policyholders who have specific estate, tax, or permanent dependency planning needs. For the average American family under 45, term life combined with consistent index fund investing typically outperforms on a pure return basis.” — financeauthorityhub.com Expert Panel, February 2026

Is Whole Life Insurance Worth It in 2026? The Decision Framework

This is the section your insurance agent will never show you — an honest decision matrix with no agenda.

✅ Buy Whole Life Insurance IF…

- You have maxed out your 401(k), IRA, and all other tax-advantaged accounts and need another vehicle

- You have a permanent financial dependent — a child with special needs, a business partner, or a lifelong obligation

- You are focused on estate planning — passing wealth, covering estate taxes, or equalizing an inheritance

- You are a high-net-worth individual ($500K+ annual income) seeking a non-correlated, market-proof asset

- You want a guaranteed, risk-free savings component that cannot lose value in a market crash

- You can commit to holding the policy for at least 15–20 years without lapsing

If you’re also planning retirement, read our Retirement Planning in Your 30s guide to see how whole life fits within a broader strategy.

❌ Skip Whole Life Insurance IF…

- You are under 40 with a young family on a moderate income — term life covers the same risk for 90% less

- You carry high-interest debt (credit cards, student loans, mortgages) that yields a guaranteed return on payoff higher than whole life cash value growth

- You need maximum death benefit at minimum cost right now

- You will not hold the policy for 10+ years — early surrender typically returns very little

- You are comfortable with index fund investing and understand that the “buy term and invest the difference” strategy typically beats whole life in pure wealth accumulation

For strategies to eliminate debt before committing to a large premium, explore the Snowball vs. Avalanche debt payoff comparison.

The 2026 Decision Matrix

| Your Situation | Best Choice |

|---|---|

| Young family, tight budget | Term Life |

| High-net-worth, estate planning | Whole Life |

| Business owner, key-person insurance | Whole Life |

| Maxed all retirement accounts | Whole Life |

| Need income replacement only | Term Life |

| Want guaranteed, market-proof savings | Whole Life |

| Carrying significant debt | Term Life first |

| Special needs dependent, lifetime obligation | Whole Life |

Best Whole Life Insurance Companies 2026 + FAQs + Disclaimer

Top 5 Whole Life Insurance Companies — Expert-Ranked for 2026

Ranked using four criteria: AM Best rating, COMDEX score, 2026 dividend performance, and policyholder complaint ratio per NAIC’s company data.

| Rank | Company | AM Best | COMDEX | 2026 Dividend | Best For |

|---|---|---|---|---|---|

| 🥇 1 | Northwestern Mutual | A++ | 100 | $9.2B | Overall best, wealth building, IBC |

| 🥈 2 | New York Life | A++ | 100 | $2.78B | Seniors, policy customization |

| 🥉 3 | MassMutual | A++ | 100 | $2.5B | Cash value growth, high-issue-age |

| 4 | Guardian | A++ | 99 | $1.7B | Health conditions, HIV coverage, flexibility |

| 5 | Penn Mutual | A+ | 97 | N/A | Infinite Banking, policy design optimization |

Northwestern Mutual is the strongest overall performer in 2026 with a COMDEX score of 100, a 165+ year dividend history, and the largest payout in insurance industry history at $9.2 billion this year.

MassMutual’s Whole Life 100 offers a guaranteed cash value rate of 3.75% — one of the most generous in the industry. Guardian stands out for covering applicants with HIV and accepting policyholders up to age 90.

For a comprehensive look at how life insurance fits your overall financial picture, see our complete Life Insurance Guide and our Term Life Insurance Rates and Calculator to compare your options side by side.

Frequently Asked Questions About Whole Life Insurance (2026)

1: What is whole life insurance in simple terms?

Whole life insurance is permanent life coverage that lasts your entire lifetime as long as premiums are paid. It combines a guaranteed death benefit with a cash value account that grows at a fixed rate tax-deferred inside the policy.

2: How much does whole life insurance cost per month in 2026?

A $500,000 whole life policy for a healthy 35-year-old costs approximately $390/month for men and $330/month for women. The same coverage in a 20-year term life policy costs roughly $30–$40/month — making whole life 8–10x more expensive on average.

3: Is whole life insurance a good investment?

For most average-income Americans, term life insurance combined with index fund investing typically outperforms whole life on a pure return basis. For high-net-worth individuals who have maxed retirement accounts and need estate planning tools, whole life is a legitimate and powerful financial vehicle.

4: What is cash value in whole life insurance?

Cash value is a tax-deferred savings component built inside your policy. It grows at a guaranteed rate of 3%–4.65% in 2026, and you can borrow against it or withdraw it without triggering a taxable event — as confirmed by IRS Publication 525.

5: Can I cancel whole life insurance and get money back?

Yes. Surrendering your policy returns the current accumulated cash value, minus any surrender charges. In the first 1–5 years, the returned amount is often minimal or zero. After 10+ years, the cash value can be substantial.

6: What happens to cash value when you die?

In most standard whole life policies, the insurance company retains the cash value and pays your beneficiaries only the death benefit. Some policies offer a “Return of Cash Value” rider that pays both — at a higher premium.

7: What is the difference between whole life and universal life insurance?

Whole life has fixed premiums and fully guaranteed cash value growth. Universal life offers flexible premiums and an adjustable death benefit, but the cash value performance is linked to interest rates and carries more risk.

8: Who should NOT buy whole life insurance?

People carrying high-interest debt, those who need maximum coverage at minimum cost, and young families on moderate incomes are typically better served by term life insurance. If you cannot hold the policy for at least 10 years, the costs of whole life rarely justify the benefits.

9: Are whole life insurance dividends guaranteed?

No. Dividends are not contractually guaranteed. However, Northwestern Mutual, New York Life, and MassMutual have each paid dividends to eligible policyholders every year for 150+ consecutive years without a single missed year.

10: Is whole life insurance worth it for seniors?

For seniors focused on estate planning, legacy transfer, or covering final expenses without burdening family, yes — whole life offers guaranteed coverage with no expiry date. Guardian Life accepts new applicants up to age 90 for whole life policies.

11: How does the Infinite Banking Concept work with whole life?

Infinite Banking uses your policy’s cash value as a personal financing system. You borrow against it — the cash value continues earning interest even while the loan is outstanding — and repay yourself on your own schedule. It is a powerful strategy for high-income earners with 15+ year time horizons, but requires disciplined execution and professional guidance.

Disclaimer

This article is for educational and informational purposes only and does not constitute financial, legal, or insurance advice. Premium figures shown are illustrative estimates based on 2026 industry data and will vary by insurer, individual health profile, state of residence, and policy design. Dividend figures are sourced from public insurer announcements and are not guaranteed future payments. Always consult a licensed financial advisor or insurance professional before purchasing any life insurance policy. financeauthorityhub.com does not sell, broker, or recommend specific insurance products.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.