Capital Gains Tax 2026: Rates, Loopholes & Save $12K

Understanding capital gains tax in 2026 could save you $12,000+. Learn current rates (0%-20%), legal reduction strategies, calculation methods, and special situations for stocks, real estate & crypto.

In This Article

Understanding capital gains tax in 2026 could save you thousands of dollars on your investment profits. Whether you’re selling stocks, real estate, or cryptocurrency, knowing the new rates and legal strategies can dramatically reduce your tax bill. This comprehensive guide breaks down everything you need to know about capital gains tax, from basic calculations to advanced wealth-preservation techniques.

What Is Capital Gains Tax?

Capital gains tax is a levy on the profit you make when selling an asset for more than you paid for it. The Internal Revenue Service (IRS) treats these profits as taxable income, though often at more favorable rates than ordinary income.

The tax only applies when you “realize” the gain by selling the asset. If you own stock that has doubled in value but haven’t sold it, you won’t owe capital gains tax yet. These unrealized gains only become taxable when you complete the sale.

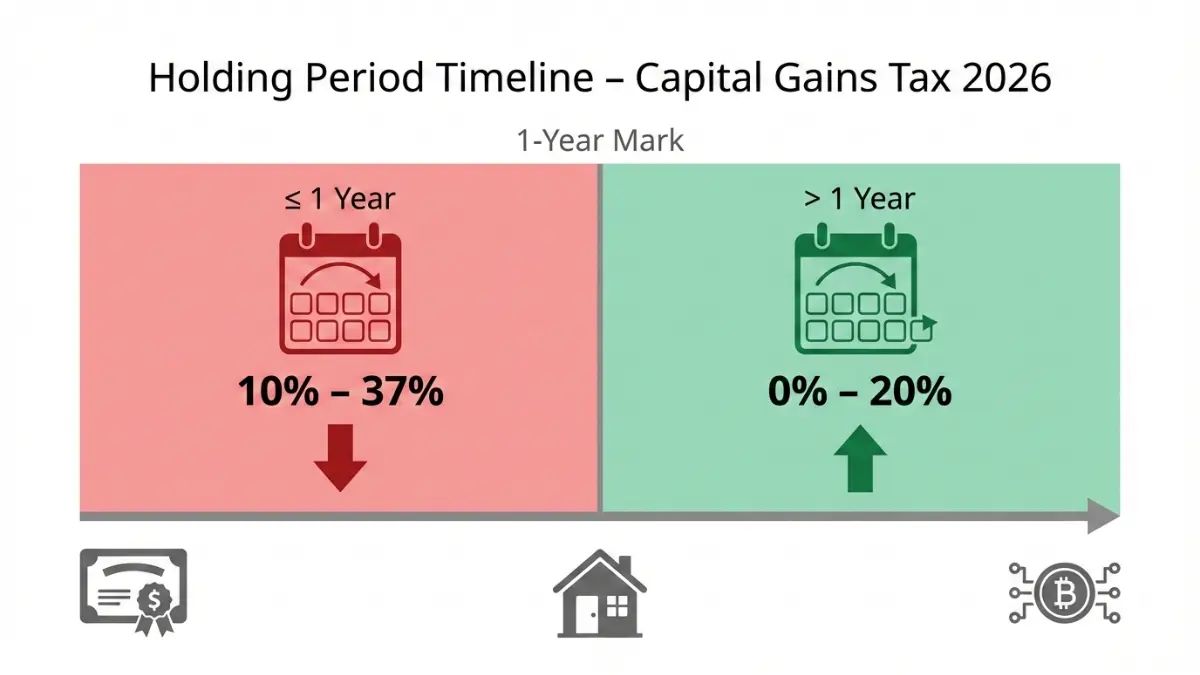

Long-Term vs Short-Term: The Critical Difference

The IRS categorizes capital gains into two distinct types based on how long you held the asset:

Long-term capital gains apply to assets held for more than one year. These benefit from preferential tax rates of 0%, 15%, or 20%, depending on your income level.

Short-term capital gains apply to assets held for one year or less. These are taxed as ordinary income at rates ranging from 10% to 37%.

| Type | Holding Period | Tax Rate | Example |

|---|---|---|---|

| Short-Term | ≤ 1 year | 10% – 37% | Stock bought May 2026, sold Dec 2026 |

| Long-Term | > 1 year | 0%, 15%, 20% | Stock bought Jan 2025, sold Feb 2026 |

The difference between these rates can be substantial. A $10,000 profit on a short-term investment could cost you $3,700 in taxes (at the 37% bracket), while the same long-term gain might only cost $2,000 (at 20%).

What Assets Trigger Capital Gains Tax?

According to the Tax Foundation, nearly everything you own qualifies as a capital asset:

- Stocks, bonds, and mutual funds

- Real estate (including rental properties)

- Cryptocurrency and NFTs

- Business interests and partnerships

- Collectibles like art, coins, and antiques

- Vehicles (though personal-use cars typically aren’t taxed)

Understanding these fundamentals is essential for anyone managing investments or planning major asset sales in 2026. The strategies you employ can make a difference of thousands of dollars in your final tax bill.

2026 Capital Gains Tax Rates & Brackets

The IRS has released updated capital gains tax brackets for 2026, reflecting inflation adjustments that could save you money compared to 2025.

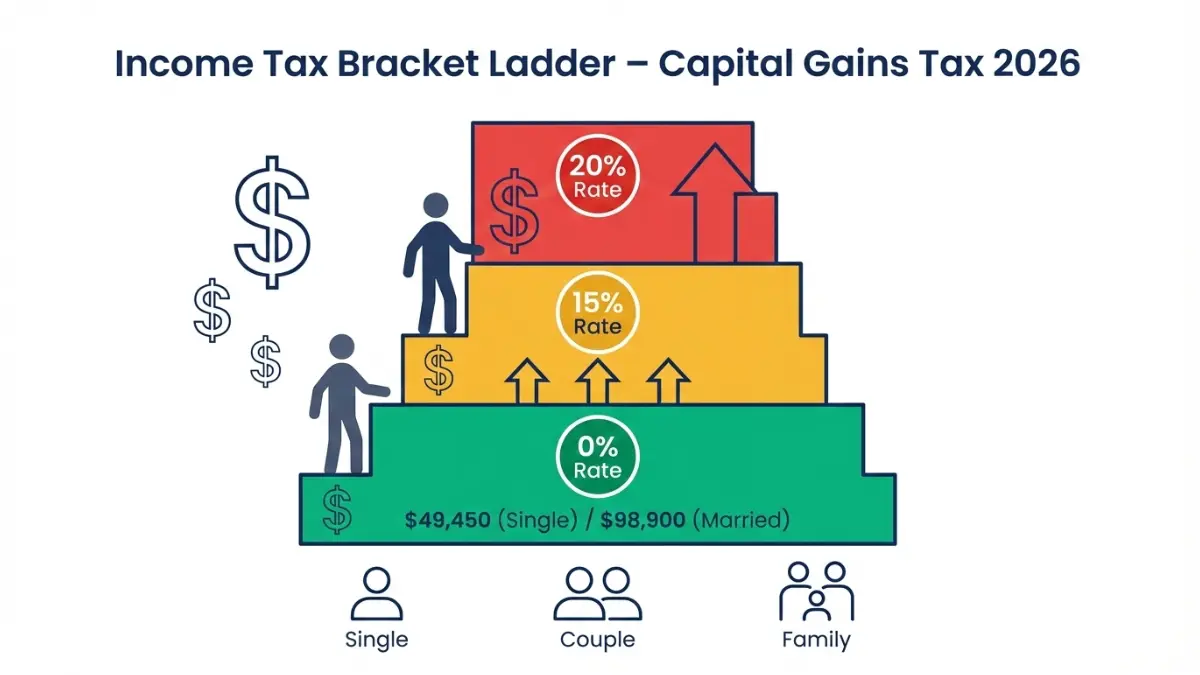

2026 Long-Term Capital Gains Rates

For assets held longer than one year, you’ll pay one of three rates based on your taxable income:

| Filing Status | 0% Rate | 15% Rate | 20% Rate |

|---|---|---|---|

| Single | Up to $49,450 | $49,451 – $545,500 | Above $545,500 |

| Married Filing Jointly | Up to $98,900 | $98,901 – $613,700 | Above $613,700 |

| Married Filing Separately | Up to $49,450 | $49,451 – $306,850 | Above $306,850 |

| Head of Household | Up to $66,250 | $66,251 – $579,600 | Above $579,600 |

Key 2026 Changes: The 0% threshold for married couples increased by $2,200 from 2025, while the 15% threshold jumped by over $13,600. These inflation adjustments mean more income can be taxed at lower rates.

Short-Term Capital Gains: Ordinary Income Rates

Short-term gains are taxed at the same rates as your regular income. For 2026, these federal tax brackets range from 10% to 37%.

| Tax Rate | Single | Married Filing Jointly |

|---|---|---|

| 10% | Up to $11,925 | Up to $23,850 |

| 12% | $11,926 – $48,475 | $23,851 – $96,950 |

| 22% | $48,476 – $103,350 | $96,951 – $206,700 |

| 24% | $103,351 – $197,300 | $206,701 – $394,600 |

| 32% | $197,301 – $250,525 | $394,601 – $501,050 |

| 35% | $250,526 – $626,350 | $501,051 – $751,600 |

| 37% | Above $626,350 | Above $751,600 |

Net Investment Income Tax (NIIT)

High-income earners face an additional 3.8% Medicare surtax on investment income. This Net Investment Income Tax applies when your modified adjusted gross income exceeds:

- $200,000 for single filers

- $250,000 for married filing jointly

- $125,000 for married filing separately

Example: A single filer earning $300,000 with $50,000 in long-term capital gains would pay 15% capital gains tax plus 3.8% NIIT, totaling 18.8%.

Special Capital Gains Rates

Certain assets face different maximum rates:

- Collectibles (art, coins, precious metals): 28% maximum

- Qualified small business stock: 28% on excluded portion

- Unrecaptured Section 1250 gain (real estate depreciation): 25% maximum

Understanding these rates is crucial for tax planning throughout 2026. Strategic timing of asset sales can help you stay within lower brackets and minimize your overall tax burden.

How to Calculate Your Capital Gains Tax

Calculating capital gains tax requires understanding your cost basis, sale price, and holding period. Here’s the step-by-step process used by tax professionals.

Step 1: Determine Your Cost Basis

Your cost basis is typically what you originally paid for the asset, plus certain adjustments:

- Purchase price

- Broker commissions and fees

- Improvements (for real estate)

- Reinvested dividends (for mutual funds)

Inherited assets receive a “step-up” basis to fair market value at the date of death, which can eliminate decades of capital gains.

Step 2: Calculate the Gain or Loss

The formula is straightforward: Sale Price – Cost Basis = Capital Gain

If the result is negative, you have a capital loss that can offset other gains.

Real Calculation Examples

Example 1: Stock Sale

- Bought 100 shares at $50 = $5,000 cost basis

- Paid $25 commission

- Total basis: $5,025

- Sold for $8,000 (after $25 commission)

- Capital gain: $8,000 – $5,025 = $2,975

If held over one year and you’re in the 15% bracket: $2,975 × 0.15 = $446.25 tax

Example 2: Real Estate Sale

- Purchased home: $300,000

- Improvements: $50,000

- Total basis: $350,000

- Sale price: $500,000

- Capital gain: $500,000 – $350,000 = $150,000

With primary residence exclusion ($250K single/$500K married), this gain may be completely tax-free.

Example 3: Cryptocurrency Sale

- Bought Bitcoin: $10,000

- Sold for: $25,000

- Capital gain: $15,000

If held less than one year and you’re in the 24% bracket: $15,000 × 0.24 = $3,600 tax

Reporting Your Capital Gains

The IRS requires reporting on specific forms:

- Form 8949: Lists each transaction with dates, proceeds, cost basis, and gain/loss

- Schedule D: Summarizes all capital gains and losses

- Attach to Form 1040 when filing your return

Many investors use tax software or work with professionals to ensure accurate reporting, especially when dealing with multiple transactions or complex situations like wash sales.

Cost Basis Methods for Stocks

If you bought shares at different times and prices, you can choose from several methods:

- First-In, First-Out (FIFO): Sells oldest shares first

- Specific Identification: Choose which shares to sell

- Average Cost: Used primarily for mutual funds

Specific identification gives you the most control, allowing you to sell high-basis shares first to minimize gains. However, you must identify the specific shares to your broker before the sale.

Understanding these calculations empowers you to make informed decisions about when and what to sell, potentially saving thousands in taxes through strategic planning.

7 Legal Strategies to Reduce Capital Gains Tax & Save $12K

Smart investors use legitimate tax strategies to minimize capital gains liability. These seven techniques can save you thousands of dollars while staying fully compliant with IRS regulations.

Strategy #1: Hold Assets for One Year or Longer

The simplest way to cut your tax bill is patience. Holding investments for more than 12 months qualifies you for long-term rates instead of ordinary income rates.

Real Savings: A $50,000 gain taxed at 37% (short-term) costs $18,500. The same gain at 15% (long-term) costs only $7,500—a savings of $11,000.

Strategy #2: Tax-Loss Harvesting

This powerful technique involves selling losing investments to offset gains from winners. You can deduct capital losses against capital gains dollar-for-dollar, and if losses exceed gains, you can deduct up to $3,000 against ordinary income annually.

Example: You sold stock A for a $15,000 gain. Before year-end, you sell stock B with a $10,000 loss. Your taxable gain drops to $5,000, saving you $1,500-$2,000 in taxes.

Important: The IRS wash sale rule prohibits buying the same or substantially identical security within 30 days before or after the sale. Violating this rule disallows the loss deduction.

Strategy #3: Primary Residence Exclusion

Homeowners get one of the biggest tax breaks available: up to $250,000 in gains tax-free for single filers ($500,000 for married couples) when selling a primary residence.

Requirements:

- Owned the home for at least 2 years

- Lived in it as your main home for at least 2 of the past 5 years

- Haven’t used the exclusion in the past 2 years

Example: You bought your home for $400,000 and sold it for $850,000. Your $450,000 gain is completely tax-free for married filers, saving approximately $67,500 in capital gains tax.

This exclusion can be used repeatedly throughout your lifetime, making it a cornerstone of wealth building through real estate investment strategies.

Strategy #4: Maximize the 0% Bracket

If your income falls below certain thresholds, you pay zero tax on long-term capital gains. For 2026, this means taxable income under $49,450 (single) or $98,900 (married).

Strategic Application: Retirees often have flexibility to control income year-to-year. By timing withdrawals from retirement accounts and realizing capital gains in low-income years, you can harvest gains tax-free.

Example: A retired couple with $80,000 in taxable income realizes $15,000 in long-term gains. They pay $0 in capital gains tax because their total income ($95,000) stays under the $98,900 threshold—a savings of $2,250.

Strategy #5: Donate Appreciated Assets to Charity

Instead of selling appreciated stock and donating cash, donate the stock directly to a qualified charity. You avoid capital gains tax entirely and can deduct the full fair market value.

Example: You own stock worth $20,000 with a $5,000 cost basis. Selling it would trigger $15,000 in gains and $2,250-$3,000 in taxes. Donating the stock directly saves this tax while giving you a $20,000 charitable deduction.

This strategy works particularly well with donor-advised funds, which provide immediate tax deductions while allowing you to distribute to charities over time.

Strategy #6: 1031 Exchange for Real Estate

Real estate investors can defer capital gains indefinitely using a 1031 like-kind exchange. This allows you to sell investment property and reinvest proceeds in similar property without paying immediate taxes.

Requirements:

- Both properties must be held for investment or business use

- Properties must be “like-kind” (most real estate qualifies)

- Must identify replacement property within 45 days

- Must close within 180 days

Example: You sell a rental property with a $200,000 gain. Instead of paying $30,000-$40,000 in taxes, you use a 1031 exchange to buy another rental, deferring all taxes. This strategy can be repeated indefinitely, preserving wealth for growth.

Strategy #7: Invest Through Tax-Advantaged Accounts

Retirement accounts like 401(k)s, IRAs, and Roth IRAs shelter your investments from capital gains tax. You can buy and sell within these accounts without triggering any immediate tax liability.

Traditional 401(k)/IRA: Contributions are tax-deductible, investments grow tax-deferred, and you pay ordinary income tax only upon withdrawal.

Roth IRA: Contributions are after-tax, but all growth and withdrawals are completely tax-free after age 59½ (with certain conditions met).

Example: You invest $10,000 that grows to $100,000 over 30 years in a Roth IRA. The $90,000 in gains escapes both capital gains tax and ordinary income tax—potentially saving $18,000-$27,000 compared to a taxable account.

Combined Strategy: The $12,000+ Savings Scenario

Here’s how these strategies work together:

- Tax-loss harvesting: Offset $20,000 in gains with $15,000 in losses = $750-$3,000 saved

- Hold for long-term rates: Save $5,500 on a $50,000 gain (37% vs 15%)

- Use 0% bracket strategically: Harvest $15,000 gains tax-free = $2,250 saved

- Donate appreciated stock: Avoid $3,000 in taxes on $20,000 donation

- Total estimated savings: $11,500-$13,750

By implementing these strategies consistently, disciplined investors can legally minimize their tax burden while building long-term wealth.

Special Situations & State Taxes

Beyond federal capital gains tax, several special circumstances require additional consideration for complete tax planning.

Cryptocurrency and NFT Capital Gains

The IRS treats cryptocurrency as property, not currency. This means every transaction—including trading one cryptocurrency for another—creates a taxable event.

Example: You bought Bitcoin for $15,000, then traded it for Ethereum when Bitcoin was worth $30,000. You owe capital gains tax on the $15,000 profit, even though you never converted to cash.

Detailed record-keeping is essential. You need to track:

- Purchase date and price for every cryptocurrency acquisition

- Sale date and price for every disposition

- Transaction fees (these add to cost basis)

The same rules apply to NFTs and other digital assets. If you’re actively trading, consider using specialized cryptocurrency tax software to maintain accurate records.

Inherited Assets and Step-Up in Basis

One of the most valuable tax benefits is the step-up in basis for inherited assets. When you inherit property, your cost basis “steps up” to the fair market value on the date of the original owner’s death.

Example: Your parent bought stock for $10,000 that’s now worth $100,000. If they sold it, they’d owe tax on $90,000 in gains. However, if you inherit it, your basis becomes $100,000. If you sell immediately for $100,000, you owe zero capital gains tax.

This provision makes inherited assets particularly tax-efficient and is a key reason wealthy families focus on estate planning rather than pre-death asset sales.

Gifts and Capital Gains

When you receive a gift, you inherit the donor’s cost basis and holding period. The annual gift exclusion for 2026 is $19,000 per recipient.

Example: Your parents gift you stock they bought for $5,000, now worth $25,000. Your basis is $5,000, not $25,000. When you sell, you’ll owe tax on gains above $5,000.

This differs significantly from inherited assets and makes gifting less tax-efficient than bequests for highly appreciated property.

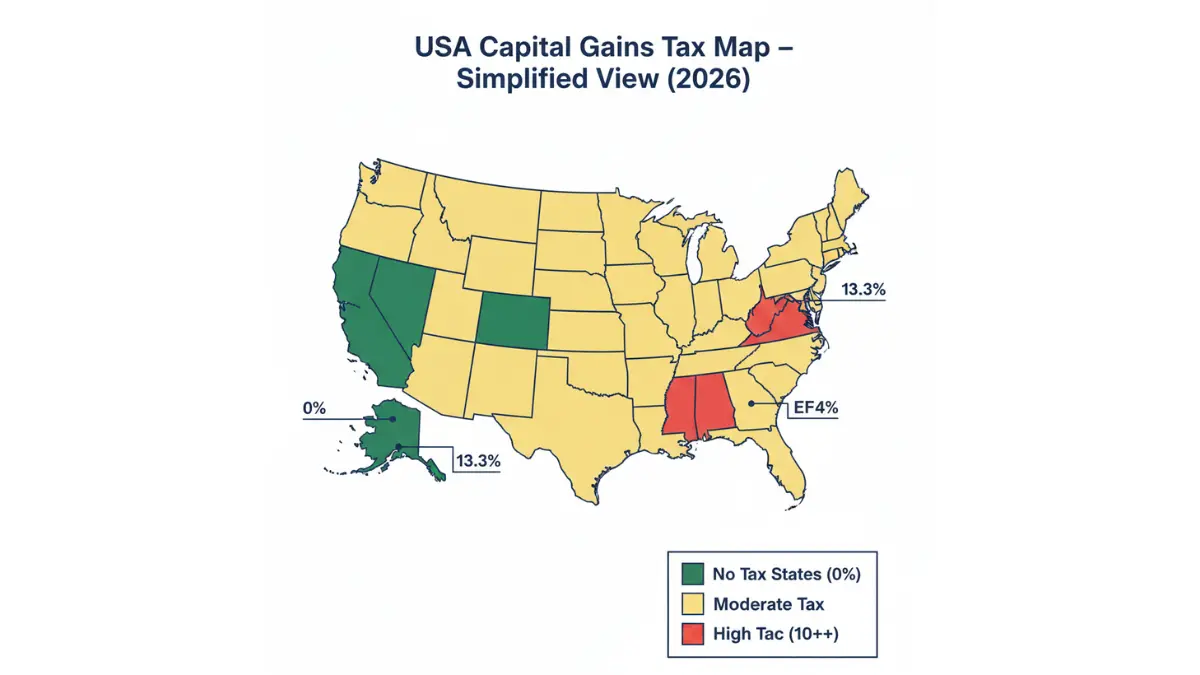

State Capital Gains Taxes

While federal rates get the most attention, state taxes can add substantially to your bill. Nine states have no income tax and therefore no capital gains tax:

States with NO Capital Gains Tax:

- Alaska

- Florida

- Nevada

- New Hampshire (dividends/interest only)

- South Dakota

- Tennessee

- Texas

- Washington (except 7% on high earners’ capital gains)

- Wyoming

High-Tax States for Capital Gains:

| State | Top Rate | Combined Federal + State |

|---|---|---|

| California | 13.3% | 33.3% (20% + 13.3%) |

| New York | 10.9% | 30.9% |

| New Jersey | 10.75% | 30.75% |

| Oregon | 9.9% | 29.9% |

| Minnesota | 9.85% | 29.85% |

For high earners in California, the effective capital gains rate including the 3.8% NIIT can reach 37.1%—nearly double the federal 20% rate alone.

Some investors consider strategic relocation before realizing large gains, though establishing legitimate residency requires careful planning and documentation.

Retirement Account Considerations

Capital gains inside retirement accounts receive special treatment:

Traditional 401(k)/IRA: No capital gains tax while funds remain in the account. All withdrawals are taxed as ordinary income, regardless of whether gains came from capital appreciation or dividends. Understanding 401(k) fundamentals helps maximize this benefit.

Roth IRA: No tax on any gains—ever—if you follow withdrawal rules. This makes Roth accounts ideal for your highest-growth investments.

Health Savings Account (HSA): Triple tax advantage—deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

Qualified Opportunity Zones

This newer provision allows investors to defer and potentially reduce capital gains by investing in designated economically distressed areas.

Benefits:

- Defer tax on gains until December 31, 2026 (or when QOZ investment is sold, if earlier)

- Reduce taxable gain by 10% if held 5+ years

- Pay zero tax on QOZ investment appreciation if held 10+ years

This complex strategy requires careful evaluation but can provide substantial benefits for the right investor.

What This Means For You

Understanding these special situations prevents costly mistakes and reveals opportunities. Whether you’re trading cryptocurrency, inheriting assets, or planning a move to a different state, factoring in capital gains implications helps you make financially sound decisions.

For complex situations involving multiple states, significant cryptocurrency holdings, or large inheritances, consulting a qualified tax professional ensures you’re maximizing benefits while maintaining compliance.

Frequently Asked Questions

1. Do I pay capital gains tax if I don’t sell my investments?

No. Capital gains tax only applies when you sell and “realize” the gain. Unrealized gains in your portfolio aren’t taxed, which is why buy-and-hold investing offers significant tax advantages.

2. What is the holding period for long-term capital gains?

You must hold an asset for more than 12 months. If you buy on January 1, 2026, you must hold until at least January 2, 2027 to qualify for long-term rates. Exactly one year counts as short-term.

3. Can I offset capital gains with capital losses?

Yes. You can offset capital gains with losses dollar-for-dollar. If losses exceed gains, you can deduct up to $3,000 against ordinary income annually, carrying forward any excess to future years.

4. How much is capital gains tax on $100,000 profit?

It depends on your total taxable income and holding period. At the 0% bracket: $0. At 15%: $15,000. At 20%: $20,000. Plus potentially 3.8% NIIT for high earners. Short-term gains could cost $10,000-$37,000 depending on your tax bracket.

5. Do capital gains count as income?

Yes, for tax purposes. Capital gains are added to your taxable income, which determines your tax bracket. However, long-term capital gains are taxed at preferential rates, not ordinary income rates.

6. What is the 2026 0% capital gains threshold?

Single filers with taxable income up to $49,450 pay 0% on long-term capital gains. Married filing jointly: $98,900. Head of household: $66,250. These thresholds increased from 2025 due to inflation adjustments.

7. Are capital gains taxed twice?

Stock gains can face double taxation—corporations pay tax on profits, then shareholders pay capital gains tax when selling appreciated shares. This is a major argument for lower capital gains rates.

8. How do I report capital gains on my tax return?

Use Form 8949 to list each transaction, then summarize on Schedule D. Both forms attach to your Form 1040. Most tax software handles this automatically, or you can work with a tax professional for complex situations.

9. Can I avoid capital gains tax on my home sale?

Yes, up to $250,000 for single filers ($500,000 married) using the primary residence exclusion. You must have owned and lived in the home for at least 2 of the past 5 years. This is one of the most valuable tax breaks available.

10. What is the Net Investment Income Tax (NIIT)?

The NIIT is an additional 3.8% tax on investment income (including capital gains) for high earners. It applies when modified adjusted gross income exceeds $200,000 (single) or $250,000 (married filing jointly).

11. When is capital gains tax due?

Capital gains tax is due when you file your annual tax return, typically April 15. For gains realized in 2026, you’ll pay when filing your 2026 return in early 2027. Estimated tax payments may be required quarterly if you have substantial gains.

Conclusion: Take Control of Your Capital Gains Tax

Understanding capital gains tax in 2026 puts powerful wealth-building tools in your hands. The difference between short-term and long-term rates alone can save thousands of dollars. Combined with strategic techniques like tax-loss harvesting, maximizing the 0% bracket, and utilizing the primary residence exclusion, disciplined investors can legally minimize their tax burden by $12,000 or more.

Key Takeaways:

- Hold investments longer than one year to access preferential long-term rates

- Use tax-loss harvesting to offset gains with losses

- Take advantage of the 0% capital gains bracket when possible

- Leverage the $250K/$500K home sale exclusion

- Consider state taxes when planning large asset sales

- Maximize tax-advantaged accounts like Roth IRAs and 401(k)s

Next Steps:

Review your current investment portfolio and identify opportunities to implement these strategies. If you’re planning significant asset sales in 2026, calculate your potential tax liability using the updated brackets. For complex situations, consult with a qualified tax professional who can tailor strategies to your specific circumstances.

Explore additional resources on Finance Authority Hub to continue building your financial knowledge. Our tax planning tools and comprehensive guides provide the information you need to make informed decisions throughout 2026 and beyond.

Disclaimer: This article is for educational purposes only and does not constitute financial, tax, or legal advice. Tax laws change frequently, and individual circumstances vary significantly. Consult a qualified tax professional, CPA, or financial advisor before making investment decisions or implementing tax strategies. The information presented reflects tax law as of February 2026 and may not reflect subsequent changes. Always verify current regulations with the IRS or a licensed tax professional before taking action.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.