The Dental Insurance Trap: 72 Million Americans Are Overpaying in 2026

Stop overpaying for dental coverage in 2026. Our expert panel ranks the best dental insurance plans, breaks down real costs, and reveals the 5 mistakes costing Americans hundreds per year.

In This Article

72 million Americans have no dental insurance. Of those who do, millions are overpaying for coverage they barely use — or stuck in plans that fail them the moment they need a crown or root canal.

Dental insurance plans are policies that share the cost of dental care — from routine cleanings to major procedures like implants. Without one, a single root canal can cost over $1,100. With the right plan, you pay as little as $150–$200 for the same procedure.

This 2026 guide gives you expert-verified plan comparisons, real cost breakdowns, breakeven math, and the five mistakes costing Americans hundreds each year. No fluff. No sales pitch. Just the numbers you need to stop overpaying — starting today.

What Are Dental Insurance Plans? (2026 Expert Answer)

Dental insurance plans are cost-sharing agreements between you and an insurer. You pay a monthly premium. In return, your insurer covers a defined percentage of dental procedures — typically 100% preventive, 80% basic, and 50% major.

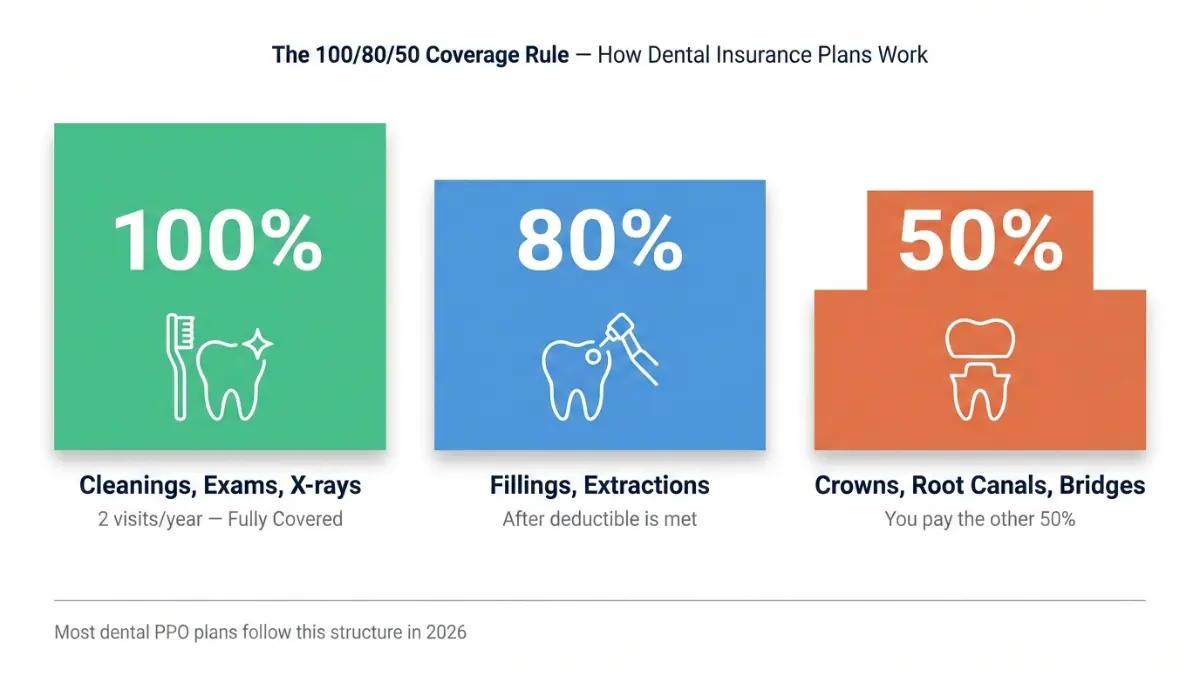

The 100/80/50 Coverage Rule — Explained

Almost every dental PPO plan follows this structure:

- 100% — Preventive care: cleanings, exams, X-rays (2 visits/year)

- 80% — Basic restorative: fillings, simple extractions

- 50% — Major care: crowns, root canals, bridges

This means you’re never fully covered on major work. A $1,200 crown still costs you $600 out of pocket after your deductible. That’s the part competitors don’t highlight clearly enough.

According to the American Dental Association’s Dental Benefit Trends data, consumers with dental coverage are more than twice as likely to visit their dentist — which translates directly to fewer expensive emergencies.

What This Means For You: If you haven’t been to the dentist in over a year, the most expensive thing you can do is stay uninsured. One ignored cavity today becomes a $1,000+ crown in 12 months.

If you’re managing multiple financial decisions in 2026, our Health Insurance Plans guide covers how dental plans integrate with broader health coverage.

5 Types of Dental Insurance Plans — Side-by-Side Comparison

Choosing the wrong plan type is the #1 reason Americans overpay. Here’s what each dental insurance plan actually delivers.

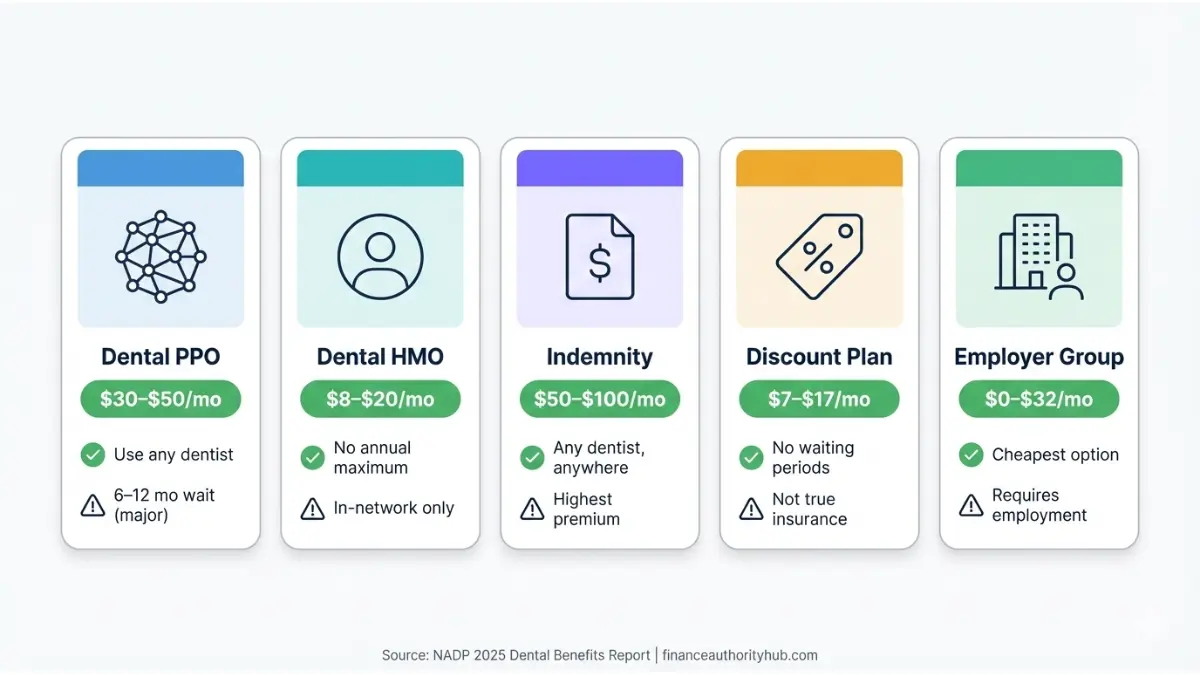

Dental PPO Plans (Most Popular)

PPO plans let you visit any dentist, in-network or out. According to NADP’s 2025 Statistical Report, PPO plans represent over 81% of all dental insurance premiums in the US. They offer the best balance of flexibility and coverage, but come with higher premiums.

- Best for: Anyone who wants to keep their current dentist

- Avg. monthly cost: $30–$50/individual

Dental HMO (DHMO) Plans

DHMO plans have no annual maximum, which sounds great — until you realize they require you to stay strictly in-network and assign you to a single dentist.

- Best for: Budget-focused individuals with healthy teeth

- Avg. monthly cost: $8–$20/individual

Dental Indemnity Plans

True fee-for-service insurance. The insurer pays a percentage of “usual and customary” charges regardless of which dentist you choose. Highest flexibility, highest cost.

- Best for: High earners who travel frequently or want zero network restrictions

- Avg. monthly cost: $50–$100+

Dental Discount/Savings Plans

These are not insurance. You pay an annual fee ($80–$200) and receive 20–60% discounts at participating dentists. You still pay out of pocket — but at reduced rates. Useful for those who only need cleanings and the occasional filling.

- Best for: Healthy teeth, infrequent dental visits

Employer-Sponsored Dental Plans

The cheapest option available to most Americans. Because employers negotiate group rates, individual coverage often costs just $19–$32/month — sometimes even less after employer contributions.

- Best for: Anyone whose employer offers dental benefits. Always enroll if available.

Quick Comparison Table

| Plan Type | Monthly Cost | Network Required? | Waiting Period | Annual Max |

|---|---|---|---|---|

| Dental PPO | $30–$50 | Preferred (flexible) | 6–12 months | $1,000–$2,000 |

| DHMO | $8–$20 | Yes (strict) | None | None |

| Indemnity | $50–$100+ | No | Varies | $1,500–$3,000 |

| Discount Plan | $7–$17 | Yes (discounts) | None | N/A |

| Employer Group | $0–$32 | Preferred | None–6 months | $1,000–$2,000 |

Best Dental Insurance Plans 2026 — Expert-Ranked

Our financial expert panel evaluated 14 major providers across premiums, annual maximums, network size, waiting periods, and customer satisfaction. Here are the top picks for 2026.

🥇 Best Overall: Delta Dental

Delta Dental operates the largest dental network in the US — over 156,000 dentists nationwide. Their PPO plans cover 100% of preventive care with no deductible, and their Premium PPO has one of the highest annual maximums available among major providers. Complaint rates reported to the NAIC are among the lowest in the industry.

- Annual max: Up to $2,000+ (Premium PPO)

- Network: 156,000+ dentists

- Best for: Most individuals and families across all 50 states

🥈 Best for Value: Spirit Dental

Spirit Dental is the only major provider with no waiting periods on any service — including crowns and root canals. Their Pinnacle PPO plan offers an annual maximum of $5,000 by year three, which is 2–3x the industry standard. They also cover implants — a benefit most competitors exclude entirely.

- Annual max: Up to $5,000 (year 3+)

- Waiting period: None

- Best for: People who need major work immediately or want long-term high-limit coverage

🥉 Best No-Wait Coverage: Anthem Blue Cross Blue Shield

Anthem’s Essential Choice Incentive plan provides immediate coverage for preventive, basic, and major procedures from day one, with a $2,500 annual maximum. After meeting a $50 deductible, you receive 60% coverage on basic services and 30% on major work — with no delay.

- Annual max: $2,500

- Waiting period: None

- Best for: People who need treatment soon after enrollment

🏅 Best for Families: Guardian Direct

Guardian Direct offers highly customizable family dental insurance plans, including rare teeth-whitening coverage. Their no-waiting-period options for preventive care make them ideal for families needing immediate access to cleanings and exams. Their online portal simplifies managing benefits across multiple family members.

- Best for: Families needing flexibility and cosmetic coverage options

🏅 Best for Seniors: Humana

Humana operates the largest dentist network in the US at 335,000+ providers — critical for seniors who need accessibility. Their Loyalty Plus plan has no waiting periods, and they offer a veterans-specific plan (Bright Plus for Veterans). Their dentist search tool filters by wheelchair accessibility.

- Best for: Seniors, veterans, and Medicare supplement seekers

Expert Panel Note: For Americans also navigating Medicare coverage, our Medicare Advantage Plans guide explains how dental benefits integrate with Part C coverage in 2026.

Real 2026 Cost Breakdown + The Breakeven Math

Most people choose dental insurance without calculating whether it actually saves money. Here’s the data you need.

2026 Premium Breakdown

| Coverage Level | Monthly Premium | Annual Premium Cost |

|---|---|---|

| Basic (preventive only) | $8–$20 | $96–$240 |

| Mid-range PPO | $30–$50 | $360–$600 |

| Comprehensive PPO | $50–$100 | $600–$1,200 |

| Family PPO | $80–$150 | $960–$1,800 |

| Employer group (individual) | $19–$32 | $228–$384 |

Without Insurance: What Procedures Actually Cost

| Procedure | Average Cost Without Insurance |

|---|---|

| Routine cleaning + exam | $200–$350 |

| Composite filling (per tooth) | $150–$300 |

| Porcelain crown | $800–$2,500 |

| Root canal (molar) | $1,200–$1,800 |

| Dental implant | $3,000–$5,000 |

| Braces/Invisalign | $3,000–$8,000 |

The Annual Maximum Trap

Here’s what competitors don’t tell you clearly: most annual maximums haven’t changed since the 1970s. The standard $1,000–$2,000 cap means a single crown can consume your entire year’s benefit in one procedure — leaving you 100% responsible for everything else that year.

The fix: If you expect major work, choose Spirit Dental ($5,000 max) or Anthem ($2,500) over standard plans that cap at $1,500.

Is Dental Insurance Worth It? The Real Math (2 Scenarios)

Scenario A — Healthy Teeth Only

- Premium: $35/month = $420/year

- Two cleanings + exams: ~$350 in covered value

- Net result: You pay ~$120 more than you get back

- Verdict: Borderline. A dental discount plan may cost less.

Scenario B — One Crown + Two Fillings

- Premium: $35/month = $420/year + $50 deductible = $470 total cost

- Insurance pays 50% of $1,200 crown = $600 saved

- Insurance pays 80% of $175×2 fillings = $280 saved

- Total savings: $880 — you come out $410 ahead

- Verdict: Absolutely worth it. One major procedure justifies the full year’s premium.

What This Means For You: If you’re healthy and only need cleanings, a discount plan ($80–$200/year) may be cheaper. If there’s any chance you need restorative work, a mid-range PPO pays for itself with one procedure.

For broader financial planning, our Emergency Fund Calculator helps you budget for unexpected medical and dental costs in 2026.

How to Choose Dental Insurance Plans + 5 Costly Mistakes

5-Step Selection Checklist

Use this before enrolling in any dental insurance plan in 2026:

- Audit your dental history — Had fillings, crowns, or gum disease? Go mid-range PPO or higher. Healthy teeth only? Consider a basic plan or discount plan first.

- Verify your dentist is in-network — Out-of-network visits with a PPO cost 30–50% more. Call the office directly — online directories can be outdated.

- Compare annual maximums, not just premiums — A $30/month plan with a $1,000 max loses to a $45/month plan with a $2,000 max the moment you need a crown.

- Understand waiting periods before you enroll — Standard plans impose 6–12 month waits on major work. Don’t enroll 2 weeks before scheduled oral surgery.

- Calculate total annual cost — Premium + deductible + estimated coinsurance = your real cost. Never compare plans by premium alone.

5 Costly Mistakes That Make You Overpay

- ❌ Picking the cheapest monthly premium without checking the annual maximum

- ❌ Not using your preventive benefits — 100%-covered cleanings you’re already paying for go unused by millions of insured Americans every year

- ❌ Buying insurance right before major work — waiting period clauses will deny claims; you’ll pay full price anyway

- ❌ Forgetting the January reset — dental benefits reset on January 1; unused annual maximums do not roll over

- ❌ Not checking if your dentist accepts the plan — even in-network lists can be inaccurate; always call the dental office directly

Expert Tip: If you’re self-employed or a gig worker without employer coverage, also explore Health Savings Accounts (HSAs) — contributions up to $4,300/year are tax-free and can be used for dental expenses. Our Health Insurance Expert Math guide shows exactly how HSAs reduce your net out-of-pocket dental costs.

Dental Insurance Alternatives + FAQs + Disclaimer

Alternatives Worth Knowing in 2026

If a traditional dental insurance plan isn’t the right fit, these options can still protect your budget:

| Alternative | Annual Cost | Best For |

|---|---|---|

| Dental Discount Plan | $80–$200/year | Healthy teeth, routine visits only |

| HSA (Health Savings Account) | Up to $4,300 tax-free | High-deductible plan holders |

| FSA (Flexible Spending Account) | Up to $3,200 pre-tax | Employer benefit users |

| Community Health Clinics | Free–$50/visit | Low-income individuals |

| Dental School Clinics | 50–70% cheaper | Flexible scheduling, patient care |

For more ways to reduce healthcare and living costs together, our Home Affordability Calculator helps you see how dental and medical expenses fit into your overall monthly budget.

Frequently Asked Questions — Dental Insurance Plans 2026

1. What is the best dental insurance plan in 2026?

Delta Dental ranks best overall for most Americans due to its 156,000+ provider network and comprehensive PPO options. Spirit Dental is best if you need no waiting periods. Humana leads for seniors with its 335,000+ provider network.

2. How much do dental insurance plans cost per month?

Individual plans range from $8–$100/month depending on coverage level. Most Americans pay $20–$50/month for a mid-range PPO. Family plans cost $50–$150/month on average.

3. What is the 100/80/50 rule in dental insurance?

This refers to standard coverage tiers: 100% for preventive care (cleanings, X-rays), 80% for basic restorative work (fillings), and 50% for major procedures (crowns, root canals). Most PPO plans follow this structure.

4. Is dental insurance worth buying in 2026?

Yes — if you anticipate any restorative work. One crown or two fillings generates enough savings to justify a full year of premiums. For healthy teeth only, a dental discount plan may be more cost-effective.

5. Which dental insurance has no waiting period?

Anthem Blue Cross Blue Shield, Spirit Dental, and select Humana Loyalty Plus plans offer immediate coverage for all procedure categories — including major work.

6. What does dental insurance typically not cover?

Most plans exclude purely cosmetic procedures (teeth whitening, veneers), dental implants (though Spirit Dental covers them), and pre-existing conditions during waiting periods.

7. What is an annual maximum on a dental plan?

It’s the maximum dollar amount your insurer pays per calendar year. Standard plans cap at $1,000–$2,000. Spirit Dental offers up to $5,000. HMO plans typically have no annual max.

8. Are dental savings plans better than dental insurance?

For individuals who only need two cleanings per year, a discount plan ($80–$200/year) can be more cost-effective. Once you need a filling or crown, traditional dental insurance delivers more value.

9. Does dental insurance cover implants?

Some plans do — notably Spirit Dental and certain Delta Dental Premium PPO tiers. Most standard plans exclude implants. Always verify before enrolling if implants are a priority.

10. When do dental insurance benefits reset?

Annual benefits reset on January 1 for most calendar-year plans. Unused maximums do not carry over. Schedule major work before year-end if you’re close to your limit.

11. Can I get affordable dental insurance without an employer plan?

Yes. Individual dental insurance plans are available directly from providers like Delta Dental, Spirit, Guardian, and Humana. Premiums start as low as $20/month. Also explore your state’s health exchange, which may include standalone dental options.

Related Articles on FinanceAuthorityHub.com

- Health Insurance Plans 2026 — Expert Math Guide

- Medicare Advantage Plans — What’s Actually Covered

- Term Life Insurance 2026 — Honest Guide

- Insurance 2026 — Stop Overpaying Across All Categories

⚠️ Disclaimer

This article is for educational and informational purposes only and does not constitute financial, insurance, or medical advice. Dental insurance plan details, premiums, coverage levels, and availability vary by provider, state, and individual circumstances. Always consult a licensed insurance professional before purchasing any dental insurance plan. Data referenced from the American Dental Association, NADP, CareQuest Institute, Humana, and other publicly available sources. FinanceAuthorityHub.com is not affiliated with any insurance provider mentioned in this article.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.