Annuity: $461B Industry’s Biggest Secret Revealed

Americans poured $461B into annuities in 2025. Our certified financial experts break down all 5 types, real 2026 payout tables, and the fastest-growing product most retirees have never heard of.

In This Article

Quick Answer: An annuity is a contract between you and an insurance company. You pay a lump sum or series of payments. In return, you receive guaranteed income — either immediately or at a future date — for a set period or for life. It is the only financial product designed to ensure you never outlive your money.

What Is an Annuity? (The $461B Answer Everyone Gets Wrong)

Americans invested $461.3 billion in annuities in 2025 — a fourth consecutive record year, according to LIMRA’s 2026 Annuity Sales Survey. Yet most buyers sign a contract without understanding what they actually purchased.

An annuity is a legal contract issued by an insurance company. You transfer money — in one lump sum or installments — and the insurer promises to return it as a guaranteed income stream. That stream can start within 30 days or decades from now, depending on the annuity type you choose.

Key Takeaway: An annuity converts your savings into predictable income you cannot outlive. It is one of the only financial products that protects against longevity risk — the fear of running out of money in retirement.

How Does an Annuity Work? (3-Step Process)

- Accumulation Phase — You pay your premium to the insurance company (lump sum or over time). Your money grows tax-deferred inside the contract.

- Growth Phase — Depending on the annuity type, your money earns a fixed interest rate, tracks a market index, or invests in sub-accounts.

- Distribution Phase (Payout) — You begin receiving income payments — monthly, quarterly, or annually — for a fixed period or for the rest of your life.

The U.S. Securities and Exchange Commission via Investor.gov defines an annuity as “a contract between you and an insurance company that requires the insurer to make payments to you, either immediately or in the future.” That definition is simple. The strategy behind choosing the right one is not.

The 3 Participants in Every Annuity Contract

| Role | Who They Are | What They Do |

|---|---|---|

| Owner | You (the buyer) | Pays premiums, controls the contract |

| Annuitant | Usually the owner | Receives income payments; age determines payout amount |

| Beneficiary | Spouse, child, or estate | Receives death benefit if annuitant dies before payout begins |

What This Means For You: If you are planning retirement income alongside your other obligations — like evaluating your mortgage refinance options — understanding which role you play in an annuity contract determines how benefits are paid and to whom.

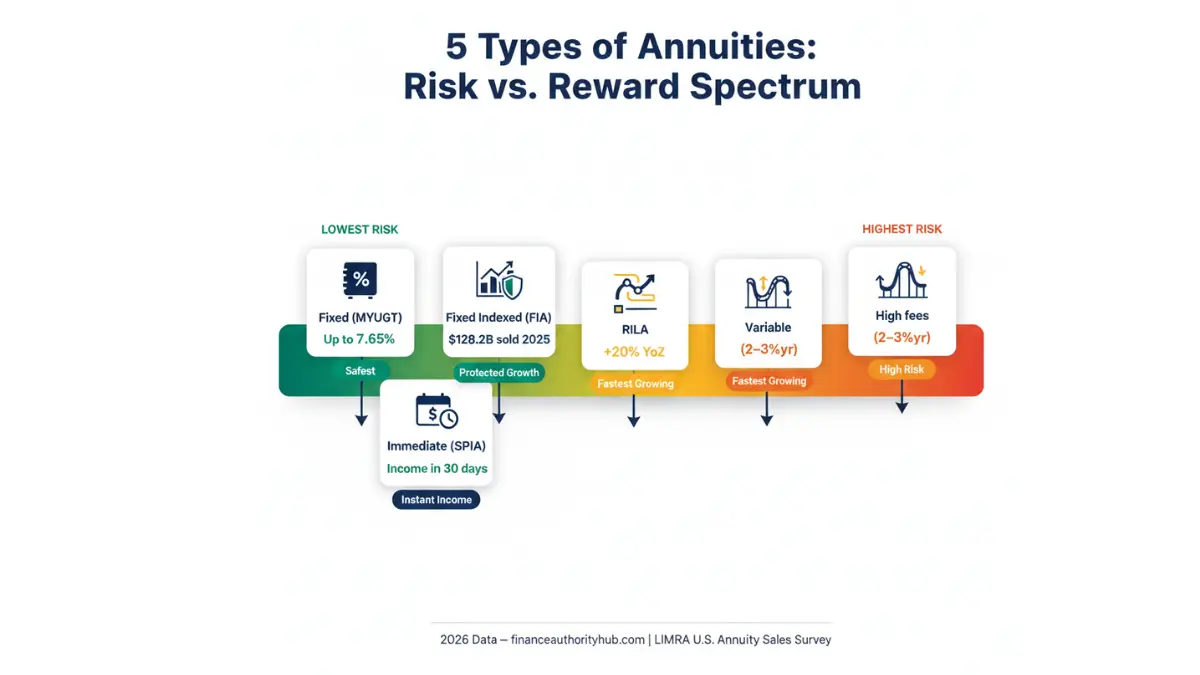

All 5 Types of Annuities Explained (Including the One Growing 10x in a Decade)

Not all annuities work the same way. Choosing the wrong type could cost you tens of thousands in locked-up funds or missed growth. Here is the complete 2026 breakdown.

The 5 Types of Annuities: Master Comparison Table (2026)

| Type | Risk Level | Growth Potential | Principal Protection | Best For | 2026 Avg. Rate |

|---|---|---|---|---|---|

| Fixed (MYGA) | Very Low | Low–Moderate | ✅ Yes | Conservative retirees | Up to 7.65% (10yr) |

| Fixed Indexed (FIA) | Low | Moderate | ✅ Yes | Balanced growth + safety | Cap rates up to 10.75% |

| RILA | Low–Moderate | Moderate–High | Partial (buffer) | Growth-oriented retirees | Index-linked |

| Variable | High | High | ❌ No | Aggressive investors | Market-dependent |

| Immediate (SPIA) | None | None | N/A | Instant income retirees | Based on age + deposit |

Fixed Annuity (MYGA) — The Safe Play

A fixed annuity (also called a Multi-Year Guaranteed Annuity, or MYGA) locks in a guaranteed interest rate for a set term — typically 3, 5, 7, or 10 years.

- As of February 2026, the top 10-year fixed annuity rate is 7.65% (Atlantic Coast Life)

- Top 3-year rate: 5.85% — which currently beats the best 3-year CD rate of 4.65%

- Interest grows tax-deferred — you pay no taxes until withdrawal

- Most contracts allow 10% annual penalty-free withdrawals

Real Example: A 65-year-old invests $100,000 in a 5-year MYGA at 5.50%. At the end of the term, the guaranteed value is approximately $130,696 — with no market risk whatsoever.

Fixed Indexed Annuity (FIA) — The Middle Ground

A fixed indexed annuity links your interest earnings to a market index — most commonly the S&P 500 — but protects your principal from market losses.

- $128.2 billion sold in 2025 (5th consecutive year of record FIA sales — LIMRA)

- Uses cap rates (maximum earn) and participation rates (% of index gain credited)

- Current top cap rates: up to 10.75% for 5, 7, and 10-year terms (Feb 2026)

- Your account value cannot go below zero due to market downturns

RILA — The $79.6B “Secret” Most Retirees Have Never Heard Of

This is what competitors are missing. A Registered Index-Linked Annuity (RILA) is the fastest-growing annuity product in America — and barely any mainstream finance site covers it properly.

- RILA sales hit $79.6 billion in 2025 — up 20% year-over-year (LIMRA)

- That is 10 times the sales recorded a decade ago

- LIMRA projects RILA sales to exceed $85 billion in 2026

- RILAs offer a buffer against market losses (e.g., absorbs first 10% of index losses) while allowing higher upside than FIAs

- First outpaced variable annuity sales in Q4 2023 — the market is pivoting fast

If you are building a comprehensive retirement planning strategy in your 30s or 40s, RILAs deserve serious consideration before they become as mainstream — and expensive — as 401(k)s.

Variable Annuity — Proceed with Caution

A variable annuity invests your premium into sub-accounts — essentially mutual funds. Your payout depends entirely on how those investments perform.

- The SEC and FINRA have both issued public warnings about variable annuities due to high costs, complexity, and aggressive sales tactics

- Commissions can reach up to 10% on some contracts

- Annual fees (mortality, expense, rider fees) can reduce returns by 2–3% per year

- Variable annuities rank among the top sources of consumer complaints filed with FINRA

Immediate Annuity (SPIA) — Turn Cash Into Income Today

A Single Premium Immediate Annuity (SPIA) starts paying you within 30 days to 12 months of purchase. You hand over a lump sum — no accumulation phase.

- Best for retirees who need income right now

- Payout is locked in for life (or a set period) based on your age and deposit

- No ongoing fees — the insurer builds their profit margin into the payout rate

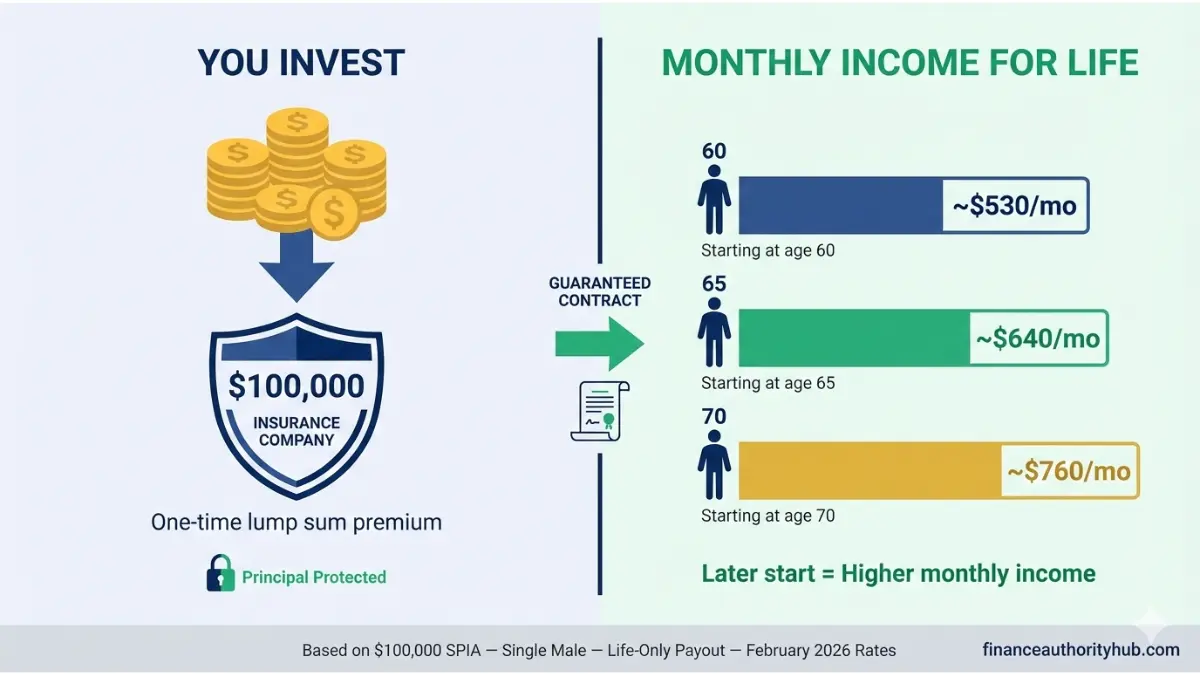

How Much Does an Annuity Pay? (Real 2026 Payout Tables)

What This Means For You: The #1 financial fear among American retirees is running out of money — not a market crash, not inflation. An annuity directly eliminates that fear with a guaranteed income floor. Here is exactly what you can expect to receive.

Real Annuity Payout Examples — February 2026 Rates

The table below shows actual estimated monthly income from an immediate income annuity (life-only payout), based on current February 2026 market rates.

| Investment | Age 60 | Age 65 | Age 70 |

|---|---|---|---|

| $100,000 | ~$530/mo | ~$640/mo | ~$760/mo |

| $250,000 | ~$1,325/mo | ~$1,600/mo | ~$1,900/mo |

| $500,000 | ~$2,650/mo | ~$3,200/mo | ~$3,800/mo |

Estimates based on 2026 SPIA quotes for a single male. Women typically receive 5–8% less per month due to longer life expectancy. Actual quotes vary by insurer, state, and payout option.

What Factors Determine Your Annuity Payout?

- Your age — older buyers receive higher monthly payments (shorter expected payout period)

- Your gender — women statistically live longer, so insurers pay them less per month

- Payment start date — delaying payments (deferred) significantly increases future payout

- Payout type — life-only pays the most; joint-life (with spouse) pays less

- Interest rate environment — 2026 rates remain near 15-year highs, meaning now is a historically strong time to lock in

Best Fixed Annuity (MYGA) Rates — February 2026

| Term | Top Rate | Insurer |

|---|---|---|

| 3-Year | 5.85% | Available from multiple A-rated carriers |

| 5-Year | 6.50%+ | Available from multiple A-rated carriers |

| 7-Year | 6.75%+ | Available from multiple A-rated carriers |

| 10-Year | 7.65% | Atlantic Coast Life |

Bold Callout: Fixed annuity rates remain significantly above bank CD rates in 2026. A 3-year MYGA at 5.85% beats the best 3-year CD (4.65%) by over 120 basis points — that difference on $250,000 adds up to more than $9,000 in additional guaranteed interest.

If you are also weighing whether to pay off debt vs. invest, clearing high-interest debt first before locking funds into an annuity is strongly advisable — annuity surrender periods can run 7–10 years.

Annuity Pros, Cons & Who Should (and Shouldn’t) Buy One

What Certified Financial Planners Say in 2026

“An annuity is not an investment — it is insurance against outliving your money. When used correctly as part of a retirement income floor strategy, it removes the single biggest risk retirees face: longevity risk. When sold incorrectly, it is an expensive mistake that traps your money for a decade.” — Daniel Moreau, Certified Financial Planner®, financeauthorityhub.com Expert Panel

Annuity Pros vs. Cons — Side-by-Side (2026)

| ✅ Pros | ❌ Cons |

|---|---|

| Guaranteed lifetime income — you cannot outlive payments | Surrender charges last 7–10 years on most contracts |

| Tax-deferred growth — no taxes until withdrawal | Sales commissions can reach 10% on complex products |

| Protects principal (fixed and indexed types) | Variable annuities have no principal protection |

| Death benefit for beneficiaries | Inflation risk on fixed payouts over 20–30 years |

| Customizable with riders (income, long-term care) | Riders add 0.5–1.5%/year in additional fees |

| No contribution limits (unlike IRA/401k) | Early withdrawal before age 59½ = 10% IRS penalty |

Can You Lose Money in an Annuity?

The answer depends entirely on the type:

- Fixed annuity (MYGA): No. Your principal and guaranteed rate are contractually protected by the insurer.

- Fixed Indexed Annuity (FIA): No. A 0% floor means market losses are never passed to you.

- RILA: Partially. A buffer absorbs the first 10–15% of losses; losses beyond the buffer are yours.

- Variable annuity: Yes. Your sub-account investments can and do lose value in market downturns.

As the IRS notes in Tax Topic 410, annuity withdrawals are taxed as ordinary income — not at the lower capital gains rate. This distinction matters significantly when comparing annuities to other investment options.

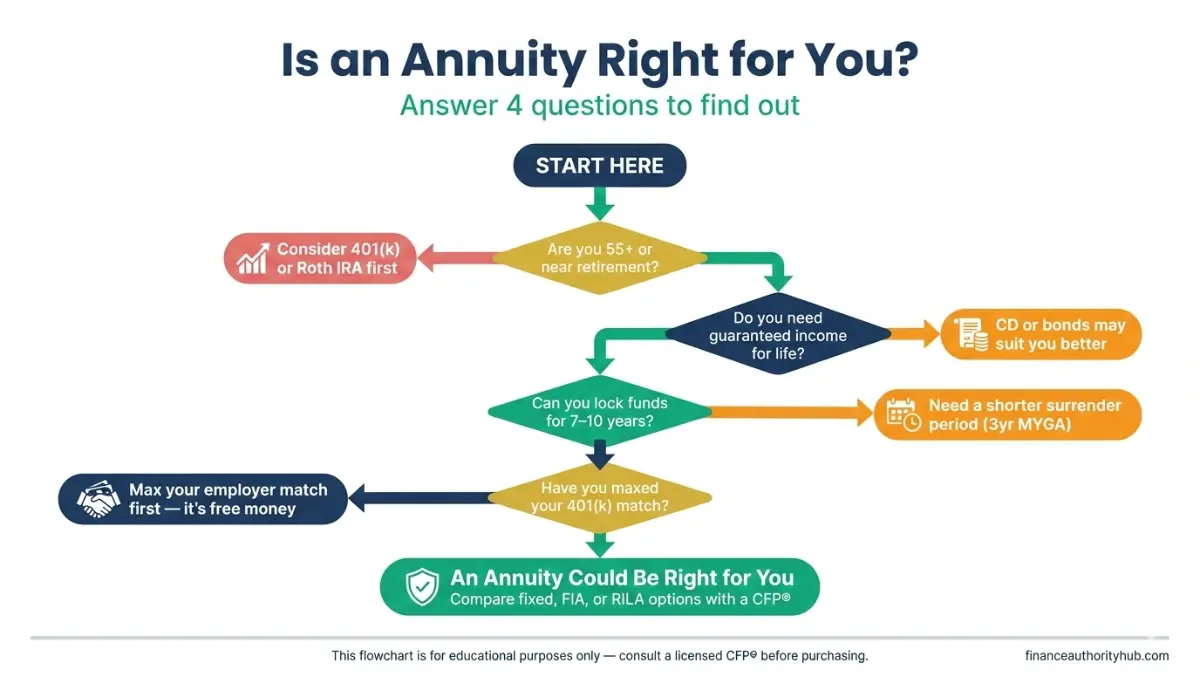

Who Should Buy an Annuity?

- ✅ Retirees with no pension who need a guaranteed income floor

- ✅ High earners who have already maxed out their 401(k) and IRA contributions

- ✅ Risk-averse investors who cannot stomach market volatility near or in retirement

- ✅ People aged 55–70 who are worried about outliving their savings

- ✅ Those looking to leave a guaranteed death benefit for a spouse or dependent

Who Should NOT Buy an Annuity?

- ❌ Anyone who needs liquidity in the next 3–10 years

- ❌ People with significant high-interest debt — pay that down first

- ❌ Younger investors (under 45) who have time to grow wealth in lower-cost vehicles like Roth IRAs or index funds vs. mutual funds

- ❌ Anyone who doesn’t understand the surrender schedule in the contract

Annuity vs. 401(k) vs. IRA vs. CD — The 2026 Showdown

One of the most searched questions about retirement planning: “Is an annuity better than a 401(k)?” The answer is nuanced — and the wrong choice costs tens of thousands of dollars.

Master Comparison Table: Annuity vs. 401(k) vs. Roth IRA vs. CD (2026)

| Feature | Annuity | 401(k) | Roth IRA | CD |

|---|---|---|---|---|

| Tax Treatment | Tax-deferred (non-qualified) | Pre-tax contributions | After-tax; tax-free growth | Taxable interest |

| Contribution Limit | No limit | $23,500/yr (2026) | $7,000/yr (2026) | No limit |

| Guaranteed Income for Life | ✅ Yes | ❌ No | ❌ No | ❌ No |

| Principal Protection | Yes (fixed/FIA) | No | No | Yes (FDIC) |

| Employer Match | ❌ No | ✅ Yes | ❌ No | ❌ No |

| Early Withdrawal Penalty | 10% IRS + surrender | 10% before 59½ | 10% on earnings | Varies |

| Best For | Guaranteed income floor | Employer match + growth | Tax-free retirement income | Short-term safe savings |

When an Annuity Beats a CD (2026 Scenario)

A 5-year MYGA annuity at 6.50% vs. the best 5-year CD at approximately 4.90% means:

- On $200,000, the MYGA earns approximately $13,800 more over 5 years — on a guaranteed basis

- Annuity growth is tax-deferred; CD interest is taxed annually, reducing effective yield further

The gap widens significantly in higher tax brackets. For investors in the 24–32% federal bracket, the tax deferral advantage of a MYGA can add an additional $5,000–$12,000 in real value over 5 years.

When a 401(k) or IRA Wins

Always maximize your employer 401(k) match first — that is a guaranteed 50–100% return on your contribution that no annuity can match. After capturing the full match, explore whether to prioritize your 401(k) vs. IRA before considering an annuity.

The Hybrid Retirement Strategy (What Top Financial Planners Actually Use)

Most certified financial planners do not recommend choosing between a 401(k) and an annuity — they recommend both in a tiered structure:

- Tier 1 (Income Floor): Annuity — covers essential expenses (housing, food, healthcare)

- Tier 2 (Growth): 401(k) + IRA — grows for discretionary spending and legacy

- Tier 3 (Liquidity): Emergency fund + CD/HYSA — accessible cash for unexpected needs

If you are currently modeling your retirement timeline alongside a mortgage, our mortgage calculator can help you visualize how your home payoff date aligns with your annuity income start date.

How to Buy an Annuity in 2026 — Step-by-Step Guide

Buying an annuity is not like buying a stock. It is a long-term insurance contract with legal consequences. Here is exactly how to do it correctly.

6-Step Annuity Buying Checklist (2026)

Step 1 — Define Your Income Goal Calculate how much monthly income you need in retirement beyond Social Security. This number determines your required annuity premium.

Step 2 — Choose Your Annuity Type Use the comparison table in Section 2. Match the product to your risk tolerance:

- Conservative → Fixed MYGA

- Balanced → FIA

- Growth-oriented → RILA

- Immediate income → SPIA

Step 3 — Check Insurer Financial Strength Ratings Only consider insurers rated A- or better by AM Best. Leading carriers in 2026 include Athene (A+), MassMutual (A++), Allianz (A+), and New York Life (A++).

Step 4 — Compare Rates from at Least 3 Carriers Rates vary dramatically. A 0.50% difference in a 10-year MYGA on $250,000 equals approximately $13,500 in additional guaranteed interest.

Step 5 — Review the Surrender Schedule and Fee Structure

- Surrender periods typically range from 3 to 10 years

- Surrender charges start high (7–10%) and decrease annually

- Riders (income riders, long-term care riders) add value but increase cost

Step 6 — Use Your Free-Look Period Most states require a 10–30 day free-look period after signing. If you change your mind, you can cancel for a full refund. Never skip reading the full contract.

Bold Callout: The National Council on Aging (NCOA) recommends working with a fee-only fiduciary financial advisor — not a commission-based insurance agent — when evaluating annuity options. A commission-based agent earns up to 10% of your premium for every contract sold.

Planning your full retirement picture means understanding how multiple income streams work together. Our deep-dive guide on 401(k) explained: avoid leaving free money behind covers how to maximize employer contributions before allocating to an annuity.

Frequently Asked Questions About Annuities

1. What is an annuity in simple terms?

An annuity is a contract with an insurance company where you pay a sum of money and receive guaranteed income payments in return — either for a set period or for the rest of your life.

2. How does an annuity work?

You pay a premium (lump sum or installments). Your money grows during the accumulation phase. Then, during the distribution phase, the insurer pays you regular income based on the contract terms.

3. What are the 5 main types of annuities?

Fixed (MYGA), Fixed Indexed (FIA), Registered Index-Linked (RILA), Variable, and Immediate (SPIA). Each carries a different risk level, growth potential, and payout structure.

4. How much does a $100,000 annuity pay per month?

At age 65 in 2026, a $100,000 immediate annuity pays approximately $600–$660/month for life (male, life-only option). Women receive slightly less. Deferred annuities pay significantly more if you delay income to age 70 or beyond.

5. Can you lose money in an annuity?

In a fixed or fixed indexed annuity, no — your principal is contractually protected. In a variable annuity, yes — your sub-accounts are tied to market performance and can decline.

6. What is the biggest downside of an annuity?

Surrender charges and illiquidity. Most annuities lock your money for 7–10 years. Withdrawing beyond the free withdrawal amount (usually 10%/year) triggers significant penalty fees.

7. Is an annuity better than a 401(k)?

Not better — different. Always capture your full employer 401(k) match first (it’s a guaranteed return). An annuity complements a 401(k) by adding a guaranteed income floor that a 401(k) cannot provide.

8. How are annuities taxed?

Growth inside an annuity is tax-deferred. When you withdraw, earnings are taxed as ordinary income — not at the lower capital gains rate. Withdrawals before age 59½ trigger an additional 10% IRS penalty, per IRS Tax Topic 410.

9. What happens to an annuity when you die?

Depends on the contract. If you die during the accumulation phase, your beneficiary typically receives the greater of the account value or premiums paid. If you die during payout, a joint-life or period-certain option continues payments to a surviving spouse or beneficiary.

10. What is a RILA annuity?

A Registered Index-Linked Annuity (RILA) links returns to a market index while providing a buffer against losses (typically 10–20%). It offers higher upside than a FIA but partial downside exposure. RILA sales reached $79.6 billion in 2025, making it the fastest-growing annuity product in America.

11. At what age should you buy an annuity?

Most financial planners recommend ages 55–70 for the best combination of payout rates and retirement income timing. Buying too early (under 50) ties up money during peak earning and investing years. Buying too late (over 75) limits the compounding growth benefit.

⚠️ Disclaimer: This article is for educational and informational purposes only. It does not constitute financial, tax, investment, or legal advice. Annuity products, rates, and availability vary by state, insurer, and individual circumstances. Always consult a licensed Certified Financial Planner® (CFP®) or fee-only fiduciary advisor before making any annuity purchase decision. Tax rules referenced are based on current IRS guidance as of 2026 and are subject to change. Past performance and current rate data do not guarantee future results.

For more retirement and investment guidance, explore our full retirement savings by age guide and our deep analysis on capital gains tax 2026 rates to understand the full tax picture of your retirement income strategy.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.