Private Medical Insurance: Stop Waiting, Start Living

With 7.6M on NHS waiting lists in 2026, private medical insurance is no longer a luxury. From £28/month, here’s what it covers, costs & whether you need it.

In This Article

Private medical insurance (PMI) pays for private healthcare treatment so you skip NHS waiting lists and get faster, better access to specialists, surgery, and diagnostics. In 2026, with the NHS elective care backlog sitting at over 7.6 million treatment pathways, PMI has shifted from a luxury to a smart financial protection decision — starting from just £28/month.

PMI covers new, acute conditions — surgery, scans, consultations. Average cost: £79.59/month. You keep using the NHS for emergencies and GP visits.

📊 Private Medical Insurance at a Glance — 2026 Data

| Factor | 2026 Data |

|---|---|

| NHS Elective Waiting List | 7.6 million+ treatment pathways |

| Average Individual PMI Cost | £79.59/month |

| PMI Starting From | £28/month (age 20) |

| Private Knee Replacement (self-pay) | £12,000–£15,000 |

| Time to See Private Specialist | 3–7 days |

| Time to See NHS Specialist | 4–18+ months |

| Family PMI (average) | £166.52/month |

What this means for you: One knee replacement costs more than 11 years of PMI premiums. The maths of private medical insurance is increasingly clear for UK households.

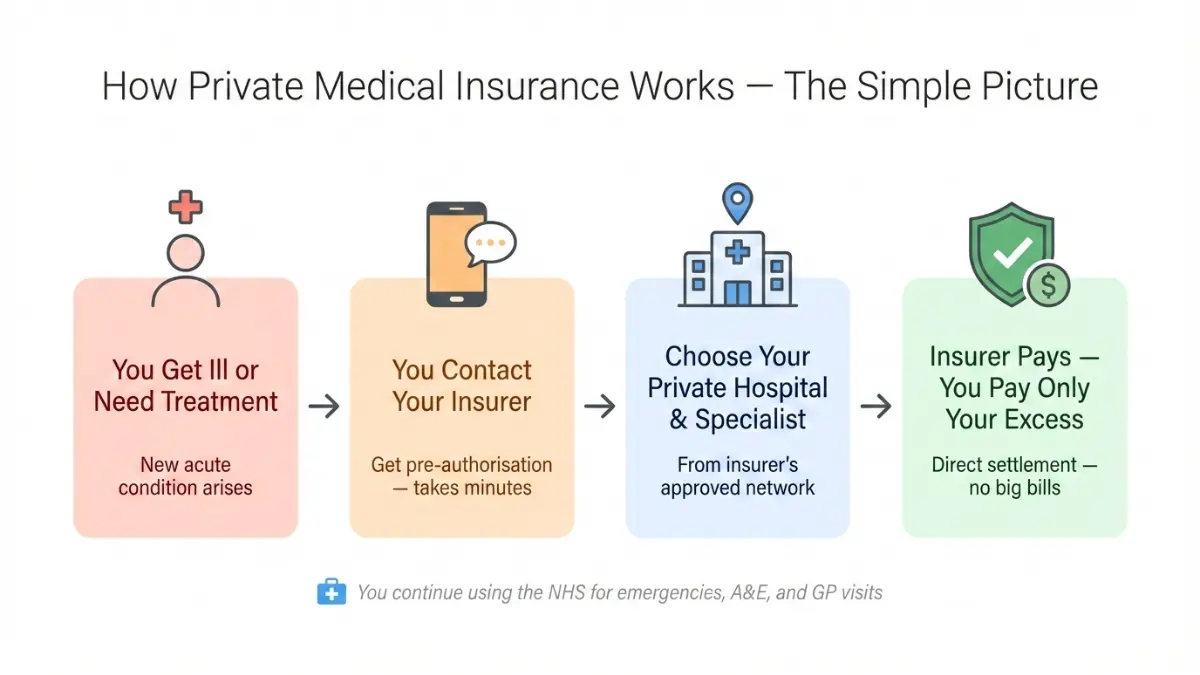

What Is Private Medical Insurance and How Does It Work?

Private medical insurance is a monthly or annual policy that covers the cost of private healthcare for acute (treatable, curable) conditions. It works alongside the NHS — you still use the NHS for emergencies and GP visits, but PMI gives you faster access to everything else.

When you need treatment, you contact your insurer, get authorisation, choose a private hospital or specialist from their approved network, and your insurer pays the bill directly. According to NHS England’s referral-to-treatment data, over 2.8 million people have been waiting more than 18 weeks for elective care — PMI eliminates that wait entirely for covered conditions.

✅ What Private Medical Insurance Covers vs. What It Doesn’t

| ✅ PMI Covers | ❌ PMI Does NOT Cover |

|---|---|

| Acute, curable conditions | Chronic conditions (diabetes, asthma) |

| Elective surgery (hip/knee replacement) | Emergency A&E treatment |

| Private specialist consultations | Pre-existing conditions (initially) |

| Cancer diagnosis and treatment | Cosmetic procedures |

| Diagnostic scans (MRI, CT, X-ray) | Pregnancy and maternity |

| Mental health treatment (most policies) | GP visits |

| Physiotherapy and rehabilitation | Long-term condition management |

The single biggest misunderstanding: PMI is not a replacement for the NHS. It is a financial shield for the gap between what the NHS can offer and how fast you need it.

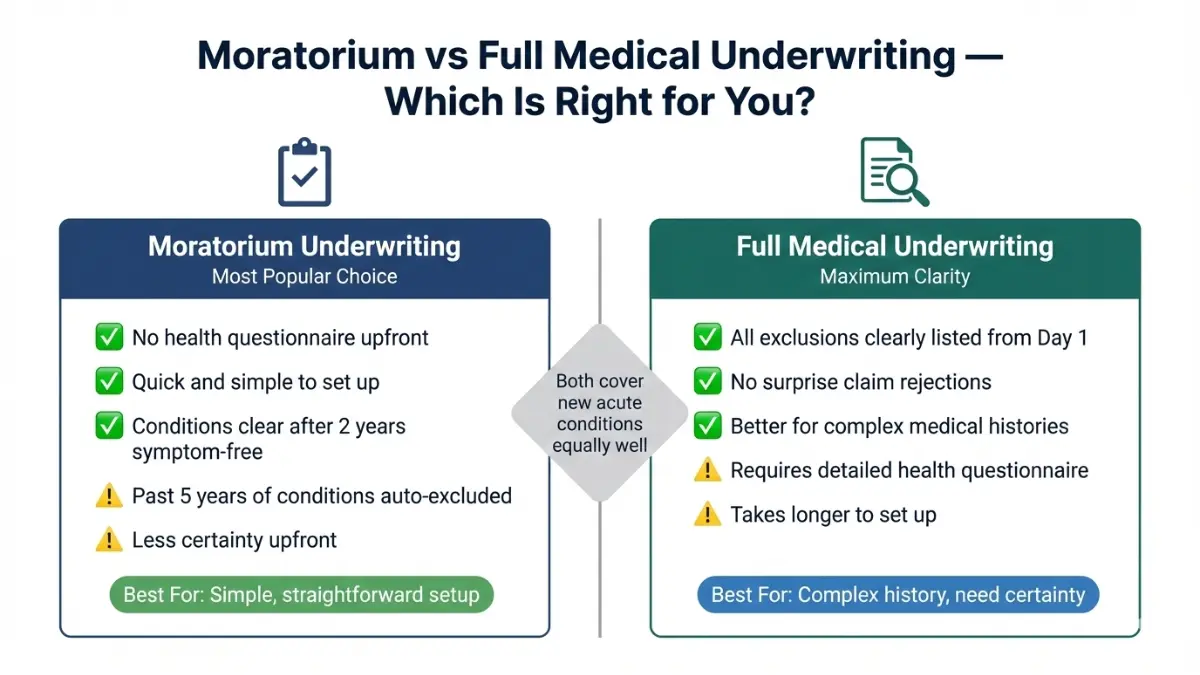

How Underwriting Works — The Decision That Changes Your Cost

There are two ways insurers assess your medical history before covering you.

Moratorium Underwriting (most common)

- You don’t declare your full medical history upfront

- Conditions from the past 5 years are automatically excluded

- If you go 2 continuous years symptom-free on the policy, that condition may become covered

- Best for: People who want simplicity and quick setup

Full Medical Underwriting (FMU)

- You complete a detailed health questionnaire at application

- The insurer explicitly lists every exclusion from day one

- Provides total certainty about what is and isn’t covered

- Best for: People with a clear medical history who want no surprises at claim time

💡 Which should YOU choose? If you haven’t had major health issues in the past 5 years, moratorium is faster and simpler. If you have a complex history and want clear boundaries, FMU gives you certainty.

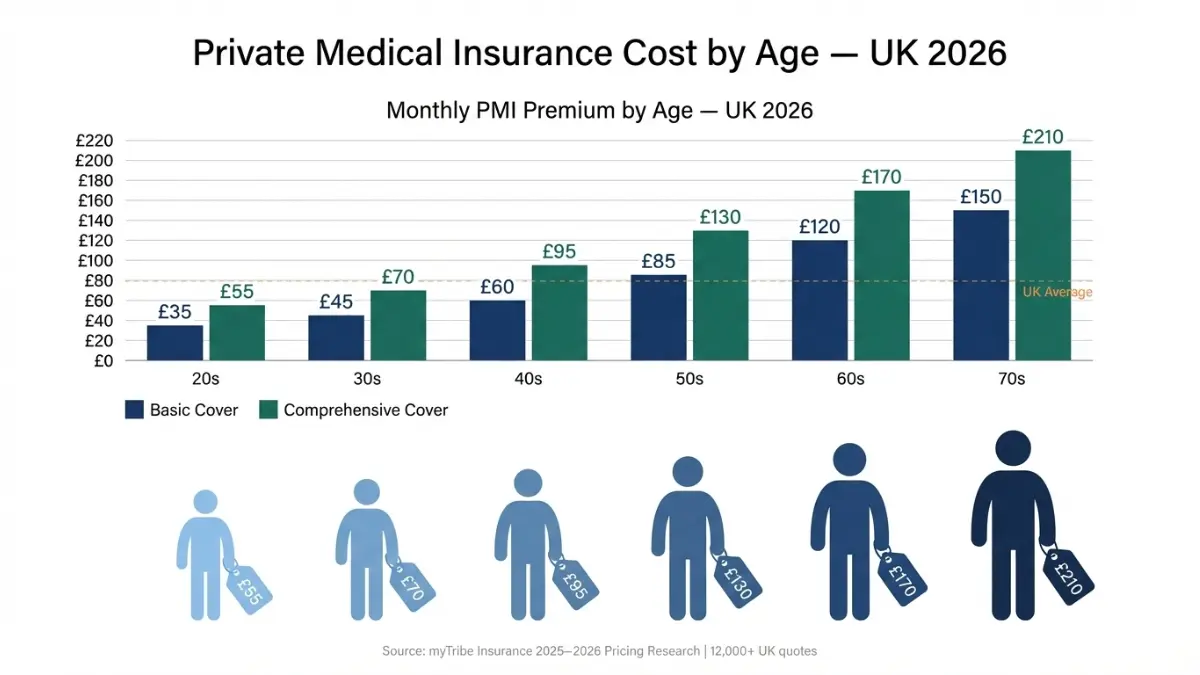

How Much Does Private Medical Insurance Cost in 2026?

The average UK private medical insurance cost in 2026 is £79.59/month for an individual, £145.77 for a couple, and £166.52 for a family of four — based on analysis of over 12,000 UK insurance quotes.

Your actual premium is not a fixed number. It is a personalised calculation driven by seven key factors.

2026 Average Monthly PMI Premiums by Age

| Age Group | Basic Cover/month | Comprehensive Cover/month |

|---|---|---|

| 20–29 | ~£28 | ~£41 |

| 30–39 | ~£44 | ~£65 |

| 40–49 | ~£65 | ~£95 |

| 50–59 | ~£90 | ~£130 |

| 60–69 | ~£120 | ~£170 |

| 70+ | ~£137 | ~£200 |

Source: myTribe Insurance, 2025–2026 pricing research across 12,000+ UK quotes

7 Factors That Drive Your PMI Premium

- Age — The single biggest driver. A 70-year-old pays roughly 5× more than a 20-year-old for identical cover.

- Location — Central London commands the highest premiums due to the “London uplift” on private hospital costs.

- Cover Level — Basic (inpatient only) vs. comprehensive (inpatient + outpatient + diagnostics + mental health).

- Policy Excess — The amount you pay per claim. Higher excess = lower monthly premium.

- Hospital List — A restricted regional list is cheaper than a full national network including London clinics.

- Smoking Status — Smokers and vapers typically pay 10–15% more.

- Underwriting Type — FMU vs. moratorium can affect both cost and what’s covered.

5 Proven Ways to Cut Your Premium by Up to 30%

- Add the 6-week NHS wait clause: If the NHS can treat you within 6 weeks, you use the NHS. If it can’t, PMI kicks in. This alone can cut your premium by up to 30%. Note: Some insurers like AXA have suspended this option due to current NHS wait lengths — check current availability.

- Choose a higher excess: Moving from £0 to £500 excess can reduce your monthly cost by 15–25%.

- Select a regional hospital list: Excluding high-cost London hospitals if you don’t need them saves meaningful money.

- Pay annually: Most insurers offer a 5% discount for annual upfront payment vs. monthly billing.

- Use a guided consultant list: Agreeing to choose specialists from a pre-approved shorter list reduces admin costs for insurers — and your premium.

If you’re budgeting PMI alongside a mortgage or major financial commitment, our Home Affordability Calculator helps you model the full monthly picture clearly.

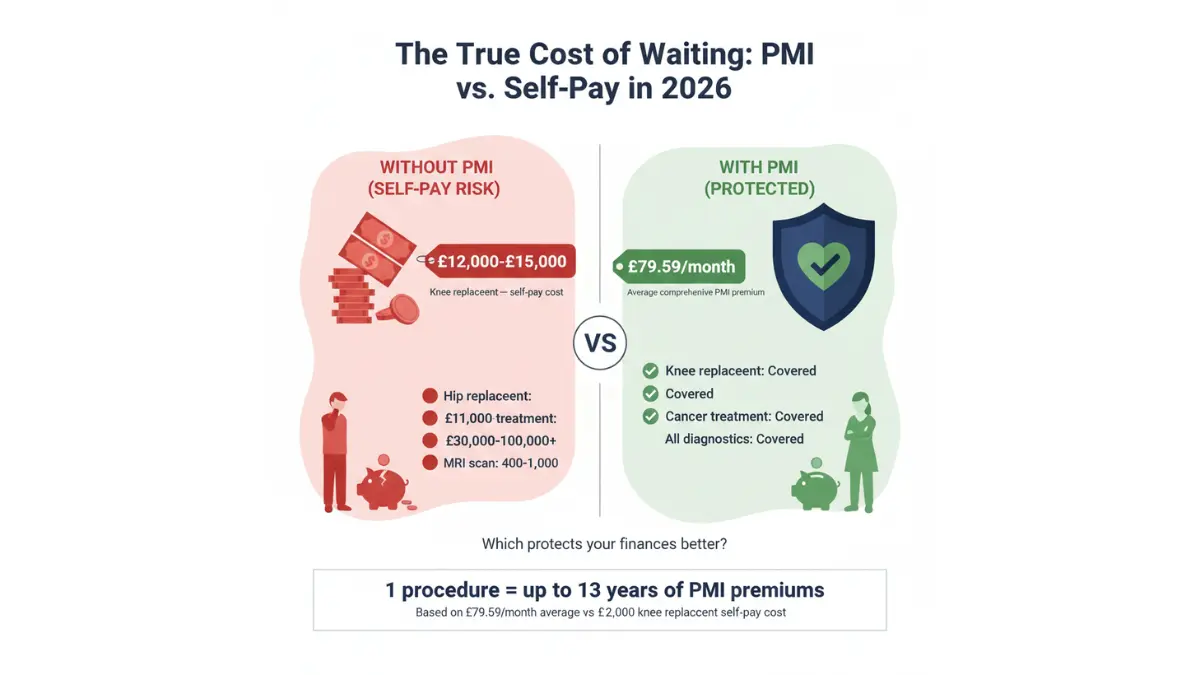

Is Private Medical Insurance Worth It? The Financial Case

This is the question every competitor avoids answering directly. Here is the honest financial answer.

With the NHS elective care backlog at record levels, the financial risk of not having PMI has fundamentally changed. Self-paying for a single major procedure can cost more than a decade of premiums.

The £10,000+ Self-Pay Reality — 2026 Procedure Cost Comparison

| Procedure | Self-Pay Cost | Annual PMI Premium (40yr old) | PMI Verdict |

|---|---|---|---|

| Knee replacement | £12,000–£15,000 | ~£1,080/year | ✅ PMI wins after 1 year |

| Hip replacement | £11,000–£14,000 | ~£1,080/year | ✅ PMI wins after 1 year |

| Cataract surgery | £2,500–£3,500 | ~£1,080/year | ✅ PMI wins after ~2 years |

| MRI Scan | £400–£1,000 | ~£1,080/year | ✅ 1 scan = ~10 months of premiums |

| Cancer treatment | £30,000–£100,000+ | ~£1,080/year | ✅ Unmistakably worth it |

| Rotator cuff surgery | £6,000–£9,000 | ~£1,080/year | ✅ PMI wins after ~6 years |

Figures based on UK private hospital self-pay estimates. Individual costs vary by hospital and consultant.

Real Case Study: Sarah, 44, Self-Employed Marketing Consultant

Sarah developed persistent shoulder pain in late 2025. Her NHS GP referred her to an orthopaedic specialist — wait time: 19 weeks for an appointment, then a further 12 weeks for an MRI.

Using her PMI policy (premium: £94/month):

- Saw a private specialist in 4 days

- Had an MRI scan in 6 days

- Rotator cuff tear diagnosed. Surgery booked in 3 weeks

- Back at full capacity in 8 weeks

- Total out-of-pocket cost: £250 excess

- Lost income avoided: estimated £8,000–£12,000 (8 months of reduced work capacity vs. 8 weeks)

For self-employed professionals, PMI is not just a healthcare decision — it is income protection. Our Health Insurance Expert Math guide breaks down the financial logic in full.

Who Gets the Most Value from PMI in 2026?

The Self-Employed Professional

- No employer sick pay safety net

- Income directly linked to ability to work

- PMI + income protection = complete financial shield

- Workers’ compensation and self-employed healthcare planning are closely linked

The Family with Children

- Adding children to a family policy costs relatively little (typically £10–£15/child)

- Some insurers offer free cover for newborns for the first year

- Fast access to paediatric consultants without months of waiting

The Over-50 Planning for Retirement

- Health conditions statistically accelerate from age 50

- Buying PMI before conditions develop locks in lower premiums and broader coverage

- Pairs strategically with retirement planning in your 30s as part of holistic financial planning

PMI vs. Self-Pay vs. NHS: 3-Way Decision Framework

| Scenario | Best Option | Why |

|---|---|---|

| Emergency (heart attack, broken bone) | NHS | A&E is NHS — PMI doesn’t cover this |

| GP visit, repeat prescription | NHS | PMI doesn’t cover routine GP care |

| Elective surgery (joint replacement) | PMI | Skip 12–18 month NHS wait |

| One-off diagnostic scan needed fast | Self-pay (MRI from ~£400) or PMI | Depends on urgency and policy excess |

| Cancer diagnosis and treatment | PMI | Access to drugs not yet NHS-approved; fastest diagnosis pathway |

| Ongoing chronic condition management | NHS | PMI doesn’t cover chronic conditions |

Choosing the Right Private Medical Insurance — 2026 Buyer’s Guide

Not all PMI policies are equal. The right policy depends on your life stage, budget, and priorities. Here is what to look for — and what to avoid.

Top UK Private Medical Insurance Providers at a Glance — 2026

| Provider | Best For | Key Strength | Notable Feature |

|---|---|---|---|

| Bupa | Comprehensive cover | Largest hospital network | Direct Access — no GP referral needed for some conditions |

| AXA Health | Digital-first users | 24/7 virtual GP app | Strong mental health coverage |

| Aviva | Families | 1.2M+ members, wide network | Digital GP included at no extra cost |

| Vitality | Health-active people | Rewards for healthy behaviour | Premium discounts for exercise and healthy living |

| The Exeter | Pre-existing conditions | Flexible FMU underwriting | Best for complex medical histories |

| WPA | Customer service | Highest claims satisfaction | No-claims discount protection options |

Provider data based on 2026 Trustpilot ratings, Which? customer surveys, and published policy comparisons. Always get at least 3 quotes before committing.

Your 5-Step PMI Buying Checklist

Follow this before purchasing any private health insurance policy:

- Step 1 — Define your core need. Speed of access? Cancer cover? Mental health support? Knowing your priority shapes everything else.

- Step 2 — Choose your cover level. Basic (inpatient only) for budget buyers; mid-range for most adults; comprehensive if you want full outpatient diagnostics included.

- Step 3 — Decide your underwriting type. Moratorium for simplicity; FMU for clarity. See Section 1 for the decision guide.

- Step 4 — Set your excess strategically. A £500 excess vs. £0 can cut your monthly premium by 20%+. Only set an excess you can genuinely afford to pay.

- Step 5 — Compare at least 3 quotes. Premiums for identical cover can vary by 30–40% between providers for the same individual.

Employer PMI vs. Personal PMI — The Tax Angle You Must Know

If your employer provides PMI as a benefit, HMRC treats it as a taxable benefit in kind. You’ll pay income tax on the premium value through your payroll.

Key considerations:

- Employer PMI only covers you while employed there — it disappears if you change jobs

- You cannot always choose your own policy terms or excess

- Personal PMI gives you full control and portability

Self-Employed PMI: The Tax Rules in 2026

For self-employed individuals and sole traders in the UK, PMI premiums are not currently tax-deductible as a personal expense. However, if you operate through a limited company, the company can pay for PMI as a business expense — though it becomes a taxable benefit in kind for the director.

For full employer reporting obligations, see GOV.UK’s guide to medical treatment expenses and benefits. This is a critical area to clarify with your accountant — the tax treatment directly affects the real cost of your policy.

Understanding PMI is one layer of financial protection planning. Alongside it, reviewing your life insurance costs and types and term life insurance creates a complete financial safety net. For those weighing up all insurance costs together, our cheap insurance strategies guide offers practical ways to optimise your total protection spend.

If you want to understand how PMI premiums fit into your total household financial picture, our Mortgage Refinance Calculator helps model your full monthly obligations.

Reading Mode — The Expert Financial Perspective

The Association of British Insurers (ABI) reports that private medical insurance demand continues to rise in the UK, driven by sustained NHS capacity pressures and rising medical inflation estimated at 8–10% annually.

What this means practically for buyers in 2026:

- PMI premiums are rising — locking in a policy now, before your health profile changes, means lower long-term cost

- Medical inflation outpaces general inflation — the cost of self-paying for procedures is rising faster than PMI premiums

- Insurer competition is increasing — the market is more competitive than 5 years ago, making it a strong time to shop and compare

The NHS Confederation’s analysis of waiting list pressures confirms that without a dramatic increase in NHS capacity, elective wait times are structurally unlikely to improve in the short term. This structural backdrop is what makes PMI a rational financial decision for millions of households — not a luxury.

For broader financial planning context — especially if you’re weighing PMI against other financial priorities — our guide to health insurance plans covers the wider landscape of health protection options available in 2026.

Private Medical Insurance FAQs — Expert Answers

1. What is private medical insurance?

Private medical insurance is a policy that covers the cost of private healthcare for acute (new, curable) medical conditions. You pay a monthly or annual premium, and your insurer pays your private treatment costs, allowing you to bypass NHS waiting lists.

2. How much does private medical insurance cost per month in the UK?

The average cost of private health insurance in 2026 is £79.59/month for an adult, £145.77 for a couple, and £166.52 for a family of four. Premiums start from around £28/month for a healthy 20-year-old on basic cover.

3. What does private medical insurance cover?

PMI covers acute conditions that arise after your policy starts — including elective surgery, specialist consultations, diagnostic scans (MRI, CT, X-ray), cancer treatment, physiotherapy, and mental health support (on most policies).

4. What is NOT covered by private medical insurance?

PMI does not cover: emergency A&E treatment, chronic conditions (diabetes, asthma, arthritis), pre-existing conditions (in most cases, initially), GP visits, cosmetic procedures, or pregnancy and maternity care.

5. Is private medical insurance tax-deductible in the UK?

For individuals, PMI premiums are generally not tax-deductible. For limited company directors, the company can pay PMI as a business expense, but it becomes a taxable benefit in kind. See HMRC’s guidance for the full reporting rules.

6. Can I get private medical insurance with pre-existing conditions?

Yes, but pre-existing conditions are typically excluded initially. Under moratorium underwriting, a condition may become covered after 2 consecutive years without symptoms or treatment. Under FMU, exclusions are confirmed upfront. Specialist providers like The Exeter offer more flexible terms for complex histories.

7. What is moratorium underwriting vs. full medical underwriting?

Moratorium: No upfront health questionnaire. Conditions from the past 5 years are auto-excluded but may become covered after 2 symptom-free years on the policy. FMU: Full health questionnaire at application. Every exclusion is listed from day one. Choose FMU if you have a complex health history and want certainty.

8. Is private health insurance worth it if I can use the NHS?

For many people in 2026 — yes. With NHS waiting lists for non-urgent procedures reaching record levels, the elective care waiting list in England stood at over 7.6 million treatment pathways in early 2026. One procedure can cost more than years of combined premiums when self-paid.

9. How does the 6-week NHS wait option work?

You only use private insurance if the NHS cannot treat you within 6 weeks. If NHS treatment is available within that window, you use the NHS. This option can reduce your premium by up to 30% — but some insurers have suspended it due to current NHS backlog levels, so confirm availability before selecting.

10. Can self-employed people get private medical insurance?

Yes. Self-employed individuals can purchase PMI as individuals. If you operate through a limited company, the company can pay the premium as a business expense, though tax implications apply. For broader self-employed financial planning, our health insurance guide covers the full protection picture.

11. How do I make a claim on private medical insurance?

Typically:

(1) See your GP and get a referral letter.

(2) Contact your insurer before booking — get pre-authorisation for the treatment.

(3) Choose a hospital or specialist from your insurer’s approved list.

(4) Your insurer pays the hospital directly, minus any excess you owe.

🏆 Expert Verdict

Private medical insurance in 2026 is no longer a luxury for the wealthy. With NHS waiting lists at structural highs, medical inflation running at 8–10% annually, and self-pay procedure costs routinely exceeding £10,000, PMI offers genuine financial protection for individuals, families, and self-employed professionals alike.

The financial case is simple: A comprehensive policy costs an average of £79.59/month. One elective surgical procedure — without PMI — costs £11,000–£15,000. The maths has shifted firmly in favour of cover.

Start with 3 quotes, match your cover level to your actual priorities, and treat PMI as part of your complete financial protection strategy — alongside life insurance, dental insurance, and your broader insurance planning.

⚠️ Disclaimer: This article is for educational and informational purposes only. It does not constitute financial, medical, or insurance advice. Private medical insurance products vary significantly by provider, individual health status, and policy terms. Always consult a qualified, FCA-authorised insurance adviser before purchasing any policy. Premium figures cited are illustrative averages based on 2026 market research and will vary based on your personal circumstances. Finance Authority Hub is not an insurance broker and does not sell or endorse any specific insurance product.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.